To move products, they need to be packaged, i.e. containers that can be used more than once, which will be classified as returnable containers, for which the supplier takes a deposit, which is reimbursed when the container is returned in good working order. Accounting for such packaging is maintained by both the supplier and the buyer. These points (return, terms, etc.) must be reflected in the supply agreement. The movement of containers must be reflected in the primary documents.

Let's look at how organizations keep track of returnable packaging.

Documents reflecting the movement of containers

Returnable packaging is not included in the cost of products sold. Therefore, the organization must highlight it in the primary documents for the supply of products as a separate line. The price of returnable packaging, which the buyer must transfer to the organization in the event of non-return of the packaging, must be indicated in the agreement with the buyer (purchase and sale agreement, supply agreement, etc.).

Acting State Advisor of the Russian Federation, 3rd class S. Razgulin

Returnable packaging (including those with a deposit value) must be reflected in the following documents:

- agreement for the supply of goods, which stipulates that the goods are supplied in returnable packaging, conditions for its return, payment in the event that the packaging is not returned (deposit value)

- act of acceptance and transfer of goods, where the quantity, price and cost of packaging are indicated on a separate line

- act of reconciliation of returnable containers, which reflects the movement of containers between counterparties

- a certificate for returnable packaging, provided to the buyer within 2 days from the date of delivery and reflecting its quantity, cost and date of return (the certificate may not be provided, but a stamp may be placed on the documents for the shipped products).

Internal movement of returnable containers must be documented with an invoice for internal movement in the TORG-13 form, for example, for packaging goods (if the enterprise uses unified forms or independently developed and approved documents), where its value is reflected in accounting prices or at the actual cost of the container. The invoice is signed by the MOL of both parties and transferred to the accounting department.

In accounting, container transactions are reflected in the analytical accounts of subaccounts of account 41, and in the case of pledged containers - in off-balance sheet account 002.

Explanation of the term

The definition of container largely duplicates the definition of packaging. But these two terms are not synonymous. The semantic load of each of these terms has its own differences, but it is often not easy to draw a clear line between containers and packaging. There are several concepts that explain the difference between containers and packaging, and each of them has its own weak point.

According to one of the concepts, containers, unlike packaging, necessarily perform frame-bearing functions and are the main protection against mechanical loads. For example, pasta in plastic bags is placed in a hard container. At the same time, the package only plays the role of a shell, mostly performs marketing and hygienic functions and is not a container. The container protects products from damage, allows them to be transported, stored, facilitates loading and unloading, makes stacking and other logistics operations possible without the risk of destruction of fragile commercial packaging.

The weak point of this concept is the existence of so-called soft packaging - bags, soft containers, etc. This type of container does not have a frame, but is often reversible, which is one of the defining features of packaging. By the way, the bag, even without frame qualities, has the necessary strength to work with bulk cargo. Sugar, flour in bags made of polyethylene fabric, cement and other building mixtures in bags made of multi-layer paper can be safely stacked on pallets, dropped, loaded and unloaded without harm to the contents. In addition, consumer packaging, while not being a container, can also have frame-supporting properties (for example, a corrugated cardboard box for a TV with foam inserts).

Soft packaging (polypropylene bags)

Another concept contrasts consumer packaging with packaging that is intended for logistics and production purposes. In the same example with pasta, the plastic bag is intended for the end consumer, in this packaging he brings the purchase home, and throws it away when the pasta runs out. The container does not reach the end consumer and he, most often, does not even see it. But it is repeatedly used by manufacturers, carriers, wholesale and retail trade enterprises.

There are also exceptions to this concept. For example, glass beer bottles are essentially consumer packaging. However, they are never called packaging, but are collectively called “glass containers” and even have the same defining quality of containers - turnover; glass containers can be used many times. And in general, the contrast between containers and packaging is not entirely correct, since containers are an element of packaging.

Glass containers

An important feature of packaging is its focus not on a specific product, but on the type of cargo. Thus, packaging is developed for a specific product, with all the appropriate prints and design features. Containers are developed for entire groups of goods, for example, for bulk goods, for liquids, for fruits.

Thus, although with reservations, we can define the main characteristics of packaging as follows:

- the container is intended for production and logistics purposes;

- the container may be intended for use more than once;

- the container has frame-bearing properties;

- the container is adapted not for a specific product, but for the type of cargo.

The main difference between the terms “packaging” and “container” is that packaging forms a consumer unit (with all the ensuing consequences), while packaging provides protection of the product from unwanted influences along the “production-logistics-sale” process. At the same time, taking into account that the container is an element of packaging, we can confidently say that the functions of the container largely coincide with the functions of packaging, and are divided into protective, optimizing and informational functions. (for more information about the functions of containers and packaging, see the article Packaging).

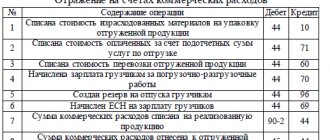

Accounting procedure for returnable packaging

Receipts from the seller of containers that are reused must be accounted for in Debit 41, subaccount Container and Credit in account 60 or account 76 for the actual purchase costs excluding VAT. In case of receipt of a large volume of containers of different types and at different prices, it is recommended to use accounting prices, which can be contractual, planned and calculated, etc., which a trade organization can set independently for a long period of time, and deviations from the actual cost of containers are written off as other income or expenses as financial results.

In payment documents, returnable packaging is reflected as a separate line at the price established by the contract, the cost of which is not included in the sales price of the goods.

Provided that the returnable container is transferred as collateral, the price in the payment documents is indicated as the collateral value of the container. According to the terms of the contract, in case of untimely return of the container, which is under security, the seller may reduce the amount of return of the security deposit or not return it if it is lost, damaged, etc.

Important! Returnable packaging must be taken into account at the collateral value reflected in the contract.

An example of reflecting transactions with returnable packaging

Alpha and Omega LLC shipped goods to Beta and Gamma LLC in returnable packaging - 50 pieces of plastic boxes. The deposit price of 1 box is 100 rubles. Based on the contract, within 10 days from the date of transfer of the goods, Beta and Gamma LLC is obliged to return the container. In fact, 45 boxes were returned, 5 boxes were lost.

Reflection of returnable packaging by the Supplier Alpha and Omega LLC (only for operations involving the movement of returnable packaging):

| Operation | Debit | Credit | Sum |

| returnable packaging was delivered to the buyer at the deposit value upon shipment of the goods | 76 | 41 subaccounts Tara | 5000 |

| deposit received for returnable packaging | 51 | 76 | 5000 |

| returnable packaging has arrived | 41 subaccounts Tara | 76 | 4500 |

| a deposit was transferred to the buyer for the returned packaging | 76 | 51 | 4500 |

The buyer of Beta and Gamma LLC reflected:

| Operation | Debit | Credit | Sum |

| returnable packaging has arrived | 41 subaccounts Tara | 76 (60) | 5000 |

| deposit of returnable packaging has been paid | 76 (60) | 51 | 5000 |

| the container was returned to the supplier | 76 (60) | 41 subaccounts Tara | 4500 |

| shortage of returnable packaging written off | 94 | 41 subaccounts Tara | 500 |

| the shortage is attributed to the perpetrators | 73 | 94 | 500 |

| Or: the shortage is written off in the absence of those at fault | 91 | 94 | 500 |

| reflected the return of the deposit reduced by the cost of the unreturned packaging | 51 | 76 (60) | 4500 |

If it is necessary to repair the container, then such expenses must be taken into account by the supplier in trading organizations in account 44 Sales expenses, and then written off from this account 44 to Debit 91 subaccount Other expenses.

Tax accounting of returnable packaging

Operations with returnable packaging are not sales turnover. Except when the goods are sold directly with packaging, then its cost must be included in the price of the goods and subject to VAT at the rate of the goods; in other cases, the packaging must be reflected separately.

Thus, the documents must indicate: “Deposit value of returnable returnable packaging, excluding VAT.” When selling goods in returnable containers, the deposit on the container, which must be returned to the seller, is not included in the tax base in accordance with clause 7 of Art. 154 Tax Code of the Russian Federation. That is, VAT does not need to be charged on the amount of the deposit of returnable packaging that is transferred to the buyer. In this regard, it is important to provide in contracts the procedure for making payments for returnable packaging at deposit prices, in the amount of the accounting value of the packaging from the supplier. The deposit value must ensure the return of the packaging. therefore the supplier collects a deposit from the buyer. Expenses for operations with containers must be taken into account in non-operating expenses based on paragraphs. 12 clause 1 art. 265 Tax Code of the Russian Federation.

If the returnable packaging at the deposit prices is not returned to the seller, then the amount remains with the seller and the ownership of the container passes to the buyer. This means that the sale must be reflected and VAT must be charged by the supplier. If the container is sold at a deposit value including VAT, which must be specified in the contract, then VAT must be calculated at a rate of 18/118%, and provided that the deposit value is without VAT, then a tax rate of 18% must be applied.

Also, an invoice is issued in 2 copies for the sold containers. The first is transferred to the buyer, and the second remains with the seller and is recorded in the sales book. In the same quarter, the amount of VAT reflected by the packaging supplier can be deducted. To do this, you need to separate it from the cost of the container using reversal postings.

Features of accounting for collateral containers

For some types of reusable packaging, according to the contract, the supplier may charge the buyer a deposit (instead of the cost of the container). Collection of a deposit for packaging is carried out in cases provided for in contracts and is a means of ensuring the buyer’s obligation to return the packaging.

The terms of the agreement may also provide for additional sanctions for failure to fulfill obligations to return the deposit container.

If the reusable packaging is returned to the supplier within the period stipulated by the contract, its deposit value is returned to the buyer or is counted, by agreement of the parties, to pay off the buyer's debt for goods already supplied or as an advance for future deliveries of goods.

If the container is not returned to the supplier within the terms stipulated by the contract, ownership of it passes to the buyer and the deposit value of the container is not returned to him.

In this case, the supplier must reflect the deposit value of the container as proceeds from its sale and charge VAT.

The amounts of the received (paid) collateral are reflected in account 76 “Settlements with various debtors and creditors” in correspondence with the cash accounts (both for the supplier and the buyer).

Accounting for collateral containers from the seller

The owner of returnable containers shipped to the buyer is the supplier. This container is not sold to the buyer, but is transferred to him for temporary possession and use.

After shipping the container to the buyer, the supplier does not write it off from his balance sheet, but must record the fact of this shipment, i.e. credit account 41.3. The question arises: which account should be debited? Some authors suggest using account 45 “Goods shipped” for this purpose. However, the instructions for using the chart of accounts indicate that account 45 “is intended to summarize information on the availability and movement of shipped products (goods), the proceeds from the sale of which cannot be recognized in accounting for a certain time...”. It follows that there will eventually come a time when this revenue will be recognized. One of the conditions for recognizing revenue in accordance with clause 12 of PBU 9/99 “Income of the organization” is the transfer of ownership from the seller to the buyer. However, this transition usually does not occur and, therefore, it is unlawful to use the score 45 in this case. In our opinion, the movement of returnable packaging (shipment to the buyer, return by the buyer) should be reflected within the account in which the deposited packaging is accounted for (for example, in separate sub-accounts: “Containers shipped to customers” and “Containers in warehouse”).

Clause 182 of the guidelines for accounting for inventories states that reusable packaging, for which deposit amounts are established in accordance with the terms of contracts, is accounted for at these amounts (hereinafter referred to as deposit prices). The difference between the actual cost of the container and its deposit price is taken into account by the supplier in the financial performance accounts as operating income and (or) expenses.

Main accounts:

Debit 41 subaccount 3 “Containers shipped to customers” Credit 41 subaccount 9 “Containers in warehouse” - shipment of containers to the buyer;

At the same time, in order to receive on account 62 “Settlements with buyers and customers” the total amount of the buyer’s debt (for shipped goods and the deposit for the packaging) for the collateral value of the packaging, the following entry should be made:

Debit 62 “Settlements with buyers and customers” Credit 76 “Settlements with various debtors and creditors” Debit 51 “Settlement accounts” Credit 62 “Settlements with buyers and customers” - receiving money from buyers for goods and the collateral value of containers; Debit 41 subaccount 9 “Containers in warehouse” Credit 41 subaccount 3 “Containers shipped to customers” - receipt of returnable packaging from the buyer; Debit 76 “Settlements with various debtors and creditors” Credit 51 “Settlement accounts” - return to the buyer of the deposit for packaging; Debit 76 “Settlements with various debtors and creditors” Credit 62 “Settlements with buyers and customers” - offset of the deposit for packaging to pay off the buyer’s debt for goods already delivered or as an advance for future deliveries; Debit 76 “Settlements with various debtors and creditors” Credit 91 subaccount 1 “Other income” - for the cost of collateral containers not returned by the buyer;

At the same time, a record is made:

Debit 91 subaccount 2 “Other expenses” Credit 41 subaccount 3 “Containers shipped to customers” Debit 91 subaccount 2 “Other expenses” Credit 68 “Calculations with the budget” - VAT is charged on the packaging sold.

In this case, the supplier must issue an invoice to the buyer for the amount of VAT.

Answers to common questions

Question No. 1 : How can the buyer reflect returnable packaging in accounting on off-balance sheet accounts?

Answer : Returnable packaging should not be included in the cost of products and its cost is highlighted in the primary documents as a separate line. The price of returnable packaging (deposit) is determined by the contract and the buyer transfers it to the supplier in case of non-return of the packaging. The supply agreement may provide that in order to fulfill the obligation to return the packaging, the organization is required to pay a deposit. Received containers are accounted for at the collateral value established in the contract. You need to make the following wiring:

| Operation | Debit | Credit |

| the amount of the deposit for the return of the packaging has been transferred | 60 (76) | 50 (51) |

| reflects the amount of the deposit for returnable packaging | 002 | |

| Returnable packaging received, paid separately | 10-4 (41-3) | 60 (76) |

| returnable packaging returned to the supplier | 60 (76) | 10-4 (41-3) |

| deposit returned | 50 (51) | 60 (76) |

| the deposit amount for the packaging was written off | 002 |

If the organization does not return the container (violates the contract), then the deposit is not returned and the amount of the deposit is considered as the purchased container. The following transactions are made:

| Operation | Debit | Credit |

| The receipt of returnable packaging at the cost of the deposit was reversed | 10-4 (41-3) | 60 (76) |

| containers were capitalized at cost (excluding VAT) | 10-4 (41-3) | 60 (76) |

| VAT on packaging is taken into account based on the invoice from the supplier | 19 | 60 (76) |

| deposit amount written off | 002 |

Returnable packaging is not a product for transactions subject to VAT (for resale) and VAT amounts are not accepted for deduction, but are included in the cost of the packaging. If the buyer returns the returnable container, the amount of the deposit does not increase the VAT base.

Accounting: return of packaging

When selling goods in returnable containers, make the following entries:

Debit 76 Credit 41-3

– reflects the transfer of returnable packaging to the buyer.

When returning containers, make the following entries:

Debit 41-3 Credit 76

– the return of packaging is reflected.

This procedure follows from the letter of the Ministry of Finance of Russia dated May 14, 2002 No. 16-00-14/177.

After the buyer returns the container, transfer to him the funds that were previously received to secure the obligation to return the container. When transferring funds to the buyer, make the following entry:

Debit 76 Credit 50 (51…)

– the deposit amount is returned to the buyer;

Credit 008

– the amount of the deposit returned to the buyer is written off.

This procedure is established in paragraphs 180–184 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia dated December 28, 2001 No. 119n, Instructions for the chart of accounts.

Advice : since at the moment the returnable container is transferred to the buyer, its cost is debited from account 41-3, organize control over its safety. This is necessary in order to know how many containers the buyer has and how many are in the organization. Since the legislation does not regulate such a procedure for accounting for returnable packaging, the organization must develop it independently.

In practice, to control the movement of returnable packaging for each department (or financially responsible person), off-balance sheet accounting can be maintained. The chart of accounts does not provide for a separate off-balance sheet account for accounting for returnable containers put into operation. Therefore, you need to open it yourself. For example, this could be account 014 “Returnable containers used for packaging goods sold.” Keep records on it both in quantitative and in total terms.

In this case, when selling goods in returnable containers, make the following entry:

Credit 014

– reflects the collateral value of returnable packaging transferred to the buyer of the goods.

When returning containers, make the following entries:

Debit 014

– the return of packaging is reflected.

Fix this option in the accounting policy of the organization for accounting purposes (clause 4 of article 8 of the Law of December 6, 2011 No. 402-FZ).

If the buyer does not return the container, do not return the deposit to him. In this case, take into account the amount of the deposit as part of other income (clause 7 of PBU 9/99).

Make the following entries in your accounting:

Debit 76 Credit 41-3

– the collateral value of returnable packaging transferred to the buyer of the product was reversed;

Debit 41-3 Credit 19

– input VAT included in the cost of packaging has been reversed;

Debit 68 subaccount “VAT calculations” Credit 19

– input VAT relating to the cost of unreturned packaging has been accepted for deduction;

Debit 62 Credit 91-1

– sales of packaging not returned by the buyer are reflected;

Debit 91-2 Credit 68 subaccount “VAT calculations”

– VAT is charged on the sale of unreturned packaging (if the organization’s activities are subject to VAT);

Debit 91-2 Credit 41-3

– the collateral value of the sold packaging is written off;

Credit 008

– the amount received to secure the obligation to return the packaging is written off;

Debit 76 Credit 62

– the amount of the deposit received is credited as payment for the sold containers.

Also write off any previously incurred deferred tax asset or deferred tax liability.

Such rules are established in the Instructions for the chart of accounts (accounts 62, 68, 76, 91).

To account for the movement of containers, fill out a report using the TORG-30 form. The container report must be drawn up by the financially responsible person in two copies. One copy is transferred to the accounting department along with the product report and the primary documents on the basis of which the reports were compiled. This procedure is provided for in the instructions approved by Resolution of the State Statistics Committee of Russia dated December 25, 1998 No. 132.

When writing off returnable packaging due to normal wear and tear or sale, make the following entry:

Debit 91-1 Credit 41-3

– the cost of the container is written off.

This procedure is provided for in paragraph 190 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia dated December 28, 2001 No. 119n.

The procedure for accounting for the containers in which an organization packages sold products when calculating taxes depends on what taxation system the organization uses.