What is the best RKO - in Word or other format

The cash receipt form can be presented in 2 main formats - Word and Excel.

Each of them has its own advantages and disadvantages. Word documents open in a larger number of programs - in common operating systems (Windows, Linux, MacOS), as a rule, there is always pre-installed software that can work with files of the corresponding format.

Relatively few solutions work correctly with Excel files - Microsoft Excel, Open Office Calc and their analogues, including “cloud” types of software. As a rule, they are not installed by default in modern operating systems.

If you have solved the cash receipt order in Excel format, then you will have a more universal file at your disposal. For example, when it is created in one version of Microsoft Excel, it can be recognized without problems in any other, and in most cases also in third-party programs. While Word files, due to the peculiarities of their structure, are not always correctly recognized in programs other than those in which they were created.

Another argument for using RKO in Excel is the convenience of filling it out on a computer. The structure of files of this type is such that it is more difficult for an accountant to make a mistake when filling out the necessary data on a PC, since the cells for entering information are highlighted. When filling out a Word document, there is a possibility of mistakenly affecting other elements of the document formatting, as a result of which its structure may be disrupted.

What unified form should the RKO form correspond to?

In accordance with the provisions of Bank of Russia Directive No. 3210-U dated March 11, 2014, Russian organizations are required to use the unified form KO-2 (corresponding to OKUD number 0310002) as a RKO form. This form was approved by Decree of the State Statistics Committee of the Russian Federation dated August 18, 1998 No. 88.

Read more about the legal requirements for primary documents in the article “Primary document: requirements for the form and the consequences of its violation .

NOTE! As of August 19, 2017, new rules for conducting cash transactions are in effect, which you can read here.

How RKO is free

You can download the expense cash order in form KO-2, that is, its structure fully complies with the requirements of the law, on our website using the link below:

NOTE! It is important not only to download the current RKO form in one of the presented formats, but also to make sure that the file does not have a “read-only” attribute (otherwise it will not be possible to edit it on a PC). To do this, you need to find it on the disk, right-click on it, select “Properties” and, if necessary, uncheck the corresponding attribute.

Downloading the cash receipt order is only half the battle; the next task will arise - to fill it out correctly. Let's consider the key points of this procedure.

Do I need to print out the KO-2 cash order form?

Filling out the RKO can be done either on a computer - followed by printing, or manually - using an already printed form (clause 4.7 of instructions No. 3210-U). Automated solutions can also be used - in this case, printing out cash settlement orders is not necessary (order files are saved in the memory of the corresponding programs and signed using an electronic digital signature). True, in the latter case, the organization will have to buy electronic signatures for all persons who must sign on these documents: the manager, the chief accountant, the cashier, as well as other employees (including accountants).

A completed RKO sample may look like this, you can download it from the link below:

This completed sample cash receipt order can be used as a sample for the cashier of your organization.

What you should pay special attention to when filling out the cash receipt form:

- in the column “OKPO code” it is necessary to indicate data corresponding to what is contained in the state statistics registers;

- if the enterprise does not have structural divisions, then a dash must be placed in the corresponding column of the form;

- in the “Document number” column, the cash settlement number should be recorded in order; as a rule, calculation begins on January 1 of each year;

- the amount in the tabular part of the form can be indicated in rubles and kopecks, separated by a comma or hyphen (for example, 200.75 or 200-75);

- Data is entered into the “Purpose Code” item only if the organization in practice uses a system of codes that determines the expenditure and receipt of funds;

- in the “Amount” paragraph, which is located below the table, you should indicate the amount of funds issued under cash settlement services, in rubles - in words with a capital letter of the first word, in kopecks - in numbers;

- in the “Grounds” column you must indicate the content of the business transaction

- in the “Appendix” column, information is provided about the document that is the basis for conducting a cash transaction (for example, it could be a payroll when issuing salaries in cash), indicating the number and date of its preparation.

For more information about filling out a payroll sheet, read the article “Sample of filling out a payroll sheet T 49” .

If the cash register is filled out by an individual entrepreneur who does not hire cashiers, then the “Issue” column should contain his data. If the individual entrepreneur does not hire an accountant, only his signature as the head of the organization should be on the RKO.

To whom should RKO be issued when paying wages according to the payroll?

Since there are no clear rules in the Directive regarding how to formalize cash settlement settlement when issuing wages according to a statement, we will proceed from the general rules. They are like that. The salary slip has a validity period of maximum 5 working days. 6.5 Instructions. The director must indicate a specific period in the statement, based on how many days are needed to pay salaries to all employees (taking into account the established deadlines for paying salaries, current business trips, vacations, time off, etc.). During this period, the amount to be issued according to the statement may be kept in the cash register in excess of the limit. 2 Directions. And until this period expires or the entire salary is paid before the end of this period. 4.6, 6.5 Instructions:

- RKO is not issued either for the total amount indicated in the statement, or for the amounts already issued according to the statement from the beginning of its validity period;

- The cash book does not reflect either the money intended for issue or the money already issued according to the statement to employees.

At the end of the last day of validity of the statement, the cashier signs the statement, marks the deposited amounts on it and transfers it to the accounting department. The accountant checks everything and also signs. And only after this, but always on the same day, the accountant draws up cash settlements for the total amount actually issued to employees para. 3 p. 6.5 Instructions, and its number and date are indicated on the last page of the statement. Then the cashier registers the cash register in the cash book. 4.6 Instructions.

If there are several statements, for example, each department has its own, then it is not necessary to create a separate cash register for each of them. You can make one RKO for the total amount of the salary issued and attach all the statements to it. Accordingly, the number of this cash register must be indicated in all statements.

In a regular, non-salary cash settlement, the indication of the recipient and his passport data, as well as his signature para. 2, 3 clause 6.1, clause 6.2 Instructions are needed so that the organization has confirmation that it paid a certain amount to a certain person, and that person received it. And such a cash settlement is drawn up before the money is issued to the recipient indicated in it. 6.1 Instructions.

But at the time of compiling cash settlements based on the payroll:

- the money has already been issued from the cash register to the employees according to the statement, some of it, perhaps, in previous days;

- There is already confirmation of the payment of a certain amount to each person - these are the signatures of the employees on the statement.

Therefore, the RKO, compiled on the basis of the salary sheet, is needed only for making entries in the cash book about the amounts issued according to the sheet and is not confirmation of the transfer of money. This means entering someone’s f. And. O. in the “Issue” line and passport data in the “By ___” line is not required. Accordingly, no one should sign the RKO for the recipient. That is why the Instruction mentions filling out these lines only in relation to the general procedure for issuing money from cash registers. 6.1, 6.2 Instructions. And for the payment of wages, a special procedure has been established that we have considered, in which there are no such rules. 6.5 Instructions.

At the same time, in practice one can encounter other, erroneous, options for registering cash settlements:

- <or>on the cashier himself - his name. And. O. put in the “Issue” line, and in the “By ___” line indicate his passport details. The reasoning here is this: the cashier issues the salary according to the statement, therefore, the cash register must be issued in his name. This is incorrect, since all the money in the cash register, including that intended to pay salaries, is already with the cashier, because he is the person financially responsible for the cash register. A cash settlement can be issued for someone who works as a cashier only if he acts not as a cashier, but as a recipient of money. For example, as an accountable person, when he is tasked with purchasing something for cash on behalf of the organization.

It happens that an organization has several cashiers per cash register, one of whom is a senior cashier. 2 p. 4 Instructions, and the salary is issued as follows: the senior cashier transfers money from the cash register to the others, and they then distribute it to the employees according to the statements. But even in this case, the transfer of money between the senior cashier and the others is not formalized by cash register for the same reason: as long as one of the cashiers has the money, it is considered to be in the cash register. Such a transfer is recorded in a special book for recording funds accepted and issued by the cashier (form No. KO-5utv. Resolution of the State Statistics Committee dated August 18, 1998 No. 88) p. 4.5 Instructions;

- <or>to the director or chief accountant. The wording in the “Issue” line in these cases is as follows: “Fomin A.A. for the payment of wages to employees for the second half of June 2015”, and below, in the line “By ___”, Fomin’s passport details are indicated. This is incorrect, since with such registration it will turn out that you transferred this amount from the cash register to the named person, and he must distribute the salary to the employees somewhere else. But this in fact did not happen: the cashier issued the salary - it is his signature that appears on the statement in the line “Payment made.” Of course, the director can conduct cash transactions himself. 4 Instructions, but then he acts as a cashier, and for the cashier, as we have already said, cash registers are not drawn up.

In some organizations, the following order has been established: the director, chief accountant, head of department, foreman, and so on, according to the cash registers registered in their name, receive salaries for their subordinates at the cash desk, and then distribute them to employees according to the payroll. They return the unpaid amounts, together with the statement, to the cash desk according to the PKO. But it's not right. The salary must be issued from the cash register by the cashier - this is the requirement of Directive No. 3210-Uabz. 2 clause 6.5, clause 6.2, clause 4, clause 6.1 Instructions, that is, it cannot be issued through accountable persons.

Therefore, the one who actually issues the salary must be appointed cashier with full financial responsibility for the money entrusted to him. Then the main cashier will be the senior one at this time, and the transfer of salary money to the distributor must be recorded in the book of accounting for funds accepted and issued by the cashier (form No. KO-5utv. Resolution of the State Statistics Committee dated August 18, 1998 No. 88).

Innovations in the procedure for registering cash settlements for 2021 - 2021

Fortunately, there were no changes in the procedure for filling out cash registers in 2021 - 2021. They were there before. Thus, on August 19, 2017, the instruction of the Central Bank of the Russian Federation dated June 19, 2017 No. 4416-u came into force, which introduced a number of changes to the procedure for filling out and issuing cash receipts:

- The cashier has the right to draw up one cash settlement at the end of the working day for the entire amount issued during the day from the cash register, but provided that there are fiscal documents from the online cash register for the money issued.

- The cashier is obliged to check whether there are signatures of the chief accountant and accountant or director on the cash register, but signatures are now checked against samples only if the document was drawn up on paper.

- If the cash settlement is issued in electronic form, then the recipient of the money has the right to put his electronic signature on the document.

- You can issue money on account by order of the director; now it is not necessary to ask for an application from the accountable person. However, the chosen procedure for issuing funds (upon application or order) should be fixed in the Regulations on settlements with accountable persons.

- An employee’s debt on a previously received advance is no longer a reason for refusing a new issuance of accountable funds.

Read more about all changes in the procedure for issuing reports here.

If you have access to ConsultantPlus, check whether you are completing cash transactions correctly. If you don't have access, get a free trial of online legal access.

How to close a payroll form T-53?

The issuance of wages according to the payroll form T-53 is carried out within three days. The salary payment deadline is agreed upon with the bank.

The information that is provided after these calculations can be used to assemble a document for printing. This way, you already have a document ready for the employee to sign for receipt of the amount on the date it appears. You can also make a copy of this worksheet so you can then mock the tests and check the operation and calculation of each information.

Improving business management

This brings many benefits to the company, such as optimization of internal processes, integration between all sectors of the company, in addition to security and excellent value for money.

Main module features

Integration, generation, export and import of files. Advance Work Notice, Refund, and Request to Cease Termination. Insurance form. Inkjet and matrix termination form. Inkjet and dot matrix mold. Notice of suspension and communication failure, delay and early termination, breastfeeding licensing and lack of labeling.

- Notice of contract with employee and employer.

- Early termination of the contract.

- Employee-employer contact center.

- Unemployment Help Center.

- Employee registration form.

- Vacancy scale.

Published in 15 updates 17.

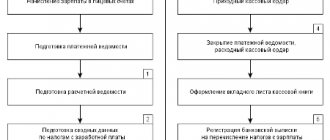

If the salary was not paid in full on time, the payroll must be closed. All uncollected amounts are deposited.

Exceeding the payment deadlines may result in penalties. After the deadline for paying salaries, the cashier completes the preparation of the payroll form T-53. The cashier performs the following actions:

At the time of payment of his salary, each employee must be provided with a payment contribution. Some references are required in this document. Unless otherwise agreed by the employee, the employer may issue payslips electronically. Failure to comply with the provisions of the Labor Code relating to payroll is punishable by the fine prescribed for Class 3 violations.

What is the required information?

This language can be stated as follows: “This bulletin is retained indefinitely.” For its part, the employer maintains a duplicate of employee payslips or payslips transmitted electronically to employees for a period of five years. It also ensures that an electronically issued receipt is available to the employee for either 50 years or until the employee reaches age 75.

Employers with fewer than 300 employees

The employer may also delete lines related to the employer's social security contributions.

- Calculates the amount of wages paid (the amount is indicated in both numbers and words).

- If there are unpaid amounts, deposit each one (the note “Deposited” is made).

- Checks the accuracy of the calculations.

- To confirm the fact of issuing (depositing) the specified amounts, the cashier signs the document (deciphering his signature).

- An expense cash order is issued for the amount of wages paid (form KO-2).

The payroll is returned to the accounting department. After this, the document is checked by an accountant and entered into the synthetic accounting register.

Results

An expense cash order is filled in when funds are issued from the cash register. The rules for filling it out are strictly regulated and are regulated for the most part by instruction No. 3210-U. In 2021, you need to fill out the RKO according to the well-known rules.

Sources:

- Directive of the Bank of Russia dated March 11, 2014 No. 3210-U

- Resolution of the State Statistics Committee of the Russian Federation dated August 18, 1998 No. 88

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

What day should I indicate in the “Date of compilation” field of RKO

This question arises if the salary is issued within several days. Instruction No. 3210-U directly states that RKO is drawn up for the amounts actually issued, para. 4 p. 6.5 Instructions. Consequently, the date of compilation of the cash register is the closing date of the statement, that is, the last day of payment of wages. This rule is explained by the fact that it is not known in advance whether all employees will come to the cash desk for their salaries, therefore, it is impossible to predict what amount will be issued.

Some organizations set the date of the 1st day of payment of wages (the 1st day of the period indicated in the statement), since they believe that the expense order formalizes the director’s order to issue wages in cash, and not transfer them to the accounts of employees. However, this is not true. Such an order is the payroll or payroll itself, signed by the director, and non-cash wages are transferred on the basis of the payroll. Instructions for the use and completion of forms of primary accounting documentation for accounting for labor and its payment (Payroll), approved. Resolution of the State Statistics Committee dated January 5, 2004 No. 1. In addition, since June 1 last year, the signature of the director in the RKO is not required.