- August 31, 2019

- Accounting

- Marina Lobacheva

Companies use a cash book to keep track of cash. It is used by both companies and private entrepreneurs. With its help, the procedure for preparing various financial statements is greatly simplified. Filling out the cash book is carried out by an appointed responsible specialist, who is vested with the appropriate powers based on the order of the head of the company. Usually it is represented by an accounting employee, but some individual entrepreneurs carry out this process independently.

Why is a cash book needed?

Based on the information contained in this document, the financial condition of any company is monitored. It can even be used by tax authorities auditing a company. Additionally, the book is useful for the head of any company, since with its help you can easily understand how much money the company receives, as well as how much money is spent on certain purposes.

The cash book is mandatory documentation, and it is presented in each company in a single copy. According to the law, it is not allowed to maintain several books containing different data at once.

Who is in charge?

Filling out the cash book can be done by hand or using a computer. This process is carried out by a cashier or accountant who is appointed responsible for maintaining the book using a special order. He is represented by the financially responsible person. His responsibilities include the following:

- competent filling of the cash book;

- issuance and acceptance of money or other material assets and securities;

- acceptance and issuance of various accountable documentation;

- filling out income or expense cash orders that are required when issuing salaries or bonuses;

- control over various cash transactions.

The activities of the cashier are controlled by the chief accountant of the enterprise. If a businessman is an individual entrepreneur, then he independently fills out this document.

Cash book: how to conduct it correctly (2020)

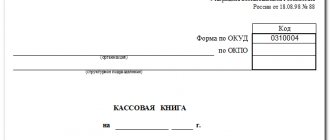

Accounting for financial transactions of a non-profit organization or LLC should be kept on a unified cash book form (OKUD code 0310004). The unified document form KO-4 was approved by Resolution of the State Statistics Committee No. 88 of August 18, 1998. The filling procedure is presented in paragraph 2 of Instructions No. 3210-U.

Cash book, form (download word)

This form is intended for chronological registration of details of incoming and outgoing cash orders, on the basis of which cash flows in the institution.

The legislation allows several ways of maintaining a book:

- drawing up documents by hand on prepared forms;

- filling out a table on a computer and then printing the completed pages;

- the report can be prepared in specialized accounting programs, electronically, with the subsequent generation of an electronic document certified by an electronic signature.

The cashier or other official determined by order of the manager must fill out the rows and columns of the form, as well as carry out transactions with cash. It is possible to transfer the management of the cash book to a representative of the outsourcing organization. Finding such a company is not difficult, for example, look for advertisements in Moscow.

Filling rules

Each person appointed as the person responsible for filling out this documentation must understand how to properly maintain a cash book. To do this, the following rules and requirements are taken into account:

- data is entered into the documentation on the basis of special instructions issued by the Central Bank;

- It is allowed to maintain a document in paper or electronic form;

- Only forms that have a strictly established form are used for these purposes;

- It is not allowed to use your own form developed by employees of a separate company, since the law requires a single format to be used;

- a new book begins every year, so at the end of the year it can be used to determine how much money was earned and spent by the company;

- it is important to correctly number each sheet of the book, so skipping pages is a gross violation;

- all pages must be stitched together, and at the end the number of available sheets is written down;

- the document bears the signature of the director of the enterprise, as well as the seal of the company;

- If the book is kept in printed form, then two identical copies are made at once.

When maintaining documentation, the responsible person must strive to ensure that there are no blots, errors or corrections.

Features for e-readers

Filling out the cash book manually is becoming less and less common, as many companies prefer to switch to electronic document management. Therefore, this document is filled out electronically. To complete this process correctly, the following rules are taken into account:

- as soon as the document is completely filled out, it must be printed;

- printed documentation is stapled and signed by the director of the company;

- if the responsible person in the company is responsible for maintaining the cash register in electronic form, then it is allowed to register the book quarterly;

- entries must be made daily by a designated person;

- The balance of money in the account must be indicated at the beginning of the day, and at the end of the day the total is summed up based on the transactions performed for one day of work;

- any transactions carried out during the day must be indicated in the book.

The advantages of using the electronic version include the fact that if the cashier makes any mistake for various reasons, it can be easily and quickly corrected.

How to fill out a cashier-operator log in 2021

Cashier-operator journal form according to the KM-4 form

• Download the current KM-4 form (Excel format).• Download sample filling KM-4.

— Instructions for filling —

The log is filled out based on Z-reports at the end of the shift.

Click on each instruction field of interest to see detailed information.

COUNT 1 “Date (shift)”

Enter the shift date indicated in the Z-report. For example, 01/13/15.

If, for example, you work around the clock and have 2 shifts on one date, then you can add the shift number to the date - 01/13/15 (2).

BOX 2 “Department (section) number”

Usually this column is not filled in in any case.

In addition, many cash registers do not provide division into departments in Z-reports. But if we talk about all the possible filling options, it might look like this:

If the cash register serves 1 department:

— put the number 1

- leave the column empty

- put dashes

If the cash register serves more than 1 department:

— enter the numbers of the departments for which the amounts were allocated for a given shift

- leave the column empty

- put dashes

COUNT 3 “Last name, first name, patronymic of the cashier”

The full name of the cashier-operator is indicated, i.e. a person who worked at the cash register during the specified shift.

COUNT 4 “Sequence number of the control counter (fiscal memory report) at the end of the working day (shift)”

The serial number of the Z-report is entered in the column. Indicated on the Z-report itself.

Depending on the cash register model, it is printed differently, for example, Z-report No. 0001, Z 0001, CLOSED. SHIFT 0001.

COUNT 5 “Sequence number of the control counter (fiscal memory report) recording the number of transfers of the summing money counter readings”

This form of the cashier-operator book is outdated and now this column is essentially useless, so it is better not to fill it out at all.

However, some put the number of sales per shift in this column, others duplicate column 4, i.e. put the serial number of the Z-report.

COUNT 6 “Readings of summing cash counters at the beginning of the working day (shift)”

• This is the so-called. cumulative total. On the Z-report it can be written as, for example, GROSS TOTAL, ACCRUAL TOTAL OF SALES, or just two letters NI.

• This column records the amount at the beginning of the day of all the money entered on this cash register for the entire period of its operation from the moment of registration, the so-called. cumulative total.

• If the cash register is new, then the first amount written will be 1 rub. 11 kopecks, which is stamped at the tax office during registration.

• The amount in this column must be equal to the amount in column 9 for the previous shift (day). We take the data from it:

• You can also find out the amount of the cumulative total from the morning X-report, if, of course, this data is reflected in it, which is not supported in all cash registers.

BOX 7 and 8: Signature of the cashier and administrator

The cashier and administrator are signed at the end of each shift.

If these “positions” are represented by one person, then sign in both columns.

COUNT 9 “Readings of summing cash counters at the end of the working day (shift)”

Simply put, this is the sum of all the money spent since the registration of the cash register plus the revenue for the current shift (day).

Written off from the evening Z-report at the end of the shift.

Formula: 6 columns + 10 columns = 9 columns.

This amount can be immediately entered into column 6 for the next shift.

COUNT 10 “Amount of revenue per working day (shift)”

Indicate the revenue (cash + non-cash + returns) per shift (day), entered on the cash register.

The revenue amount is printed on the evening Z-report.

Formula: 9 columns - 6 columns = 10 columns.

Check the data from the Z-report with the data in the formula - they must match.

BOX 11 “Deposited in cash”

The actual amount of cash deposited into the cash register at the end of the shift is entered.

This amount does not include:

- cashless payments

-refunds

Formula: 10 columns - 13 columns - 15 columns = 11 columns

BOX 12 “Paid according to documents, quantity”

The number of sales by bank transfer (bank cards, checks, etc.) is reflected.

If there were no non-cash payments, put a dash or leave the line empty.

Also, you don’t need to enter anything when you can’t count the number of such payments, because besides, many cash registers do not have counters for non-cash transactions.

BOX 13 “Paid according to documents, amount”

The actual amount of all non-cash payments made is recorded.

BOX 14 “Total delivered”

The total amount of all funds for cash and non-cash payments minus returns to customers and erroneously punched checks is reflected.

Formula: 10 columns - 15 columns = 14 columns.

BOX 15 “Amount of refunds”

The total amount of all returns and erroneously punched checks is indicated.

You can write off the amount from the Z-report.

Formula: 14 columns + 15 columns = 10 columns.

BOX 16, 17, 18: Signatures of responsible persons at the end of the shift

The signature of the cashier, administrator, and manager is affixed.

If these “positions” are represented by one person, then he must sign in all the boxes.

Instructions for filling

If the cashier is not well versed in this work, then he should study an example of filling out a cash book. In fact, the procedure is considered quick and simple. To do this, you just need to follow the correct instructions:

- The book begins with a title page, which contains general information about the entrepreneur or company;

- indicate the personal data of the individual entrepreneur, provided by his full name, date of birth and passport details;

- if a document is filled out in a company, then its name, legal address and other significant details are provided;

- the title page indicates the period for which the documentation is kept;

- Next, the usual sheets of the book are filled in, intended for entering information about all operations carried out during the working day;

- each leaf has two parts that can be easily torn off;

- At the top is the date the information was entered, as well as the sheet number;

- Next is a table with 5 columns;

- the table indicates the document number, the entity from which the money was received or to whom the funds were issued, the account number, as well as the amount of income and expenses;

- at the end the balance at the beginning and end of the day is given;

- if after filling out the table there are empty lines left, then they should be crossed out using a capital letter Z, so that in the future it is impossible to enter any false information into the cash book;

- at the end of the sheet the signature of the cashier responsible for maintaining documentation is placed.

A sample of filling out the cash book can be found below.

Sample of filling out the cashier's journal

Let's look at how to fill out the cashier's journal.

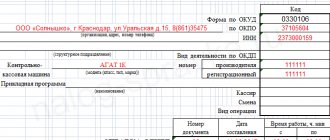

The design of a document begins with the cover. In the appropriate fields you must indicate the full name of the company, its address and contact telephone number. The code is also indicated here according to the OKPO classifier.

If the cash register is located in a specific structural unit, its name is written in the column below.

Then the name of the cash register is indicated. In the column on the right you also need to enter the manufacturer and registration numbers. They differ in that the manufacturer's number is assigned at the factory and can usually be found in the passport and on the cash register body. The registration number is the number that the device received from the tax office.

Under the title of the document, the start and end dates of filling out the journal, as well as the position and full name are indicated. person responsible for this.

The log is filled line by line, with one line allocated to each Z-report. It is not permissible to omit them or summarize multiple reports into one entry.

Column 1 contains the date for which the report was withdrawn from the cash register.

Column 2 indicates the number of the department for which the amount was entered. This column is not filled in if there are no departments in the cash register, or only one is used.

Rules for correcting information

Often, in the process of maintaining documentation, responsible persons make some mistakes. Filling out a cash book is considered a simple process, but there is always a chance that incorrect information will be entered. Various clerical errors or typos, as well as corrections, are not welcome in official documentation.

Any correction may be considered a violation by the company, and therefore the person responsible may be subject to disciplinary action. Only minor errors are allowed that are not related to the indicated amounts and do not affect the summary. How to fix errors? For this, the following rules are taken into account:

- incorrect data is simply crossed out;

- The correct information is written at the top;

- a correctly corrected error is certified by the signature of the responsible cashier and accountant who checks the documentation;

- if errors are identified related to the size of the balance, then the sheet in the book is completely crossed out, after which a mark is made to cancel it;

- After crossing out one sheet, the second sheet is filled in.

It is the cashier who is responsible for filling out the document correctly, so if they make serious mistakes, it is important to draw up a special memo addressed to the company’s chief accountant. This note is reviewed by a specially created commission, after which the necessary changes are made. The accountant generates a certificate of the adjustments made. Only after this the page is canceled.

Stitching rules

The cashier appointed as the person responsible for maintaining documentation must understand not only the rules for filling out the cash book, but also the specifics of stitching it together. All sheets must be numbered and stitched. For this, high-quality special threads are used. After tying them, they should be on the back of the document.

A small piece of paper containing information about the number of sheets is glued to the unit. The information is certified by the company seal, after which the sheet is signed by the director.

Features of management

Individual entrepreneurs may not be responsible for maintaining a cash book, but they must keep records of their expenses and income. Therefore, it is most important to use this document for this purpose. If a businessman uses a cash book, then he must follow the rules for its design. There is no requirement to indicate the cash balance limit, and entrepreneurs do not draw up cash orders.

Companies are required to follow all requirements for this documentation. If there are errors or violations, this may become the basis for a more thorough inspection by Federal Tax Service employees.

An example of filling out a cash book manually can be studied below.

Book of the cashier-operator

Synthetic and analytical accounting.

course work, added 02/27/2013

Document: approach, variety and significance. Types of e-books: e-books, e-readers, travelers, etc.

The concepts are “book”, “document”, “seen” and their publications. The main characteristics of an electronic book, the concept of power.

course work, added 05/28/2010

Analysis of the state of accounting and on-farm control of the use of funds in the cash register of the enterprise. The procedure for conducting cash transactions, their documentation and accounting. Generating a cashier's report. Inventory of funds.

course work, added 09/11/2015

Carrying out shipment of goods according to transport and accompanying documents of the sender, certifying their quantity. Issuing a receipt upon sale. Reflection of revenue for the day in the book of the cashier-operator. Release of goods based on the “Order-selection sheet”.

test, added 05/22/2010

Economic essence and organization of cash circulation. Conducting cash transactions in the Republic of Belarus. Documentation of cash transactions. Procedure for maintaining a cash book. The procedure for checking and accounting processing of cashier's reports.

course work, added 08/19/2012

Maintaining cash register and cash book. Responsibilities of a cashier, instructions for ensuring the safety of funds. Basic practical aspects of cash payments. Accounting for external payments. Non-payment under contracts. Cash payments.

course work, added 04/07/2012

Requirements for filling out, processing and storing primary documents and registers in the organization. Document flow system for primary accounting documents. Development of assumptions and recommendations for improving document flow in the enterprise.

course work, added 06/07/2015

Is it possible not to print an electronic document?

Companies have the right to maintain a cash book electronically without printing it. In this case, the enterprise completely switches to electronic document management. The basis for filling out the cash book is any financial transaction performed in the company.

The ability to maintain documentation exclusively in electronic form appears only after the company purchases certain technical equipment. They are the ones who ensure data protection from fraudsters and hackers. By using them, it is ensured that the person in charge cannot in any way make a mistake. Additionally, documentation is protected from loss of information.

All electronic samples of the book must be signed using an electronic signature, which must meet the conditions of Federal Law No. 63. The electronic version is slightly different from the paper document in appearance, but it contains the same rows and columns.

If an entrepreneur decides to switch completely to the electronic version of the book, then he must prepare for serious expenses associated with the purchase of expensive equipment. The selected cashier must be able to operate this equipment.

How to fill out a cash book: algorithm

The employee responsible for filling out cash documents, including the cash book, is appointed by order of the manager. This may be a cashier, accountant, chief accountant, other official, and in the absence of such, the manager himself, or an individual providing accounting services, can manage the cash book and other cash documents.

The basis for making entries in the cash book are incoming and outgoing cash orders. Orders have continuous numbering; they are used to document each receipt or issue of cash. Entries in the cash book are made only for the days when there was movement in the cash register.

General algorithm for filling out the cash book:

- at the beginning of the day, the cash balance is indicated, which should be equal to the balance at the end of the previous day;

- entries are made in the book for each incoming and outgoing order issued during the day;

- at the end of the working day, the cash book summarizes the receipts and expenditures of “cash” and displays the balance at the end of the day.

How to keep a cash book if there was no movement at the cash register during the day? There is no need to reflect such a day in the cash book.

Having verified the amount of cash remaining in the cash register at the end of the day, the turnover and the balance displayed in the cash book, the cashier certifies the entries made in the book with his signature, and then passes them along with the cash documents for verification to the chief accountant, or manager.

It is allowed to make corrections to the cash book, unlike cash orders, but only if they are certified by the signatures of the persons who made these changes and their transcripts, and the date of the correction is indicated.

The cash book, along with other cash documents, must be kept in the organization for at least 5 years.