How to become a payer of the simplified tax system

A company or individual entrepreneur can become a “simplified” if it meets the following requirements (Article 346.12 of the Tax Code of the Russian Federation):

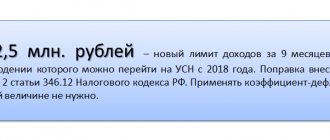

- The amount of income for the 9-month period of the year preceding the year in which the simplified tax system began to be applied is less than 112.5 million rubles. (criterion for organizations only). For example, if the transition is planned from 2021, the company’s income from January to September 2021 cannot exceed the specified amount.

NOTE! This income limitation is provided only for organizations. Individual entrepreneurs can switch to the simplified tax system for any amount of income, but in the future they must comply with the revenue limit of 150 million rubles. in a year.

- The average number of employees is no more than 100.

- The residual value of fixed assets is no more than 150 million rubles.

NOTE! This requirement applies to both companies and individual entrepreneurs.

- The percentage of participation in the organization of another taxpayer-legal entity is less than 25%.

- The payer category is not reflected in subparagraph. 1–13 p. 3 art. 346.12 Tax Code of the Russian Federation.

According to the requirements of Art. 346.13 of the Tax Code of the Russian Federation, in order to switch to the simplified tax system, an application should be sent to the tax authority with which the company or individual entrepreneur is registered:

- before December 31 of the year preceding the transfer, or

- within 30 calendar days - for newly registered payers.

For more information on how to become a payer on the simplified tax system, see the material “Who are the payers of the simplified tax system?” .

Where to pay tax under the simplified tax system if an individual entrepreneur does not work at his place of registration, find out here.

When UTII does not apply

Please note that the transition to imputation is not possible if an organization or individual entrepreneur violates the following conditions:

- Number of employees - more than 100 people;

- 25% or more of the organization’s authorized capital belongs to other legal entities;

- The entrepreneur's transition to the simplified system was carried out on the basis of a patent;

- The enterprise is registered as a simple partnership;

- Agricultural tax applies.

Let us note that if all the above conditions are met, the transition to UTII will not present any difficulties for all categories of taxpayers who are on the simplified tax system.

How to become a UTII payer

IMPORTANT! UTII cannot be used from 2021. It has been canceled throughout the Russian Federation. A number of regions abandoned the special regime already in 2020. See here for details.

The procedure for transition to imputation is specified in Art. 346.28 of the Tax Code of the Russian Federation and provides for:

- registration at the place of activity (or registration) of the company or individual entrepreneur;

- submitting a notice of transition to UTII no later than 5 days from the date of commencement of UTII application.

ConsultantPlus experts explained whether it is possible to switch to UTII in mid-2021 and answered the most common questions from taxpayers:

If you don't have access to the system, get a free trial online.

UTII payers can provide the following types of services:

- of a domestic nature;

- veterinary;

- repair and maintenance of cars and motorcycles;

- on the organization of parking lots;

- catering (the area of the premises should not exceed 150 sq. m);

- retail sale of food and non-food products (maximum area limitation - 150 sq. m);

- for transportation by road;

- outdoor advertising on special structures or on vehicles;

- leasing buildings and land plots for retail chains;

- for the placement and residence of people in an area of no more than 500 square meters. m.

Read more about the procedure for registering as a UTII payer here.

Transition to UTII from General Taxation

When changing the OSN to “imputation” for organizations and enterprises, there are still the same restrictions: on the number of employees (no more than 100 people) and on the share of third-party legal entities in the authorized capital (no more than 25%).

If the activity engaged in by an enterprise operating under the general tax regime falls under UTII in the region where it is carried out, then to switch to “imputation” it is enough to submit the appropriate Application to the tax office at the place of registration of the individual entrepreneur or LLC.

This must be done no later than five days from the date of actual commencement of work or provision of services. At the same time, it is not at all necessary to abandon the SST, since, as mentioned above, different tax regimes can be combined with UTII, and in the future, under General Taxation, it will be enough to submit zero returns. The change of the OSN to “imputation” is accompanied by one important point: namely, the restoration of VAT. What it is? To put it in simple and understandable language, this is the payment of tax that was previously accepted for deduction. After completing the VAT restoration process, it will be necessary to reflect this action in the organization’s sales book.

How to switch from simplified tax system to UTII

The transition from simplified tax system to UTII (here we are talking about replacing one mode with another, without combining, which we will talk about below) is carried out in the following ways:

- At the end of the year in which the taxpayer lawfully applied the simplified tax system. To do this, you must meet 2 deadlines. Before January 15 of the year following the year of application of the simplified tax system, the Federal Tax Service must be notified of the refusal to use this system. What happens if such notice is not submitted, see here. At the same time, no later than 5 working days from the date of commencement of application of UTII, you must inform the Federal Tax Service about this circumstance (see forms for individual entrepreneurs and for organizations). Accordingly, if you intend to apply UTII instead of the simplified tax system from the beginning of the year, you must submit both applications in compliance with both established deadlines. Such a transition cannot be made during the year, since there is an obligation to apply the simplified tax system throughout the entire tax period, unless the right to use this regime is lost.

- In case of loss of the right to use the simplified tax system during the year due to non-compliance with the requirements of Art. 346.12 of the Tax Code of the Russian Federation (these include both termination of compliance with the above requirements and exceeding the maximum allowable limit of possible income for the simplified tax system of 150 million rubles), the payer must stop charging tax under this system from the beginning of the quarter in which this occurred. The Federal Tax Service must be notified of this fact within 15 days following the quarter of loss. From the quarter of loss until the end of the year, taxes should be calculated in the manner in force for OSNO, since the Tax Code of the Russian Federation does not provide for the possibility of replacing the simplified tax with UTII before the end of the year in the event of loss of the right to the simplified tax system. If you intend and have the opportunity to apply UTII at the end of the year in which the right to the simplified tax system was lost, you must report this to the Federal Tax Service within 5 working days from January 1 of the year following the year of loss.

The form of notification of refusal to use the simplified tax system is contained in the order of the Federal Tax Service of Russia dated November 2, 2012 No. ММВ-7-3/ [email protected]

It should also be noted that, by virtue of the norms of paragraph 7 of Art. 346.13 of the Tax Code of the Russian Federation, in the event of a transition to UTII from the simplified tax system back to the simplified tax system, the taxpayer can only transfer one year after the transition from the simplified tax system.

How to switch to UTII when registering an individual entrepreneur and registering an LLC

Let's start with detailed step-by-step instructions for switching to UTII when establishing a new enterprise and registering with the Federal Tax Service. The first step is to register an individual entrepreneur or LLC with the tax authorities. This is followed by writing and submitting an application.

Filling out an application for registration as a UTII taxpayer

As soon as the company begins its activities, it is necessary to fill out and submit the corresponding application in two copies no later than five days. The form for legal entities is called UTII-1, for individual entrepreneurs - UTII-2. It must indicate the UTII type of business activity code. If the company operates where it is registered, the checkpoint is placed as in the registration certificate, and if in another place - only with the numbers 35.

and can be found on the website of the Federal Tax Service using the following links:

- UTII-1;

- UTII-2.

Photo gallery: Forms and samples of completed applications and applications

The established form of the form for transferring enterprises to UTII Form UTII-1 is filled out for the enterprise and signed by the head The established form of the form for individual entrepreneurs who want to switch to UTII Form UTII-2 is filled out and signed by the individual entrepreneur The application form is stamped with the enterprise's seal The appendix to the application indicates the types of activities and places of their implementation

Video: instructions for filling out and submitting an application for UTII

https://youtube.com/watch?v=9IR2uzkDRTE

Table: codes of types of entrepreneurial activities UTII

| Code number | Type of business activity |

| 01 | Household services (all household services) |

| 02 | Veterinary services (including treatment services for pets) |

| 03 | Repair, maintenance, car wash |

| 04 | All types of paid parking lots (providing space for them) |

| 05 | Motor transport services (cargo transportation) |

| 06 | Motor transport services (passenger transportation) |

| 07 | Retail trade (through trading floors in a stationary retail chain) |

| 08 | Retail trade (through facilities of a stationary retail chain, without the presence of trading floors, in which the area of the retail space is no more than 5 m2). |

| 09 | Retail trade - pavilions and kiosks (through objects of a stationary retail chain, without the presence of trading floors; through objects of a non-stationary retail chain, in which the retail area is more than 5 m2). |

| 10 | Delivery and differential retail trade (that is, trade from cars and other trade) |

| 11 | Catering services (canteens, cafes and bars) with halls for serving visitors |

| 12 | Catering services (cheburek, pancake, etc.) that do not have halls for serving visitors |

| 13 | Outdoor advertising (using advertising structures, except for structures with automatic image changing) and other framed outdoor advertising (billboards) |

| 14 | Outdoor advertising (using designs with automatic image change) |

| 15 | Outdoor advertising (electronic displays) |

| 16 | Advertising on transport |

| 17 | Temporary accommodation services |

| 18 | Leasing of retail spaces that are located in the facilities of a stationary retail chain that do not have sales floors; objects of non-stationary trading network; catering facilities that do not have halls for serving visitors, when the area of each of them is less than 5 m2. |

| 19 | Leasing of retail spaces that are located in the facilities of a stationary retail chain that do not have sales floors; objects of non-stationary trading network; catering facilities that do not have halls for serving visitors, if the area of each of them is more than 5 m2. |

| 20 | Leasing of plots of land for the purpose of placing objects of a stationary (non-stationary) retail chain, catering facilities (if the area of the land plot is no more than 10 m2). |

| 21 | Leasing of plots of land for the purpose of locating objects of a stationary (non-stationary) retail chain, catering facilities (if the area of the land plot is more than 10 m2). |

When and how to submit an application to the Federal Tax Service department

Submit applications to the tax department at the place of business. That is, at the address of location for legal entities, at the place of residence for individual entrepreneurs. This is provided when your business focuses on the following services:

- retail trade through distribution, delivery;

- advertising on cars;

- transportation of goods and passengers.

This is important: running a business in several districts of a municipality does not oblige you to register with all INFS. However, separate divisions are registered for tax purposes (a point with a permanent workplace at an address different from the head enterprise).

You should also prepare a certificate of registration of a legal entity or individual entrepreneur, a certificate of registration with the INFS, and a personal passport.

Next, you should wait to receive a notification that will confirm your registration. It is issued no later than five days from the date of submission of the application.

The transition to UTII begins with submitting an application to the local tax office

Is it possible to combine simplified taxation system and UTII?

The Tax Code of the Russian Federation does not contain a ban on the simultaneous use of both regimes; Moreover, if the taxpayer calculates UTII for some types of activity, then the simplified tax system applies to all other types of activity (that is, there is no need to formalize withdrawal from simplified taxation). However, when combining these 2 modes, an individual entrepreneur or company must maintain separate records.

For more information about separate accounting, see the material “Separate accounting under the simplified tax system and UTII: maintenance procedure” .

About the nuances of these tax regimes, see the material “UTII or simplified tax system: which is better - imputation or simplified taxation?” .

Features of the transition from simplified to imputation

Due to some differences in accounting for income and expenses in a simplified manner, there are a number of features that you should definitely pay attention to when switching to UTII.

Let's consider several situations that taxpayers may encounter:

Situation 1

The taxpayer, using the simplified tax system, sold products for which payment was received while on UTII. What to pay - tax according to UTII or according to the simplified tax system?

There is no need to pay a simplified tax; you only need to pay UTII for the period of sale.

See also: “How to take into account for the simplified tax system goods purchased in the “imputed” period?”

Situation 2

The taxpayer received an advance payment during the period of being on the simplified tax system, and the implementation was reflected in the period of application of UTII. What should I pay - imputed or simplified tax?

You must pay tax according to the simplified tax system for the period in which the funds were received.

Situation 3

A taxpayer using the simplified tax system, not being a VAT payer, as a general rule usually does not use accounts 19 “Input VAT” and 68.2 “Accrued VAT” in accounting. Do I need to pay VAT when switching to imputation?

A taxpayer using UTII also does not have to pay VAT. There will be 2 situations as exceptions for both him and the simplified tax system payer:

- He is a tax agent for VAT.

- He issued a VAT invoice.

In both cases, non-payers of this tax must pay it to the budget. Therefore, when applying both the simplified tax system and UTII, the tax that needs to be paid will appear in account 68.2. In this case, account 19 will not be used, since tax evaders do not have the right to deduction.

For more information about the peculiarities of the work of VAT payers and non-payers, see the material “Basic rules when an organization without VAT works with an organization with VAT” .

Income after the transition from UTII to simplified tax system

Let's start with accounting for income after the transition to the simplified tax system from UTII.

If in 2021 money will be received for goods actually sold this year, when UTII was still applied, you need to proceed from the following.

UTII does not tax real income, but imputed income. Therefore, the fact of payment does not matter for tax calculation.

This is not the case with the simplified tax system. All funds received as income are taken into account in the tax base under a single tax.

In order not to make a mistake with the recognition of income from the sale of goods (works, services) after the transition from UTII to the simplified tax system, you need to take into account the moment of transfer of ownership of them to the buyer.

The procedure for filling out reports on the simplified tax system and UTII

If a taxpayer, having decided to switch to UTII for certain types of activities, applies the simplified tax system and UTII in parallel, he will have to fill out the appropriate declaration for each type of activity and pay taxes to the budget.

The form of declaration under the simplified tax system is established by order of the Federal Tax Service of Russia dated February 26, 2016 No. ММВ-7-3/ [email protected] ; At the same time, you should pay attention to the fact that for the objects “income” and “income minus expenses” the procedure for filling out the declaration is slightly different.

In accordance with Art. 346.23 of the Tax Code of the Russian Federation, organizations send reports to the tax authority according to the simplified tax system until March 31 after the end of the year, individual entrepreneurs - before April 30. However, in certain situations, the simplified tax system declaration should be submitted earlier: before the 25th day of the month following the one in which the activity on the simplified tax system was terminated at the initiative of the taxpayer, and before the 25th day of the month following the quarter of termination due to loss of the right to be in the specified regime .

Advance payments are due by the 25th day of the month of the next quarter. Payment of the simplified tax at the end of the year is made within the reporting deadlines.

This material will help you fill out the simplified tax return correctly.

Now about what concerns reporting on UTII. Currently, the declaration form is in force, approved by order of the Federal Tax Service dated June 26, 2018 No. ММВ-7-3/ [email protected]

For a sample of filling out a declaration using the new form, see here.

The deadline for submitting the declaration is regulated by clause 3 of Art. 346.32 of the Tax Code of the Russian Federation - no later than the 20th day of the month following the expired quarter.

Payment of UTII, according to clause 1 of Art. 346.32 of the Tax Code of the Russian Federation, is carried out before the 25th day of the month following the expired quarter.

Results

When switching from the simplified tax system to UTII, the taxpayer must promptly notify the tax authority about this in order to avoid unpleasant consequences. Despite the fact that the simplified tax system and UTII are similar in some aspects, for a correct transition from one special regime to another, it is necessary to correctly distinguish between the periods of application of the simplified tax system and UTII.

And don’t forget that 2021 is the last year when you can work on UTII. And not everyone. We talked about the abolition of imputation here.

Sources:

- Tax Code of the Russian Federation

- Order of the Federal Tax Service of Russia dated November 2, 2012 No. ММВ-7-3/ [email protected]

- Order of the Federal Tax Service of Russia dated June 26, 2018 No. ММВ-7-3/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

General provisions

The procedure for switching from the simplified tax system to UTII is regulated by the Tax Code of the Russian Federation. However, to begin with, it should be said that “imputation” is very popular among small businesses due to the fact that instead of several mandatory payments, the company pays a single fee calculated from the estimated amount of income.

In addition, this prevalence of “imputation” can also be explained by the fact that the taxpayer only needs to submit declarations to the fiscal service 4 times during the year in order to confirm the indicators used to calculate the payment amount. In addition, the already small amount can be reduced by the amount of insurance contributions to the Social Insurance Fund.

If we talk about who has the right to work under “imputation”, then it should be noted that in order to implement the planned actions, enterprises and organizations must meet the following criteria:

- the enterprise or organization must have a total income of no more than 45.0 million rubles;

- such a business entity must have no more than 100 employees;

- the balance of fixed assets of such an enterprise should not exceed the amount of 100.0 million rubles;

- the type of activity of a legal entity or individual entrepreneur is not subject to the mandatory application of other fiscal regulations.

Only in this case can organizations choose a simplified taxation system.

However, if the type of activity corresponds to the one for which the proposed regulation is applicable, then such an enterprise or organization has the right to change the simplified tax system to the preferred taxation regulation. The types of activities applicable for imputation include:

- provision of household services;

- provision of veterinary services;

- transportation of passengers and cargo;

- retail trade;

- catering.

In order to become a participant in the specified tax regulations, the management of the organization is required to timely submit an application to the tax authorities.