We prepare the implementation: how invoices and delivery notes are issued

Each fact of economic activity is accompanied by the preparation of primary documents.

Based on them, the accountant records the completed transaction in accounting. Operations for the sale of products, work, services, etc. are no exception. During this operation, the seller must issue a primary document (for example, a bill of lading), on the basis of which the product, work, service is transferred (or ownership is transferred) to the buyer. If the seller pays VAT, then in general cases he issues an invoice to the buyer. But he can do this not at the time of transfer of the asset or ownership of it, but within five days after shipment. Thus, the delivery note and invoice are a single set of documents for the sale of goods, but they are intended to take into account various objects. To understand the difference between a delivery note and an invoice, let's look at each document separately.

What is the difference between them?

The difference between an invoice and an invoice is that the latter document is issued exclusively for organizations that are VAT payers. A consignment note differs from any of these types of invoices in that it does not represent information about inventory items, but the very fact of the sale of goods or products.

Invoices issued by various organizations are not always binding. But the invoice data must be entered into the tax records of both counterparties. But the delivery note is issued on the basis of a power of attorney from a third-party organization, that is, it must be issued if the buyer comes to pick up his goods.

The delivery note is signed by both the seller and the buyer. The invoice is signed only by the seller. All these documents indicate the details of the counterparties and information about the product, product or service, as well as their cost, including or excluding VAT.

Attention! Two sample documents are drawn up, one of which remains with the seller, and the other is provided to the buyer.

For more information about what a delivery note and an invoice are and how these documents differ, read this material.

What is a bill of lading used for?

A consignment note in the form TORG-12 is one of the types of primary documents on the basis of which the transfer, for example, of goods purchased for resale or products of own production to the buyer takes place. That is, the invoice is needed to record inventory items.

The form and instructions for filling out the consignment note were approved by Decree of the State Statistics Committee of the Russian Federation dated December 25, 1998 No. 132. However, according to the Law “On Accounting” dated December 6, 2011 No. 402-FZ, economic entities have the right:

- develop your own forms of primary documentation while maintaining the necessary details;

- supplement unified forms with essential details.

Is it necessary to indicate bank details in TORG-12? What if it doesn't have a seal? You will find answers to these and other controversial questions about filling out the document in ConsultantPlus. Trial access to the legal system is free.

Simultaneously with the issuance of the consignment note, accounting entries are generated for the sale of:

- Dt 62.1 Kt 90.1 - reflects the fact of sale of products or goods to the buyer;

- Dt 90.2 Kt 41, 43 - cost of goods or products sold.

Based on the delivery note, the buyer will reflect in his accounting the receipt of material assets by posting Dt 10, 15, 41... Kt 60.1.

List of goods in the delivery note TORG-12

The table with the list of goods is filled with data in accordance with the column headings.

- Column 1 - item number , indicates the serial number of the product.

- Column 2 - Name , indicates the name, characteristics, grade, and article number of the product. If you have a trade turnover and each product is assigned an article number, then it is in this field that it is indicated, either before or after the name of the product, separated by a comma, in parentheses, separated by a dash or other sign.

- Column 3 - Code , in practice it is not filled in and is marked with a dash. This field is in addition to the name of the product and is indicated if it is impossible to identify the product by the name of the product (by the second column).

- Column 4 and 5 - Unit of measurement , indicate the name and code of the unit of measurement of the product, in accordance with the OKEI classifier.

- Column 6 - Type of packaging , in practice is not filled in and is marked with a dash.

- Column 7 and 8 - Quantity , in one place and places, pieces , in practice, is usually not filled in and is marked with a dash. Please note that the quantity of the product is indicated in the tenth column.

- Column 9 - Gross weight , in practice it is usually not filled in and is marked with a dash.

- Column 10 - Quantity (net weight) , indicates the quantity of the product.

- Column 11 - Price, rub. cop. , the price per unit of goods is indicated without VAT.

- Column 12 - Amount excluding VAT, rub. cop. , indicates the amount of the product excluding VAT.

- Column 13 and 14 - VAT rate, % and amount, rub. cop. , the VAT percentage rate and the VAT amount are indicated.

- Column 15 - Amount including VAT , indicates the amount of the product including VAT.

Total by invoice - the sums of numbers in columns Nos. 8, 9, 10, 12, 14 and 15 are summed up.

What is the difference between a bill of lading and other transfer documents?

We have already found out when a delivery note is issued, but in addition to it, other transfer documents can be issued during the sales process:

- invoice for the release of materials to the third party - form No. M-15;

- act of completion of work / provision of services;

- act of acceptance and transfer of fixed assets - form No. OS-1, etc.

From the names it is clear that the execution of the listed documents occurs depending on what property is being transferred: materials, work, services, fixed assets, intangible assets, etc.

All these documents are characterized by the fact that they must contain the details of the transferring and receiving parties, the name and, if necessary, characteristics of the transferred asset, quantity, price and value, the date when the asset was transferred, etc. The documents must be certified by the signatures of authorized persons with each party to the transaction and sealed (if any).

Look at what details should be present in the primary documents.

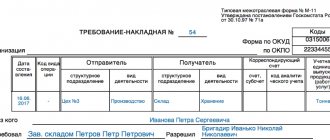

The lower part of the consignment note TORG-12 (basement)

The lower part contains the summary data of the delivery note:

- The consignment note has an attachment on _ sheets - in practice it is not filled out, it is marked with a dash.

- contains _ serial numbers of records - indicates the number of serial numbers of the record in the list of goods. You must write the number in words.

- Total seats _ - in practice it is not filled in, it is marked with a dash.

- Cargo weight (net) _ and Cargo weight (gross) _ - in practice they are not filled in, they remain empty.

- Application (passports, certificates, etc.) on _ sheets - in practice it is not filled out, a dash is added.

- Total issued for the amount of _ - indicates the total amount of all goods in the invoice. You must write the amount in words.

Signatures of responsible persons (left side, seller):

- The release of cargo is authorized - the position, full name and signature of the responsible person are indicated.

- Chief (senior) accountant - the full name and signature of the chief accountant are indicated.

- The cargo has been released - the position, full name and signature of the responsible person are indicated.

Shipment of goods . An individual entrepreneur signs only once in the column Release of cargo allowed. In large companies, different people can sign in all three places, in accordance with their job responsibilities. In small companies, the same person may sign in all three places, for example, the General Director . The manager can also sign in all three fields, but only with a valid intra-organizational order with the right to ship goods, sign shipping and accounting documents.

What is the purpose of an invoice and how is it different from a delivery note?

An invoice is a primary document used to record value added tax. The seller-taxpayer is obliged, when performing transactions subject to the specified tax, to issue an invoice, thus showing the accrual of VAT: Dt 90.3 Kt 68/VAT.

An invoice can be issued not only upon shipment, but also under other circumstances (for example, when funds are received from the buyer as an advance), when an invoice is not required, but VAT must be charged.

The buyer - a VAT payer has the right, on the basis of the received invoice, to accept the amount of VAT for deduction, reducing the amount of tax payable to the budget. The buyer's incoming VAT is reflected on the basis of posting Dt 19 Kt 60.1, and the tax deduction statement is Dt 68/VAT Kt 19. However, for this, the document must comply with all the requirements of tax legislation.

The form of the invoice and the rules for filling it out are given in Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137 (as amended on August 19, 2017 No. 981). The invoice, as well as the delivery note, must indicate the name of the product, its quantity, unit price and total cost, VAT rate and amount, amount including VAT. In addition, the details of the seller and buyer (shipper, consignee) are provided here. The document is certified by the signatures of authorized persons (usually the manager and chief accountant of the organization or individual entrepreneur). Unlike the consignment note, there is no space for printing in it.

What details of the consignment note in the TORG-12 form are required to be filled out in order to accept expenses for tax accounting and apply VAT deductions? You will find the answer to this question from 2nd class adviser to the State Civil Service of the Russian Federation E. S. Grigorenko in K+, having received trial access to the system for free.

Question and answer: Registration of TORG-12

Title of the document; date of compilation; name of company; content of a business transaction; meter of business transactions in physical and monetary terms; a list of officials responsible for the execution of a business transaction and the correctness of its execution; personal signatures of these persons and their transcripts.

The service does not issue TORG-12 for spare parts. How to correctly reflect in accounting the costs of spare parts issued in the work order by a car service?

What will be the basis for the receipt and write-off of these spare parts?

: There is no need to come in separately and then write off as expenses the cost of spare parts that were replaced in the car when it was repaired by a car service center. After all, the property was not actually transferred to you.

The car service has performed repair work for you. Based on the work order and the work completion certificate, you simply take into account the following at a time:

- in tax accounting - as other expenses.

- in accounting - as expenses for ordinary activities (posting debit 20 “Main production” (26, 44, etc.) - credit 60 “Settlements with suppliers and contractors”);

HER. Fofanova, Perm Our new suppliers are located in Magnitogorsk.

The second copy of the consignment note is transferred to the buyer (consignee) and is the basis for recording these values and deducting VAT. Primary documents are signed by the manager and chief accountant or authorized persons.

In what cases is it possible, in what cases is it not? March 26, 2021, 14:24, question No. 1196160 Alexander,

Situation 2. Delivery is a separate service. But what if the cost of delivery is specified in the contract? This is an independent service, the provision of which must be documented in a primary document. And this depends on how delivery will be organized - by our own transport or by a third party.

Therefore, the buyer must write out: (if) the goods will be delivered to the buyer by a third-party organization - TTN.

In this case, there is no need to draw up a separate act for delivery of goods.

After all, all data on transportation is in the transport section of the TTN; (if) you deliver the goods by your own transport - an invoice in form N TORG-12 and an act for the provision of delivery services. However, please note that

The cost of delivery is included in the waybill No. TORG-12 as a separate line (we also write out the waybill).

The first copy remains with the organization handing over the inventory items and is the basis for their write-off.

The second copy is transferred to a third party and is the basis for the recording of these valuables. At the same time, in our opinion, reflecting delivery services as a separate line in the invoice is not a violation of the requirements of the legislation of the Russian Federation on filling out this document, and it is not a basis for recognizing the cost of delivery services in the buyer’s accounting.

Therefore, in order to avoid tax disputes, an organization should confirm delivery with a certificate of services rendered issued by a third party. As for the consignment note, in essence, this document is the basis for the seller to recognize delivery costs provided by a third-party transport organization as income tax expenses.

Based on the above, the following conclusions can be drawn.

The consignment note in form No. TORG-12 certifies the movement of goods and does not serve as a document confirming the provision of transport services.

This is stated in the Letter of the Ministry of Finance of the Russian Federation dated February 27, 2007 No. 03-03-06/1/135. When transporting cargo, motor transport organizations must issue a consignment note (Form No. 1-T). If the buyer does not have documents confirming delivery issued by a third-party organization, there will be no reason to include the costs of such delivery in profit expenses.

At the same time, we inform you that this Answer expresses the private opinion of a tax consultant, is of an informational and explanatory nature and does not prevent you from following the norms of the legislation of the Russian Federation in an understanding that differs from the interpretation set out in the above Answer.

(Answer prepared using materials from SPS ConsultantPlus)

Guided by paragraph 1 of Art. 5 of this Law, general methodological guidance of accounting in the Russian Federation is carried out by the Government of the Russian Federation. The Government of the Russian Federation adopted a resolution dated July 8, 1997.

No. 835. According to this resolution, the State Committee of the Russian Federation on Statistics (now Rosstat) is entrusted with the function of developing and approving albums of unified forms of primary accounting documentation and their electronic versions. At the same time, the content and composition of the unified forms of primary accounting documentation are agreed upon by the Committee with the Ministry of Finance of the Russian Federation and the Ministry of Economy of the Russian Federation.

Thus, by resolution of the State Committee on Statistics of the Russian Federation dated May 29, 1998 No.

As a rule, the price and quantity of transferred products are indicated in the contract or in annexes (specifications). An option is possible when, under the terms of the contract, the price of the goods is determined by the current price list of the company, and the quantity is determined in the application from the buyer.

An alternative form is a universal transfer document (Letter of the Federal Tax Service of Russia dated October 21, 2013 No. ММВ-20-3/ [email protected] ).

Typically, the TORG 12 consignment note is drawn up by the seller. The form contains information about the seller, buyer, name of the product, its quantity and cost, information about the financially responsible persons who shipped and received the goods.

| Invoice column TORG 12 | Invoice TORG 12, filling rules |

| Shipper organization, address, telephone, fax, bank details | The name fits both full and short. |

| Structural subdivision | Maximum complete information (name, contact details). |

| Provider | Full and short name, address and bank information. |

| Consignee | Same as for the supplier. |

| Payer | The purchasing organization is indicated (if it independently purchases and pays for the cargo). |

| Base | The data of the contract or work order on the basis of which the transaction took place is indicated. |

| OKUD and OKPO codes, type of activity according to OKDP | The codes assigned to the organization by the statistics body upon registration are indicated. |

| Tabular section TORG 12 | The supplier lists the goods sold, their units of measurement and quantity, gross and net weight, price and VAT rate. The amount of goods with and without VAT is also indicated here. |

| The consignee received the cargo | Signature of the manager or employee who has the right to sign (order, power of attorney). |

| Accepted the cargo | Signature of the financially responsible person receiving the goods (storekeeper, driver, manager, etc.). |

| By power of attorney No. | Power of attorney details of the employee who received the cargo. Not to be filled in if the manager signed the line “The cargo was received by the consignee”. |

| The consignee received the cargo | To be completed when the cargo is received by the head of the organization. |

| Supplier side printing location | The supplier's seal is affixed, if available. |

| Place of seal on the part of the consignee | The consignee's stamp is affixed. If the cargo is received by proxy, then stamping is not required. |

| Date indicator | The actual date of shipment must match the date on the invoice. |

Employees of organizations should pay attention to the details of filling out the document. This often helps to minimize the legal and tax risks of companies.

Pay attention to the seal! So, for example, a seal is not a mandatory requisite (it is not named in the list of mandatory requisites in 402-FZ). But the TORG 12 consignment note must have a stamp, since it is provided for by the form. On this issue, disagreements may arise when offsetting VAT with the tax office.

Persons who signed the invoice on the part of the seller and the consignee bear, among other things, criminal liability in the event of, for example, theft or theft of goods. Therefore, accountants need to pay special attention to the presence of all the necessary signatures in the document when accepting it for accounting.

If the goods are returned to the supplier, TORG 12 is filled in by the buyer: a “reverse” sale occurs. The rules for filling out the document in this case remain unchanged.

Invoice template

Option 1. Use the form of a universal transfer document (UDD) recommended by the Federal Tax Service. In this case, “1” must be indicated in the “Status” field of the UPD.

1) supplement the invoice form with the following details (part 2 of article 9 of Law N 402-FZ, clause 9 of the Rules for filling out an invoice)):

- a description of the business transaction - the release of goods (for example, “the goods were released” or “the cargo was released”);

- the title of the position of the representative of your company who released the goods, with his signature, surname and initials;

- a description of the business transaction - acceptance of goods (for example, “received the goods” or “received the goods”);

- the title of the position of the company representative - buyer or consignee, with his signature, surname and initials;

2) by order of the head of the organization, to approve such an amended invoice form as a primary document as an annex to the accounting policies.

However, you cannot exclude any invoice details from the combined document.

The supplemented invoice or UPD must be drawn up:

- upon shipment, and not within five calendar days from the date of shipment;

- in two copies, one of which is given to the buyer, and the second is recorded in the sales book - just like a regular invoice.

Is it possible to issue a delivery note and an invoice in one document?

So, a delivery note is intended to account for inventory items, an invoice is intended to account for VAT. Is it possible to compose them in the form of one document?

Maybe. Such a document has been in effect since 2013 - from the moment the Federal Tax Service issued a letter dated October 21, 2013 No. ММВ-20-3 / [email protected] in order to facilitate the document flow of business entities. The letter contains a new form with the details of both documents. It was called UTD (universal transfer document).

Our legislation periodically adjusts the invoice form, and therefore the UTD form also changes.

UPD replaces:

- set of invoice and transfer document;

- transfer document.

The law does not oblige the use of UPD; this is voluntary. If a business entity decides that the UTD will be issued during shipment, then it is better to register such a decision in the accounting policy.

How to do TN correctly?

In printed version according to TORG-12

To compile it, it is advisable to use TORG-12. The document contains information about the seller and buyer .

How many copies need to be issued? The delivery note must be written out in two copies:

- one copy must remain with the company supplying the goods, since this is the primary accounting document for writing off the goods;

- the second must be with the organization purchasing the products, and is the right to use inventory items.

The paper version requires 5 signatures:

- three from the supplier side;

- one on the recipient's side;

- another one is placed by the person responsible for the cargo, in the line “The cargo was received by the consignee.”

You can find out how to correctly fill out a delivery note, as well as study the form and a sample of the TORG-12 form in our material.

Requirements for the electronic version

The formation of an electronic version is similar to a paper one , the only difference is that the electronic technical specification is created in one copy. It consists of two files: the first file is compiled by the seller, the second - on the buyer’s side, when sending the document.

An electronic signature is used to sign the electronic version. There should be only two signatures on the invoice - one on each side.

Thus, the paper version of the TN does not require an electronic signature; it can be compiled and transmitted without the use of a computer or the Internet.

An electronic version of the TN can be drawn up in cases where both parties have access to the Internet and everyone has an electronic signature.

Results

So what is the difference between an invoice and a delivery note?

They are intended to reflect two different accounting objects in the accounting and tax registers. The delivery note takes into account inventory items, and the invoice takes into account VAT. Both documents are issued upon shipment or upon transfer of title, but the invoice is issued immediately at the time of shipment, and the invoice is issued within 5 days after that. The information reflected in these two documents overlaps to some extent. That is why, in order to simplify document flow, tax authorities have developed a single form that combines the details of the invoice and the primary transfer document. A sample UPD is shown above. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

General rules

- How to set TN according to TORG-12? If the sale of goods is intended, then the basis for drawing up TORG-12 is a supply agreement. The price and quantity of products that belong to the transfer are indicated in the contract or annexes.

- The form contains information about the shipper, supplier, payer; date and number of the invoice; a table is filled in with a list of supplied products in accordance with the data in the invoice for this delivery batch; three signatures are placed.

- The invoice is prepared by the supplier of the goods.

- The sequence number is considered a property and is used to take into account the order and synchronization of processes. But at the same time, the lack of numbering is not a serious error and the document will be valid. The law does not provide for strict numbering for this document, so the type of numbering is chosen by the enterprise itself.

- The paper form must have five signatures: three on the seller’s side and two on the buyer’s side. On the supplier's side, all signatures must be required; their absence leads to tax liability.

But at the same time, there are no negative consequences for the buyer if one signature (in the “Cargo accepted” column) is missing.Two electronic signatures are placed on the electronic version, on the part of the supplier and on the part of the recipient. Both signatures are required.

- Is a buyer's stamp required on the TORG-12 document issued for the goods? The delivery note (both copies) must be certified with a seal if receipt is made without a power of attorney. Is a seal required, if there is a power of attorney and the goods are received according to it, is it necessary to simultaneously put a stamp on TORG-12 and present the document? If received by proxy, a stamp is not needed; moreover, the seller’s requirement to simultaneously affix a stamp and present a power of attorney is unlawful.

Read about why you need a bill of lading, whether it can replace a sales receipt, and from this article you will learn about the difference between an invoice and a delivery note, as well as the nuances of using both documents.