In the process of carrying out entrepreneurial activities, an organization may face the problem of a lack of finances to meet its needs. Under these conditions, it has to borrow money from other commercial firms or from its founders. Loans can be issued for use on interest-bearing terms or without them. It is important to know how to process transactions for a loan from the founder in 1C 8.3.

Accounting for interest-bearing and interest-free loans

Loans issued with or without the payment of additional income are accounted for in various ways. When applying for an interest-bearing loan, the company bears costs. In contrast, the founder of the company receives income. The amount of costs for paying interest commissions reduces the borrower's profit, so it can be classified as non-operating expenses. For a legal entity, interest is the income component, therefore they are subject to personal income tax at a rate of 13%. Withholding and payment of obligatory payments is carried out by the tax agent (borrower).

When a company takes out an interest-free loan, there are no income and expense parts.

Reflection of short-term loans

Many commercial firms use loans and borrowings, which should be correctly reflected in the accounting program 1C: Enterprise Accounting. These funds cannot be taken into account as income, since the organization incurs monthly expenses to repay these loan resources. At the same time, repayment of the loan reduces the amount of income on which the tax contribution is levied.

At the same time, you need to correctly calculate the share of interest for transfer to a banking organization. To ensure reliable accounting in 1C, you should have information about the amount, monthly interest charges, as well as the final date for transferring finances.

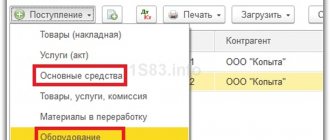

Registration of a loan in the program occurs according to the document “Receipt to the current account.” It also requires you to fill in all required fields:

- type of operation - Obtaining a loan from a bank;

- payer column - indicate the name of the bank where the loan funds were issued;

- contract - created in advance or in the process of generating data in electronic form. In this case, you need to go from the tabular form to the list of contracts and click on the “Create” button. After this, a new agreement will be formed. In the corresponding document window we indicate the numbers 66.01.

How to reflect the receipt of a short-term loan in 1C: Accounting 8.3?

Of course, we get a loan from the bank. But money received into the organization’s account, loan payments, bank commissions, and interest must be reflected in 1C: Accounting. We will tell you further how to do this correctly.

Let's imagine a situation where we received a bank loan in the amount of UAH 100,000, and it goes to our current account. We need to create a module in 1C in which we will interact with the bank to service our credit line.

The algorithm of our actions is as follows

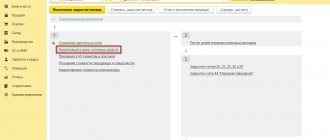

- Go to the “Bank” menu.

- Select the “Bank Statements” section.

- In tasks, click “Add”.

- And, since we work with receipts to the account, we select the appropriate item and click on “Ok”.

- A context menu appears in front of us. Select “Calculations for loans and borrowings”.

- A form appears in front of us that we must fill out. Everything is extremely logical.

The payer is a bank, fill in the bank details. If the institution is not in the drop-down list, enter the details manually. We confirm our actions by clicking on the “Ok” button.

The form has a line to add an agreement. After clicking on it, a separate window “Counterparty Agreement – Add” pops up. We register the name and number according to our register. The payer's account should be adjusted automatically. If this does not happen, the document will pass without it.

In the “Amount” line we enter the 100,000 USD we took.

The last thing we need to do is register the settlement account. There are 2 accounts responsible for accounting for the loan – numbers 66 and 67.

The first is “responsible” for short-term loans, the second – for long-term loans, for a period of 1 year or more. We choose option 1. Select the subaccount “Short-term loans”.

- The last thing we need to do is to register the purpose of the payment – “Receiving a bank loan.”

- And on the task bar, click “Perform”.

The status of the task changes immediately and we can check this by clicking on the status icon. Now the 1C short-term loans form we filled out looks like this.

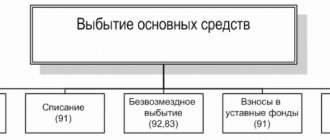

The organization can issue itself or receive borrowed funds. According to the terms of loans, short-term and long-term are distinguished. Another nuance that affects accounting is whether the loan is provided without payment for the use of funds (interest-free) or whether interest must be paid (interest-bearing). In this article we will look at examples of postings for loans issued and received.

A legal entity, individual entrepreneur and individual can receive a loan. In turn, the organization can temporarily issue funds and property for use, both to other companies and to individuals (its employees, founders, strangers).

Getting a loan with interest

Let's look at a simple example. A commercial company received 200,000 rubles from the founder, Vyacheslav Yakovlevich Salimgareev. According to the terms, the money was issued at 8% per annum. The return period is 12 months.

It is required to reflect the corresponding loan acceptance transactions and interest calculations. In addition, you need to reliably show the withholding of personal income tax, payment of monthly fees and debt.

If a company took money based on certain requirements, the accountant must create a settlement order in 1C 8.3. First of all, select the “Receiving a loan from a counterparty” section. In the window that appears, you need to enter current information:

- name of the organization and the corresponding date;

- the name of the organizer who issued the money;

- total loan amount.

Important! It is necessary to reflect the information using settlement account 66.03, because in the above situation the loan was taken out for a short-term period.

The following is the accounting entry: Dt 51 Kt 66.03 (credit funds were credited to a commercial company).

The loan reflects the amount of the company's total debt to the relevant person. Registration of funds for personal needs is available to the company in cash. In such a situation, an electronic document is created in 1C 8.3 “Cash receipt”. To do this, select the item “Receiving a loan from a counterparty.”

Calculation and accrual of interest on the loan

There is no uniform documentation for calculating interest charges. For this reason, you can only create a manual entry:

- go to the Operations item, then Accounting - Operations entered manually.

- Then click “Create” with the mouse.

- Here is the necessary accounting entry: Dt 91.02 Kt 66.04, for the amount of interest expenses for the month.

Important! The credit reflects interest calculated to be paid over 30 days. It is necessary to indicate the founder and the agreement.

A similar method will be used to calculate income for other periods. For general accruals, it is necessary to timely withhold personal income tax from an individual at a rate of 13% per annum. In this case, we will create a transaction manually using the posting: Dt 66.04 Kt 68.01 for the amount of personal income tax from the founder.

The accountant must enter this entry every month.

At the same time, in order to reflect the personal income tax in the financial statements, it is necessary to create an electronic document “Personal Income Tax Accounting Operation”:

- While in the “Salaries and Personnel” menu, go to “Personal Income Tax - All personal income tax documents”;

- Click on “Personal Tax Accounting Operation”.

In electronic form, you must provide information about your income, as well as the amounts of calculated and withheld personal income tax. A similar document should be created in subsequent months.

Transfer of interest to the founder

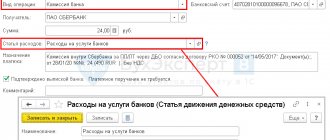

To return to a legal entity the money that is owed to it, you need to create a “Write-off from the current account” order. In this case, the link “Return of loan to counterparty” should be used.

The reporting form should indicate:

- what is the name of the company itself (select from the list);

- the individual or legal entity who founded the company;

- contract number;

- income interest part minus calculated personal income tax.

You can enter the information in the table as follows: Dt 66.04 Kt 51 for the payment amounts under the loan agreement. The debit reflects expenses paid to the company.

In subsequent months, interest is paid in the same way. Any of the actions must be performed strictly within the specified time frame.

Repayment of the loan amount

At the end of the credit period, the principal amount of the debt must be transferred to the founder in full. For these purposes, it is important to make a document in the 1C 8.3 program “Write-off from a current account.”

When filling out the document we write down:

- name of the organization, date of compilation;

- parent company and contract number;

- the amount of the principal debt;

- In the Type of payment column, select “Debt repayment”.

Here is the current posting: Dt 66.03 Kt 51 for the amount of the repaid principal debt. The debit of the account reflects the paid loan to the founder.

Reflection of employee personal income tax

And one more manual operation, the most difficult, with filling out registers (Fig. 10). It is needed to reflect personal income tax on material benefits in accounting.

We fill out the operation itself (Dt 70 - Kt 68.01) and select two registers:

- Mutual settlements with employees

- Salary payable

The registers are filled in for the same amount (personal income tax amount calculated earlier) with a minus sign. Type of movement – “Coming” (Fig. 11).

To correctly draw up a loan agreement, as well as maintain tax and accounting records, you should pay special attention to the key points that must be specified in the agreement:

- Loan amount;

- The period for which the funds were issued;

- Method of receipt. The highest priority is to transfer the loan to the employee’s card. You can issue a loan from the cash register by first withdrawing funds from your current account, since issuing a loan from an organization’s cash proceeds is prohibited by the instructions of the Bank of Russia dated October 7, 2013. N3073-U;

- Purpose of the loan. If the loan is issued for the purchase of real estate, the borrower is exempt from taxation of material benefits.

- Terms of issue - interest-free or interest-free. If the agreement does not mention that the loan is interest-free or the rate is not specified, then according to the agreement the amount of interest is equal to the refinancing rate;

- Loan repayment date: in full or in monthly payments and interest payment period.

Taxation by the lender

The amount of the loan issued is not an expense of the organization, just as its repayment is not income. Interest on a loan, by virtue of clause 6 of Article 250 of the Tax Code, is recognized as non-operating income and is taken into account when calculating income tax:

Taxation for the borrower

According to paragraph 2 of Art. 212 of the Tax Code, the material benefit from saving on interest is recognized as an individual’s income if the calculated interest on the loan agreement is less than two-thirds of the current refinancing rate established by the Bank of Russia on the date of actual receipt of income by the taxpayer:

Article 223 of the Tax Code of the Russian Federation indicates that the date of receipt of income in the form of material benefits from savings on interest is from 01/01/2016. is the last day of every month. At the same time, the organization as a tax agent is obliged to withhold personal income tax from material benefits with the next payment of wages at the following rates:

- 35% – if the employee is a tax resident of the Russian Federation;

- 30% – if the employee is a non-resident of the Russian Federation.

If the agreement, in accordance with Article 212 of the Tax Code of the Russian Federation, states the purpose of the loan as obtaining funds for the construction or purchase of housing or land for construction, then the tax inspectorate, at the request of the employee, issues a notification to the organization about the exemption of this employee from taxation of material benefits.

How to make a loan in 1C 8.3

In the 1C Accounting 8.3 program, settlements for loans provided to employees are carried out in account 73.01 Settlements for loans provided.

Step 1. Issuing a loan to an employee of the organization

To formalize the transaction for issuing a loan in 1C 8.3 Accounting, we will generate a payment order for the transfer of funds to an employee of the organization: section Bank and cash desk - Payment orders - Create - transaction type Issuing a loan to an employee:

Based on the payment order, we will create the document Write-off from the current account:

Posting Dt 73.01 – Kt 51 – funds were transferred to the employee under the loan agreement:

Step 2. Registration in 1C Accounting 8.3 new deductions

To register new deductions, go to the section Salaries and HR – Directories and settings – Deductions:

Click the Create button and fill in the name of the deduction type:

- In our case, this is Retention for loan repayment;

- Retention Category

field blank, since not a single category from the proposed list is suitable; - Assign a unique code and click the Save and close button:

Similarly, we create a type of deduction – Deduction of interest for using a loan:

Step 3. Calculation of interest on loans in 1C 8.3 and reflection of deductions when calculating wages

Let's register the deduction of part of the debt and the accrual of interest on loans in 1C 8.3 using the Payroll document.

On the

Retentions

, click the

Add

to fill out the table part:

- In the Employee column – an employee of the organization from whose salary the deduction is made;

- In the Retention column - types of deductions. In our case, there are two of them: deduction for loan repayment and deduction of interest;

- In the Result column - the amounts of deductions:

Let's look at the payslip in detail:

To reflect in accounting the amounts of deductions on the principal debt and interest for the use of borrowed funds, we will draw up the document Transaction entered manually. Postings are generated:

- Dt 70 - Kt 73.01 - reflects deductions from wages to pay off debt and interest;

- Dt 73.01 – Kt 91.01 – other non-operating income is reflected in the amount of interest on the loan:

Step 4. Calculation of material benefits from savings for the use of borrowed funds and withholding personal income tax

Let's look at how the refinancing rate changed in the period from November 5, 2015. until 04.11.2016:

- From 05.11.2015 until December 31, 2015 refinancing rate is 8.25%;

- From 01/01/2016 the refinancing rate is equal to the key rate and is 11%;

- From June 14, 2016 the key rate, and therefore the refinancing rate, is 10.5%.

Let's calculate the interest on the loan and material benefits by month:

- November – for the period from 05.11.2015 until November 30, 2015:

- % on loan = 72,000.00*6%/365*27 = 319.56 rubles;

- The interest rate under the loan agreement is 6% more than 2/3 of the refinancing rate (2/3*8.25%), so there is no material benefit.

- December 2015

- % on loan = 66,000.00*6%/365*31 = 336.33 rubles;

- There is no material gain.

- January 2021

- % on loan = 60,000.00*6%/366*31 = 304.92 rubles;

- Material benefit = 60,000.00 * (2/3 * 11% - 6%) / 366 * 31 = 67.76 rubles;

- Personal income tax on material benefits = 67.76 * 35% = 24.00 rubles.

Let us reflect the material benefit in the 1C 8.3 program using the personal income tax accounting operation: section Salaries and personnel - personal income tax - all documents on personal income tax - personal income tax accounting operation. On the Income

we indicate:

- The date of receipt of income in the form of material benefits;

- Income code 2610 – Material benefit received from savings on interest for the use of borrowed (credit) funds;

- Amount of income;

- Tax calculated at rates of 9% and 35%:

On the Withheld for all bets tab:

- Date of receipt of income;

- Tax rate;

- The transfer deadline is no later than the day following the payment of income;

- Income code:

We will reflect the deduction of personal income tax in accounting using a manual operation: entry Dt 70 - Kt 68.01 withheld from salary personal income tax for material benefits:

In order for 1C 8.3 Accounting to automatically deduct tax on material benefits from an employee’s salary, it is necessary to reflect the corresponding adjustments in the registers. button – Select registers:

Mutual settlements with employees and Salaries payable:

Data is generated:

- February 2021:

- % on loan = 54,000.00*6%/366*29 = 256.72 rubles;

- Material benefit = 54,000.00 * (2/3 * 11% - 6%) / 366 * 29 = 54.05 rubles;

- Personal income tax on material benefits = 54.05 * 35% = 19.00 rubles.

- March 2021:

- % on loan = 48,000.00*6%/366*31 = 243.93 rubles;

- Material benefit = 48,000.00 * (2/3 * 11% - 6%) / 366 * 31 = 54.21 rubles;

- Personal income tax on material benefits = 54.21 * 35% = 19.00 rubles.

- April 2021:

- % on loan = 42,000.00*6%/366*30 = 206.56 rubles;

- Material benefit = 42,000.00 *(2/3*11% - 6%)/366 * 30 = 45.90 rubles;

- Personal income tax on material benefits = 45.90 * 35% = 16.00 rubles.

- May 2021:

- % on loan = 36,000.00*6%/366*31 = 182.95 rubles;

- Material benefit = 36,000.00 *(2/3*11% - 6%)/366 * 31 = 40.65 rubles;

- Personal income tax on material benefits = 40.65 * 35% = 14.00 rubles.

- June 2021:

- % on loan = 30,000.00*6%/366*30 = 147.54 rubles;

- Material benefit = 30,000.00 * (2/3 * 10.5% - 6%) / 366 * 30 = 24.59 rubles;

- Personal income tax on material benefits = 24.59 * 35% = 9.00 rubles.

- July 2021:

- % on loan = 24,000.00*6%/366*31 = 121.97 rubles;

- Material benefit = 24,000.00 * (2/3 * 10.5% - 6%) / 366 * 31 = 20.33 rubles;

- Personal income tax on material benefits = 20.33 * 35% = 7.00 rubles.

- August 2021:

- % on loan = 18,000.00*6%/366*31 = 91.48 rubles;

- Material benefit = 18,000.00 * (2/3 * 10.5% - 6%) / 366 * 31 = 15.25 rubles;

- Personal income tax on material benefits = 15.25 * 35% = 5.00 rubles.

- September 2021:

- % on loan = 12,000.00*6%/366*30 = 59.02 rubles;

- Material benefit = 12,000.00 * (2/3 * 10.5% - 6%) / 366 * 30 = 9.84 rubles;

- Personal income tax on material benefits = 54.21 * 35% = 3.00 rubles.

- October 2021:

- % on loan = 6000.00*6%/366*31 = 30.49 rubles;

- Material benefit = 6,000.00 * (2/3 * 11% - 6%) / 366 * 31 = 5.08 rubles;

- Personal income tax on material benefits = 54.21 * 35% = 2.00 rubles.

Let's present the loan calculation in the form of a summary table.

Applying for an interest-free loan in 1C

Let's look at a simple example. The founder, Pavel Vladimirovich Ivanov, issued a loan to a commercial organization without interest in the amount of 100,000 rubles for a period of 1 year.

In this situation, it is necessary to reflect only two operations in the 1C 8.3 program: the fact of receiving borrowed funds and their subsequent return.

Receiving a loan from the founder

After the company accepts the funds, the accountant must formalize the transaction in the same way as described in the previous section. The program requires you to create an electronic transaction for the receipt of funds. The document “Receipt to the current account” indicates the following information:

- name of company;

- Full name of the lender;

- type of operation “Receiving a loan from a counterparty”;

- then click on the “Add” button;

- in the tabular part that appears, we indicate the agreement and the current item of income, for example, “Receiving a loan”;

- Next, we manually enter the amount received;

- settlement account 66.03, if the loan was issued for a short period of time.

To complete the operation you have started, you must click the “Perform and close” button. Let's make an accounting entry: Dt 51 Kt 66.03 the loan amount was received into the current account.

Repayment of debt to the founder

To reflect the debt repayment transaction, you need to create a “Write-off from the current account” document. It contains the following information:

- Company name;

- name of the lender;

- type of operation “Repayment of loan to counterparty”;

- then click the “Add” button;

- in the open sign you should indicate the Type of payment “Debt repayment”, as well as important information on contractual obligations;

- in the program, select the expense item “Loan repayment” from the list;

- in the required window, indicate the amount of funds to be returned;

- settlement accounts 66.03.

To finish the work and save the information, click the “Execute and close” button. In this case, the transfer of borrowed funds in 1C 8.3 is completed correctly.

Posting in the document: Dt 66.03 Kt 51 for the share of money paid under an interest-free agreement.

Loan from the founder in 1C

USEFUL LINKS:

Restoring the 1C 1SPARK database Risks - a guarantee of diligence 1C dossier: Counterparty - protection for business Remote support of 1C programs Advance report in 1C

It happens that a company begins to have financial problems.

Business owners can easily support the economy of their brainchild by providing a loan, and it can be with or without interest. In this case, the accountant must correctly document the receipt of funds to the company’s current account and return them to the borrower. Let's consider the main subtleties of organizing the process of receiving and repaying a loan from the founder, as well as the method of deducting personal income tax from material benefits in 1C.