Accounting of withholding operations according to executive documents

after taxes are withheld (Part 1, Article 99 of Law No. 229-FZ).

All mandatory deductions of amounts of money from the income of employees on the basis of an executive document are carried out without issuing a special order from the manager on deduction and without the consent of the employee. The basis for calculating the corresponding amounts due for withholding are the executive documents themselves. In this case, a separate sub-account is opened for account 76, for example, “Calculations based on writs of execution.” This sub-account must be fixed in the working chart of accounts, which is an integral part of the organization’s accounting policy (clause 4 of PBU 1/2008 “Accounting Policy of the Organization”). Withheld funds from employees' wages on the basis of executive documents can be issued to the claimant personally from the organization's cash desk, transferred to him by mail or to his account at a bank institution: It must be taken into account that the total amount of all deductions for each payment cannot exceed 20 percent, and in in cases provided by law, 50 percent of wages.

Return of the writ of execution to the bailiff

After the organization has withheld all the amounts specified in the writ of execution (or at the end of the period during which it was necessary to make deductions), this document must be returned to the bailiff (for example, sent by mail).

The same should be done if the employee from whose income the deductions are made quit.

At the same time, on the back of the writ of execution, write what amount the organization withheld and transferred to the claimant, as well as the balance of the debt. For example, the entry may look like this: “Alimony in the amount of 21,100 rubles. withheld and transferred to the claimant in full. The remaining amount is 10,000 rubles. not withheld due to the dismissal of an employee. The employee’s new place of work is unknown.” In addition, indicate the numbers of payment orders (receipts) and the dates of transfer of funds. The entry made must be certified by the signature of the chief accountant and the seal of the organization. Similar explanations are contained in subparagraph 10 of paragraph II of Appendix No. 1 to the Methodological Recommendations of the FSSP of Russia dated June 19, 2012 No. 01-16, letter of the FSSP of Russia dated June 25, 2012 No. 12/01-15257.

As a rule, the writ of execution is sent to the bailiff within three days after the employee is dismissed. In relation to alimony, such a period is established by Article 111 of the Family Code of the Russian Federation. For other deductions, the law does not establish a specific period. However, Part 4 of Article 98 of Law No. 299-FZ of October 2, 2007 states that the writ of execution must be returned immediately after the debtor changes his place of work.

Situation: how to withhold child support for the month in which an employee’s child turns 18?

Payment of alimony stops when the child reaches the age of majority (Clause 2 of Article 120 of the Family Code of the Russian Federation). Therefore, to calculate alimony, the salary accrued to the employee for the month in which his child turns 18 years old must be divided into two parts.

The first is the one that falls from the beginning of the month until the day the child comes of age. Child support must be withheld from this amount.

The second is that part of the salary that was accrued for the time when the employee’s child turned 18 years old. There is no need to withhold alimony from this amount.

Accounting

To account for mandatory deductions under writs of execution for account 76, open the subaccount “Settlements under writs of writ.”

When deducting amounts under executive documents from an employee’s salary, make an entry in your accounting:

Debit 70 Credit 76 sub-account “Settlements based on executive documents”

– deducted from the employee’s salary according to the executive document.

When paying the withheld funds to the claimant from the cash register, make the following entry:

Debit 76 subaccount “Settlements on executive documents” Credit 50

– the amount withheld under the writ of execution was issued to the recipient.

When transferring the withheld funds to the creditor's bank account, make a note:

Debit 76 subaccount “Settlements on executive documents” Credit 51

– the amount withheld under the writ of execution is transferred to the recipient.

Reflect the transfer fee using the following entries:

Debit 76 subaccount “Settlements on executive documents” Credit 51

– the bank withheld a commission for the transfer of the amount withheld under the writ of execution.

The fee for a bank transfer or postage is paid by the debtor, that is, the employee (Part 3 of Article 98 of the Law of October 2, 2007 No. 229-FZ).

Therefore, deduct the bank transfer fee from the employee’s salary:

Debit 70 Credit 76 sub-account “Settlements based on executive documents”

– the commission for bank transfer of the amount under the writ of execution is repaid from the employee’s salary.

If the withheld amount is transferred by mail, make the following entries:

Debit 71 Credit 50

– the amount of alimony was issued on account, which must be sent by postal order, and money to pay the postage;

Debit 76 subaccount “Settlements on executive documents” Credit 71

– the amount withheld under the writ of execution has been transferred by postal order, and the postage fee has been paid.

Debit 70 Credit 76 sub-account “Settlements based on executive documents”

– the postal fee for transferring the amount under the writ of execution is paid from the employee’s salary.

Types of deductions under a writ of execution from wages

A writ of execution is mandatory for recovery from an individual’s income, regardless of the employer’s wishes.

You do your duty and work honestly. I definitely recommend Nadezhda Vladimirovna! I have worked with the company several times already. Deduction is made when accruing income - wages and other receipts from the employer. The legislation establishes a number of payments for which no deduction is made. Amounts received in the form of compensation payments, compensation for harm, and social benefits are exempt from collection. We will tell you in the article how deductions are made from wages based on a writ of execution, and what entries are made. The procedure for deductions is determined by the Federal Law of October 2, 2007 No. 229-FZ “On Enforcement Proceedings”.

There are several types of executive documents used in circulation. Documents of an enforcement nature, the most well-known in circulation: Executive documents are binding from the day they are received by the enterprise by mail or through the claimant.

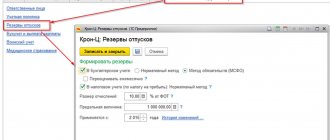

Document “Writ of Execution” in 1C Accounting

This document assigns withholding to a specific employee.

Salary and personnel / Salary / Writs of execution

Let's create a document and indicate the necessary data in it. In the “Recipient” field, the program offers a choice from the directory of counterparties, so the recipient (it can be an individual or legal entity) must first be entered into this directory.

The retention period and calculation method are filled in according to the executive document received by the organization. If you do not specify the end of the period, the program will perform the deduction every month. There are three options for the calculation method: percentage, share or fixed amount.

Please note: in this 1C document it is not possible to indicate the withheld remuneration of the paying agent. It will have to be entered manually when calculating salaries.

The writ of execution does not make accounting entries and does not have a printed form.

Collection procedure and examples of deduction from wages under a writ of execution

Deductions under a writ of execution from an employee’s salary are made forcibly upon receipt of the corresponding document by the organization’s accounting department.

The procedure for such actions is reflected in the Labor Code of the Russian Federation. The decision on its approval is made as a result of a court hearing. In addition, this type of document is the basis for making deductions from wages based on a writ of execution against the employee’s debts. an agreement on the payment of alimony for the maintenance of disabled relatives or minor children, previously certified by a notary; acts, protocols of authorized bodies providing for recovery in accordance with federal legislation; resolution of an FSSP employee or a notary; acts, certificates issued by the Pension Fund in relation to an employee in the status of an individual entrepreneur.

How is deduction carried out under a writ of execution from wages in 2021?

A court decision is a written position of a court of any instance on any issue.

It must be remembered that a court decision cannot be canceled and, if it is made, it must be executed. For example, if the amount of alimony payments is calculated. The permissible amount of deductions is understood as a certain part of the salary, after deducting which a certain amount must remain.

For example, if alimony is withheld from an employee’s salary, the result must necessarily remain an amount the amount of which will be no less than the minimum wage in the region. For example, today its value is 5,965 rubles (for 2021).

Writ of execution: calculations, reflection in accounting

At any time, an organization’s accountant can receive a writ of execution for payment of alimony or compensation for damage caused. According to Art. 138 of the Labor Code of the Russian Federation (hereinafter referred to as the Labor Code of the Russian Federation), deductions from an employee’s salary are made only in cases provided for by the Labor Code of the Russian Federation and other federal laws. After receiving a writ of execution, the accountant first of all needs to determine which normative act governs this deduction. If a writ of execution is received in connection with the employee’s obligation to pay alimony, then the deductions will be regulated by the Family Code of the Russian Federation (hereinafter referred to as the RF IC), Decree of the Government of the Russian Federation dated July 18, 1996 N 841 (as amended on February 6, 2004 “On the list of types of wages”) fees and other income from which alimony for minor children is withheld"), as well as the Federal Law of July 21, 1997 N 119-FZ (as amended on December 27, 2005) "On Enforcement Proceedings". If the writ of execution contains a requirement to withhold the amount for damage caused, then the withholding is subject only to Law N 119-FZ.

Next, you should check the presence of all the necessary details of the writ of execution. According to Law N 119-FZ, the writ of execution must indicate:

name of the court that issued the writ of execution;

number of the case or materials for which the writ of execution was issued;

date of adoption of the judicial act subject to execution;

names of the recoverer-organization and the debtor-organization, their addresses; surname, name, patronymic of the creditor-citizen and debtor-citizen, their place of residence, date and place of birth of the debtor-citizen and place of his work;

the operative part of a judicial act or an act of another body;

date of entry into force of a judicial act or act of another body;

the date of issue of the writ of execution and the deadline for presenting it for execution;

official seal and signature of the judge.

Deductions from wages according to executive documents

Writs of execution can be received by the employer by mail, through a bailiff, or personally from the claimant under the writ of execution (for example, from the recipient of alimony).

At the same time, not only the employer (to avoid mistakes), but also the employee himself should familiarize himself with it in as much detail as possible. This will allow him to monitor the legality of all actions of the employer. In accordance with Federal Law No. 229-FZ “On Enforcement Proceedings”, from the date of receipt of the writ of execution, the employer is obliged to withhold the amounts specified in it from the employee’s income (Article 98 of Law No. 229-FZ). In this case, executive documents include:

- writs of execution;

- notarized agreements on the payment of alimony or their notarized copies;

- court orders;

- other documents listed in Art. 12 of Law No. 229-FZ.

- orders of the bailiff;

The basis for withholding is the original of the writ of execution, or its duplicate, which in its legal force is equal to the original.

The timing of deductions and the procedure for their reflection in accounting.

According to paragraph 3 of Art. 98 of Law No. 229-FZ, organizations paying wages or other periodic payments to the debtor, from the date of receipt of the writ of execution from the claimant or a copy of the writ of execution from the bailiff, are obliged to withhold funds from the wages and other income of the debtor in accordance with the requirements contained in the executive document. Within three days from the date of making payments in favor of the debtor, they are obliged to transfer the withheld funds to the recoverer. Transfer and transfer of funds are made at the expense of the debtor.

The amounts collected under the writ of execution can be transferred to the recoverer by mail or to his bank account. Information about the details by which it is necessary to transfer the amount collected from the debtor must be contained in the writ of execution (writ of execution, court order, resolution of the authorized body) or the resolution of the bailiff on foreclosure of the debtor’s income (clause 9, clause II of the Memo) .

The actual address of the claimant is a mandatory detail of the writ of execution (Article 13 of Law No. 229-FZ). It turns out that if the enforcement documents do not contain either the address of the collector or the bank details of the collector, then the institution making payments in favor of the debtor employee is not obliged to transfer the calculated amounts of deductions. At the same time, in paragraphs. 9, paragraph II of the Memo, it is recommended that in the case where the address of the person in whose favor alimony is being collected is unknown, alimony should be transferred to the bank account of a structural unit of the territorial body of the FSSP.

In accordance with paragraph 273 of Instruction No. 157n, to account for calculations of deductions from wages and allowances, scholarships or other periodic payments for non-cash transfers under writs of execution and other documents, account 304 03 “Calculations of deductions from wage payments” is used.

According to paragraph 108 of Instruction No. 162n in the budget accounting of a government institution, this account is reflected in the correspondence:

- with the debit of account 1 302 00 000 “Settlements for accepted obligations” - when calculating deductions on writs of execution;

- with the credit of accounts 1 304 05 000 “Settlements for payments from the budget with the financial authority”, 1 201 21 610 “Retirement of funds of the institution from accounts in a credit institution” - when transferring withheld amounts.

Let's consider the procedure for reflecting in budget accounting transactions for the accrual and transfer of deductions based on writs of execution using an example.

Based on the writ of execution, the state institution withholds monthly alimony from the employee’s salary in the amount of 25% of his salary, which is 20,000 rubles. Alimony is sent to the recipient by postal order through a cashier. The postage fee is 1% of the alimony amount.

In the budget accounting of a government institution, these operations will be reflected as follows:

| Contents of operation | Debit | Credit | Amount, rub. |

| Employee's salary accrued | 1 401 20 211 | 1 302 11 730 | 20 000 |

| Personal income tax withheld (RUB 20,000 x 13%) | 1 302 11 830 | 1 303 01 730 | 2 600 |

| Funds were received from the personal account at the cash desk to pay wages to an employee (20,000 - 2,600) rub. | 1 210 03 560 Off-balance sheet account 17 (KOSGU 510) | 1 304 05 211 | 17 400 |

| 1 201 34 510 Off-balance sheet account 17 (KOSGU 510) | 1 210 03 660 Off-balance sheet account 18 (KOSGU 610) | ||

| Amount of alimony withheld* (20,000 - 2,600) rub. x 25% | 1 302 11 830 | 1 304 03 730 | 4 350 |

| The amount of postage is withheld when transferring alimony (RUB 4,350 x 1%) | 1 302 11 830 | 1 304 03 730 | 43,5 |

| Salary was issued to the employee minus deductions made (20,000 - 2,600 - 4,350 - 43.5) rub. | 1 302 11 830 | 1 201 34 610 Off-balance sheet account 18 (KOSGU 211) | 13 006,5 |

| Funds were issued to the cashier on account for making a postal transfer (4,350 + 43.5) rub. | 1 208 11 560 | 1 201 34 610 Off-balance sheet account 18 (KOSGU 211) | 4 393,5 |

| The postal transfer of alimony through the cashier is reflected on the basis of an advance report with a receipt attached for the amount of the postal transfer and postage: | |||

| - in the amount of alimony | 1 304 03 830 | 1 208 11 660 | 4 350 |

| – in the amount of postage | 1 304 03 830 | 1 208 11 660 | 43,5 |

* The amount of deductions for executive documents is calculated according to the payroll (f. 0504402), payroll (f. 0504401).

The amount of permissible deduction from wages under a writ of execution

There is a court decision or a norm established by law for deductions from accrued wages.

The process of deducting money from accrued wages is possible only if the decision on this has already entered into force. Article 107 of the Labor Code of the Russian Federation clearly establishes a list of grounds for withholding financial resources. Material deductions are made in favor of the state or those persons whose rights were violated by the employee.

There are the following types of retention:

- at the employer's own initiative. If the employer is not obliged to withhold, but has the right to do so;

- at the initiative of the employee.

- mandatory, when the employer is in any case obliged to withhold the amount of money earned;

Deductions of a certain amount from the monthly accrual of financial resources carried out by the head of the organization are regulated by Article 137 of the Labor Code of the Russian Federation and are of the following types:

- reimbursement of an advance not yet received, but also without working out according to the norms.

- full reimbursement of the advance payment not worked out according to the law;

In addition, the amount that the organization pays as a commission for making transfers is withheld from him. Get 200 video lessons on 1C for free: You can deduct a certain percentage of all accruals from your salary - up to 20% and up to 50% (in some cases).

The exceptions are payments under writs of execution: In the form of alimony for children For compensation for harm to health For compensation of funds to persons who have lost a breadwinner For payments for compensation for harm caused during a crime These transfers are not subject to these restrictions. Postings for salary payments and personal income tax and contributions are made on the day of the actual transfer (issue) of funds.

Payroll Expenses on wages are written off to the cost of products or goods, therefore the following accounts correspond to account 70: for a manufacturing enterprise - account 20 “Main production” or account 23 “Auxiliary production”, 25 “General production expenses”, 26 “General business ( administrative) expenses”, 29 “Service production and facilities”; for a trading enterprise - account 44 “Sales expenses”.

What payments must be deducted from?

Payments in favor of children must be made from all “labor” income that the alimony payer receives. These include:

- wages, both at the main place of work and part-time;

- income from business activities;

- vacation pay;

- sick leave;

- allowances for hazardous working conditions, for difficult climatic conditions, which are paid to employees;

- bonuses and other remuneration directly related to the payer’s work activity.

You cannot make deductions from the following income:

- received from compensation for harm to health or loss of a breadwinner;

- compensation paid by government authorities to the population in connection with emergency situations;

- business trips;

- financial assistance from the employer;

- various benefits;

- maternity capital issued at the birth of a second or subsequent child;

Deduction amount

In Art. 81 of the RF IC states that alimony in favor of a child/children can be calculated either in a fixed amount or as a percentage of wages. The court, as a rule, sets the alimony payment as a percentage:

- for one child you need to transfer no more than a quarter of the salary;

- for two children - no more than a third;

- for three or more – no more than half.

If the parents agree among themselves, then alimony can be paid in a fixed amount.

The organization should not know that their employee is an alimony payer. Notifying the manager is the responsibility of such an employee.

Writs of execution: deductions, payments, postings

In the common understanding, deduction under writs of execution is the payment of alimony.

In fact, there are other situations where it is necessary to withhold part of an employee’s salary by court order.

In this material we will look at what it is and look at the main entries for deductions from an employee’s salary based on a writ of execution.

- For reimbursement of loans, loans and interest on them

- Child support for elderly relatives

- On child support for minors

- For compensation of damage caused to organizations

- For compensation for harm to physical or moral health

This obligation covers all employee income, except those that fall under the regulations of Art. 101 of Law 212-FZ. In addition, the amount that the organization pays as a commission for making transfers is withheld from him.

What is a writ of execution?

Deductions under a writ of execution from an employee’s salary are made forcibly upon receipt of the corresponding document by the organization’s accounting department. The procedure for such actions is reflected in the Labor Code of the Russian Federation.

Example of a writ of execution.

A writ of execution is the main way of influencing a debtor through enforcement proceedings.

And in order to receive a writ of execution, you will have to fill out a Sample Application for the Issue of a Writ of Execution, which you can download here.

The decision on its approval is made as a result of a court hearing. In addition, this type of document is the basis for making deductions from wages based on a writ of execution against the employee’s debts.

Calculation of the amount of deductions

Determination of the amount that should be withheld on the basis of a writ of execution is carried out on the basis of the information specified in the document. When calculating deduction, an accountant should pay attention to:

- amount of recovery (fixed amount or percentage of monthly income);

- the period during which the employer must make deductions (a certain period or until the occurrence of a particular event);

- other conditions affecting the amount of recovery or termination of deductions.

If the amount of deduction is determined as a percentage of monthly income (relevant for alimony under a writ of execution), then the following formula is used to calculate penalties:

Amount of withholding = (Income - personal income tax) * Percentage of withholding.

When calculating income for deduction, amounts paid by the employer as wages are taken into account, namely:

- salary;

- additional payments, allowances;

- awards, bonuses;

- vacation pay, sick leave;

- other payments that, according to labor legislation, are recognized as elements of remuneration.

The base for withholding is determined as the difference between monthly income and withheld personal income tax, that is, the amount of collection takes into account wages minus income tax.

When withholding amounts under a writ of execution, the employer is obliged to charge and pay insurance contributions to extra-budgetary funds in the general manner.

Executive documents: main types

Mandatory documents that are required by law to be implemented in a strict manner in relation to a specific employee of the organization include:

- writs of execution issued on the basis of decisions made by courts of general jurisdiction;

- orders issued by courts according to a written request from creditors;

Order and instruction: what is the main difference?

- an agreement on the payment of alimony for the maintenance of disabled relatives or minor children, previously certified by a notary;

- acts, protocols of authorized bodies providing for recovery in accordance with federal legislation;

- resolution of an FSSP employee or a notary;

- acts, certificates issued by the Pension Fund in relation to an employee in the status of an individual entrepreneur.

Executive documents (sheets) are divided according to the types of requirements:

- requiring urgent compensation for damage caused to the health and property of citizens as a result of an offense;

- mandatory payment of alimony for children under the age of majority;

- sheets providing for the payment of an administrative fine;

- requirements for the repayment of debts in favor of financial and economic institutions or housing and communal services.

Types of executive documents.

Collection of alimony through judicial authorities

If the parties fail to reach an agreement peacefully, then the party raising the child has the right to file an application with the court.

You can download a sample application for alimony collection from the link.

Types of writs of execution against alimony defendants:

- document - issued on the basis of a court decision made on the basis of a claim;

- court order - issued after contacting the authorized bodies with a written application for collection, through which the procedure for collecting alimony is carried out;

- agreement certified by a notary.

A writ of execution and a court order have equivalent force, differing only in the method of receipt.

An order issued following a court hearing can be obtained by submitting a written application to the highest authorities. If the defendant has no objection to what is stated in the document, the judge makes a decision.

In what cases is a writ of execution invalid?

A writ of execution deduction from wages will not have the proper effect if it does not contain the following data:

- name of the judicial authority;

- production number;

- date of decision of the judicial authorities;

- composition of the decision made;

- date of document execution;

- initials of the recipient and debtor;

- if a child is involved in enforcement proceedings, then in this case his date of birth and initials are indicated.

If a writ of execution (sheet) for deducting an amount from an employee’s wages is lost, the basis for proceedings is its duplicate. Deductions from the debtor’s profit through such paper are carried out without an order, and the employee’s consent is not required for this.

How should the employer act in this case?

After receiving a document for deduction according to a writ of execution from wages to an enterprise, the following procedure must be followed:

1. This retention document is registered in a special journal.

you can learn more about the magazine.

2. After the document is received by the accounting department of the enterprise, its employees inform the bailiff in writing that it has arrived at its destination.

The writ of execution is a paper of strict accountability, therefore it is stored in a safe.

When dismissing an employee for whom a document for deduction has been received under a writ of execution from wages, the accounting department is obliged to send the document back to the bailiff, attaching calculations of the deductions made: date, payment slip number when the funds were paid. And also the amount of debt, if any.

Deductions under a writ of execution from wages are made from the employee’s income on a monthly basis. The plaintiff must transfer alimony according to the data specified in the paper within 3 days from the start of payment of wages.

In what cases is it impossible to deduct from wages under a writ of execution?

The Federal Law “On Enforcement Proceedings” contains a list of cases in which deductions from wages under a writ of execution are unacceptable:

- payments from social state funds or from the employer’s own funds, but disability benefits do not apply here; deductions from it are made in the usual manner;

- compensation payments - travel expenses, in case of loss of a breadwinner, compensation for damage to health;

- partial or full payment for health resort treatment of employees.

Amount of salary deduction

The amount of monthly deduction from the income received is indicated in the text of the document by the bailiff. This can be either a certain percentage or a fixed amount of earnings.

And 12 rules for filling out Form T-54 of an employee’s personal account will help you fill out deductions correctly.

Withholding under a writ of execution from wages is the required amount, which is deducted from the accruals made and sent to the recipient.

If an employee has accumulated debt on his obligations, then they are fulfilled to the maximum possible extent until the existing debt is repaid.

According to the rule, no more than half of the salary remaining after personal income tax has been deducted can be withheld from an employee’s income, even if several enforcement documents have been submitted to him at once.

Exceptions to this are the following situations:

- the penalty is aimed at supporting children under the age of majority;

- compensation for harm caused to health, damage caused, death of the sole breadwinner, as a result of criminal actions.

In such situations, the percentage of deduction from the employee’s salary reaches 70%.

Calculation of debt amounts.

Example 1

The company received a document to withhold alimony under a writ of execution from an employee’s salary, starting from March 22, 2015.

For March, part of the debt is withheld from wages accrued from March 22 to March 31. In March, the employee is awarded a bonus based on the results of work for 2014, since the employee’s obligations do not apply to this period of time, no deduction is made.

Example 2

The child for whom the employee pays child support turns 18 years old on April 23, 2015. In this example, the deduction is made:

- from wages for the period from April 1 to April 22 inclusive;

- from the premium for the 4th quarter, proportionally from April 1 to April 22;

- from the 2015 premium, falling for the period from January 1 to April 22.

It does not matter that at the time of accrual of financial incentives for the quarter and year, the employee’s obligations are terminated.

If, upon reaching adulthood, there is arrears of child support, then the obligations are not canceled until the debt is fully repaid, regardless of how old the child is.

Reflection of deduction of alimony under a writ of execution on accounting accounts (entries)

All accruals and deductions made on the sheet from wages in the accounting department are reflected in certain entries:

- employee payroll: D – 26, K – 70;

- Personal income tax: D – 70, K – 68;

- deductions that are calculated from the deduction document according to the writ of execution from wages: D – 70, K –76;

- issuance of alimony to the plaintiff from the cash register of the enterprise: D – 76, K -50;

- payment of alimony from the organization's current account: D – 76, K – 51;

- commission for the transfer: D – 76, K – 51;

- payment of alimony by mail: D – 71, K – 50.

Read more about accounting entries.

Responsibility of accounting employees

Papers on withholding under a writ of execution are strictly accountable documents, therefore the accounting department of the enterprise is responsible for their storage and execution. At the same time, a fine is provided for non-fulfillment or loss of such documents.

There are several types of violations regarding the implementation of deductions under writs of execution:

- deductions are not made despite the presence of a certain document;

- alimony payments are received late into the recipient's account;

- loss of a document or untimely transfer to another enterprise.

And you can find out how to pay wages correctly in article 6 main rules for filling out a payroll for the issuance of wages.

Reflection of deduction of alimony under a writ of execution from wages.

You will find information about how the state can detect this incident.

For such violations, a fine is imposed on the manager and the organization, after which the accountant most likely will not work in the company.

If alimony is withheld in excess of the due rate, the overpayment will not be demanded back from the recipient, but will be deducted from the salary of the accounting employee who made the mistake.

Fresh materials

- Clarification on 4 FSS When it is necessary to adjust 4-FSS The calculation presented in the FSS in form 4-FSS does not need adjustments if...

- Social tax 2021 Tax accrualIn accounting, the amounts of advance tax payments are reflected in the credit of account 69 (68)…

- Tax planning Tax planning in an organization Tax planning can significantly affect the formation of the financial results of an organization,…

- Why do they buy gold? Selling gold competently is a process that will require you to spend some free time. It will be necessary to find out...

Write-off from the current account by court decision

Question According to a court decision, it is necessary to return part of the money paid for the work done to the legal successor of the bankrupt company. What wiring needs to be done?

Answer In the situation under consideration, the organization will have to incur expenses that represent the repayment of debt in the form of overdue payment for work performed based on a court decision.

In this regard, these expenses in the form of payment of the principal amount must be reflected as part of other expenses using account 91 “Other income and expenses” in correspondence with account 76 “Settlements with various debtors and creditors”, subaccount “Settlements on claims”.

According to clause 12 and clause 14.2 of PBU 10/99, compensation for losses caused by the organization is accepted for accounting in amounts awarded by the court or recognized by the organization.

Moreover, in accordance with clause 18 of PBU 10/99, expenses are recognized in the reporting period in which they occurred, regardless of the time of actual payment of funds and other form of implementation (assuming the temporary certainty of the facts of economic activity).

Therefore, the necessary accounting entries must be reflected on the date the court decision entered into legal force: Debit 91, subaccount “Other expenses” Credit 76, subaccount “Settlements on claims” - an expense in the form of overdue payment is recognized.

- (3 kB)

- (130 kB)

- (28 kB)

- (26 kB)

- How to correctly reflect in accounting the design work (150,000 rubles) and installation of a fire alarm (844,800 rubles) in the company’s office ✒ Design work Costs for the development of design documentation for construction….

- Is it possible to partially write off a loss from car theft and how to show all this in the declaration?

IN…. 1. We have an office for rent, we are tenants.

Rental period 11 months,…. What is the best account for renting premises?

6 275 Back Forward

Penalties for personal income tax: accounting entries

In this case, the agreement may be worded regarding the payment of a penalty in one of three options:

- payment of debt and penalties from above;

- payment of one of the amounts at the choice of the debtor.

- payment of penalties only;

According to officials, the penalty for late payment of goods should be attributed to the payment of sold products, thus, the accountant must reflect the penalty as part of other income.

Debt collected by court decision, how to reflect it in accounting

Deductions for these days are not made if the employee is dismissed on the grounds provided for in paragraph 8 of part one of Article 77 or paragraphs 1, 2 or 4 of part one of Article 81, paragraphs 1, 2, 5, 6 and 7 of Article 83 of this Code.

In the cases provided for in paragraphs two, three and four of part two of this article, the employer has the right to decide to deduct from the employee’s salary no later than one month from the end of the period established for the return of the advance, repayment of debt or incorrectly calculated payments, and provided that if the employee does not dispute the grounds and amounts of the withholding.

Wages overpaid to an employee (including in the event of incorrect application of labor legislation or other regulatory legal acts containing labor law norms) cannot be recovered from him, except in cases of: counting error; Article 138.

Accounting and legal services

Regarding accounting (on question No. 1) No, not entirely true.

It was not worth reflecting future income.

The accrual of contractual sanctions, amounts of compensation for losses (damages) for violation of contractual obligations recognized by the counterparty or awarded to him by the court, and their receipt must be done using account 76.

2 “Calculations for claims.” Discount rate of the Central Bank: How in this situation to reflect the receipt of money as revenue from ordinary activities or other income? What to do with VAT and income tax on this receipt?

Debt collection through court (postings)

If legal proceedings do not attract, then for peace of mind it is better to charge VAT. Attention! The government believes that the supplier must pay VAT on the penalty.

Sometimes it happens that you have to collect the debt from the debtor under a writ of execution. This is a rather complicated process, since you have to contact the bailiff service. Often, defendants do not agree with the court order and are unwilling to pay the debt voluntarily.

Debit Credit Description of transaction Dt 51 Kt 76 Funds received into the current account that were collected by bailiffs Dt 76 Kt 62 (60) Received money accepted to repay a debt from the counterparty It is important to clearly understand when to reflect the receipt of funds. The income must be taken into account at the time the court decision comes into force.

Accounting entries based on a court decision

But nothing is there on his first visit to Chita in 2007, Putin said that the road had been built, 3 years later, a new mega project (Putin-Lada Kalina) was built again with a show off. Huge areas are not paved, not to mention infrastructure. And at the end of the JOKE, along the road where Putin was driving, they removed the direction indicators to the villages

“God forbid I should go to a Siberian poverty-stricken, drunken village”

How to correctly prepare accounting entries for this operation.c.

Stanislav Bychkov, Deputy Director of the Department of Budget Methodology of the Russian Ministry of Finance. . Reimbursement of legal costs and state fees by court decision. This will be a training manual for beginning swindlers. Bribes. PS Very cool picture.

I liked the Shine picture! Well, there’s nothing else to do. That's not how books are written. You need to experience this matter for yourself.