Often citizens who do not have legal knowledge, when they hear about an assignment or assignment agreement, do not understand what we are talking about. This fact may lead to the fact that, if necessary, a person is unable to protect his rights. The fact is that this document is drawn up to alienate the right to loan obligations to another individual or legal entity, guided by the legislation of the Russian Federation.

In other words, this is an agreement to transfer financial responsibility and obligations without the consent of the person holding the debt. The most typical example of such an agreement: the bank sells the obligations of clients to collectors. Let's consider what accounting entries document the assignment of the right to claim debt between legal entities.

Dear readers! Our articles talk about typical ways to resolve legal issues, but each case is unique.

Basic provisions

Legal details regarding the assignment agreement are indicated in Art. 382, 390 - 392 of the Civil Code of the Russian Federation. There are three parties to the agreement:

- assignor - transferring the right to claim the debt;

- assignee – accepting the right to claim an obligation;

- debtor.

If an assignment agreement is drawn up, a bilateral agreement can be concluded, in which case it is not necessary to have consent from the debtor; it is enough to notify him, or to draw up a tripartite agreement.

It is important to note that it is impossible to arrange an assignment for personal debts:

- payment of moral damages;

- satisfaction of material damage, as well as damage caused to life and health;

- alimony payments.

Grounds for transferring rights under an assignment agreement

The basis for recording transactions involving the transfer of rights to claim debt is an assignment agreement. The agreement can be drawn up by two parties and signed by the creditor and the recipient of the claim.

In addition, the parties can enter into a tripartite agreement, the signatories of which will be the assignor, assignee and debtor.

In addition to the assignment agreement, the transfer of rights to claim a debt can be carried out on other grounds provided for by the Civil Code of the Russian Federation. Most often, such grounds are court decisions and other executive documents.

How is the assignment of debt between legal entities reflected in accounting?

According to clause 3 of PBU 19/02, DZ, which was purchased under an assignment agreement, is an object of financial investment, taking into account compliance with a list of criteria.

Therefore, in the case of acquiring a DZ assignment under an agreement, it is important that the following conditions are met:

- there is available documentation that will confirm the right to obligations;

- along with the debt, the assignee receives financial risks associated with the obligation;

- future economic benefits pass to the assignee.

The assignee has no right to change the terms of the original agreement. In this case, the transaction may be challenged in the future.

If all these points are met, then the assignee takes into account the acquired debt in the account. 58 “Financial investments”.

The assignee reflects the acquired debt at the cost of all costs that it incurred during the acquisition process:

- expenses that were paid to the assignor under the concluded agreement;

- expenses for services that were required to purchase finance. attachments;

- remuneration paid to intermediary organizations.

Allocation of the VAT amount is required only if the purchased debt was formed as a result of the functioning of an agreement for the sale of goods (services or work). In such a situation, VAT is required to be charged on the excess of the debt that needs to be repaid over expenses. The tax is calculated - 18/118 or 10/110 (clause 2 of article 155; clause 4 of article 164 of the Tax Code of the Russian Federation).

And then the assignor, in turn, takes into account the requirements for the assignment agreement on the account. 91.

The debtor reflects the amount on the required account, on which the analytics must be present. Therefore, when a creditor changes, the debtor must reflect the changes in analytical accounting.

From the date of signing the agreement, the primary lender writes off the debt - the obligation of a specific borrower.

Documentation of the assignment by the assignee

The Civil Code does not stipulate the concept of assignment of debt. To manipulate the transfer of obligations, the law provides two options:

- assignment of the right of claim;

- transfer of debt.

Obligations are transferred under transfer agreements using the procedure described in Art. 391 Civil Code of the Russian Federation. And the assignment of the right of claim is regulated by Art. 388 Civil Code of the Russian Federation. At times, confusion arises between the assignment of a claim and the transfer of a debt.

Note from the author! An assignment of the right of claim is a situation when the creditor, that is, the party collecting the receivable, changes. Debt transfer, on the contrary, is a change of debtor who transfers his obligations to a third party.

Features of displaying transactions in enterprise accounting depend on the party on which the party to the agreement acts. In case of transfer of your rights, an assignment agreement is concluded. The creditor who assigns the original right to collect the obligation is called the assignor, and the new owner of the debt is called the assignee.

For the assignee, the newly received debt becomes a financial investment under clause 3 of PBU 19/02. Of course, for this a number of conditions must be met:

- Availability of primary documents on the occurrence of obligations.

- The ability to obtain economic benefits from the acquired liability.

- Financial risks associated with arrears.

The assignee makes special accounting entries:

- Debit of account 58 “Financial investments” - Credit of account 76 “Settlements with various debtors and creditors.”

The new owner records a profitable debt for the total costs incurred for its purchase:

- for information and consulting services;

- intermediary fees;

- to the assignor for the acquisition.

When the debtor pays off his monetary obligations, the assignee carries out the necessary operations in the accounting program:

- Debit 76 of account Credit 91.01 “Other income” - the financial result is accounted for in the form of debt repaid under assignment.

- Debit 91.02 “Other expenses” Credit 58 “Financial investments” - the transferred receivables are repaid.

- Debit 51 “Current accounts” Credit 76 accounts - money came from the debtor by bank transfer.

Since receivables include accrued value added tax, the assignee must also take into account VAT:

- Debit 91.02 “Other expenses” Credit 68.02 “Value added tax”.

Postings from the parties to the contract

After concluding an assignment agreement of the right to claim debt between legal entities, the assignee’s transactions will look like this:

| Debit | Credit | Operation description |

| Dt 58 | Kt 76 | Accounting for acquired debt |

| Dt 76 | Kt 91 | When the debtor repays the debt, the assignee records income as the amount received |

| Dt 91 | Kt 58 | The amount of the obligation contributed by the debtor is written off |

| Dt 51 | Kt 76 | Received funds from the debtor |

If VAT has been charged, then in the situation of expiration of the agreement or in the event of the next assignment, the assignee makes the following entry: Dt 91 Kt 68/for analytical accounting, a value added tax subaccount is used.

When assigning a debt between legal entities, the accounting entries made by the assignor look like this:

| Debit | Credit | Operation description |

| Dt 76 | Kt 91 | The amount of income received from the sale is reflected |

| Dt 91 | Kt 62 (76) | The amount of the repaid liability is written off |

| Dt 51 | Kt 76 | Settlements under the contract in case of payment |

This material will tell you in detail how to draw up an agreement on the assignment of the right of claim between legal entities.

Participants in the assignment of claims

From the name it becomes clear that the contract is concluded so that one party to the contract cedes its right of claim to another party. By rights we mean receivables. So why do organizations resort to such measures?

Let's take, for example, organizations conducting joint activities under a supply agreement, provision of services or provision of a loan. Sometimes, after some time of working together, the buyer, despite strict payment terms and penalties for delay specified in the contract, does not transfer money to the supplier.

The supplier decides to sell its receivables by concluding an assignment agreement with a third-party company. He can do this without notifying his debtor partner (Articles 382, 384, 385 of the Civil Code of the Russian Federation).

When concluding an agreement for the assignment of the right of claim, the parties to the transaction are the following participants:

- seller (assignor);

- buyer (assignee).

The debtor, i.e., an organization that does not want to repay its creditor, is sent a letter indicating the details of the new creditor and the details of the assignment agreement on the basis of which the debt was transferred to it.

After signing the agreement, the assignor transfers all primary documents to the assignee. They will be confirmation of the purchased debt.

Such documents include:

- supply agreement (service or loan);

- delivery notes, acts, invoices, etc.;

- act of reconciliation between the assignor and the debtor.

After this, the parties to the transaction need to make the appropriate entries under the assignment agreement in accounting.

Registration in the 1C program

In 1C, in such cases, manual entries are made. Documents are generated in the “Operations entered manually” section; you can find the item in the “Operations” menu.

The assignment of debt between legal entities in 1C is reflected by the following transactions:

| Debit | Credit | Operation description |

| Dt 76.09 (with analytics for the lender) | Kt 91.01 | The entry amount is made up of the assignee's obligation under the agreement |

| Dt 91.02 | Kt 62.01 | The size of the debt is indicated in accordance with the amount of the assignor |

The assignee must generate transactions of the following type:

| Debit | Credit | Operation description |

| Dt 58.05 | Kt 76.09 | The amount of this operation is the total costs that were incurred for the purchase of remote control |

Repayment of obligations is reflected as follows:

| Debit | Credit | Operation description |

| Dt 76 | Kt 91.01 | The amount of debt that must be collected from the debtor |

| Dt 91.02 | Kt 58.05 | For the amount of actual costs incurred |

| Dt 51 | Kt 76.09 | Based on the amount of funds received |

Assignment agreement in 1C 8.3 from the debtor

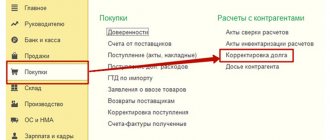

Automation of accounting at the debtor's enterprise implies the following actions: having received notification of a change of creditor, the debtor must transfer the amount of debt from one counterparty to another. To do this, use the “Debt Adjustment” document, which can be located in the “Purchases” and “Sales” sections.

Fig. 1 Purchases - Debt adjustment

Fig.2 Sales-Debt Adjustment

Create a new document Debt adjustment. In the document:

Type of operation – Transfer of debt; Transfer – Debt to the supplier.

We fill in the data on the creditor and the new supplier from the counterparties directory.

By clicking the “Fill” button, you can automatically generate a tabular part, and, if necessary, later adding the necessary parameters (in our case, these are a New Agreement and a New Account).

Fig.3 Fill in

Let's look at the entries in the document.

Fig.4 We look at the postings according to the document

Sometimes there is a need to reformat a document, but an error occurs - it is suggested that you first unapprove it. Here you can use the menu option using the “More” button.

Fig.5 Unconfirm

How can the assignor reflect the assignment of the right of claim in accounting?

At the same time, on the date of signing the assignment agreement, make an entry in the accounting: Debit 76 subaccount “Settlements under the agreement of assignment of the right of claim” Credit 91-1 - the right of claim under the assignment agreement has been realized. When transferring property rights, the assignor may have an obligation to charge VAT if the amount of income from the transfer of the claim exceeds the size of the claim itself (paragraph 2, clause 1, article 155 of the Tax Code of the Russian Federation). For more information about this, see. The value of the right of claim, at which it is recorded on the assignor’s balance sheet, is reflected as part of other expenses in the debit of account 91 (clause

Assignment agreement: accounting entries for the assignor

The original creditor records the transaction as a disposal of property. That is, the amount of debt must be written off as other expenses, and the amount of the assignment must be written off as income.

At the same time, if the obligation is sold at a profit, then VAT must be calculated and paid to the budget on the difference between income and expenses. This situation is rare. As a rule, the right of claim is realized at a loss.

Assignment of the right of claim, accounting entries for the assignor:

| Operation | Debit | Credit |

| The obligation under the assignment agreement has been transferred | 76 | 91-1 |

| The liability being sold is written off | 91-2 | 62, 66, 67 |

| Payment received from assignee | 51 | 76 |

In tax accounting, when a debt is sold after the payment due date, the loss is fully recognized. If sold before payment is due, the loss is recognized in the manner set out in paragraph 1 of Art. 279 Tax Code of the Russian Federation.

Assignment of debt between legal entities: accounting entries

Alize LLC paid its debt to .

The accounting records of the accountant of Kassandra LLC show the following entries:

- demand purchased Db 58, Kd 76, subaccount is 210,000 rubles; the demand was paid in full by Alize LLC in the amount of 210,000 rubles; money was received from Vympel LLC Db 51, Kd 76, the subaccount is 250,000 rubles. income from the repayment of debt of Vympel LLC db 76 is officially recognized, the subaccount is 250,000 rubles; the amount of debt 210,000 rubles was transferred.

Sometimes creditors decide to forgive the debt to the borrower and then it is necessary to negotiate a bilateral agreement to terminate claims on the debt obligation.