What is a chart of accounts

A unified chart of accounts of a government institution (CA) is needed to systematize accounting registers according to quantitative, group and digital values, depending on the object of accounting and the target functioning of a particular organization. It is the link between accounting indicators and financial statements. The plan combines those accounts that are used in operations directly related to the financial and economic activities of enterprises. All reflected information is used to analyze the functioning of institutions and forecast its further financial development.

The plan is used in accounting for absolutely all organizations, regardless of their form of ownership. The following types are distinguished according to the types of economic entities:

- register for business entities;

- for budgetary institutions;

- accounts for credit institutions.

Each PS created for different types of economic entities reflects data grouped in accordance with the sectoral and organizational specifics of the institutions. Intersectoral ministries and departments are responsible for the content and regulatory regulation of the document. For each type of institution, its own instructions for use have been developed, which provide details of accounts and subaccounts to them.

The plan aims to:

- to simplify and create a unified accounting methodology;

- ensuring variability in records of similar operations;

- improvement of control measures regulating the correctness of accounting transactions;

- generalization of similar indicators obtained from various sources both at the enterprise and across regions and the country as a whole;

- streamlining the preparation of accounting documentation, interim and final reporting;

- reducing errors in invoice correspondence.

Who is required to use the chart of accounts?

All economic entities that maintain accounting records are required to apply the chart of accounts. Exemptions are provided only for individual entrepreneurs and private practitioners. Other commercial firms, government agencies and enterprises are required to maintain accounting.

But merchants also have the right to organize accounting as part of their activities. There is no prohibition on conducting. Individual entrepreneurs make decisions independently. If accounting is necessary, you will have to comply with the current rules:

- Develop and approve accounting policies.

- Appoint responsible persons.

- Maintain primary and accounting documentation.

- Conduct audits, inventories and inspections.

- Prepare financial statements.

Some economic entities have the right to conduct accounting in a simplified form. For example, non-profit organizations, small businesses, representatives of Skolkovo. But even the transition to a simplified method does not exempt you from using a single PS.

IMPORTANT!

The use of a chart of accounts is mandatory for all economic entities that must maintain accounting records. There are no exceptions even for simplifiers.

Features in autonomous accounting policy institutions

It is established by law that the requirements of the accounting regulations do not apply to corporate entities. They work on the basis of special regulatory documents that establish uniform methodological rules.

In the AC it is necessary to take into account separately:

- Funds that represent subventions and subsidies. Expenses incurred at their expense are also taken into account separately.

- Income and costs, the formation of which occurs in the process of economic activity.

- Real estate and especially expensive property, which is funded by the founder of the organization and assigned to him while the organization is functioning. Also OS purchased using funds invested by him (the founder).

The accounting policy of accounting companies is formed based on the peculiarities of their structure, belonging to a certain industry, and the powers they exercise. Its construction should ensure rational and effective accounting, commensurate with the scale and capabilities of the management. By order regarding accounting policies, the following is adopted:

- A working chart of accounts, which indicates all the necessary accounts.

- Methods on the basis of which property and liabilities are assessed.

- The order of their inventory.

- Rules for processing information on accounting and features of document flow.

- Forms and forms of primary accounting. They must indicate the details provided for in the instructional materials.

- Construction of internal audit and financial control.

Important! It is allowed to enter additional codes (analytical) into the internal chart of accounts of the AU, which should ensure the formation of objective accounting information that is accessible only to users within the AU, but also to external ones.

Plan for state employees

The unified chart of accounts for accounting in budgetary institutions for 2021 is regulated by Order of the Ministry of Finance of Russia No. 157n dated December 1, 2010. Instruction 157n regulates the financial and economic activities of institutions operating in the Russian budget system.

All budgetary organizations are divided into autonomous, budgetary and state-owned. For each structure, various regulations have been approved that are responsible for accounting within a given organizational form:

- Order of the Ministry of Finance of the Russian Federation No. 162n dated December 6, 2010 - for government institutions, extra-budgetary funds and government bodies;

- order No. 174n dated December 16, 2010 - for BU;

- order No. 183n dated December 23, 2010 - for AU.

Clause 21 of Order No. 157n of the Ministry of Finance states what a budget accounting chart of accounts is (with explanations and entries) - this is a register used by government agencies, extra-budgetary funds and government bodies. That is, those organizations that operate within the framework of order 162n.

IMPORTANT!

The Ministry of Finance approved changes to Order 162n (Order of the Ministry of Finance No. 246n dated October 28, 2020). Now, when maintaining budget accounting, business transactions are reflected in the accounts of the working PS, approved by the institution as part of the formation of the institution’s accounting policy, using the financial security code in the 18th digit of the account number. When financed from the budget of the Russian Federation - code 1, from funds at temporary disposal - 3. This rule is used starting from 01/01/2021. Another important innovation is accrual accounting. According to the rules of this method, all operating results are recognized upon completion of transactions.

All other state employees use accounting software in their work. This difference arose in connection with the possibility of budgetary and autonomous institutions conducting business activities and receiving income from it (clauses 2, 3 of Article 298 of the Civil Code of the Russian Federation). Budgetary organizations formulate a work plan based on instruction No. 157n. The numbering of working accounts consists of 26 digits, which reflect the analytical accounting code, the type of cash security, the synthetic accounting account code and the code of the financial and economic transaction according to KOSGU.

The budget plan consists of balance sheet and off-balance sheet accounts. It is carried out in accordance with funding sources: budgetary and extra-budgetary.

Structure and table

An account, as an accounting unit, helps to organize the property, debts of the institution and the financial institution. In accounting for budgetary organizations, accounts can be active or passive , in contrast to commercial organizations, where there are active-passive accounts:

- Active for the organization's property and resources.

- Sources of financing are reflected in passive

The account number contains 26 digits. The following is part of the table given in Order No. 174n. With its help you can easily decipher the composition of the invoice.

Let's look at it in more detail, taking into account the changes that need to be taken into account in 2021:

- In the working Chart of Accounts of an institution, during synthetic accounting, it is customary to display zeros in the first seventeen digits, and when establishing postings, show zero values in the first fourteen, unless otherwise specified in the accounting policy.

- Next are the codes for the type of inflows or outflows, corresponding to the code for the type of expenses and other groups. They are indicated in the next three digits.

It should be noted that for budgetary institutions the list of types of expenses has been trimmed. They can apply codes to

- employee salaries;

- insurance premiums;

- purchase of goods;

- payment of taxes and fees, etc.

These are only partial elements of entire groups of types of expenses. In more detail, you can find the list of acceptable CWR in the letter of the Ministry of Finance dated March 15, 2021 No. 02-05-11/14269.

Note! From January 1, 2021, in digits 1-4, the code of the type of function of the institution is entered instead of zeros. (See paragraph two of the decree of the Ministry of Finance of the Russian Federation dated December 31, 2015 No. 227n).

The 18th bit indicates the financial security code. Below are the main codes listed in Order No. 157n:

1 - at the expense of budget revenues; 2 - at the expense of funds earned independently; 3 - funds on a temporary basis; 4 - payments for the execution of orders from the state; 5 — payments for other tasks; 6 - payments for the implementation of capital investments; 7 - cash receipts from compulsory medical insurance.

Find out what employers face in 2021 for failure to pay wage advances. Law of the Russian Federation on trade secrets 98-FZ: how can organizations join the confidentiality regime? Find out from the article.

The synthetic account code is shown from 19 to 21 digits, and in 22 and 23 digits the serial number or analytical account is reflected.

Worth considering! From 2021, the name of the corresponding analytical accounting account must include the name of the suitable account and the designation of the codification indicator of the type of inflows or outflows in brackets.

chart of accounts for accounting in budgetary organizations

Structure of the budgetary chart of accounts

The structure of the budget plan is presented in the following sections:

| Chart of accounts section | Contents of accounts | Account code, example |

| Non-financial assets | The “Non-financial assets” section reflects information about all non-current assets of an economic entity. The section includes accounting for the following objects:

New groups:

| 0 101 05 000 “Vehicles” - generation of information on the initial cost of vehicles owned (operably managed) by the enterprise. 0 108 51 000 “Real estate that constitutes the treasury” - reflects the initial cost of real estate located in the treasury. No depreciation is charged on such property. Also, for assets located in the treasury, there is no provision for the allocation of particularly valuable and other property. |

| Financial assets | The “Financial Assets” section accumulates information about all current assets of the institution. Current assets are understood not only as funds in the cash desk and current accounts of an institution, but also as investments in financial assets, advances and receivables. The section includes the following groups:

| 0 201 11 000 “Cash in the institution’s accounts” - discloses information about the availability of finances in current accounts opened with the body providing cash services to the entity (in rubles and foreign currency). 0 205 31 000 “Calculations for income from the provision of paid services (work).” It accrues income from business and other income-generating activities. |

| Liabilities | The “Obligations” section discloses data on accepted obligations:

| 0 302 11 000 “Payroll calculations” - reflects the amount of accrued wages in favor of employees working under an employment contract. 0 302 21 000 “Settlements for communication services” - reflects accounts payable arising under contracts for the provision of communication services. 0 303 01 000 “Calculations for personal income tax” - records data on tax deductions made from the salaries of employees of the organization and from other taxable income. |

| Financial results | A special section “Financial result” is used to reflect income and expenses based on the results of the activities of an economic entity for a certain period. Detailing by time intervals is provided. Information is grouped according to the results of the current period, previous years and future periods. | 0 401 10 000 “Current period income” - used to calculate the institution’s income due in the current financial year. 0 401 28 000 “Expenses of the financial year preceding the reporting year” - discloses information about incurred expenses of the previous period. |

| Authorization of expenses | The registers in the “Authorization of Expenses” section disclose accounting information on:

| 0 501 11 000 “Adjusted LBO” - reflects the amount of completed limits of budget obligations within the current financial year. |

Composition of the budget PS

- Non-financial assets;

- Financial assets;

- Liabilities;

- Financial results;

- Authorization of expenses.

Non-financial assets include fixed assets, intangible and non-productive assets, materials, expenses, depreciation, etc. The difference between a budget PS and a commercial one can be called the presence of a special account for investing in inventories.

Financial assets include DS (in accounts, in cash, etc.), securities, receivables from other counterparties, investments in financial assets. assets, etc.

Section 3, liabilities , includes accounts payable of counterparties and all payments, including settlements between counterparties.

Section 4 contains income-expense and financial accounts. results .

We can say that the composition of budgetary liabilities and assets is similar to these concepts in commercial accounting. The composition of accounts and accounting methods differ.

Section 5 is a list of accounts that reflect movements on:

- budget allocations;

- limits on budget obligations;

- planned income (expenses).

Most of the accounts of the new budget PS are subaccounts of the first, second and third order to the previously existing analytical accounts.

Each individual budget PS account can be active or passive; there is no third option.

The credit balance on the active account is reflected in the account balance in the amount with a minus sign. Similarly, the debit balance on a passive account is a negative credit amount.

In the absence of standard correspondence accounts in the approved Instructions, the organization has the right to create its own, subject to non-violation of the law.

Chart of accounts for budgetary and government institutions

Current table of budget accounting accounts in 2021 for state and budgetary institutions according to instruction 157n:

| Balance account name | Synthetic account of an accounting object | Group name | ||

| Synthetic | Analytical | |||

| Group | View | |||

| 1 | 2 | 3 | 4 | 5 |

| NON-FINANCIAL ASSETS | 1 0 0 | 0 | 0 | |

| Fixed assets | 1 0 1 | 0 | 0 | |

| 1 0 1 | 1 | 0 | Fixed assets - real estate of the institution | |

| 1 0 1 | 2 | 0 | Fixed assets - especially valuable movable property of an institution | |

| 1 0 1 | 3 | 0 | Fixed assets - other movable property of the institution | |

| 1 0 1 | 9 | 0 | Fixed assets - other movable property of the institution | |

| 1 0 1 | 0 | 1 | ||

| 1 0 1 | 0 | 2 | ||

| 1 0 1 | 0 | 3 | ||

| 1 0 1 | 0 | 4 | ||

| 1 0 1 | 0 | 5 | ||

| 1 0 1 | 0 | 6 | ||

| 1 0 1 | 0 | 7 | ||

| 1 0 1 | 0 | 8 | ||

| Intangible assets | 1 0 2 | 0 | 0 | |

| 1 0 2 | 2 | 0 | Intangible assets - especially valuable movable property of an institution | |

| 1 0 2 | 3 | 0 | Intangible assets - other movable property of the institution | |

| Non-produced assets | 1 0 3 | 0 | 0 | |

| 1 0 3 | 1 | 0 | Non-produced assets - real estate of the institution | |

| 1 0 3 | 3 | 0 | Non-produced assets - other movable property | |

| 1 0 3 | 9 | 0 | Non-produced assets - as part of the grantor's property | |

| 1 0 3 | 0 | 1 | ||

| 1 0 3 | 0 | 2 | ||

| 1 0 3 | 0 | 3 | ||

| Depreciation | 1 0 4 | 0 | 0 | |

| 1 0 4 | 1 | 0 | Depreciation of the institution's real estate | |

| 1 0 4 | 2 | 0 | Depreciation of particularly valuable movable property of the institution | |

| 1 0 4 | 3 | 0 | Depreciation of other movable property of the institution | |

| 1 0 4 | 4 | 0 | Depreciation of rights of use of assets | |

| 1 0 4 | 5 | 0 | Depreciation of property constituting the treasury | |

| 104 | 6 | 0 | Amortization of rights to use intangible assets | |

| 1 0 4 | 9 | 0 | Depreciation of the property of an institution in a concession | |

| 1 0 4 | 0 | 1 | ||

| 1 0 4 | 0 | 2 | ||

| 1 0 4 | 0 | 3 | ||

| 1 0 4 | 0 | 4 | ||

| 1 0 4 | 0 | 5 | ||

| 1 0 4 | 0 | 6 | ||

| 1 0 4 | 0 | 7 | ||

| 1 0 4 | 0 | 8 | ||

| 1 0 4 | 0 | 9 | ||

| 1 0 4 | 2 | 9 | ||

| 1 0 4 | 3 | 9 | ||

| 1 0 4 | 4 | 9 | ||

| 1 0 4 | 5 | 1 | ||

| 1 0 4 | 5 | 2 | ||

| 1 0 4 | 5 | 4 | ||

| 1 0 4 | 5 | 9 | ||

| Material reserves | 1 0 5 | 0 | 0 | |

| 1 0 5 | 2 | 0 | Material reserves are particularly valuable movable property of an institution. | |

| 1 0 5 | 3 | 0 | Material reserves - other movable property of the institution | |

| 1 0 5 | 0 | 1 | ||

| 1 0 5 | 0 | 2 | ||

| 1 0 5 | 0 | 3 | ||

| 1 0 5 | 0 | 4 | ||

| 1 0 5 | 0 | 5 | ||

| 1 0 5 | 0 | 6 | ||

| 1 0 5 | 0 | 7 | ||

| 1 0 5 | 0 | 8 | ||

| 1 0 5 | 0 | 9 | ||

| Investments in non-financial assets | 1 0 6 | 0 | 0 | |

| 1 0 6 | 1 | 0 | Investments in real estate | |

| 1 0 6 | 2 | 0 | Investments in particularly valuable movable property | |

| 1 0 6 | 3 | 0 | Investments in other movable property | |

| 1 0 6 | 4 | 0 | Investments in financial lease objects | |

| 1 0 6 | 6 | 0 | Investments in the rights to use intangible assets | |

| 1 0 6 | 0 | 1 | ||

| 1 0 6 | 0 | 2 | ||

| 1 0 6 | 0 | 3 | ||

| 1 0 6 | 0 | 4 | ||

| Non-financial assets in transit | 1 0 7 | 0 | 0 | |

| 1 0 7 | 1 | 0 | The institution's real estate is in transit | |

| 1 0 7 | 2 | 0 | Particularly valuable movable property of the institution is in transit | |

| 1 0 7 | 3 | 0 | Other movable property of the institution in transit | |

| 1 0 7 | 0 | 1 | ||

| 1 0 7 | 0 | 3 | ||

| Non-financial assets of treasury property | 1 0 8 | 0 | 0 | |

| 1 0 8 | 5 | 0 | Non-financial assets that make up the treasury | |

| 1 0 8 | 5 | 1 | ||

| 1 0 8 | 5 | 2 | ||

| 1 0 8 | 5 | 3 | ||

| 1 0 8 | 5 | 4 | ||

| 1 0 8 | 5 | 5 | ||

| 1 0 8 | 5 | 6 | ||

| 1 0 8 | 5 | 7 | ||

| 1 0 8 | 9 | 0 | ||

| 1 0 8 | 9 | 1 | ||

| 1 0 8 | 9 | 2 | ||

| 1 0 8 | 9 | 5 | ||

| Costs of manufacturing finished products, performing work, services | 1 0 9 | 0 | 0 | |

| 1 0 9 | 6 | 0 | Cost of finished products, works, services | |

| 1 0 9 | 7 | 0 | Overhead costs of production of finished products, works, services | |

| 1 0 9 | 8 | 0 | General running costs | |

| Rights to use assets | 1 1 1 | 0 | 0 | |

| 1 1 1 | 4 | 0 | Rights to use non-financial assets | |

| 1 1 1 | 4 | 1 | ||

| 1 1 1 | 4 | 2 | ||

| 1 1 1 | 4 | 4 | ||

| 1 1 1 | 4 | 5 | ||

| 1 1 1 | 4 | 6 | ||

| 1 1 1 | 4 | 7 | ||

| 1 1 1 | 4 | 8 | ||

| 1 1 1 | 4 | 9 | ||

| 1 1 1 | 6 | 0 | Rights to use intangible assets | |

| Impairment of non-financial assets | 1 1 4 | 0 | 0 | |

| 1 1 4 | 1 | 0 | Depreciation of the institution's real estate | |

| 1 1 4 | 2 | 0 | Depreciation of particularly valuable movable property of an institution | |

| 1 1 4 | 3 | 0 | Depreciation of other movable property of the institution | |

| 1 1 4 | 4 | 0 | Impairment of rights to use assets | |

| 1 1 4 | 6 | 0 | Impairment of rights to use intangible assets | |

| 1 1 4 | 0 | 1 | ||

| 1 1 4 | 0 | 2 | ||

| 1 1 4 | 0 | 3 | ||

| 1 1 4 | 0 | 4 | ||

| 1 1 4 | 0 | 5 | ||

| 1 1 4 | 0 | 6 | ||

| 1 1 4 | 0 | 7 | ||

| 1 1 4 | 0 | 8 | ||

| 1 1 4 | 0 | 9 | ||

| 1 1 4 | 6 | 0 | ||

| 1 1 4 | 6 | 1 | ||

| 1 1 4 | 6 | 2 | ||

| 1 1 4 | 6 | 3 | ||

| FINANCIAL ASSETS | 2 0 0 | 0 | 0 | |

| Institutional funds | 2 0 1 | 0 | 0 | |

| 2 0 1 | 1 | 0 | Cash in the institution’s personal accounts with the Treasury | |

| 2 0 1 | 2 | 0 | Funds of the institution in a credit institution | |

| 2 0 1 | 3 | 0 | Cash in the institution's cash desk | |

| 2 0 1 | 0 | 1 | ||

| 2 0 1 | 0 | 2 | ||

| 2 0 1 | 0 | 3 | ||

| 2 0 1 | 0 | 4 | ||

| 2 0 1 | 0 | 5 | ||

| 2 0 1 | 0 | 6 | ||

| 2 0 1 | 0 | 7 | ||

| Funds in budget accounts | 2 0 2 | 0 | 0 | |

| 2 0 2 | 1 | 0 | Funds in budget accounts with the Federal Treasury | |

| 2 0 2 | 2 | 0 | Funds in budget accounts in a credit institution | |

| 2 0 2 | 3 | 0 | Budget funds in deposit accounts | |

| 2 0 2 | 0 | 1 | ||

| 2 0 2 | 0 | 2 | ||

| 2 0 2 | 0 | 3 | ||

| Funds in the accounts of the body providing cash services | 2 0 3 | 0 | 0 | |

| 2 0 3 | 0 | 1 | ||

| 2 0 3 | 1 | 0 | Funds in the accounts of the body providing cash services | |

| 2 0 3 | 2 | 0 | Funds in the accounts of the body providing cash services are in transit | |

| 2 0 3 | 3 | 0 | Funds in accounts for cash payments | |

| 2 0 3 | 0 | 2 | ||

| 2 0 3 | 0 | 3 | ||

| 2 0 3 | 0 | 4 | ||

| 2 0 3 | 0 | 5 | ||

| Financial investments | 2 0 4 | 0 | 0 | |

| 2 0 4 | 2 | 0 | Securities other than shares | |

| 2 0 4 | 3 | 0 | Shares and other forms of capital participation | |

| 2 0 4 | 5 | 0 | Other financial assets | |

| 2 0 4 | 2 | 1 | ||

| 2 0 4 | 2 | 2 | ||

| 2 0 4 | 2 | 3 | ||

| 2 0 4 | 3 | 1 | ||

| 2 0 4 | 3 | 2 | ||

| 2 0 4 | 3 | 3 | ||

| 2 0 4 | 3 | 4 | ||

| 2 0 4 | 5 | 2 | ||

| 2 0 4 | 5 | 3 | ||

| Income calculations | 2 0 5 | 0 | 0 | |

| 2 0 5 | 1 | 0 | Calculations for tax revenues, customs duties and insurance contributions for compulsory social insurance | |

| 2 0 5 | 2 | 0 | Calculations for property income | |

| 2 0 5 | 3 | 0 | Calculations of income from the provision of paid services (works), compensation of costs | |

| 2 0 5 | 4 | 0 | Calculations of fines, penalties, penalties, damages | |

| 2 0 5 | 5 | 0 | Calculations for gratuitous cash receipts of a current nature | |

| 2 0 5 | 6 | 0 | Calculations for gratuitous cash receipts of a capital nature | |

| 2 0 5 | 7 | 0 | Calculations of income from operations with assets | |

| 2 0 5 | 8 | 0 | Calculations for other income | |

| 2 0 5 | 1 | 1 | ||

| 2 0 5 | 2 | 1 | ||

| 2 0 5 | 2 | 2 | ||

| 2 0 5 | 2 | 3 | ||

| 2 0 5 | 2 | 4 | ||

| 2 0 5 | 2 | 6 | ||

| 2 0 5 | 2 | 7 | ||

| 2 0 5 | 2 | 8 | ||

| 2 0 5 | 2 | 9 | ||

| 2 0 5 | 3 | 1 | ||

| 2 0 5 | 3 | 2 | ||

| 2 0 5 | 3 | 3 | ||

| 2 0 5 | 3 | 5 | ||

| 2 0 5 | 4 | 1 | ||

| 2 0 5 | 4 | 4 | ||

| 2 0 5 | 4 | 5 | ||

| 2 0 5 | 5 | 1 | ||

| 2 0 5 | 5 | 2 | ||

| 2 0 5 | 5 | 3 | ||

| 2 0 5 | 6 | 1 | ||

| 2 0 5 | 7 | 1 | ||

| 2 0 5 | 7 | 2 | ||

| 2 0 5 | 7 | 3 | ||

| 2 0 5 | 7 | 4 | ||

| 2 0 5 | 7 | 5 | ||

| 2 0 5 | 8 | 1 | ||

| 2 0 5 | 8 | 3 | ||

| 2 0 5 | 8 | 4 | ||

| 2 0 5 | 8 | 9 | ||

| Calculations for advances issued | 2 0 6 | 0 | 0 | |

| 2 0 6 | 1 | 0 | Calculations for advances on wages, accruals on wage payments | |

| 2 0 6 | 2 | 0 | Calculations for advances for work and services | |

| 2 0 6 | 3 | 0 | Calculations for advances on receipt of non-financial assets | |

| 2 0 6 | 4 | 0 | Calculations for advance gratuitous transfers of a current nature to organizations | |

| 2 0 6 | 5 | 0 | Calculations for gratuitous transfers to budgets | |

| 2 0 6 | 6 | 0 | Social Security Advance Settlements | |

| 2 0 6 | 7 | 0 | Calculations for advances for the purchase of securities and other financial investments | |

| 2 0 6 | 8 | 0 | Calculations for advance gratuitous transfers of capital nature to organizations | |

| 2 0 6 | 9 | 0 | Calculations for advances on other expenses | |

| 2 0 6 | 1 | 1 | ||

| 2 0 6 | 1 | 2 | ||

| 2 0 6 | 1 | 3 | ||

| 2 0 6 | 2 | 1 | ||

| 2 0 6 | 2 | 2 | ||

| 2 0 6 | 2 | 3 | ||

| 2 0 6 | 2 | 4 | ||

| 2 0 6 | 2 | 5 | ||

| 2 0 6 | 2 | 6 | ||

| 2 0 6 | 2 | 7 | ||

| 2 0 6 | 2 | 8 | ||

| 2 0 6 | 2 | 9 | ||

| 2 0 6 | 3 | 1 | ||

| 2 0 6 | 3 | 2 | ||

| 2 0 6 | 3 | 3 | ||

| 2 0 6 | 3 | 4 | ||

| 2 0 6 | 4 | 1 | ||

| 2 0 6 | 4 | 2 | ||

| 2 0 6 | 5 | 1 | ||

| 2 0 6 | 5 | 2 | ||

| 2 0 6 | 5 | 3 | ||

| 2 0 6 | 6 | 1 | ||

| 2 0 6 | 6 | 2 | ||

| 2 0 6 | 6 | 3 | ||

| 2 0 6 | 7 | 2 | ||

| 2 0 6 | 7 | 3 | ||

| 2 0 6 | 7 | 5 | ||

| 2 0 6 | 9 | 6 | ||

| Calculations for credits, borrowings (loans) | 2 0 7 | 0 | 0 | |

| 2 0 7 | 1 | 0 | Calculations for granted credits, borrowings (loans) | |

| 2 0 7 | 2 | 0 | Settlements within the framework of targeted foreign loans (borrowings) | |

| 2 0 7 | 3 | 0 | Settlements with debtors under state (municipal) guarantees | |

| 2 0 7 | 0 | 1 | Settlements for other debt claims | |

| 2 0 7 | 0 | 3 | ||

| 2 0 7 | 0 | 4 | ||

| Calculations with accountable persons | 2 0 8 | 0 | 0 | |

| 2 0 8 | 1 | 0 | Settlements with accountable persons for wages, accruals for wage payments | |

| 2 0 8 | 2 | 0 | Settlements with accountable persons for payment for work and services | |

| 2 0 8 | 3 | 0 | Settlements with accountable persons for receipt of non-financial assets | |

| 2 0 8 | 5 | 0 | Settlements with accountable persons for gratuitous transfers to budgets | |

| 2 0 8 | 6 | 0 | Settlements with accountable persons for social security | |

| 2 0 8 | 9 | 0 | Settlements with accountable persons for other expenses | |

| 2 0 8 | 1 | 1 | ||

| 2 0 8 | 1 | 2 | ||

| 2 0 8 | 1 | 3 | ||

| 2 0 8 | 2 | 1 | ||

| 2 0 8 | 2 | 2 | ||

| 2 0 8 | 2 | 3 | ||

| 2 0 8 | 2 | 4 | ||

| 2 0 8 | 2 | 5 | ||

| 2 0 8 | 2 | 6 | ||

| 2 0 8 | 2 | 7 | ||

| 2 0 8 | 2 | 8 | ||

| 2 0 8 | 2 | 9 | ||

| 2 0 8 | 3 | 1 | ||

| 2 0 8 | 3 | 2 | ||

| 2 0 8 | 3 | 4 | ||

| 2 0 8 | 6 | 1 | ||

| 2 0 8 | 6 | 2 | ||

| 2 0 8 | 6 | 3 | ||

| 2 0 8 | 9 | 1 | ||

| 2 0 8 | 9 | 3 | ||

| 2 0 8 | 9 | 4 | ||

| 2 0 8 | 9 | 5 | ||

| 2 0 8 | 9 | 6 | ||

| Calculations for damage and other income | 2 0 9 | 0 | 0 | |

| 2 0 9 | 3 | 0 | Cost compensation calculations | |

| 2 0 9 | 3 | 4 | ||

| 2 0 9 | 3 | 6 | ||

| 2 0 9 | 4 | 0 | Calculations of fines, penalties, penalties, damages | |

| 2 0 9 | 4 | 1 | ||

| 2 0 9 | 4 | 3 | ||

| 2 0 9 | 4 | 4 | ||

| 2 0 9 | 4 | 5 | ||

| 2 0 9 | 7 | 0 | Calculations for damage to non-financial assets | |

| 2 0 9 | 7 | 1 | ||

| 2 0 9 | 7 | 2 | ||

| 2 0 9 | 7 | 3 | ||

| 2 0 9 | 7 | 4 | ||

| 2 0 9 | 8 | 0 | Calculations for other income | |

| 2 0 9 | 8 | 1 | ||

| 2 0 9 | 8 | 2 | ||

| 2 0 9 | 8 | 9 | ||

| Other settlements with debtors | 2 1 0 | 0 | 0 | |

| 2 1 0 | 0 | 2 | ||

| 2 1 0 | 8 | 2 | Settlements with the financial authority to clarify unknown revenues to the budget of the year preceding the reporting year | |

| 2 1 0 | 9 | 2 | Settlements with the financial authority to clarify unclear revenues to the budget of previous years | |

| 2 1 0 | 0 | 3 | ||

| 2 1 0 | 0 | 4 | ||

| 2 1 0 | 0 | 5 | ||

| 2 1 0 | 0 | 6 | ||

| 2 1 0 | 1 | 0 | Calculations for tax deductions for VAT | |

| 2 1 0 | 1 | 1 | ||

| 2 1 0 | 1 | 2 | ||

| 2 1 0 | 1 | 3 | ||

| Internal settlements based on receipts | 2 1 1 | 0 | 0 | |

| Internal settlements for disposals | 2 1 2 | 0 | 0 | |

| Investments in financial assets | 2 1 5 | 0 | 0 | |

| 2 1 5 | 2 | 0 | Investments in securities other than shares | |

| 2 1 5 | 3 | 0 | Investments in shares and other forms of participation in capital | |

| 2 1 5 | 5 | 0 | Investments in other financial assets | |

| 2 1 5 | 2 | 1 | ||

| 2 1 5 | 2 | 2 | ||

| 2 1 5 | 2 | 3 | ||

| 2 1 5 | 3 | 1 | ||

| 2 1 5 | 3 | 2 | ||

| 2 1 5 | 3 | 3 | ||

| 2 1 5 | 3 | 4 | ||

| 2 1 5 | 5 | 2 | ||

| 2 1 5 | 5 | 3 | ||

| OBLIGATIONS | 3 0 0 | 0 | 0 | |

| Settlements with creditors on debt obligations | 3 0 1 | 0 | 0 | |

| 3 0 1 | 1 | 0 | Settlements on debt obligations in rubles | |

| 3 0 1 | 2 | 0 | Settlements on debt obligations for targeted foreign loans (borrowings) | |

| 3 0 1 | 3 | 0 | Calculations for state (municipal) guarantees | |

| 3 0 1 | 4 | 0 | Settlements on debt obligations in foreign currency | |

| 3 0 1 | 0 | 1 | ||

| 3 0 1 | 0 | 2 | ||

| 3 0 1 | 0 | 3 | ||

| 3 0 1 | 0 | 4 | ||

| Calculations for accepted obligations | 3 0 2 | 0 | 0 | |

| 3 0 2 | 1 | 0 | Calculations for wages, accruals for wage payments | |

| 3 0 2 | 2 | 0 | Calculations for works and services | |

| 3 0 2 | 3 | 0 | Calculations for receipt of non-financial assets | |

| 3 0 2 | 4 | 0 | Calculations for gratuitous transfers of a current nature to organizations | |

| 3 0 2 | 5 | 0 | Calculations for gratuitous transfers to budgets | |

| 3 0 2 | 6 | 0 | Social security payments | |

| 3 0 2 | 7 | 0 | Calculations for the acquisition of financial assets | |

| 3 0 2 | 8 | 0 | Calculations for gratuitous capital transfers to organizations | |

| 3 0 2 | 9 | 0 | Calculations for other expenses | |

| 3 0 2 | 1 | 1 | ||

| 3 0 2 | 1 | 2 | ||

| 3 0 2 | 1 | 3 | ||

| 3 0 2 | 2 | 1 | ||

| 3 0 2 | 2 | 2 | ||

| 3 0 2 | 2 | 3 | ||

| 3 0 2 | 2 | 4 | ||

| 3 0 2 | 2 | 5 | ||

| 3 0 2 | 2 | 6 | ||

| 3 0 2 | 2 | 7 | ||

| 3 0 2 | 2 | 8 | ||

| 3 0 2 | 2 | 9 | ||

| 3 0 2 | 3 | 1 | ||

| 3 0 2 | 3 | 2 | ||

| 3 0 2 | 3 | 3 | ||

| 3 0 2 | 3 | 4 | ||

| 3 0 2 | 4 | 1 | ||

| 3 0 2 | 4 | 2 | ||

| 3 0 2 | 5 | 1 | ||

| 3 0 2 | 5 | 2 | ||

| 3 0 2 | 5 | 3 | ||

| 3 0 2 | 6 | 1 | ||

| 3 0 2 | 6 | 2 | ||

| 3 0 2 | 6 | 3 | ||

| 3 0 2 | 7 | 2 | ||

| 3 0 2 | 7 | 3 | ||

| 3 0 2 | 7 | 5 | ||

| 3 0 2 | 9 | 3 | ||

| 3 0 2 | 9 | 5 | ||

| 3 0 2 | 9 | 6 | ||

| Calculations for payments to budgets | 3 0 3 | 0 | 0 | |

| 3 0 3 | 0 | 1 | ||

| 3 0 3 | 0 | 2 | ||

| 3 0 3 | 0 | 3 | ||

| 3 0 3 | 0 | 4 | ||

| 3 0 3 | 0 | 5 | ||

| 3 0 3 | 0 | 6 | ||

| 3 0 3 | 0 | 7 | ||

| 3 0 3 | 0 | 8 | ||

| 3 0 3 | 0 | 9 | ||

| 3 0 3 | 1 | 0 | ||

| 3 0 3 | 1 | 1 | ||

| 3 0 3 | 1 | 2 | ||

| 3 0 3 | 1 | 3 | ||

| Other settlements with creditors | 3 0 4 | 0 | 0 | |

| 3 0 4 | 0 | 1 | ||

| 3 0 4 | 0 | 2 | ||

| 3 0 4 | 0 | 3 | ||

| 3 0 4 | 0 | 4 | ||

| 3 0 4 | 8 | 4 | ||

| 3 0 4 | 9 | 4 | ||

| 3 0 4 | 0 | 5 | ||

| 3 0 4 | 0 | 6 | ||

| 3 0 4 | 8 | 6 | ||

| 3 0 4 | 9 | 6 | ||

| Calculations for cash payments | 3 0 6 | 0 | 0 | |

| Settlements on transactions on the accounts of the body providing cash services | 3 0 7 | 0 | 0 | |

| 3 0 7 | 1 | 0 | Settlements on transactions on the accounts of the body providing cash services | |

| 3 0 7 | 0 | 2 | ||

| 3 0 7 | 0 | 3 | ||

| 3 0 7 | 0 | 4 | ||

| 3 0 7 | 0 | 5 | ||

| Internal settlements based on receipts | 3 0 8 | 0 | 0 | |

| Internal settlements for disposals | 3 0 9 | 0 | 0 | |

| FINANCIAL RESULTS | 4 0 0 | 0 | 0 | |

| Financial result of an economic entity | 4 0 1 | 0 | 0 | |

| 4 0 1 | 1 | 0 | Revenues of the current financial year | |

| 4 0 1 | 1 | 6 | Income of the financial year preceding the reporting year, identified through control measures | |

| 4 0 1 | 1 | 7 | Income of previous financial years identified through control measures | |

| 4 0 1 | 1 | 8 | Income of the financial year preceding the reporting year, identified in the reporting year | |

| 4 0 1 | 1 | 9 | Income of previous financial years identified in the reporting year | |

| 4 0 1 | 2 | 0 | Expenses of the current financial year | |

| 4 0 1 | 2 | 6 | Expenses of the financial year preceding the reporting year, identified through control activities | |

| 4 0 1 | 2 | 7 | Expenses of previous financial years identified through control activities | |

| 4 0 1 | 2 | 8 | Expenses of the financial year preceding the reporting year identified in the reporting year | |

| 4 0 1 | 2 | 9 | Expenses of previous financial years identified in the reporting year | |

| 4 0 1 | 3 | 0 | Financial results of previous reporting periods | |

| 4 0 1 | 4 | 0 | revenue of the future periods | |

| 4 0 1 | 4 | 1 | Deferred income to be recognized in the current year | |

| 4 0 1 | 4 | 9 | Deferred income to be recognized in subsequent years | |

| 4 0 1 | 5 | 0 | Future expenses | |

| 4 0 1 | 6 | 0 | Reserves for future expenses | |

| Result for budget cash transactions | 4 0 2 | 0 | 0 | |

| 4 0 2 | 1 | 0 | Receipts | |

| 4 0 2 | 2 | 0 | Disposals | |

| 4 0 2 | 3 | 0 | The result of past reporting periods for cash budget execution | |

| AUTHORIZATION OF EXPENSES | 5 0 0 | 0 | 0 | |

| 5 0 0 | 1 | 0 | Validation for current financial year | |

| 5 0 0 | 2 | 0 | Authorization for the first year following the current (next financial year) | |

| 5 0 0 | 3 | 0 | Authorization for the second year following the current one (first year following the next one) | |

| 5 0 0 | 4 | 0 | Authorization for the second year following the next one | |

| 5 0 0 | 9 | 0 | Authorization for other subsequent years (outside the planning period) | |

| Limits on budget obligations | 5 0 1 | 0 | 0 | |

| 5 0 1 | 0 | 1 | ||

| 5 0 1 | 0 | 2 | ||

| 5 0 1 | 0 | 3 | ||

| 5 0 1 | 0 | 4 | ||

| 5 0 1 | 0 | 5 | ||

| 5 0 1 | 0 | 6 | ||

| 5 0 1 | 0 | 9 | ||

| Liabilities | 5 0 2 | 0 | 0 | |

| 5 0 2 | 0 | 1 | ||

| 5 0 2 | 0 | 2 | ||

| 5 0 2 | 0 | 5 | ||

| 5 0 2 | 0 | 7 | Obligations accepted | |

| 5 0 2 | 0 | 9 | Deferred liabilities | |

| Budget allocations | 5 0 3 | 0 | 0 | |

| 5 0 3 | 0 | 1 | ||

| 5 0 3 | 0 | 2 | ||

| 5 0 3 | 0 | 3 | ||

| 5 0 3 | 0 | 4 | ||

| 5 0 3 | 0 | 5 | ||

| 5 0 3 | 0 | 6 | ||

| 5 0 3 | 0 | 9 | ||

| Estimated (planned, forecast) assignments | 5 0 4 | 0 | 0 | |

| Right to assume obligations | 5 0 6 | 0 | 0 | |

| Approved amount of financial support | 5 0 7 | 0 | 0 | |

| Financial support received | 5 0 8 | 0 | 0 | |

The principle of working with a register

Accounting accounts are numerical codes that indicate a specific type of asset, liability, income, expense and capital. They are used to systematize information about accounting objects.

The key principle of working with these accounting registers is the preparation of accounting entries using the double entry method. Transactions on off-balance sheet accounts are reflected in a simple way. Double entry involves the simultaneous reflection of one transaction in two accounts at once: the debit of one and the credit of the other. For example, when the size of an enterprise’s assets changes, the importance of their sources of financing will necessarily change. The principle also applies to the preparation of reports and balance sheets.

All accounts are classified into:

- Active. They can only have a debit balance of the account (positive value). The balance of active accounts at the end of the reporting period forms the active part of the balance sheet.

- Passive. Can only have a credit balance (debt, obligation, debt). Indicators of passive accounts reflect the liabilities of the balance sheet.

- Active-passive. Mixed type: characterized by balances of both debit and credit. Balances are included in the reporting, depending on the type of balance for the reporting period.

Read more: “Active and passive accounts: what is the difference and how to work with them.”

Scheme of operation of budget accounts

I cannot draw attention to one nuance regarding changes in the assets and liabilities of public sector institutions. The fact is that when the same type of assets or liabilities moves in the accounting of public sector employees, different accounts are used, i.e. when

an accounting subject

increases, the Debit of one

account, and when it decreases, accordingly, according to

the Credit of another

.

For example, if it increases

the cost of materials, then the accountant generates a posting:

If the cost of materials decreases

, the posting will be different:

Unified Chart of Accounts

And this is a table of the chart of accounts with a breakdown for 2021 for commercial enterprises and non-profit organizations by order of the Ministry of Finance No. 94n dated October 31, 2000:

| Account number | Name |

| 01 | Fixed assets |

| 02 | Depreciation of fixed assets |

| 03 | Profitable investments in material assets |

| 04 | Intangible assets |

| 05 | Amortization of intangible assets |

| 07 | Equipment for installation |

| Investments in non-current assets | |

| 09 | Deferred tax assets |

| Materials | |

| 11 | Animals being raised and fattened |

| 14 | Reserves for reduction in the value of material assets |

| 15 | Procurement and acquisition of material assets |

| 16 | Deviation in the cost of material assets |

| 19 | Value added tax on purchased assets |

| Primary production | |

| 21 | Semi-finished products of our own production |

| 23 | Auxiliary production |

| 25 | General production expenses |

| General running costs | |

| 28 | Defects in production |

| 29 | Service industries and farms |

| 40 | Release of products (works, services) |

| Goods | |

| 42 | Trade margin |

| 43 | Finished products |

| Selling expenses | |

| 45 | Goods shipped |

| 46 | Completed stages of unfinished work |

| 50 | Cash register |

| 51 | Current accounts |

| 52 | Currency accounts |

| 55 | Special bank accounts |

| 57 | Transfers on the way |

| 58 | Financial investments |

| 59 | Provisions for impairment of financial investments |

| 60 | Settlements with suppliers and contractors |

| 62 | Settlements with buyers and customers |

| 63 | Provisions for doubtful debts |

| 66 | Calculations for short-term loans and borrowings |

| 67 | Calculations for long-term loans and borrowings |

| 68 | Calculations for taxes and fees |

| 69 | Calculations for social insurance and security |

| 70 | Payments to personnel regarding wages |

| 71 | Calculations with accountable persons |

| 73 | Settlements with personnel for other operations |

| 75 | Settlements with founders |

| 76 | Settlements with various debtors and creditors |

| 77 | Deferred tax liabilities |

| 79 | On-farm settlements |

| 80 | Authorized capital |

| 81 | Own shares (shares) |

| 82 | Reserve capital |

| 83 | Extra capital |

| 84 | Retained earnings (uncovered loss) |

| 86 | Special-purpose financing |

| 90 | Sales |

| 91 | Other income and expenses |

| 94 | Shortages and losses from damage to valuables |

| 96 | Reserves for future expenses |

| 97 | Future expenses |

| 98 | revenue of the future periods |

| 99 | Profit and loss |

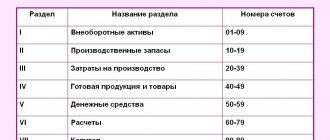

Accounts for business entities

The plan for business entities that keep records using the double entry method, including non-profit organizations, is fixed and regulated by Order of the Ministry of Finance No. 94n dated October 31, 2000. This plan is the same for all institutions, except budgetary and credit (banks).

PAS consists of synthetic and analytical accounts, each of which has a specific numbering. Thus, the register structure represents first and second order accounts. The working document of each organization is developed in accordance with a single PS and includes synthetic and subaccounts.

Accounting registers differ in their content and are active, passive and active-passive. In total, the PAS, which is used by non-profit organizations and other business entities, contains 71 synthetic accounts, including 11 off-balance sheet accounts. The following sections of the PS for business entities are distinguished:

- fixed assets;

- productive reserves;

- production costs;

- finished products, goods;

- cash;

- calculations;

- capital;

- financial results.

1.8. Structure of the budget accounting account number

The Unified Chart of Accounts contains the names and numbers of synthetic accounts of accounting objects (synthetic account codes (first order accounts) and analytical codes of synthetic accounts). An institution has the right to introduce additional analytical codes for synthetic accounts of the Unified Chart of Accounts[56]. The working chart of accounts for accounting is developed and approved by the institution on the basis of the Chart of Accounts for budgetary accounting and the Instructions for its application.

We recommend reading: How much will your pension be increased in January 2021?

The budget accounting account number consists of twenty-six digits (Table 1): Table 1 Budget accounting account number Account number Analytical code according to the budget classification of the type of activity synthetic account analytical according to KOSGU of the accounting object group of the type account digit number 1 - 17 18 19 20 21 22 23 24 25 26 1 – 17 categories – analytical code according to the budget classification of the Russian Federation.

To indicate the first seventeen digits

Accounts for banking organizations

The Central Bank of the Russian Federation has made significant changes to the current plan for credit institutions. Now the procedure by which the bank’s chart of accounts is applied is regulated by the regulation of the Central Bank of the Russian Federation No. 579-P dated 02/27/2017 (as amended on 02/28/2019) with the indication of the Central Bank of the Russian Federation No. 4722-U dated 02/15/2018.

The structure of the plan consists of the following chapters:

- Chapter A - balance sheet accounts;

- Chapter B - trust management accounts;

- Chapter B - off-balance sheet accounts;

- Chapter D - accounts for accounting for claims and obligations under derivative financial instruments and other agreements (transactions), under which settlements and delivery are carried out no earlier than the next day after the conclusion of the agreement (transaction).

Each chapter includes specific sections and subsections.