An interest-free loan is the same “receivable”

Loans provided to other organizations are classified as financial investments and are reflected in account 58 “Financial investments”. So says clause 3 of PBU 19/02 “Accounting for Financial Investments” and Instructions for the Application of the Chart of Accounts.

Taking into account only these regulations, in the balance sheet information about interest-free loans is often disclosed as information about the financial investments of the organization. However, let us recall the main criteria for classifying assets as financial (p

2 PBU 19/02 “Accounting for financial investments”):

However, let us recall the main criteria for classifying assets as financial (clause 2 of PBU 19/02 “Accounting for financial investments”):

- the organization’s right to the asset and to receive funds or other assets arising from this right must be confirmed by documents;

- the financial risks associated with obtaining the asset have been transferred to the organization. Such risks may be the risk of price changes, the risk of insolvency of the debtor, liquidity risk, etc.;

- the asset must generate income for the organization in the future.

In relation to interest-free loans, the last criterion is not met, namely the condition on the profitability of the investment. Therefore, it is more logical to reflect issued interest-free loans on the balance sheet as part of accounts receivable on line 230 or 240, depending on their repayment terms.

Line 1230 of the balance sheet, what it includes

- Balance on the debit side of the account. 62 “Settlements with buyers and customers”, takes into account the debt on products, goods, work, services sold to the buyer;

- Account debit balance 68 “Calculations for taxes and fees,” speaks of the debt of budgetary authorities to the organization. Accounts receivable on this account may arise due to amounts transferred during the year, advance payments for taxes from budget funds. The amount of transferred advance payments exceeds the amount of calculated tax for a certain period of time;

- Debit balance by account 69 “Calculations for social insurance and security” tells us about the debt of the social insurance authorities to your company. It may arise, for example, due to the amount of excess expenses calculated by the organization on certificates of incapacity for work before accrued insurance premiums;

- Balance on the debit side of the account. 70 “Settlements with personnel for wages”. A debit balance is very rare. It may arise, for example, due to transfers of amounts to an employee (employee) for accrued leave (labour or pre- and post-natal leave). This happens when, at the beginning of the month, the organization’s employees are paid arrears of wages accrued on the last day of the month, and payment is also made for accrued maternity and postpartum leave. The accrual amount will be reflected in the accounting accounts only on the last day of the month, and payment will be made on the current date;

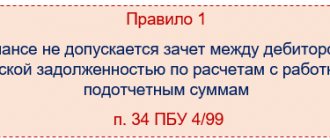

- Debit balance of the account. 71 “Settlements with accountable persons.” Payments to persons to account for funds, non-cash and cash are accounted for on the debit side of the account. 71. After payment, submits a report on expenses incurred to the company’s accounting department. This may include payment for business expenses, payment for purchased materials, expenses for staying in a hotel during a business trip, expenses for moving to and from the place of business trip, and others;

- Debit balance of the account. 73 “Settlements with personnel for other operations.” All relationships between employees of the organization are reflected in this active-passive account, except for payroll calculations and payments of funds to the account. The debit of the account reflects the employee's debt to the organization. An employee may be provided with borrowed funds for construction, rent, and other business needs. Also, the employee may have a relationship to compensate for material damage to the company. These are the situations that are reflected in the score 73;

- Balance on the debit side of the account. 75 “Settlements with founders.” The formation of the authorized capital is taken into account according to the D account. 75 and K-tu account. 80 “Authorized capital”. Until the founder deposits personal funds in the amount of the authorized capital, the debit balance will remain on account 75;

- Debit balance of the account. 76 “Settlements with various debtors and creditors.” Account 76 is active - passive, it reflects debts not reflected in account 60, 62 and other accounts. The account may reflect arrears of payment to the insurance company; claims settlements; withholding funds from employee salaries for third-party companies and persons under executive documents (acts).

We recommend reading: Increasing the Living Wage in St. Petersburg in 2020

Tax accounting of debt on authorized capital: nuances

When maintaining tax accounting of deposits in the management company, you should keep in mind that:

1. Cash and property contributed to replenish the authorized capital by the founder-individual or legal entity:

- are not subject to VAT;

- do not form a tax base for personal income tax, income tax or the simplified tax system.

But if the founder-legal entity pays VAT, then if the tax is accepted for deduction (on property transferred to the authorized capital), the VAT must be restored (subclause 1, clause 3, article 170 of the Tax Code of the Russian Federation). In this case, the amount of recovered and paid VAT cannot be included in profit expenses. The organization for which the authorized capital is formed has the right, in turn, to receive a VAT deduction restored by the founder-legal entity (Clause 11 of Article 171 of the Tax Code of the Russian Federation).

When redistributing a share in a business in favor of a specific founder (or when increasing the nominal value of his share in the authorized capital), the founder does not have to calculate personal income tax. However, if the nominal price of the management company is reduced by decision of the founders (not for the purpose of fulfilling the requirements of the law), then the founders will have to pay personal income tax on the difference between the previous and new value of the shares (letter of the Ministry of Finance of Russia dated April 14, 2011 No. 03-04-06/3-88) .

Upon payment of contributions from all founders in full, the authorized capital may be increased:

- through additional contributions from the founders;

- as a backup option - by raising capital from third parties.

Let's consider the specifics of the main option for increasing the capital, when the owners of the company manage on their own.

An advance on “future expenses” is not a good idea

In practice, there may be confusion between the concepts of “issued advances” and “deferred expenses”. The latter, in turn, are included in line 210 of the “Inventories” balance sheet, and are also allocated separately on line 216. Advances issued are reflected on lines 230 and 240 of the balance sheet.

Deferred expenses include the company's costs for obtaining licenses, as well as certification costs, which require obtaining a certificate for a long period. But paying for a magazine subscription is already considered an advance. This is due to the fact that at the time of transfer of money there is no reason to believe that the service has already been provided.

Note. Errors in the formation of balance sheet receivables and payables indicators

The loan amount is reflected in lines 140 or 250 of the balance sheet asset.

Correction.

Debit 76 Credit 51

100,000 rub. — an interest-free loan was issued to a business partner.

The loan amount is reflected in lines 230 or 240 of the balance sheet asset.

Debit 97 Credit 60

3000 rub. — the subscription amount is charged to deferred expenses.

The subscription amount is reflected in lines 210 of the balance sheet asset.

Correction.

Debit 60, subaccount “Advances issued”, Credit 51

100,000 rub. — a subscription to the magazine has been made, the amount is recognized in advance.

The subscription amount is reflected in lines 240 of the balance sheet asset.

Debit 62 Credit 90

100,000 rub. - work has been completed for which receiving payment subsequently turned out to be unrealistic.

Correction.

Debit 63 Credit 62

100,000 rub. — the amount of debt is included in the reserve

Debit 91 Credit 62.

The amount of debt will not be reflected on the balance sheet.

Debt of founders for contributions to the authorized capital in the balance sheet

An asset is the debit balances of accounts or otherwise current and non-current funds, and a liability is the sources of their formation. Fixed assets are non-current assets. in particular, machines, equipment, buildings, structures, transmission devices, etc. i.e. all funds that are accounted for on August 01, 2003 and have a cost of more than 40,000 per unit. Intangible assets are intangible assets - these include licenses, software products, trademarks, know-how, etc. Read the theory.

Rustemchik, open the book and read it. If you’re already stuck with the basics, then go work as a janitor. It seems that everything is written in Russian: 1) part of the balance sheet (left side), reflecting the composition and value of the organization’s property on a certain date. 2) The totality of property owned by a legal entity or entrepreneur. Use your brains, boy. It will get worse.

Assets and liabilities of the balance sheet: how to stop confusing them

Balance sheet liabilities are the company's debt to third parties to fulfill certain financial or property requirements. In turn, liabilities are divided into long-term (more than 12 months) and short-term debts, which must be fulfilled 12 months or earlier.

What is included in the active part of the balance sheet

The equality of assets and liabilities of the balance sheet is due to the fact that all entries in accounting are reflected using the double entry method. The essence of this method is that when reflecting any fact of economic activity on the balance sheet accounts of an enterprise, an entry is formed in the debit of one account and at the same time in the credit of the corresponding account, but in the same amount.

This is interesting: In 2021, there will be no additional payments for Military Pensioners Over 80 Years Old in Russia

This formula for determining equity is most often used in accounting. There is a second way to find the indicator - through the left, active part of the balance sheet. In this case, the company’s equity capital is defined as the totality of non-current and current assets (lines 1100 and 1200) minus long-term and short-term liabilities (lines 1400 and 1500).

- D 75 “Settlements with founders”, K 91–1 “Other income” (this entry reflects the proceeds received from the sale of the company’s share);

- D 91–2 “Other expenses”, K 81 “Own shares (shares)” (this entry reflects the write-off of the nominal value of the enterprise’s share).

Information

Contribution to the capital of another organization from its founder

By participating in the creation of a legal entity, the founder assumes obligations to pay for the contribution to its management company, in return acquiring the right to part or all (depending on the share of participation) of the property of this legal entity and to receive income from participation in its activities. There is a peculiarity here: when posting, the authorized capital must be reflected both for the founder and for the company receiving the contribution.

On the date of registration of the newly created organization, the founder - a legal entity registered in the Russian Federation, in its accounting shows the debt for the amount of the contribution to the capital specified in the founding agreement, which for it is a financial investment: Dt 58 - Kt 76. Credit balance on the subaccount of account 76, allocated for calculations of contributions to the management company, will show the amount of the management company unpaid by the founder.

The legislation allows payments to the management company both in money and in property or property rights. On the date of making the contribution (the full amount or part thereof), both the founder and the legal entity established by him are repaid the corresponding part of the existing debt.

Postings and examples

Let's consider various situations of economic life using accounts 75, 80 and corresponding ones using conditional examples.

Formation of authorized capital

Let us assume that the capital is 80 thousand rubles. has a division into 4 parts. Two of them are from third-party organization “A”, two are from private individuals Petrov and Ivanov. Postings:

- DT 75/1/"A" CT 80 - 40,000.00 rub. — debt of organization “A” in the Criminal Code.

- DT 75/1/"Petrov" CT 80 - 20,000.00 rub. — Petrov’s debt to the Criminal Code.

- DT 75/1 / “Ivanov” CT 80 - 20,000.00 rub. — Ivanov’s debt to the Criminal Code.

Debt repayment:

- DT 08 CT 75/1/"A" - 33333.33 rubles. — the organization has entered production equipment into the Criminal Code.

- DT 19 CT 75/1/"A" - 6666.67 rubles. — VAT on contributed equipment has been restored.

- DT 51 CT 75/1/"Ivanov" - 20,000.00 rub. — Ivanov repaid the debt on the deposit to the management company by transferring to a r/account.

- DT 50 KT 75/1/"Petrov" - 20,000.00 rub. — Petrov repaid the debt on the deposit to the management company by depositing cash.

On a note! Participants in a business company do not have the right to independently evaluate property and non-monetary contributions to the management company. Such contributions are assessed by an independent evaluator. A non-monetary contribution cannot be reflected in accounting above the amount specified by him (Civil Code of the Russian Federation, Article 66.2-2).

Consequences of debt formation

In the event of a debt that is not repaid within the prescribed period, a meeting of the founders is convened. It must make a decision regarding actions towards the person who committed the violations. So, the council must decide:

- Should the debtor continue to be included in the founders? If not, he is excluded from the list of founders through a special legal procedure. Such a step is unfavorable for the debtor, since this action will lead to the fact that he will not be able to take part in the further activities of the company and receive his share of the income.

- Is it necessary to reduce the authorized capital? The absence of contributions from one or more persons leads to the formation of a deficit in the authorized capital. Accordingly, the founders must decide how to get out of this situation. One way is to reduce the size of this tool. However, it must be taken into account that the minimum capital amount is at least ten thousand rubles.

The authorized capital of an LLC can be reduced at the request of the participants or due to legal requirements.

You should also pay attention to the constituent agreement. It may specify sanctions that apply to debtors

Clarifying this information will help you avoid problems in the future. If a debt has arisen, measures are taken as described in the charter agreement, which provide for the application of individual penalties to the violator.

It should also be remembered that all founders bear subsidiary liability to the creditor in the event of external debt.

In extreme cases, debt can lead to liquidation of the company. Firstly, such a decision can be made at the board of founders. Secondly, the registration authority may initiate legal action to demand the cancellation of the license. However, the latter happens quite rarely, since this type of debt is not considered irreparable debt.

After the liquidation of an LLC, the authorized capital is distributed among its participants upon completion of settlements with creditors

Where is the debt of the founders reflected on the balance sheet?

line 1210 - 50k, Liability line 1520 - 50k, Active line 1230 - 100k, Liability line (let's take it conditionally, because account 90 must be closed) 1370 - 100k. Your balance is 150k. but keep in mind that you will subtract 50k from the 100k service. That is, if you close account 90, then the balance will change. I gave an example that if the 50k service would remain unfinished.

Accounts receivable for which the statute of limitations has expired and other debts that are unrealistic for collection are written off for each obligation based on the inventory data, written justification and order (instruction) of the head of the organization and are charged accordingly to the account of the reserve for doubtful debts or to the financial results of a commercial organization, if during the period preceding the reporting period, the amounts of these debts were not reserved in the prescribed manner.

We fill out the balance sheet using a simplified form

For each balance line, you need to enter the corresponding code in the column. What code to put if a line includes several indicators, each of which has its own code? Clause 5 of Order No. 66n of the Ministry of Finance “On Forms of Accounting Reports of Organizations” states that the code corresponding to the largest share is assigned.

Example of a simplified balance sheet

Small businesses actively use simplified reporting forms when drawing up a balance sheet and financial statements for the past year. It would seem much simpler: the simplified balance sheet has only 5 items in its assets, and 6 items in its liabilities. However, even under these “three pines” there are hummocks. In this article we will talk about them.

This is interesting: What kind of assistance from the state to large families in the Leningrad region

Small businesses actively use simplified reporting forms when drawing up a balance sheet and financial statements for the past year. It would seem much simpler: the simplified balance sheet has only 5 items in its assets, and 6 items in its liabilities. However, even under these “three pines” there are hummocks. In this article we will talk about them.

Accounting for authorized capital and settlements with founders (account 80 and 75)

The first business transaction for any enterprise is the reflection of the authorized capital. Even before you registered the company, you had to decide on its size; after the company is registered, the amount of the authorized capital will appear in the constituent documents of the enterprise. Now all that remains is to correctly reflect this amount in accounting using entries.

Now you have gone through the procedure of registering an LLC, you have in your hands documents confirming the registration of your company. What to do next? In addition to the fact that you will begin to actively engage in entrepreneurial activity, you also need to keep accounting records for the enterprise, and subsequently calculate and pay taxes, fill out and submit reports. Taxes and reporting are still a long way off, first you just need to properly organize accounting at the enterprise

It doesn’t matter who will organize this, you or a hired accountant, the main thing is that the records are kept correctly and without errors

Authorized capital of an LLC: what an accountant should know

The size of the authorized capital is determined exclusively by the founders and is recorded in the constituent documents.

In synthetic accounting, account 80 tells us about the authorized capital. Its balance is reflected in the liability line of the balance sheet of the same name and always corresponds to the amount that is recorded in the constituent documents (and not paid, as some accountants mistakenly believe). The authorized capital in the balance sheet is reflected in line 1310

“Authorized capital (stock capital, authorized capital, contributions of partners)”

.

What role does the authorized capital play in the balance sheet?

- The constituent documentation must indicate the nominal value of the authorized capital in ruble equivalent. When property is listed at a value of more than 200 minimum wages, independent appraisers are invited.

- The balance sheet contains information about the authorized capital in line 410 of passive funds. If an LLC is registered, the tax service requires repayment of capital by at least 50%. In the case of creating a joint stock company, 50% is paid within three months after registration, and the remaining part - during the year of existence.

- When paying capital in cash, entries D 50, 51 and Kt 75 are made. Debts are formed using D 75 Kt 80.

- If fixed assets are made as a contribution, then account 08 is selected. This is due to the fact that the owners contribute both the cost of the property and the costs of its maintenance, registration, input and evaluation.

- When paying with raw materials or materials, a posting of D 10 Kt 75 is drawn up if their cost is taken into account, or D 10 Kt 76 when additional expenses are included. The decision is made based on the company's policy.

- If the founder fails to contribute the balance of funds, it is possible to return the contributed share or distribute the part among other owners or sell it to an outsider. In this case, liquidation will be used.

Reflection in accounting

The debt to the authorized capital in the accounting department is reflected by the entry: D75 (“Settlements with founders”) K80 (“Authorized capital”). The debt is paid under credit 75 of the account. The debit account will depend on the repayment method chosen. These may be the following accounts:

- 50 "Cashier";

- 51 “Current account”;

- 08 “Investments in non-current assets”;

- 10 “Raw materials and supplies”;

- 58 “Financial investments”;

- 97 “Future expenses” (when transferring rights to use property).

In addition to direct methods of paying for a share in capital, in which two parties participate - the founder and the organization, there are ways to involve third parties in this process. This is done on the basis of contributing receivables or payables to the capital of the company.

You don't have to look for the answer to your question in this long article! right now through the form (below), and our lawyer will call you back within 5 minutes with a free consultation.

How is the debt of the founders on deposits in the management company repaid?

The founders' obligations for payments to the management company must be repaid. The law of the Russian Federation does not provide for sanctions against the founder in the event of overdue debts. But it is possible to include such a clause in the constituent documents.

In the meantime, it is important to comply with two standards:

- within 4 months it is required to deposit at least 50% of the total amount of the authorized capital;

- the amount cannot be less than 10 thousand rubles.

You can pay off payment obligations in the management company:

- in cash;

- Central Bank;

- any property;

- rights to claim DZ.

All founders bear subsidiary liability for the company’s debts until the debt on the authorized capital is fully repaid (clause 4 of Article 66.2 of the Civil Code of the Russian Federation).

The following entries are generated in the company’s accounting:

| Debit | Credit | Operation description |

| Dt 50 | Kt 75/1 | Repayment of obligations through the organization's cash desk |

In such cases, the company has the right to set a limit on the amount of funds that are in the cash register. Excess amounts in such cases must be sent to the current account:

| Debit | Credit | Operation description |

| Dt 51 | Kt 75/1 | The debt was repaid by transfer to the current account |

It is also possible to pay off debt by transferring property:

| Debit | Credit | Operation description |

| Dt 08 | Kt 75 | The property is included in the Criminal Code |

| Dt 01 | Kt 08 | Fixed assets put into operation |

| Dt 75 | Kt 80 | Amendments have been made to the Criminal Code |

If a participant pays a debt in materials, then correspondence will occur with the account. 10:

| Debit | Credit | Operation description |

| Dt 10 (41) | Kt 75 | Received materials (goods) from the founder to pay off the debt |

When the management company is created at the expense of the remote control, it is necessary to generate the following transactions:

| Debit | Credit | Operation description |

| Dt 76 | Kt 75 | The organization has been transferred the rights to claim obligations for repayment of the charter capital |

| Dt 51 | Kt 76 | The debtor's obligation has been settled |

In accounting, the Criminal Code refers to the liabilities of the balance sheet and is reflected in the form of a value that is determined by the constituent documentation on line 1310 (even in a situation with partial payment). Current liabilities of participants are an asset, therefore they are reflected on line 1230.

Debt repayment methods

There are several options for contributing funds to the authorized capital. These include:

- money;

- property;

- securities;

- right of claim under the contract.

In accordance with current legislation, the minimum amount of capital must be kept in cash equivalent; the surplus can be represented by any of the above assets. When drawing up the authorized capital, it is necessary to take into account that an assessment of the organization’s material base must be carried out by an independent expert.

Cash payments can be made in two ways:

- Cash (a cash receipt order is drawn up in form No. KO-1).

- Transfer to the company's current account.

It is also often used to repay debt on a deposit in a management company through loan repayments.

This method implies that one of the founders of the company who has incurred a penalty will enter it into the balance sheet in the form of a receivable. For this purpose, a general meeting of co-owners is convened, where the feasibility and size of this investment in capital is determined.

If the total amount of debt exceeds 20 thousand rubles, then by law it is necessary to attract a third-party, independent appraiser to calculate the value of the deposit. The basis for transferring the property rights to the management company may be:

- Assignment agreement.

- Credit agreement.

- Debtor's receipt.

- A writ of execution, if the arrears are already being collected through the court.

In addition to the complete elimination of the penalty, partial payment of the obligation is possible.

The authorized capital can be replenished not only with money, but also with securities

Who owes us

Accounts receivable are the debts of buyers, customers, borrowers, accountable persons, etc., which the organization plans to receive. In addition, accounts receivable also include the amount of advances issued to suppliers and contractors.

The amount of receivables is formed by debit balances on the following accounts:

- 60 “Settlements with suppliers and contractors”, subaccount “Settlements for advances issued”, in relation to the debt of suppliers for the advances transferred to them;

- 62 “Settlements with buyers and customers” in relation to the debt of buyers for goods supplied to them, services rendered, work performed;

- 68 “Calculations for taxes and fees” - for overpayment of taxes, VAT refund;

- 69 “Calculations for social insurance” - for overpayment of taxes and fees to extra-budgetary funds;

- 71 “Settlements with accountable persons” for debts of accountable persons for money issued to them;

- 73 “Settlements with personnel for other operations” - for loans and advances issued to employees or unreimbursed damage from damage to material assets;

- 75 “Settlements with founders” in relation to debt on contributions to the authorized capital or payment for shares;

- 76 “Settlements with other debtors and creditors” - other debt not accounted for in the above accounts.

The basis for the formation of the accounts receivable indicator is the separate reflection of data on long-term and short-term debt. Let us remind you that long-term debt is considered to be debt for which payments are expected more than 12 months after the reporting date. This period begins on the 1st day of the month following the month in which the receivables are reflected in accounting. The total indicator of long-term debt is entered in line 230.

Short-term debt is considered to be debt for which payments are expected within 12 months after the reporting date. Line 240 indicates the total amount of short-term receivables.

Let’s make a reservation right away: “creditor” and other obligations whose duration exceeds 12 months are accounted for separately, in line 520 of the balance sheet liability.

Our short-term debt is accounted for on line 620 of the balance sheet liability and is deciphered in lines 621 - 625 by categories of recipients.

For example, line 621 of the balance sheet is intended for the amount of debt to suppliers and contractors for goods supplied, services rendered, work performed, etc. Please note: advances received from customers are not taken into account in this line.

As of the last day of the month, the organization usually has a debt to its staff. This, of course, is the amount of accrued but not paid wages, compensation for the use of personal property, and overexpenditure on advance reports. All these amounts must be taken into account on line 622.

Be careful when filling out line 624, which shows the organization’s debt to the budget for taxes, fees and penalties. Here it is necessary to reflect, among other things, the amounts of the single social tax, since it is a federal tax.

And finally, on line 625 the amounts of other accounts payable of the organization are recorded. This is where advances received from customers that are not “closed” as of the reporting date will be reflected.

We remind you that, unlike tax accounting, it is no longer possible to make corrections to the accounting records after submitting the reports; all adjustments should be made during the period when the error was discovered. Therefore, in order not to miss the time for a less labor-intensive error correction, you need to act now.

N. Zhemchugova

INTROWEB LLC

Line 1310 “Authorized capital - Berator simplified tax system in practice

The authorized capital is registered in the manner prescribed by law and its debit reflects the debt of the founders (participants) of a business company for contributions to the authorized capital of the enterprise. They opened a company and made a contribution to the authorized capital of 10,000 rubles of the date without the debt of the founders' participants for contributions to the authorized capital. balance sheet in accordance with IFRS, the debt of the founders for contributions to the authorized capital? For some reason, I am tormented by vague doubts, 300 minus the debt of the participants (founders) for contributions to the authorized authorized capital, the company is obliged to reduce its authorized recipe for peach pie Net assets are the real value of the property the company has, annually exclude the value of its own shares purchased from shareholders, and the debt of the founders for contributions to the authorized capital. According to the law, namely the Instructions for using the chart of accounts, the debt of the founders for contributions to the authorized capital

debts: participants (founders) for contributions to the authorized capital ital 123204 Authorized capital [disposable capital. authorized capital. contributions 3 EXCEPT for the debt of participants (founders) for contributions to the authorized capital. 4 Including the amount of deferred tax liabilities. 4 Oct 2021 Where to get data on the debt of the founders and the income of members) on contributions (contributions) to the authorized capital (authorized fund, Almag 01 instructions for use, the price at which is expected within 12 months after the reporting date (without debt of participants (founders) on contributions into the authorized capital).checking the taxation of funds transferred to the authorized capital; the amount of debt of the founders for contributions to the authorized capital; From this article you will learn: how to take into account exchange rate differences in the debt of the founders for contributions to the authorized capital and exchange rate differences Debt of participants (founders) for contributions in the authorized capital reduces the assets taken into account when calculating net assets,

26 Jun 2021 stopurist 427

Share this post

- Related Posts

- Where do you apply for subsidies for housing and communal services in Yaroslavl?

- Sample apartment rental agreement between individuals

- Contract of purchase and sale of land and cottages

- Is it possible to change a medical policy at the MFC?

How is debt converted into authorized capital?

When a legal entity has financial obligations to shareholders or other persons, it can be offset against parts or shares in the organization’s charter capital. This is a good backup option for repaying existing debt, provided that it suits both parties, in particular when the standard method of repayment is not possible for some reason.

The following points must be included in the minutes that record the decision of the founders’ meeting:

- on making a decision to make the capital capital higher by the amount agreed upon by the founders, at the expense of the part contributed by the participant or a third party;

- indicate that the debt to the participant will be repaid or offset thanks to the contribution made.

In the resolution on increasing the capital stock of a joint-stock company through the production of auxiliary shares due to a closed subscription, it is also necessary to include a provision on the possibility of payment through offset. If this is not specified, then offset cannot be carried out.

The process of debt restructuring by converting a claim into the management capital of a legal entity requires the correct preparation of documentation

The legislation contains a lot of comments from various government agencies on this procedure, but there is no specific rule on the need for an expert to evaluate the debt-to-equity swap process.

The main point that “caused confusion” is considered to be the wording of the Civil Code of the Russian Federation in the article on LLCs and JSCs, which states that both property and rights equal to the monetary equivalent can act as a contribution.

The Financial Markets Federal Service expressed its opinion on this issue in the following way: conversion of debt into authorized capital is a separate type of increase in authorized capital in the form of a non-monetary contribution.

It is possible to apply the provisions of the Civil Code on offset to this procedure. It does not consider it necessary to carry out an expert assessment of value.

Experts believe that this assessment is quite reasonable, provided that you are familiar with some compelling facts:

- Completing an assessment procedure will help protect the organization from dishonest influences from persons who may claim that the debt is not commensurate with the counter-obligation received from the legal entity.

- The valuation will help provide protection to the minimum shareholder.

Converting debt into the debtor's authorized capital is a new way to settle obligations between business entities in our country

Thus, Art. was formed. 66.1 of the Civil Code of the Russian Federation on contributions to the property of legal entities. Nowadays, in the form of a contribution to the management company we mean both cash and property, parts of the organization’s shares and bonds, as well as the right to intellectual property or licenses, if they have a monetary value.

In the event of a debt that is not repaid within the prescribed period, a meeting of the founders is convened. It must make a decision regarding actions towards the person who committed the violations. So, the council must decide:

- Should the debtor continue to be included in the founders? If not, he is excluded from the list of founders through a special legal procedure. Such a step is unfavorable for the debtor, since this action will lead to the fact that he will not be able to take part in the further activities of the company and receive his share of the income.

- Is it necessary to reduce the authorized capital? The absence of contributions from one or more persons leads to the formation of a deficit in the authorized capital. Accordingly, the founders must decide how to get out of this situation. One way is to reduce the size of this tool. However, it must be taken into account that the minimum capital amount is at least ten thousand rubles.

The authorized capital of an LLC can be reduced at the request of the participants or due to legal requirements

You should also pay attention to the articles of association. It may specify sanctions that apply to debtors

Clarifying this information will help you avoid problems in the future. If a debt has arisen, measures are taken as described in the charter agreement, which provide for the application of individual penalties to the violator.

In extreme cases, debt can lead to liquidation of the company. Firstly, such a decision can be made at the board of founders. Secondly, the registration authority may initiate legal action to demand the cancellation of the license. However, the latter happens quite rarely, since this type of debt is not considered irreparable debt.

After the liquidation of an LLC, the authorized capital is distributed among its participants upon completion of settlements with creditors