What is a patent for a foreigner, who needs it?

This document is necessary for a foreign citizen who wishes to officially find employment in the Russian Federation. A patent certifies the legality of employment for a foreigner.

What you need to know about this document:

- It is issued for a period of one month to a year.

- Its action is limited to a certain territory.

- Issued for a specific profession and type of activity.

- To obtain one, you must undergo a medical examination.

- Issued with the permission of the Migration Service.

Nuances of a labor patent

In order for the employment relationship with the employer to be considered completely legal, after obtaining a patent the following actions must be taken:

- Prepare a copy of the employment contract with the employer.

- Contact the Ministry of Internal Affairs for subsequent registration.

Important! The above actions must be performed by the foreign citizen no later than two months after signing the employment contract. It is necessary to pay the tax on time to avoid invalidation of the patent.

Increase in fixed advance payments for personal income tax in 2020

Fixed advance payments for personal income tax for foreigners who work under a patent are planned to be increased in 2021 by a new deflator coefficient - 1.813 (approved by order of the Ministry of Economic Development of the Russian Federation dated October 21, 2019 No. 684 (versus 1.729 in 2021)).

The fixed payment is annually indexed by a regional coefficient, which is established in each subject of the Russian Federation for the calendar year.

For example

, The Government of Moscow has established a regional coefficient reflecting the regional characteristics of the labor market in the territory of Moscow for 2021 - 2.4591 (in 2021 - 2.4099 - Moscow Law of November 20, 2019 No. 29 “On establishing a coefficient reflecting the regional characteristics of the labor market in the city of Moscow").

The fixed advance payment for personal income tax for obtaining a patent for work in Moscow will be calculated in the following order:

1,200 rub. x 2.4591 x 1.813* = 5,350 rubles.

*Note.

At the time of writing, it is known that the Ministry of Economic Development of the Russian Federation has prepared a draft order for amendments, according to which the deflator coefficient will be reduced from 1.813 to 1.810. If the order is registered with the Ministry of Justice of the Russian Federation in the prescribed manner, all fixed advance payments for the patent for 2021 established by that time will change.

Important!

If a patent was issued in 2021, but its term ends in 2020, then there is no need to recalculate personal income tax taking into account the deflator coefficient for 2020. This conclusion is confirmed by explanations from regulatory authorities (Letters of the Federal Tax Service of the Russian Federation dated January 27, 2016 No. BS-4-11/1052, Ministry of Finance of the Russian Federation dated March 19, 2018 No. 03-04-07/17158).

What taxes does a foreign worker pay?

Having an employment relationship on the territory of the Russian Federation, a foreigner pays types of taxes similar to those of local citizens.

Foreigners have received the right to a personal income tax refund, since they pay it twice. This occurs when paying tax, as well as when the employer withholds 13% when calculating wages. If there is no patent, but there is permission, taxes are calculated at a higher rate. It is tied to the period of residence in the territory of the state:

- A 30% rate is imposed on persons whose stay does not exceed six months.

- If a person has been staying in the Russian Federation for more than six months, the rate is reduced to 15%.

Interesting. Highly qualified specialists are allocated to a separate category. Regardless of the length of stay, the rate for them is 15%.

Certain groups of citizens are not required to purchase a patent. This:

- refugees;

- citizens of Belarus, Kyrgyzstan, Armenia and Kazakhstan.

Personal income tax rate for foreign citizens

The personal income tax rate will vary depending on the type of income, status and residence. Residence status is determined by the time spent on the territory of the Russian Federation. Thus, foreigners who have stayed in Russia for less than 183 days (calendar) within one year are non-residents. And persons with a special status are recognized as:

- refugees;

- high-class specialists;

- foreigners holding a patent;

- residents of the EAEU countries.

Read also: Immigration to Italy from Russia

| Foreign citizen status | Personal income tax rate (%) | ||

| Income from employment | Other types of income, with the exception of winnings and dividends, which are taxed at a higher rate | Profits from participation in a joint stock company | |

| Special status/resident of the Russian Federation | 13 | 13 | 13 |

| Special status/non-resident of the Russian Federation | 13 | 30 | 15 |

| No special status/resident of the Russian Federation | 13 | 13 | 13 |

| No special status/non-resident of the Russian Federation | 30 | 30 | 15 |

Reduction of personal income tax by the amount of a patent for a foreign citizen

Taxes are withheld from foreigners in accordance with the law.

It is not possible to issue a recalculation and receive a refund in advance. This can only be done after the tax period, once a year. In 2021, the previously in force order has been maintained. A foreign worker can apply for a deduction in person by contacting the tax service. Or submit an application to your employer, who will prepare documentation for transmission to the tax authorities.

After receiving an application with a package of documents, a tax officer conducts an inspection with the participation of the migration service. A ten-day period has been established for verification.

Read also: Repatriation to Israel in 2021

A prerequisite for approval of an application for a personal income tax refund is the implementation of legal work activities. The foreign worker must have all the necessary work permits, supporting documents, as well as a formal employment contract with the employer.

If an employee has several jobs, he makes a tax refund once, through the main employer. When conducting an audit, the tax officer will definitely check whether applications for a specific person have been received from other places of work.

If an organization employs several foreign employees, the accounting department prepares a separate package of documents for each employee to reimburse the tax.

Notice of advance payments for patents form

The article from the magazine “MAIN BOOK” is current as of September 18, 2016 M.G.

Sukhovskaya, lawyer A foreign worker must independently pay advance payments for personal income tax for the issuance, renewal or renewal of a patent; . This responsibility cannot be transferred to the employer. As you know, from 2021, only those visa-free foreigners temporarily staying in the Russian Federation who have a special patent issued by the migration service can be legally employed.

The validity period of the patent directly depends on how many months the migrant has paid a fixed advance payment for personal income tax; .

The payment amount is different in each region. At the same time, the employer, by paying the migrant a salary and calculating personal income tax on it, can reduce the amount of tax on advance payments paid by the foreigner for the period of validity of the patent relating to the current tax period (calendar year); .

Migrant workers “on patent”: we analyze individual personal income tax situations

Photo by Boris Maltsev, Kublog As you know, employers who employ foreigners who have received a special patent 1 can reduce the amount of personal income tax accrued from their salaries by advance payments paid by foreigners for the period of validity of the patent relating to the current calendar year 2.

SITUATION 1. The term of a patent paid for by a foreigner covers two tax periods at once - 2021 and 2021.

Let's say in mid-December 2021.

The cost of a patent obtained by a foreign worker can be offset against personal income tax

13.03.

2016 09:22 (archive) the procedure established by the article for calculating the amount and paying tax on personal income from employment in the Russian Federation on the basis of a patent issued in accordance with the Federal Law of July 25, 2002 No. 115-FZ “On legal status of foreign citizens in the Russian Federation.” From January 1, 2021, employers specified in subparagraph 2 of paragraph 1 perform the duties of a tax agent for the calculation and withholding of personal income tax when paying income to employees - foreign citizens working in the Russian Federation on the basis of a patent.

The total amount of personal income tax is calculated by tax agents and is subject to reduction by the amount of fixed advance payments paid by such taxpayers for the period of validity of the patent in relation to the corresponding tax period (from this year, the amount of the monthly advance payment for personal income tax in accordance with clause 2. is 1200 rubles and is adjusted by established coefficients - for example, the monthly fixed advance payment for foreign citizens working in the Moscow region on the basis of a patent in 2016 is 4,000 rubles)

Order of the Federal Tax Service of March 17, 2021

N ММВ-7-11/ “On approval of the form of notification of confirmation of the right to reduce the calculated amount of personal income tax by the amount of fixed advance payments paid by the taxpayer”

Order of the Federal Tax Service of March 17, 2021 N ММВ-7-11/

“On approval of the form of notification of confirmation of the right to reduce the calculated amount of personal income tax by the amount of fixed advance payments paid by the taxpayer”

In accordance with part one of the Tax Code of the Russian Federation (Collected Legislation of the Russian Federation, 1998, N 31, Art. 3824; 2021, N 1, Art. 15) and part two of the Tax Code of the Russian Federation (Collected Legislation of the Russian Federation, 2000, N 32 , Art.

3340; 2021, N 1, art. 33) I order: 1.

Approve the form of notification confirming the right to reduce the calculated amount of personal income tax by the amount of fixed advance payments paid by the taxpayer in accordance with this order. 2. The departments of the Federal Tax Service of Russia for the constituent entities of the Russian Federation will bring this order to the lower tax authorities and ensure its implementation.

3.

Form 6-NDFL: foreign worker with a patent (filling example)

— , The procedure for filling out and submitting calculations to the tax authority was approved by Order of the Federal Tax Service of Russia dated October 14, 2016 N. Let us recall that calculations are submitted quarterly (section 1 is compiled on an accrual basis for the first quarter, half a year, nine months and a year, and in section.

2 only data for the last three months of the reporting period are included). The deadline for submitting calculations for the first quarter, six months and nine months is the last day of the month following the corresponding period, for the year - April 1 of the year following the expired tax period (Clause 2 of Article 230 of the Tax Code of the Russian Federation).

The basis for non-submission of calculations is only the absence of employees at the organization (IP) and failure to make income payments to individuals; “zero” calculations under these circumstances do not need to be submitted (Letter of the Federal Tax Service of Russia dated 01.08.

2017 N At the same time, in the case of submitting a “zero” calculation, such calculation

Foreign worker: we reduce personal income tax by a fixed advance payment

Announcements Coming soon Vadim Chubarov: “In the future, you can think about dividing the permissions issued to arbitration institutions into full and partial.” What is the role of the amendments to the law that came into force on March 29 in arbitration and in what direction the arbitration system will develop further, read in an interview with the vice-governor President of the Russian Chamber of Commerce and Industry.

September 13, 2021 The employer - tax agent has the right to reduce the personal income tax of a foreign employee by the amount of fixed advance payments paid by him independently.

Foreign worker with a patent: We reduce personal income tax by a fixed advance payment

Important On the topic Read all materials (240) on the topic.

There is an update (+171), including: October 16, 2021 11:44 M. Sukhovskaya Magazine “” No. 19/2016 As is known, from 2021

You can legally hire only those visa-free foreigners temporarily staying in the Russian Federation who have a special patent issued by the migration service. The validity period of the patent directly depends on how many months the migrant has paid a fixed advance payment for personal income tax. The payment amount is different in each region.

Letter dated February 19, 2016 No. BS-4-11/

Source: https://domashenko-advokat.ru/uvedomlenie-na-avansovye-platezhi-po-patentam-forma-12697/

Errors when withholding personal income tax from a foreign worker

The most common mistakes are as follows:

- Incorrect calculation of the amount to be paid to the budget. It happens that a foreigner mistakenly transferred a larger amount to pay taxes than he should have. Such actions can also be intentional. In this situation, you should not hope for a refund of the overpaid amount. In accordance with the Tax Code, such excesses will not be recognized as overstatement.

- Difficulties in identifying persons from the categories of refugees or those who have received temporary asylum in the territory of the Russian Federation who are entitled to the deduction. Refugees, as well as persons granted temporary asylum in the Russian Federation, pay income tax of 13% at a preferential rate. Such non-residents cannot claim deductions. However, having received resident status and continuing to pay income tax, they will be able to claim deductions provided for in Articles 218-221 of the Tax Code.

Article 218 of the Tax Code of the Russian Federation “Standard tax deductions”

Article 219 of the Tax Code of the Russian Federation “Social tax deductions”

Article 220 of the Tax Code of the Russian Federation “Property tax deductions”

Article 221 of the Tax Code of the Russian Federation “Professional tax deductions”

How to pay taxes for a foreigner on a patent

Quantity December 10, 2021

Foreigners

who work in Russia for an employer or individual often pay income tax in a special form - in the form of the cost of

a patent

. The amount of a patent for foreign citizens depends on the region where they work.

Income tax (NDFL) on the salary of a foreigner who works on the basis of a patent is calculated at the rate 13%

. The tax rate does not depend on his status - resident or non-resident.

Alien status affects deductions. Deductions are provided only to those who are residents of the Russian Federation.

As a general rule, tax residents are individuals who are actually in the Russian Federation for at least 183 calendar days over the next 12 consecutive months.

Reasons for reducing personal income tax

The employer can reduce personal income tax by fixed advance payments paid by the employee under the patent for the same year.

To do this, you need the following documents:

P/n Documents Description

| 1 | Employee's application for tax reduction and payment document for payment of a fixed payment | A sample application can be downloaded. |

| 2 | Notification from the Federal Tax Service confirming the employer’s right to reduce tax in relation to a specific migrant | It is necessary to send the form (KND 1110055) to the tax authority along with a copy of the employee’s application and a receipt for payment (from paragraph 1 of the current table) |

Notification is only available for the current year. Next year you need to apply for a new notification.

Example.

How to reduce tax?To reduce personal income tax you need to do the following.

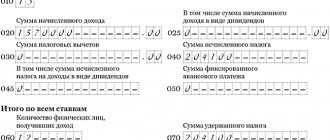

An example of calculating personal income tax when changing tax status. If at the end of the year the amount of the fixed payment paid for this year turns out to be more than the amount of personal income tax withheld from the employee’s income for the year, then the uncredited balance of the advance payment is not carried over to the next year and is not returned to the individual. How to fill out form 2-NDFL?When filling out 2-NDFL For a foreigner who works under a patent, you need to pay attention to the following. In the field “ Payer status” » you need to specify – 6. In the section “ Total income and tax amounts” » in the appropriate field you need to reflect the amount of fixed advance payments paid by the foreigner, by which the tax was reduced. If payments under the patent exceeded the tax calculated on the foreigner’s income, in the field “ Amount of fixed advance payments” "- enter the amount of calculated tax; in the fields "Amount of tax withheld", "Amount of tax transferred", "Amount of tax excessively withheld by the tax agent", "Amount of tax not withheld by the tax agent" - indicate zero. Sample of filling out certificate 2-NDFL for a foreigner on a patent How to fill out the 6-NDFL calculation?Employers must include data on foreigners who work on the basis of a patent in the calculation using Form 6-NDFL . Line 040 reflects the amount of calculated tax; personal income tax from foreigners on a patent must be included in this amount. Line 050 indicates the total amount of fixed advance payments for foreigners on a patent, which reduces personal income tax. This amount should not exceed the total amount of calculated tax.

In lines 110, 120 and 140, zeros are entered for such employees, since there is no tax to withhold and transfer. An example of filling out a 6-NDFL calculation with information about a foreigner on a patent

|