What are assets and liabilities

Assets are what generate income. Buildings, apartments, cars, money in accounts, etc., if they work and make a profit. On the contrary, liabilities are expenses that ensure the operation of the enterprise. The relationship between expenses and income is reflected in the balance sheet. This is perhaps the most difficult and important subject in accounting to understand.

Difference between liabilities and assets

A simple and ingenious example is shown in the cartoon “Three from Prostokvashino”. Remember?

The cow was rented. She gives milk - this is an asset. She also calved. The rent for it is a liability. We bought a cow and a calf and reduced our liabilities. There was one animal, now there are two. Both will be profitable. By the way, a ready-made version of the business model! But this is so, schematically. Let me look at the problem deeper.

Are own shares an asset or a liability?

There is an opinion that if a company can sell its securities and get money for them, then these are assets. Not certainly in that way. The result of the sale will indeed be the proceeds. They can be used for different purposes. And the shares themselves are a liability. They act as a mechanism for obtaining funds.

Interaction of assets and liabilities

Here is an everyday example: a citizen bought a car to go to work and to his dacha. Here he acquired a liability. The car immediately lost value because... It became used and requires expenses for refueling, repairs, storage, etc. Then this man decided to work on his car, receiving a fee for it. Then the car becomes a core asset. With its help, a person makes a profit. At enterprises the situation looks similar.

Assets and liabilities in financial statements

These are the main indicators that allow you to almost completely evaluate the activities of the enterprise. They are correlated with each other and are reflected in the form of a table. Simply put, these are items in the general balance sheet – the enterprise’s report for a certain period of time.

Assets and liabilities according to Kiyosaki

This gentleman has published 26 books on financial topics. His brilliant work “Rich Dad Poor Dad”, along with other works, is sold all over the world.

The writer’s main thesis can be formulated as follows: “Assets bring you money, whether you work or not. Liabilities take your money, whether you work or not.”

Of course, these are the basics of economics “for dummies.” This approach is too simplistic and controversial. However, in everyday life this is quite acceptable. It's more difficult with companies. Judge for yourself.

Nuances of accounting for search assets

General accounting rules also apply to exploration assets (PBU 24/2011). Tangible search assets are accounted for in the same way as fixed assets, while intangible ones are accounted for in the same way as other non-search intangible assets. For them, the PBU provides special subaccounts of account 08 “Investments in non-current assets”. If there are several plots of land under study, you need to open a separate sub-account for each of them.

Recognition of search assets

These assets are recognized as a separate section of accounting when the organization has a license for this type of activity.

REMINDER! The license itself is an intangible search asset.

The assessment is based on the funds actually spent on a particular asset. The initial accounting of a prospecting asset is maintained using the following entries:

- debit 08 “Investments in non-current assets”, subaccount “Investments in exploration assets”, credit 10 “Materials” (20, 23, 60, 69, 70, etc.) – the initial cost of the exploration asset has been formed;

- debit 08, subaccount “Tangible exploration assets” (or “Intangible”) - this asset is taken onto the balance sheet.

Depreciation of exploration assets

It occurs in the same way as depreciation of fixed assets or intangible assets. It is recommended to open a special subaccount for account 02 “Depreciation”.

FOR YOUR INFORMATION! The useful life of a search asset of any group is determined by the organization itself and fixed in its accounting policies.

The wiring will look like this:

debit 23 “Auxiliary production”, subaccount “Expenses for ordinary activities”, credit 02 “Depreciation of fixed assets”, subaccount “Depreciation of exploration assets” - depreciation of exploration assets.

IMPORTANT RULE! If an asset was first used on one plot of land and then transferred to another, then depreciation on it must be recorded against the creation of a new asset on the next plot of land. This type of accounting is typical for all cases where one asset was used to create other assets.

Write-off of search assets

Exploration assets of both groups must “leave” the accounting records if a positive or negative result of exploration and appraisal work is achieved:

- a decision has been made on the commercial feasibility of production;

- its economic futility has been proven.

Both results are search assets and are presented in accordance with the established form.

If mining is profitable, then exploration assets are automatically “transformed” into fixed assets at their residual value by the following posting:

- debit 02 “Depreciation of fixed assets”, subaccount “Depreciation of exploration assets”, credit 08, subaccount “Tangible or intangible exploration assets” - depreciation of exploration assets is written off to reduce the original cost;

- debit 01 “Fixed assets” (04 “Intangible assets”), credit 08, subaccount “Tangible or intangible exploration assets” – transfer of exploration assets to fixed assets and intangible assets.

If production turns out to be unpromising, the costs turn out to be a negative financial result, so they are written off:

debit 91 “Other expenses”, sub-account “Unpromising production”, credit 08, sub-account “Tangible or intangible exploration assets” - write-off of the exploration asset.

The depreciation or disposal of a prospecting asset is accounted for in the same way.

Kinds

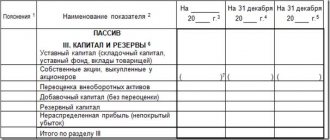

I will present the balance sheet of the organization in the form of a table.

| Assets | Liabilities |

| Negotiable. Money or goods to be sold within a year. | Equity. It is formed from the money of the founders. It turns out that the company, as it were, borrows money and is obliged to return it to the owner. Conditionally, of course. But since it must, it means a liability. |

| Non-negotiable. What the company is not going to sell: land, buildings, machines, vehicles, long-term investments, etc. | Securing future payments. |

| Future expenses. Expenses carried over to the next period after the reporting period. Example: car insurance for 2 years. Payment for the second year of the insurance policy, in this year’s report, will be reflected in the “Assets” column. | Long term duties. Own shares, bonds, mortgages, leasing, loans, etc. |

| Revenue of the future periods. Something for which money has already been received, but services or supplies will be made next year. | Current expenses (liabilities). |

Assessment of bioactives

Directly related to tracking the results of biotransformation.

Assessment of a bioactive – recording changes in its various indicators:

- by quantity (number, area, offspring, weight, length, etc.);

- by quality (fiber strength, fat content, etc.).

Performed at the time of initial recognition and subsequently according to reporting periods.

Upon first recognition and capitalization and subsequent accounting, a biological asset is measured at its fair value as of the valuation date, from which estimated sales costs are deducted (clause 12 of IFRS 41). A fair valuation is the amount of money that knowledgeable, independent parties would be willing to pay for a given asset. Distribution costs include various duties, exchange fees, taxes associated with the transfer of property, commissions if the services of dealers and brokers were used.

ATTENTION! Transport costs, according to IFRS 41, are not included in sales

How to fairly evaluate a biological asset

For fair assessment, bioactives are divided into groups according to various indicators, for example, the number of livestock of the same age, breed, etc. is assessed. There is an objective difficulty associated with the relevance of assessment only at the time of assessment. Due to biotransformation and other factors, the value of an asset may change significantly. Here are the ways in which this point is resolved in modern practice:

- Active market position. If the valued biological fund is traded on the market where it is expected to be sold, then the fair value will be the quoted price for this asset.

- Last deal. If there is no active market, the price of the last transaction in any market is considered fair, unless significant market shocks have occurred between then and the end of the reporting period.

- Adjustment of prices for analogues. Prices for similar assets are considered and adjusted depending on the degree of difference from the valued one.

- Industry indicators. Average price for the relevant sector.

- Discounted cost. The fair value of a bioasset is the expected amount of cash flows taking into account the discount factor. Factors of biotransformation of the asset are not taken into account.

- Cost price. In some cases, it is almost identical to a fair assessment, for example, if after investment of funds biotransformation does not have time to occur (for example, the field is sown just before the registration date) or it will not yet have an impact on the price (for example, one-year-old seedlings that are designed to bear fruit at the age of 5 years).

Fair value reconciliation

The company must choose the bioasset valuation method that guarantees greater reliability, and it must be applied until the asset is disposed of. Since any assessment method involves an error, the balance sheet needs to be reconciled: compare the indicators at the beginning and end of the reporting period. This takes into account:

- income or costs or losses relative to fair value;

- increase in value due to acquisition of assets;

- its decrease due to the sale of assets;

- reduction in book value due to harvesting, cutting, etc. (that is, temporary separation of the economically useful part of the bioactive);

- income from business combinations;

- exchange rate jumps in quotes, etc.

What to do with liabilities and assets

Mr. Kiyosaki speaks out clearly on this matter: get rid of the former and accumulate the latter. By the way, this approach causes criticism against him. According to the guru, I should sell my car because it is not generating income. Dacha - for the same reason. Yes, a lot more.

On the other hand, if I earn less than I pay for the maintenance of my liabilities, then sooner or later I will lose them anyway. Therefore, in my opinion, it can be formulated this way: maximize your income-generating property, reducing expenses to reasonable limits. This is exactly what successful companies do.

What are the net assets of an enterprise (NA)

The company has its own funds, which can be valued in money. There are also debt obligations. The difference between the first and second shows the enterprise's NA.

CA and legislation

Order No. 84n of the Ministry of Finance of the Russian Federation dated August 28, 2014 approves their definition. Net assets are all the assets of the organization (JSC), with the exception of the receivables of the founders in the authorized capital.

Debt obligations (DL) are all debts of an enterprise, excluding income that will be received in a future period. Assistance from the state or property received free of charge is not taken into account.

Calculation formula

NA = AO – DO. Property that is in the temporary use of an enterprise is not taken into account when determining the NA.

How are the assets and liabilities of the balance sheet formed?

The basic rule for drawing up a company's balance sheet: the indicators must be equal to each other. For example, a company took out a loan for 500 thousand rubles. This money is reflected in the asset column. At the same time, they are entered into liabilities as debt of the enterprise.

Basic rules for accounting for non-productive assets

To account for non-productive assets, you need to create a set of analytical accounts. They are opened for account 010300000. Let's look at some of the accounts included in the group:

- 010311000 – land plot.

- 010312000 – subsoil resources.

- 010313000 – other ON.

NAs are accounted for using one code. They are treated as real estate. The accounting unit is an inventory object.

Instruction No. 174n stipulates the options for admission of NA to the organization:

- Purchase. If objects are purchased, they must be accounted for at their original cost. The latter is recorded on account 010613330. You also need to display the increase in the cost of items. The value of objects will increase if measures are taken to improve them.

- Transfer of an object from the head office or divisions. The transfer is carried out on the basis of operational management. It is possible as part of the reorganization. In this case, the initial cost is not formed. Capitalization is carried out by debit and credit.

- Detection of surplus after inventory. The item must be recorded at market price.

When accounting, the accounts whose numbers are given above are used.

FOR YOUR INFORMATION! The accounting procedure is specified in Instruction No. 157n. In 2014, changes were made to this document. At the moment, the land needs to be recorded in the balance sheet. Previously, objects were taken into account off the balance sheet. However, no corresponding adjustments have been made to Instruction No. 174n

For this reason, when taking into account the cadastral value of objects, it is necessary to take into account the Methodological recommendations given in the letter of the Ministry of Finance dated December 19, 2014

Net assets of the enterprise: interpretation

A positive NA indicator of an enterprise indicates the efficiency of its work. This indicator is taken into account by investors when making decisions about purchasing securities, and by banks when making lending decisions.

On the other hand, young enterprises may have a negative NAV but not be unprofitable. Therefore, these figures should be studied over time.

Calculation example

LLC "Mechta Agraria" produces household equipment. The annual balance sheet is as follows: non-current assets (residual value of fixed assets, contributions to construction, long-term investments) - 16,000,00 rubles. Current assets (own funds, debts of third parties, inventories of goods) – 800,000 rubles.

Balance sheet liabilities: loans – 400,000 rubles, current expenses – 700,000 rubles.

NA = 1,600,000 + 800,000 – 400,000 – 700,000 = 1,200,000 rub.

Balance sheet codes and lines

The balance sheet is compiled according to a certain algorithm. There is a separate line for each indicator. Lines are assigned individual codes for ease of statistical accounting and control.

Each line expresses a cost indicator showing the operation of the enterprise. Modern codes are displayed as a four-digit number, with each digit containing specific information.

So, for example, line 1150 (fixed assets) is deciphered as follows: 1 – type of document (in this case, balance sheet); 1 – non-current assets; 5 – type of asset; 0 – line-by-line detailing of indicators.

Non-core assets are also displayed by the accounting department in the balance sheet of the enterprise.

Diagnostics of business efficiency using the net asset method

One of the main conditions for the prosperity of an enterprise is the constant search for opportunities to increase the number of assets. A negative value of this indicator may indicate that the company is unprofitable, insolvent, and exists on the money of creditors. In this case, the company may be liquidated through court proceedings.

Non-core assets

There is one more column in the accounting and financial statements, which is also required to be filled out and can provide certain information about the current activities of the enterprise - the volume of non-core assets. Essentially, this concept describes any property of a company, joint stock company or business association that is not currently used to generate income. These may even include facilities such as kindergartens and clinics - this is an echo of the first wave of privatization that occurred in the decade before last.

There is also a scenario in which non-core assets arose due to a change in the orientation of the enterprise: due to the closure of production lines, choice in favor of another market segment, re-profiling. As practice shows, the most appropriate is the transfer or sale of non-core assets, but the law does not oblige joint stock companies and companies to do this. The fact is that long-term maintenance of such objects leads the company to losses, adding to the number of expense items.

As a result, the company's assets are those objects that are used to generate profit from business activities. Also included here is property that can be used for these purposes, but has not been exploited until now.

Top

Write your question in the form below

Valuation of assets on the balance sheet

This approach uses company reports. This is necessary to determine the value of property, both tangible and intangible, as well as existing liabilities. Along with market valuation and revenue assessment, it helps create a holistic picture of the company's performance.

Cost and average value of total assets

The sum of current and non-current assets shows the value of the company's total assets. In simple words: if we add up these indicators at the beginning and end of the year and divide by 2, we get the average total assets of the organization for the year. This data is needed to assess the dynamics of enterprise development.

Real assets ratio

Characterizes the potential of the company's activities. It is calculated from the sum of the residual value of fixed assets, raw materials, materials, intangible assets, and work in progress. The result obtained must be divided by the value of the organization’s property.

It looks like this: Kr.a = page 100 + page 120 + page 211 + page 213 / page 300 balance. For an enterprise engaged in production, this coefficient must exceed 0.5. A decrease in the coefficient shows a negative trend in the subject’s activity, an increase – a positive one.

Asset immobilization ratio

Share of non-current assets in the balance sheet. Characterizes the degree of liquidity of the enterprise’s property and the ability to meet its obligations.

Permanent Balance Index Ratio

Shows how financially stable and solvent the company is, regardless of the funds raised. It is calculated by the ratio of non-current assets (line 1100) to the equity capital indicator (line 1300).

These, and a number of other ratios that reflect the company’s performance, are very carefully assessed by professional investors. Making a decision to purchase securities should not be based solely on intuition or the opinions of third-party experts. You need to carefully study all the indicators.

I hope this article was helpful to you. Subscribe to our news, share them with friends on social networks. All the best.

How to determine the value of non-produced assets

The tax base for non-productive assets, based on Article 391 of the Tax Code of the Russian Federation, is the cadastral value as of January 1 of the reporting year. The basis must be determined for each site. That is, to calculate taxes, you can use the information provided in accounting. No additional adjustments are made in this case. Based on the Constitution and a number of laws, natural resources are in national ownership. They cannot be alienated in favor of other persons. For this reason, it is impossible to evaluate them at market value.

The procedure for determining the initial cost of non-produced assets is the same as the similar procedure for fixed assets and intangible assets. Expenses for the purchase of assets must be recorded in an account related to capital investments. After the initial cost has been formed, the resulting amounts must be written off to analytical accounts. The list of expenses that are included in the initial cost when purchasing or improving assets is set out in paragraph 72 of Instruction No. 157n.