Errors in settlements with accountable persons can lead to fines for cash violations, as well as additional personal income tax and contributions.

Therefore, it is important to correctly process the issuance of money against the report and avoid mistakes when filling out the advance report. See a sample of filling out an advance report in 2021, to which the inspectors will have no questions. [td]How you can’t give out money on account

When is it necessary to fill out an advance report?

An advance report is a primary document that confirms the amounts of money spent by accountable persons. The document is required to confirm the target expenditure of money.

The advance report is compiled and submitted to the accounting department by accountable persons who were given an advance for the needs of the organization or individual entrepreneur. The period within which the employee is required to report to his employer is three working days from the date:

- the expiration of the period for the provision of amounts specified in the application for the issuance of money on account;

- a person’s return to work when the deadline expires during a period of illness or vacation;

- returning from a business trip.

Please note: an entrepreneur has the right to withdraw money from his current account and spend it for any purpose - both for his own activities and for personal needs. He does not need to prepare an advance report on the amounts spent.

***

So, we found out that the advance report is used to confirm that accountable funds were spent as intended. The document is partially filled out by the employee and sent to the accounting department. The latter, when conducting the document, must put a number on it. Numbering is carried out in such a way that it is convenient for the business entity itself.

Similar articles

- Sample advance report for a business trip

- Payment order number

- Advance report on business trip 2016-2017 (sample)

- How to correctly fill out an advance report - sample?

Advance report: form 2021

There is no official advance report form for 2021, which is mandatory for everyone. You can develop the expense report form yourself, taking into account the specifics of the company’s work. But it is more convenient to use a unified advance report on the AO-1 form (OKUD code 0302001). The form was approved by Decree of the State Statistics Committee of Russia dated August 1, 2001 No. 55 and must contain the following information:

- on the amount of funds issued on account;

- about the accountable person (full name, position, structural unit);

- about the previous advance (balance, overexpenditure);

- on the appointment of an advance;

- accounting records and others.

Whatever form you decide to use, it must first be approved by the manager in the appendix to the order on accounting policies.

Advance report form 2021[/td]

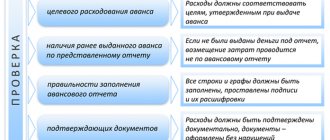

The advance report form is filled out by employees to whom the company has provided funds in advance. The advance report should answer the following questions:

- whether there are cost overruns;

- whether the documentation (checks, certificates, receipts) was provided in a timely manner;

- whether the persons responsible for the expenditure of advance funds have a debt to the enterprise;

- Is it necessary to deduct a certain amount of material resources from reporting employees from their salaries to pay off advance debt?

How to fill out an advance report in 2021

The document is drawn up in one copy. Based on the approved report, the accounting department writes off the accountable amounts as expenses, the employee deposits the unspent advance payment into the cash register, and the accounting department also issues the employee the amount of overexpenditure according to the expense cash order.

The advance report consists of the front and back sides, as well as a receipt. The document is drawn up by the accountant and the accountant: each of them fills out their part.

Front side

The expense report is filled out by the employee, but you can do it for him. You should indicate the name of the company, report number, date, surname and initials of the reporting person, its structural unit and personnel number, position, as well as the purpose of the advance.

Also in the advance report there is a table that indicates information about the previous advance, money received, expenses and balance. If the advance was issued in a foreign currency, the amount is indicated in line 1a in two currencies.

On the reverse side

In the advance report, the employee lists supporting documents (receipts, transport documents, cash and sales receipts, etc.), and the corresponding amounts of expenses.

After checking the expense report, fill out the “Accounting entry” table. Indicate the corresponding accounts and amounts. Put a mark to check the report.

In numbers and words indicate the amount in which the report is approved. Next, put the signatures and transcripts of the signatures of the accountant and the chief accountant, as well as the amount of the balance or overexpenditure (if any) and the details of the receipt (expense) documents for which funds are deposited/issued.

You can fill out the document either on paper or electronically. But if the company issues expense reports electronically, then they will need to be printed so that employees can sign them.

Employees must attach documents confirming expenses to the expense report. Documents are needed to confirm and justify expenses when calculating income tax. Before filling out the expense report, it is safer to generate supporting documents in chronological order, check their correctness and number them.

Preparing an advance report for a business trip - example in 1C 8.3

As a result of entering data on daily allowances and air tickets according to the above algorithm, an advance report is obtained, a sample of which you can.

The specificity of the activities of some budgetary institutions is associated with the need to send a large number of letters and telegrams. There are several options for sending correspondence. Each organization chooses the most convenient method for itself, depending on which the reflection of transactions for payment of postal services in accounting has its own characteristics. The article discusses the specifics of sending correspondence in different ways, as well as the procedure for reflecting these operations in accounting. Yu. Vasiliev There are several options for paying for sending correspondence by budgetary institutions:

– payment for postal services through an accountable person; – use of franking (marking) machines when paying for postal services; – payment for postal services using an advance book.

Let's consider how, using one or another method of sending correspondence, these transactions should be reflected in accounting.

Payment for postal services through accountable persons

The procedure for paying for postal items through accountable persons is extremely simple and does not differ from the usual procedure for paying for the purchase of household materials through these persons. By order of the head, a person is appointed who is responsible for receiving funds from the institution's cash desk to pay for postal services for sending correspondence. An agreement on financial liability is concluded with him, the standard form of which is approved by the Resolution of the Ministry of Labor and Social Development of the Russian Federation dated December 31, 2002 No. 85 “On approval of lists of positions and work replaced or performed by employees with whom the employer can enter into written agreements on full individual or collective (team) financial liability, as well as standard forms of agreements on full financial liability.”

To receive funds from the institution's cash desk, you must write an application and indicate in it that the funds are taken from the cash office to pay for postage. Quite often, accountants of budgetary institutions ask the question: for how long are funds from the institution’s cash desk given to the accountable person? As stated in clause 11 of the Procedure for conducting cash transactions in the Russian Federation, approved by Letter of the Central Bank of the Russian Federation dated October 4, 1993 No. 18, institutions have the right to issue cash on account to pay for business and operating expenses (their list also includes expenses for payment for communication services) authorized enterprises and organizations, individual divisions of economic organizations, including branches that are not on an independent balance sheet and located outside the area of operation of the institution, in amounts and for periods determined by the heads of the enterprises. Thus, if funds are issued on account to pay for postal services of a branch or subordinate institution, then the period for their issuance is limited by order of the manager. As a rule, this period is a month. The accountable person receives funds from the institution's cash desk at the beginning of the month and reports for them at the end of the month. However, other options are possible, for example a week. When funds are received to pay for postal services by the parent organization, the period for their issuance is also approved by order of the manager, although this is not directly stated in the said letter. The period for issuing funds to pay for postal services can be three days, a week, a month, etc.

Persons who received cash on account are required, no later than three working days after the expiration of the period for which they were issued, to submit an Advance Report to the accounting department (f. 0504049). It is accompanied by documents confirming the expenses incurred, usually a cash register receipt, receipts, invoices. If postal items are registered (registered, with declared value, ordinary), which in practice happens most often, then a receipt and an inventory of the contents are attached to the cash register receipt. According to the Rules for the provision of postal services, approved by Decree of the Government of the Russian Federation dated April 15, 2005 No. 221, the receipt reflects the type and category of postal item (postal order), the name of the addressee (name of the legal entity), the name of the postal facility of destination, the number of the postal item ( postal transfer). The list of attachments indicates the list of documents included in the sent letter (parcel).

In accordance with Order of the Ministry of Finance of the Russian Federation dated December 8, 2006 No. 168n “On approval of budget classification,” expenses for postal services are taken into account under subarticle 221 “Communication services” of the ECR.

In accounting, transactions involving the issuance of amounts for payment of postal expenses are reflected in the following accounting entries:

– the amount of funds to pay for postage was issued from the cash register for reporting:

Debit of account 208 04 560 “Increase in accounts receivable of accountable persons for payment for communication services”

Credit to account 201 04 610 “Disposals from cash”

– the accountable person reported for the expenses incurred:

Debit account 401 01 211 “Expenses for communication services”

Debit of accounts 201 05 510 “Receipts of monetary documents” (in case an accountable person purchases stamps and envelopes for sending correspondence), 208 04 660 “Reduction of accounts receivable of accountable persons for payment for communication services”

– the unspent balance of the accountable amount is returned:

Debit account 201 04 510 “Receipts to the cash desk”

Account credit 208 04 660 “Reduction of accounts receivable of accountable persons for payment for communication services”

Providing postal services using franking machines

Postal services for sending correspondence can be provided to institutions using franking or marking machines. In terms of their functional orientation, they differ from each other slightly. What is a franking (labeling) machine and what are its functional characteristics?

Franking machine (marking machine) is a machine designed for applying state postal payment marks to written correspondence, confirming payment for postal services, the date of receipt of this correspondence and other information. The amount of postage and the date of departure are set by the forwarder on the dialing mechanism of the marking drum, and the next item number is dialed automatically. Using a labeling machine, postal expenses are kept track of for non-cash payments with communication organizations.

To make payments using a franking (marking) machine, the organization enters into an agreement with the post office for its service. However, a contract alone is not enough to operate a franking machine. You must obtain permission to use it. According to the Order of the Ministry of Information Technologies and Communications of the Russian Federation dated September 29, 2006 No. 127 “On approval of the administrative regulations of the Federal Service for Supervision in the Field of Communications for the execution of the state function of issuing permits for the use of franking machines” (hereinafter referred to as the Administrative Regulations), the state service for obtaining a permit is provided on the basis of a written application to the territorial body of Rossvyaznadzor. The application can be sent by mail or delivered by the applicant directly to the territorial body of Rossvyaznadzor, in the territory of whose authority the franking machine is supposed to be used.

The application shall indicate (clause 6.3 of the Administrative Regulations):

– full name of the legal entity (full name of the individual entrepreneur), its location (place of residence) and postal address, TIN (for a branch, additionally KPP), telephone, fax;

– name of the model (series) of the franking machine; – installation location of the franking machine; – possible date and time of the inspection.

The following are attached to the application:

– a copy of the technical passport of the franking machine; – a notarized copy of the certificate of registration of the owner of the franking machine with the tax authority; – a copy of the agreement with the federal postal service organization (branch of the organization) for the provision of postal services using a franking machine (for federal postal organizations (their branches) that own franking machines, it is not required to submit an agreement for the provision of postal services); – copies of certificates of conformity; – imprint of the cliche of the franking machine.

After submitting all of the above documents, within 30 days from the date of registration of the application for a permit, Rossvyaznadzor issues a permit. Its validity period is unlimited. There is no fee for processing applications and issuing permits from applicants. If the permit is lost or damaged, a new one is issued.

Marking machines can:

1) summarize the postal expenses incurred by the organization;

2) subtract postage from the original amount set on the cash register counter.

The most convenient option for budgetary organizations (especially when paying for postal expenses from budgetary funds) is the summation of expenses incurred by the postal organization. In this case, you can avoid paying advance payments. A post office worker takes monthly readings of the franking machine meter. Based on the meter readings, an invoice (invoice) is issued at the beginning and end of the month, to which a certificate of completion of work is attached. In accounting, these transactions will be reflected as follows:

– for the amount of correspondence sent:

Debit account 401 01 221 “Expenses for communication services”

Credit to account 302 04 730 “Increase in accounts payable for settlements with suppliers and contractors for payment for communication services”

– for the amount of payment made:

Debit of account 302 04 830 “Reduction of accounts payable for settlements with suppliers and contractors for payment for communication services”

Credit accounts 304 05 221 “Settlements for payments from the budget with bodies organizing the execution of budgets for payment for communication services”, 201 01 610 “Retirement of funds of the institution from bank accounts”

If the marking machine deducts the postage from the original amount set on the counter of the cash register, the organization must transfer to the post office account a certain amount of money, which is an advance. The post office technical worker “loads” into the machine indicators equivalent to the amount of payment made. When stamping an envelope for sending, the operator (employee of the organization) indicates the amount of sending, which is subtracted from the balance of the amount entered into the machine’s memory, and is affixed to the envelope or a sticky sticker. When the cash register counter reaches zero, the labeling machine automatically turns off. In other words, the machine stops working if the entire amount deposited into the account of the postal institution has been spent.

In this case, transactions for payment of postage expenses will be reflected in the accounting records as follows:

– for the amount of the advance payment:

Debit of account 206 04 560 “Increase in accounts receivable for advances issued for communication services”

Credit accounts 201 01 610 “Retirement of institution funds from bank accounts”, 304 05 221 “Settlements for payments from the budget with bodies organizing the execution of budgets for payment for communication services”

– crediting the advance against the amount of postal services provided to the institution during the month:

Debit of account 302 04 830 “Reduction of accounts payable for settlements with suppliers and contractors for payment for communication services”

Credit to account 206 04 660 “Reduction of accounts receivable for advances issued for communication services”

Please note: Decree of the Government of the Russian Federation dated February 23, 2007 No. 126 “On measures to implement the Federal Law “On the Federal Budget for 2007” does not limit the size of the advance payment when making settlements with suppliers and contractors at the expense of budgetary funds. Let us recall that last year it also amounted to 100% of the cost of concluded agreements (contracts) (clause 37 of the Government of the Russian Federation of 22.02.2006 No. 101 “On measures to implement the Federal Law “On the Federal Budget for 2006”).

Example 1.

The budgetary institution makes payments to the post office using a franking machine, which summarizes the postal items produced. At the end of the month, the budgetary institution received an invoice in the amount of 3,562 rubles. (including VAT - 543.36 rubles) and a certificate of completion of work with a register of completed shipments. Payment for postage costs is made from budget funds.

The following entries will be made in accounting:

| Debit | Credit | Amount, rub. | |

| Accrued expenses for postal services provided | 1 401 01 221 | 1 302 04 730 | 3 562 |

| Postage paid | 1 302 04 830 | 1 304 05 221 | 3 562 |

Payment for postal services using an advance book

Payment for postal services can be made not only with the help of accountable persons, franking (marking) machines, but also with the use of an advance book. The organization enters into an agreement with the post office, the subject of which is payments for postal services using an advance book. Then an advance book is purchased, which is stored not at the institution’s cash desk, but at the post office. The organization transfers funds to the post office account as an advance against the subsequent sending of telegrams and letters. Payment information is entered into the organization's advance book. As correspondence is sent, the advance book is used up.

Practice shows that when paying for postal services using an advance book, accountants have difficulty recording transactions for paying postage expenses and purchasing an advance book. Is the advance book a monetary document or can it be reflected in accounting as an inventory? How is the replenishment of the advance book reflected in accounting?

According to the author, the advance book is not a monetary document, therefore, when purchasing it, you should not use account 201 05 000 “Cash documents”. An advance book is a printed product, therefore, its purchase, in accordance with paragraph 66 of Instruction No. 25n, should be reflected as follows:

– the purchased advance book is accounted for:

Debit of account 105 06 340 “Increase in the cost of other inventories”

Credit to account 302 22 730 “Increase in accounts payable for the acquisition of inventories”

– the cost of the advance book has been paid:

Debit of account 302 22 830 “Reduction of accounts payable for the acquisition of inventories”

Credit accounts 201 01 610 “Retirement of institution funds from bank accounts”, 304 05 340 “Settlements for payments from the budget with bodies organizing the execution of budgets for the acquisition of inventories”

As for the transfer of funds to pay for postal services, in practice the following options for reflecting this operation can be used:

– funds were transferred to the post office:

Debit of account 302 04 830 “Reduction of accounts payable for settlements with suppliers and contractors for payment for communication services”

Credit accounts 201 01 610 “Retirement of institution funds from bank accounts”, 304 05 221 “Settlements for payments from the budget with bodies organizing the execution of budgets for payment for communication services”

– for the amount of replenishment of the advance book:

Debit account 201 05 510 “Receipt of cash documents”

Credit to account 302 04 730 “Increase in accounts payable for settlements with suppliers and contractors for payment for communication services”

– expense of the advance book:

Debit of account 208 04 560 “Increase in accounts receivable of accountable persons for payment for communication services”

Account credit 201 05 610 “Disposal of monetary documents”

– report of the accountable person for sent correspondence:

Debit account 401 01 221 “Expenses for communication services”

Account credit 208 04 660 “Reduction of accounts receivable of accountable persons for payment for communication services”

However, the latter method of reflecting accounting records is not entirely correct, because:

– the post office, which is not a reporting entity of the organization, is accountable for the services provided for sending correspondence;

– replenishment of the advance book is incorrectly considered as the receipt of monetary documents, since in fact monetary documents are not purchased. The advance book in this case is a way to control the transferred advance and its expenditure;

– the use of account 302 04 000 “Settlements with suppliers and contractors for payment for communication services” when paying an advance contradicts the budget accounting methodology set out in Instruction No. 25n.

According to the author, in accounting, settlements with the post office for services rendered should be reflected as follows:

– advance payment for postal services is listed:

Debit of account 206 04 560 “Increase in accounts receivable for advances issued for communication services”

Credit accounts 201 01 610 “Retirement of institution funds from bank accounts”, 304 05 221 “Settlements for payments from the budget with bodies organizing the execution of budgets for payment for communication services”

– the post office presented an invoice, a register of poisoned correspondence, and a certificate of completion of work:

Debit account 401 01 221 “Expenses for communication services”

Credit to account 302 04 730 “Increase in accounts payable for settlements with suppliers and contractors for payment for communication services”

– the advance was offset against the amount of postal services provided to the institution during the month:

Debit of account 302 04 830 “Reduction of accounts payable for settlements with suppliers and contractors for payment for communication services”

Credit to account 206 04 660 “Reduction of accounts receivable for advances issued for communication services”

Example 2.

The budgetary institution makes payments to the post office through an advance book, the cost of which is 15 rubles. The amount of funds credited to the advance book is 2,640 rubles. (including VAT - 398.14 rubles). At the end of the month, the budgetary institution received an invoice in the amount of 1,580 rubles. (including VAT - 241.02 rubles) and a certificate of completion of work with a register of completed shipments. Payment for postage costs is made from budget funds.

The following entries will be made in accounting:

Expense reports can occur even in the smallest organization. Making an expense report in 1C is not difficult; this operation is fully automated. In this article we will look at how to prepare an expense report in 1C Accounting 8.3 step by step using specific examples as examples.