Today, banking institutions offer businesses a wide variety of services, and it is simply impossible to do without some of these services due to the fact that they are related to current economic activities. For example, enterprises are forced to open a current account, open salary accounts for employees, and enter into an agreement for settlement and banking services. Almost all other services are arranged by business owners at will. Optional services include issuing bank guarantees, opening a line of credit, drawing up documents for foreign economic transactions, and opening letters of credit. Mandatory service or optional - the bank will charge a service fee. In this regard, accountants face many questions regarding how to correctly reflect the costs of banking services in accounting. Is it possible to include the costs of “salary” services in expenses? Should bank interest fees be normalized or not for tax purposes? How to take into account the costs of services of credit institutions when purchasing fixed assets? Let's figure it out.

Expenses for banking services - transfer of wages to employee cards

The bank charges a fee for processing documentation related to the transfer of salaries to employees' accounts. According to the provisions of the Letter of the Ministry of Finance of the Russian Federation dated April 20, 2009 No. 03-03-06/2/88 and the Letter of the Ministry of Finance of the Russian Federation dated August 4, 2008 No. 03-04-06-02/88, the costs of paying remuneration to the bank in this case are allowed to be included in income tax expenses.

But controversy is caused by a reduction in the tax base by the amount of expenses for paying the bank a commission for issuing and annual servicing of plastic cards of employees, on which salaries are received. The condition for including expenses as expenses is their economic justification, and the commission is paid to the bank by the enterprise, but the cards are used by workers. The latest statement on this matter by the Ministry of Finance of the Russian Federation is set out in Letter No. 03-04-06/6-255 dated October 28, 2010, which states that the commission paid to the bank for servicing salary cards is not the income and benefit of employees (not subject to personal income tax) who use these cards is just a necessity related to the choice of payment method for wages

(the employer is obliged to pay wages on time through the cash register or in another way).

Important!

Payments by the employer to the bank for servicing employee salary accounts are not subject to personal income tax and are not subject to insurance contributions.

As for judicial practice, the courts accept the position of taxpayers and allow the costs of paying bank commissions to be taken into account as expenses. For example, the FAS Decree UO dated October 29, 2009 No. Ф09-8382/09-С3 explains the following:

- according to employment contracts, the costs of paying for bank services for servicing the salary account are borne by the employer;

- bank cards are needed to fulfill the employer’s obligation to pay wages (wages are related to the conduct of commercial activities);

- salary cards are not the property of employees - they are the property of banks and are issued to employees for temporary use.

Important!

In the agreement with the bank on servicing salary accounts, it should be mentioned that the cards were made for the needs of the enterprise, and not for the employee.

The accountant must take into account the costs in question as part of other expenses, taking care of the proper execution of personnel documents. In the text of employment contracts, additional agreements to such or other internal acts of the company, it is necessary to specify the following conditions:

- salaries will be paid by non-cash method;

- the costs of banking servicing of salary accounts are borne by the employer;

- in case of dismissal, the employee returns the card to the employer.

Expenses for banking services - an enterprise acquires a fixed asset

One of the biggest challenges is deciding whether to include banking fees in the tax cost of the acquired asset. An example is a situation where a bank charges a fee for opening a letter of credit for the purchase of some equipment under an import contract.

Let's talk. According to paragraph 1 of Art. 257 of the Tax Code of the Russian Federation, the initial cost of an asset includes the amount of costs for its purchase, manufacturing, construction, delivery, as well as bringing it to a state in which it can be used for its intended purpose. Why does a company pay a commission on a letter of credit? For the purpose of purchasing equipment. Accordingly, the amount of remuneration to the bank can be considered as a purchase cost and taken into account in the initial cost of the fixed asset. However, the bank's commission for opening a letter of credit is a fee for the bank's service. Then the costs should be classified as other or non-operating expenses. The Ministry of Finance of the Russian Federation expressed as many as 3 different positions on this matter:

- In Letter No. 03-03-04/1/111 dated 01.08.2005, the Ministry of Finance of the Russian Federation analyzed the situation with the payment of bank remuneration for providing a bank guarantee. Department officials stated that a bank guarantee for a loan taken to purchase an enterprise asset is related to the purchase of a fixed asset, which means that the costs of paying it must be included in the initial cost of the fixed asset.

- In the text of Letter No. 03-03-06/1/673 dated December 5, 2008, financiers proposed to include the costs of paying the commission for opening a letter of credit and its servicing as part of non-operating expenses.

- Letter No. 03-03-06/1/408 dated June 18, 2009 contains instructions regarding the accounting of expenses for paying commissions to the bank as interest, which are taken into account under Article 269 of the Tax Code of the Russian Federation. In this case, the norms of Art. 269 of the Tax Code of the Russian Federation is recognized by financiers as special, priority in relation to the norms of Art. 257 Tax Code of the Russian Federation. The letter of credit commission, in their opinion, is taken into account as interest on debt obligations and is not included in the initial cost of the fixed asset.

Important!

Clause 4 art. 252 of the Tax Code of the Russian Federation allows an enterprise to independently determine the procedure for accounting for expenses if expenses can be assigned to several groups of expenses on an equal basis. This position is supported by the courts.

Costs for banking services – the company applies for a loan

Legal entities and individual entrepreneurs often need additional cash injections into their business to keep it afloat in difficult times or to expand. Sometimes one of the conditions for issuing a loan is that the credit institution charges additional fees. Most often, additional payments are assigned as follows:

- commission for early repayment of the loan;

- remuneration for opening a credit line and its extension;

- additional fee for opening a loan account and its maintenance;

- commission for using a loan.

The Tax Code allows the taxpayer to choose the option for accounting for expenses for banking services that seems most appropriate to him (both options provide an open list of expenses taken into account):

- it is permitted to include such costs as non-operating expenses;

- You can also take into account the costs of banking services as part of other expenses associated with production and sales.

However, the Ministry of Finance of the Russian Federation has its own opinion regarding the accounting of such expenses, set out in Letters dated August 27, 2012 No. 03-03-06/1/432, dated August 29, 2011 No. 03-03-06/1/534. According to department officials, in this way it is allowed to take into account only those commission payments to a banking institution that are paid in a fixed amount and are presented in absolute terms. And if the bank’s remuneration is determined as a percentage, the commission must be considered as interest on debt obligations. Such payments must be standardized according to Art. 269 of the Tax Code of the Russian Federation. That is, in order to accept interest commissions as income tax expenses, the accountant must calculate the maximum amount of interest commissions when an enterprise receives a loan on a par with the maximum amount of interest for the use of borrowed funds.

But the position of the Ministry of Finance of the Russian Federation cannot but cause controversy. Interest based on clause. 2 p. 1 art. 265 of the Tax Code of the Russian Federation are calculated for tax purposes based on the actual time of use of funds borrowed on credit. At the same time, additional loan commissions, paid as a percentage, depend on the size of the loan, and not on the period of use of the funds. Moreover, interest is paid by the borrower for the bank's services, and not for the use of funds. The courts also do not support this opinion of the financial department. For example, in the Resolution of the Federal Antimonopoly Service of Moscow dated October 11, 2012 No. F05-11313/12, the court explains that the bank’s commission for issuing a loan is an independent payment charged by the bank for the loan service, and therefore the payment cannot be equated to interest on debt obligations. Expenses for payment of fees should be taken into account by the borrower's accountant as part of other expenses or non-operating expenses. With regard to payments for opening a letter of credit and commissions under a factoring agreement, the courts accept the following positions:

- There is no judicial practice on the issue of attributing expenses for paying commissions for opening letters of credit, so companies have the right to attribute such costs to other or non-operating expenses (when arguing your position, you can refer to the legal nature of a letter of credit - this is not borrowing, the function of a letter of credit is to carry out non-cash payments (Article 862 of the Civil Code of the Russian Federation), accordingly, a bank commission is paid for carrying out such an operation, and the commission also depends on the amount of the letter of credit);

- according to the courts, commissions under a factoring agreement should be classified as other and non-operating expenses, because the obligation under a factoring agreement is not a debt obligation, and therefore the bank’s commission is not recognized as interest, which must be normalized (Resolution of the Federal Antimonopoly Service of the Moscow Region dated February 16, 2011 No. KA-A40/ 16965-10).

Tax accounting of expenses for bank services and loan interest payments

Each organization bears the costs associated with paying for banking services. In addition, she sometimes needs to raise borrowed funds to implement new large projects, and then, as a rule, she turns to the bank to obtain a loan. It is clear that the company will strive to take such expenses into account when taxing profits. Moreover, tax legislation provides for this possibility. However, practice shows that tax authorities often make claims related to the tax accounting of such expenses. How you can reduce taxable profit by paying for banking services and at the same time avoid disagreements with tax inspectors is described in this article.

Depending on the legal nature, expenses for paying funds to banks may be classified in tax accounting as:

- other expenses associated with production and sales, namely expenses for paying for bank services (subclause 25, clause 1, article 264 of the Tax Code of the Russian Federation);

- non-operating expenses, namely expenses for bank services, including those related to the sale of foreign currency, when collecting taxes, fees, penalties and fines in the manner provided for in Art. 46 of the Tax Code of the Russian Federation, with the installation and operation of electronic document flow systems between the bank and clients, in particular “client-bank” systems (subclause 15, clause 1, article 265 of the Tax Code of the Russian Federation);

- expenses in the form of interest on debt obligations (subclause 2, clause 1, article 265 of the Tax Code of the Russian Federation).

Let us consider the features of the practical application of the above rules of law.

Accounting for expenses for bank services

According to the tax authorities, the remuneration paid to the bank for the transfer from the organization's current account to the bank accounts of its employees of funds intended for the payment of wages is taken into account when taxing profits on the basis of subsection. 25 clause 1 art. 264 Tax Code of the Russian Federation. This point of view is given in the letter of the Federal Tax Service of Russia dated April 26, 2005 No. 02-1-08 / [email protected] “On the procedure for recognizing expenses for paying for bank services for the production and servicing of bank cards for employees of the organization.”

At the same time, it is necessary to take into account the following clarifications from the tax service. A line of credit is a legal obligation from a bank (or similar institution) to a borrower to provide loans to the borrower over a specified period, up to an agreed limit.

In accordance with sub. 25 clause 1 art. 264 of the Tax Code of the Russian Federation, other expenses of the taxpayer include expenses for paying for bank services, if such expenses are related to production and (or) sales. In other cases, in accordance with subparagraph. 15 clause 1 art. 265 of the Tax Code of the Russian Federation, expenses for banking services are classified as non-operating. Moreover, such expenses must be economically justified.

There are no restrictions on the list of types of services provided by banks for accounting for tax purposes. Accordingly, the fee for the opportunity to receive funds under the terms of a credit line is included in expenses taken into account when taxing profits. Moreover, in accordance with paragraph 1 of Art. 272 of the Tax Code of the Russian Federation, such expenses must be recognized as current expenses evenly over the period stipulated by the transaction for opening a credit line.

Tax department specialists drew attention to the fact that this does not apply to situations where, according to the terms of the agreement for opening a credit line, by agreement of the parties, the amount of the fee for using borrowed funds increases or if the fee for opening a credit line is set as a percentage of the total amount of outstanding loans received organization under a credit line. In this case, it is necessary to use the provisions of Art. 269 of the Tax Code of the Russian Federation.

The above legal position is reflected in the letter of the Ministry of Taxes and Taxes of Russia dated September 13, 2004 No. 02-5-11 / [email protected] “On accounting for taxpayer expenses associated with servicing a credit line by a bank.”

The question of how to take into account the amount of commission charged by the bank for transactions was clarified by the Russian Ministry of Finance. In a letter dated May 10, 2006 No. 03-03-04/1/427, financiers indicated that such an amount could be taken into account as part of the cost of paying for bank services. At the same time, when the commission for transactions on a loan account is set as a percentage of the amount of the outstanding loan, this commission must be included for profit tax purposes in expenses in the form of interest on the loan in the manner prescribed by Art. 269 of the Tax Code of the Russian Federation. According to sub. 2 p. 1 art. 265 of the Tax Code of the Russian Federation, these amounts are taken into account as part of non-operating expenses.

In accordance with paragraph 8 of Art. 272 of the Tax Code of the Russian Federation for loan agreements and other similar agreements, the validity of which falls on more than one reporting period, for profit tax purposes, the expense is recognized as incurred and is included in the relevant expenses at the end of the corresponding reporting (tax) period.

Tax accounting of expenses for interest payments on a bank loan

Article 265 of the Tax Code of the Russian Federation provides that non-operating expenses not related to production and sales include reasonable costs for conducting activities not directly related to production and (or) sales. Such expenses include, in particular, expenses in the form of interest on debt obligations of any type, including interest accrued on securities and other obligations issued (issued) by the taxpayer, taking into account the features provided for in Art. 269 of the Tax Code of the Russian Federation. Interest on debt obligations of any type is recognized as expenses, regardless of the nature of the credit or loan provided (current and (or) investment).

An expense is considered only the amount of interest accrued for the actual time of use of borrowed funds (the actual time the said securities are held by third parties) and the initial yield established by the issuer (lender) in the terms of the issue (issue, agreement), but not higher than the actual one.

Features of attributing interest on debt obligations to expenses

We emphasize that the cost of paying interest for using a bank loan is a standard expense. This means that the organization has the right to write off as expenses the amount of interest paid to the bank, within the limits established by law. Let's look at these limits in more detail.

For profit tax purposes, debt obligations mean loans, commodity and commercial loans, loans, bank deposits, bank accounts or other borrowings, regardless of the form of their execution (clause 1 of Article 269 of the Tax Code of the Russian Federation).

Interest accrued on a debt obligation of any type is recognized as an expense under the following condition. It is necessary that the amount of interest accrued by a taxpayer on a debt obligation does not deviate significantly from the average level of interest charged on debt obligations issued in the same quarter (month - for taxpayers who have switched to calculating monthly advance payments based on actually received profits) on comparable terms.

Debt obligations issued on comparable terms mean obligations issued in the same currency for the same terms in comparable amounts and against similar collateral. When determining the average level of interest on interbank loans, only information on interbank loans is taken into account. This provision also applies to interest in the form of a discount, which is formed by the drawer as the difference between the repurchase (redemption) price and the sale price of the bill.

Please note that a significant deviation in the amount of accrued interest on a debt obligation is considered to be a deviation of more than 20% upward or downward from the average level of interest accrued on similar debt obligations issued in the same quarter on comparable terms.

The maximum amount of interest recognized as an expense may be determined differently if the company does not have debt obligations to Russian organizations issued in the same quarter on comparable terms, or if it itself establishes a different procedure. In such situations, the maximum interest rate is taken equal to the refinancing rate of the Bank of Russia, increased by 1.1 times, when issuing a debt obligation in rubles, and equal to 15% for debt obligations in foreign currency. Arbitration courts also point to this (see, for example, the Resolution of the FAS Volga-Vyatka District of July 4, 2006 in case No. A29-7052/2005a).

The above rules also apply to interest and amount (exchange rate) differences on obligations expressed in conventional monetary units at the rate established by agreement of the parties.

The refinancing rate of the Bank of Russia means the rate:

- valid on the date of raising funds - in relation to debt obligations that do not contain a condition on changing the interest rate throughout the entire term of the debt obligation;

- effective on the date of recognition of expenses in the form of interest - in relation to other debt obligations.

An example of the practical application of the above rules is the Resolution of the Federal Antimonopoly Service of the Ural District dated January 22, 2007 in case No. F09-11996/06-C2.

The company applied to the arbitration court to invalidate the inspectorate's decision regarding the additional assessment of income tax, penalties and fines. The dispute between the parties arose as a result of the adoption by the tax authority based on the results of an on-site audit for 2002-2003. decisions to hold the taxpayer accountable. During the inspection, the inspectorate concluded that the company had overestimated non-operating expenses as a result of including interest on debt obligations in excess of the established limits. The fact is that the taxpayer attributed costs to these expenses based on a rate of 21%, which significantly deviates from the Bank of Russia rate in force at that time, increased by 1.1 times.

The arbitration court found that during the period under review the company had obligations under several loan agreements that were concluded on comparable terms. The interest rate used by the company does not significantly deviate from the average level of interest accrued on similar debt obligations issued in the same quarter on comparable terms. When establishing this percentage, the taxpayer was guided by the provisions of paragraph 1 of Art. 269 of the Tax Code of the Russian Federation.

In this case, the use of the inspectorate to determine the percentage deviation of the Bank of Russia rate was found by the court to be unfounded, since the possibility of its use should be conditioned by the absence of debt obligations issued in the same quarter on comparable terms, as well as the independent choice of the taxpayer. As a result, the organization won the legal dispute.

In what period should expenses be recorded?

Based on clause 8 of Art. 272 of the Tax Code of the Russian Federation for loan agreements and other similar agreements, the validity of which falls on more than one reporting period, for profit tax purposes the expense is recognized as incurred and is included in the relevant expenses at the end of the corresponding reporting period.

Upon termination of the agreement (repayment of a debt obligation) before the expiration of the reporting period, the expense is recognized as incurred and is included in the corresponding expenses on the date of termination of the agreement (repayment of the debt obligation).

In one of the cases, the court noted that since the loan agreement was concluded in 2003, the costs of its conclusion also relate to this period and were legally reflected by the taxpayer in tax accounting in 2003 (Resolution of the Federal Antimonopoly Service of the Moscow District dated 18, September 25, 2006 in case No. KA-A40/8766-06).

Features of accounting for expenses on revolving loans and tax risks

Along with long-term loans, short-term loans, sometimes called revolving loans, have also become part of business customs. Their essence lies in the fact that the borrower enters into a loan agreement with the bank, under the terms of which the bank undertakes to provide the borrower with money upon request for a short period of time. In this case, the borrower, having returned the loan amount and interest to the bank, has the right to receive the loan again for a new term. The peculiarity of this transaction is that the parties enter into a long-term agreement between themselves, during which the borrower has the opportunity to receive the funds he needs at any time.

It happens that an organization, having entered into an agreement to raise borrowed funds within the framework of a revolving loan, may actually not receive money in a separate tax period. At the same time, under the terms of the agreement, the company is obliged to pay the bank a commission for the very fact of opening a credit line. In such a situation, the company may have problems with tax accounting for such expenses. Since the organization did not actually receive money under the short-term (revolving) loan, the tax authorities may make claims against it, calling into question the economic justification of these costs and their connection with production activities.

Appealing to the court under such circumstances is practically useless. Arbitration courts believe that the taxpayer does not have the right to attribute to the cost of production the commission fee paid to the bank for opening a credit line if the loan is not received. For example, in one of the disputes, the court proceeded from the fact that the commission fee can be charged to the cost price if two conditions are met: the loan is provided to the enterprise for production purposes and is actually received by the enterprise. Since the company did not receive a loan, the court concluded that the commission fee was unreasonably attributed by the taxpayer to the cost of production. This position is set out in the Resolution of the Federal Antimonopoly Service of the East Siberian District dated October 10, 2000 in case No. A19-12796/99-18-F02-2118/00-S1.

Let us note that the above Resolution was adopted on the basis of the norms of previously existing legislation. However, the provisions of Chapter 25 of the Tax Code of the Russian Federation contain similar norms. Yes, sub. 2 p. 1 art. 265 of the Tax Code of the Russian Federation provides that only the amount of interest accrued for the actual time of use of borrowed funds is recognized as an expense. Within the meaning of the above rule, in order to include interest on a debt obligation as part of non-operating expenses, it is necessary that the taxpayer actually received the borrowed funds and used them for a certain period of time.

Thus, if a company did not receive money under a revolving loan in a particular period, then recognizing the amount of commissions paid to banks for providing this loan as expenses that reduce taxable profit is associated with significant tax risks.

Organizations can defend their interests based on the following. In order to take into account any expenses when taxing profits, they must comply with the general requirements for expenses in Chapter 25 of the Tax Code of the Russian Federation.

Expenses must be justified.

However, the concept of “economic justification of costs” is not given in any act of the current legislation of the Russian Federation. Consequently, the term “economic justification” is an evaluative category, which means that if doubt arises about the justification of the expenses incurred, the tax authority, by virtue of Art. 65 and 200 of the Arbitration Procedure Code of the Russian Federation must prove this circumstance. Currently, there are three options for the interpretation of this term by arbitration courts:

- connection with activities aimed at generating income;

- production feasibility;

- compliance of prices paid for goods (works, services) with the market level.

Arbitration practice in most cases understands economic feasibility as the direction of expenses incurred to generate income (Resolutions of the FAS of the East Siberian District dated October 6, 2004 in case No. A19-2575/04-33-F02-4074/04-S1, FAS of the Northwestern District dated August 2, 2004 in case No. A56-1475/04).

The courts come to the conclusion that, within the meaning of Art. 252 of the Tax Code of the Russian Federation, the economic justification of expenses incurred by a taxpayer is determined not by the actual receipt of income in a particular tax period, but by the focus of such expenses on generating income (Resolution of the Federal Antimonopoly Service of the North-Western District of June 18, 2004 in case No. A56-32759/03). The economic justification of costs can also characterize a quantitative assessment of the costs incurred: how reasonable and necessary from the point of view of market prices was the amount of costs incurred. This, in particular, is the basis of the Federal Antimonopoly Service of the Moscow District in its Resolution dated July 6, 2005 in case No. A72-6211/04-8/585. To recognize costs as unjustified, it is necessary to evaluate their size in relation to the costs of other persons in comparable circumstances (Resolution of the Federal Antimonopoly Service of the Moscow District of July 28, 2005 in case No. KA-A40/6950-05).

If the amount of fees for providing a revolving loan corresponds to the amount of fees for similar services provided by other banks, then it can be recognized that the company’s expenses are economically justified.

Expenses must be documented. In this case, the documents justifying the expenses incurred by the borrowers are:

- loan agreement;

- documents confirming the borrower's receipt of funds;

- payment orders confirming the borrower's payment of interest to the bank.

If the specified documents are properly executed, the company’s costs for paying commissions for providing a revolving loan can be considered documented.

Expenses must be incurred in the course of activities aimed at generating income. The Russian Ministry of Finance noted on this issue that, in accordance with paragraph 1 of Art. 252 of the Tax Code of the Russian Federation, received loans or borrowings on which interest is paid, taken into account when determining the tax base for income tax, must be used to generate income. The amount of interest in this case is established according to the rules of paragraph 1 of Art. 269 of the Tax Code of the Russian Federation (letter of the Ministry of Finance of Russia dated March 22, 2005 No. 03-03-01-04/1/130).

Practice shows that arbitration courts recognize as legitimate the reduction of the tax base for expenses associated with the payment of interest for the use of loan funds. As an example, let us cite the Resolution of the Federal Antimonopoly Service of the Volga-Vyatka District dated January 30, 2006 in case No. A82-9347/2004-37.

The company entered into an agreement to provide a foreign currency loan to replenish working capital. The fee for using the loan was 8% per annum.

The inspection, as a result of a desk audit, established an understatement of taxable profit as a result of the company’s unlawful inclusion of interest accrued under a loan agreement in non-operating expenses. According to the inspectors, the loan was not used by the enterprise for its intended purpose and was not aimed at generating income. The taxpayer did not agree with this approach and appealed the actions of the officials in court.

The arbitration court supported the position of the company, guided by paragraph 1 of Art. 252, sub. 2 p. 1 art. 265 of the Tax Code of the Russian Federation and based on the fact that the tax authority did not challenge the validity of the contracts concluded by the company.

Based on the results of the consideration of the dispute, the court concluded that the company’s costs are associated with activities aimed at generating income and are economically justified and documented.

Article 252 of the Tax Code of the Russian Federation does not make the economic justification of the expenses incurred dependent on the financial results of the taxpayer’s activities. At the same time, assessment of the economic efficiency of expenses incurred by the taxpayer is not provided for by tax legislation as a criterion for forming the tax base.

Economic feasibility is not equivalent to economic efficiency, since the latter reflects the degree of skill in conducting business activities and is a qualitative indicator. In this case, the disputed expenses correspond to the activities of the taxpayer, which already indicates their economic justification.

According to paragraph 1 of Art. 265 of the Tax Code of the Russian Federation, non-operating expenses not related to production and sales include reasonable costs for conducting activities not directly related to production and (or) sales. Paragraph 2 of the same article provides that for the purposes of this chapter, losses received by the taxpayer in the reporting (tax) period are equated to non-operating expenses. The arbitration court noted that the company’s activities in using a bank loan do not relate to relationships that must be checked by the tax authority for their economic feasibility. The inspectorate did not provide evidence of the taxpayer’s bad faith and that the named type of activity is aimed at evading taxation. Thus, the court recognized, the costs of the disputed interest are rightfully classified as expenses that reduce taxable profit.

Meanwhile, arbitration courts consider it unlawful to reflect interest on loans received in tax accounting when these expenses cannot be attributed to expenses aimed at generating income (Resolution of the Federal Antimonopoly Service of the West Siberian District dated December 19, 2005 in case No. F04-9084/2005(18149 -A27-37), F04-9084/2005(17975-A27-37)). For example, in one of the disputes, the court drew attention to the fact that the amount of the loan received was used by the taxpayer to issue an interest-free and irrevocable loan to a third party, and not to finance statutory activities. In this regard, the court indicated that expenses in the form of interest on the loan do not meet the requirements established in paragraph 1 of Art. 265 of the Tax Code of the Russian Federation cannot reduce the tax base for income tax, therefore attributing the paid interest on a loan to expenses is unlawful. The court noted that the taxpayer did not confirm the validity and economic justification of these expenses. This approach is given in the Resolution of the Federal Antimonopoly Service of the West Siberian District dated May 25, 2005 in case No. F04-2958/2005 (11284-A46-15).

Meanwhile, it is necessary to take into account: the economic purpose of a short-term (revolving) loan and its specificity lie in the fact that the recipient of the loan has the opportunity, at a convenient time during the validity of the loan agreement, to quickly receive money if the need arises to replenish working capital. Therefore, from the very purpose of the loan it follows that it is not necessary that the borrower choose loan funds every month. This means that at some point the borrower may not attract them. However, this should not negate the connection between the expenses incurred by the organization and its production activities.

Thus, if the above conditions for expenses are met, the company has the right to include in expenses that reduce taxable profit the costs of paying fees for providing a revolving loan and for arranging financing.

Expenses for banking services – other or non-operating

In some cases, it is quite difficult to establish a connection between an enterprise’s costs for paying for banking services and the organization’s core activities. As an example, let's take the bank commission charged for servicing a loan account that was opened to support a loan. It can be argued that the commission is charged for the bank providing financing for the commercial company to carry out its activities. That is, on the basis of sub. 25 clause 1 art. 264 of the Tax Code of the Russian Federation, the commission can be considered other costs associated with production and sales. But we can also say that the banking commission does not have a direct focus on carrying out the production and sales activities of the enterprise. The bank's remuneration only mediates the company's receipt of borrowed funds. Accordingly, on the basis of sub. 15 clause 1 art. 265 of the Tax Code of the Russian Federation, the commission must take into account non-operating expenses.

As for judicial practice, arbitration courts side with the taxpayer (as in the case of the FAS Moscow Region Resolution No. F05-11313/12 dated October 11, 2012), because in such a situation, paragraph 4 of Art. 252 of the Tax Code of the Russian Federation allows taxpayers to make a choice in favor of one of the positions at their discretion.

What can be said for sure is that when choosing any of the proposed options (accounting for bank commissions as part of non-operating expenses or as part of expenses associated with production and sales), the tax base for income tax is not distorted. Therefore, making a mistake is not so scary - the tax authorities are loyal to the company’s choice and accept its position.

What price does the bank pay for remote customer service?

Compared to other industries, banks spend much more on information technology. According to McKinsey, on average 4.7-9.4% of operating profit comes from IT.

In comparison, insurance companies contribute 3.3% and airlines 2.6%. For the banking sector, these costs include not only remote service, but also IT infrastructure and architecture, help desk, development of front and middle/back systems. In monetary terms, this all amounts to billions of rubles, depending on the number of tasks facing the technology team.

For example, last year VTB announced a tender for software development with a starting contract price of 15 billion rubles

. The list of works included a modification of VTB Business Online, a system for remote banking services for legal entities. We are talking specifically about updating the software, and not about creating IT systems from scratch.

If we talk directly about Internet banking, then the “fork” of its cost can be very wide. The final cost of developing Internet banking is influenced by several factors:

- Business ambitions. In other words, the length of the list of work tasks in order of importance to the development team.

- The number of specialists working on the project. It depends on the amount of work.

- Geography of search for developers - salaries of IT specialists in Moscow are much higher than in the regions.

There are other, more technological nuances. For example, the depth of integration of Internet banking with other bank systems.

With standard ambitions, the bank needs about 20-30 teams that will develop the services that make up online banking. In this case, taking into account overheads - additional time to perform a particular function - which adds another 70% to the development cost, the final amount is approximately 500 million rubles per year.

The main share of expenses (70%) on remote banking accounts for services for individuals

. For business – only about 30%. This difference is due to payback: retail banking (that is, ordinary consumers, not corporations), due to its mass nature, generates income much faster. If a bank has an active base of several million customers, profits can amount to about a billion rubles per month in just a few years.

Common mistakes

Error:

The company refuses to recognize the bank commission for the letter of credit as an expense for bank services.

A comment:

This method is the most beneficial for organizations on the grounds that it allows the commission to be legally attributed to the reduction of income for tax purposes at a time (clause 7 of Article 272 of the Tax Code of the Russian Federation), and not included in expenses through depreciation.

Error:

The accountant recognized as a one-time tax expense the company's expenses for paying bank commissions for servicing employees' salary accounts.

A comment:

Such costs must be distributed between reporting periods, since costs must be taken into account in the period during which they arose based on the terms of the transaction, and card servicing is carried out continuously throughout the annual period.

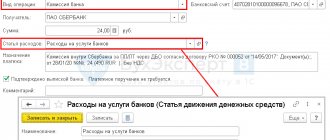

Bank commission - postings in 1C 8.3

In the accounting system, the bank’s commission is reflected in account 91.02 “Other expenses” (clause 11 of PBU 10/99).

Reflect the debiting of the bank commission using the document Debiting from the current account in the Bank and cash desk - Bank statements section.

Specify the type of transaction - Bank commission .

the expense item Expenses for banking services if the item settings indicate:

- Use silently in transactions - Payment of bank commissions .

Familiarize yourself with other ways to reflect bank commissions in 1C 8.3 Accounting

Postings

When you select the type of transaction Bank Commission, a transaction with 91 accounts is generated automatically.

Answers to common questions about the costs of banking services

Question #1:

Does the Ministry of Finance of the Russian Federation equate fees in percentage terms for other banking services, in addition to commissions for issuing a loan, to interest on debt obligations for tax purposes?

Answer:

Yes, according to the Ministry of Finance of the Russian Federation, other payments for banking services expressed as a percentage are also subject to rationing under Article 269 of the Tax Code of the Russian Federation. For example, commissions for opening a letter of credit (Letter of the Ministry of Finance of the Russian Federation dated June 18, 2009 No. 03-03-06/1/408), provision of a loan against the assignment of a monetary claim under a factoring agreement (Letter of the Ministry of Finance of the Russian Federation dated May 13, 2009 No. 03-07-11 /136).

Question #2:

Do employees of the financial department classify the bank's commission for providing a bank guarantee as interest on debt obligations?

Answer:

No. In its Letter No. 03-03-06/1/4 dated January 11, 2011, the Ministry of Finance of the Russian Federation canceled its decision regarding the recognition of the bank commission for the provision of a bank guarantee as interest on debt obligations.