What is accounting policy

Accounting policy refers to a number of methods of accounting and tax accounting used in an enterprise. Each organization has the right to draw up its own accounting policies, which may depend on a variety of parameters. Factors influencing it include:

- federal and local laws and regulations;

- types of taxation of an organization;

- way of conducting business activities, etc.

There are three types of accounting policies enshrined in legislation:

- accounting policies for accounting purposes;

- accounting policies for tax purposes;

- accounting policies for reporting according to international standards.

Change mid-tax period

The letter of the Ministry of Finance of Russia No. 03-03-06/1/45756 dated 07/03/2018 states that Article 313 of the Tax Code of the Russian Federation defines the possibility of making adjustments to the tax accounting policy of an organization only in two cases:

- when legislation on taxes and fees changes;

- when changing the accounting methods used.

Changing accounting methods is allowed only from the beginning of a new tax period, that is, from the beginning of the year. But if the legislation changes, it is allowed to change the accounting policy from the moment the new rules come into force. It depends on the organization on what principle to formulate its tax accounting policy. When new activities appear, changes must be made to it. In the middle of the tax period, the taxpayer has the right to change the accounting policy in two cases:

- the legislation has changed and these changes have entered into legal force;

- The company began to carry out a new type of activity.

What issues does accounting policy address?

The list of issues that are addressed in the accounting policy is very extensive.

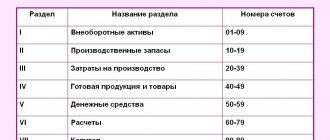

If we are talking about accounting, then here are working charts of accounts, methods of accounting for goods and materials, methods of income distribution, templates for primary documents, etc.

Tax accounting policies are also varied in content. It defines:

- system and structure of taxes paid by the organization;

- objects of taxation;

- ways to recognize expenses and income for calculating income tax;

- methods of calculating depreciation, determining the value of production and material assets;

- procedure for fulfilling tax obligations, etc.

How to change accounting policy

Accounting policy is a system of rules chosen at a time for a long time.

It comes into effect at the beginning of each calendar year.

Changes to it during the reporting period can only be made in extreme cases, for example:

- when this is required to provide the most truthful information about the accounting object;

- when editing the law on accounting policies;

- when the enterprise itself changes its direction of activity.

In order to make the necessary amendments or additions to the accounting policy, the organization must issue a corresponding order.

The role of the order

An order approving an enterprise's accounting policy, being a kind of link between the legislation of the Russian Federation on accounting and tax accounting and the company's regulations, is needed for internal use.

The order obliges all divisions of the company, regardless of their location, to comply with the rules of accounting policies, and also appoints persons responsible for monitoring this.

The order is usually written by the secretary of the organization, and he also gives it to the director for signature.

Inventory accounting

Let's move on to the block within which issues related to accounting for inventory items (TMV) are considered. First, let's look at the accounting of goods.

In relation to purchased goods, an organization has the right to establish the formation of their value in tax accounting both without taking into account additional costs for their acquisition, and taking them into account. The organization decides whether all additional costs are included in the cost of purchased goods or only certain types of them. The list of additional expenses included in the cost of purchasing goods is established in the accounting policy. Typically, the choice in favor of one or another method of forming the value of goods depends on how their value was formed in accounting.

The next point is an indication of the method of evaluating the product during its sale. One of three methods is selected: unit cost, average cost, FIFO method. It is possible to use a single method for all types of goods, or to select an individual method for each group.

In relation to raw materials and materials, the organization indicates the method of their valuation when written off. The same methods that were used to evaluate goods are offered to choose from. Similarly, it is possible to use different assessment methods for different groups of raw materials and supplies.

In relation to low-value property (tangible assets of durable use that do not fall into the category of depreciable property), the organization must indicate how its value is included in current expenses: at a time (by analogy with raw materials) or in equal shares over more than one reporting transition (based on useful life or other economically justified indicator).

How to create an order

Since 2013, the use of unified standard forms of primary personnel and accounting documents has been abolished. Now any orders can be written in any form or, if the organization has its own document template, based on its sample.

In this case, in any case, it is necessary that the order in its structure corresponds to certain parameters of office work, and in its content includes a number of mandatory information. These include:

- Title of the document;

- date of its compilation and number;

- the name of the company where it is produced.

Then comes the main part:

- the essence of the order is described, that is, the fact of approval of the accounting policy is recorded, indicating the exact date from which it is put into effect;

- a link is given to the appendices to the order - documents that, in fact, determine the main provisions of the accounting policy;

- the obligation of department heads to familiarize their subordinates with it is prescribed.

Finally, the order should designate the employees responsible for its implementation. If the administration of the organization believes that the order needs to be supplemented with some other information, it should also be included in the form in separate paragraphs.

Who is required to comply with accounting policies?

The accounting policy must be followed by all organizations registered as legal entities whose responsibility is to maintain accounting records. accounting.

Individual entrepreneurs are exempt from compliance with accounting policies, just like divisions of foreign enterprises - for them there are other regulatory documents.

One important point should be noted: there is no need to confuse accounting (which is determined in accordance with the provisions of the accounting policy) and tax accounting - if there are exceptions for the first, then everyone is required to maintain the second, regardless of the area of work and the taxation system.

How to fill out a form

An order approving a company’s accounting policy can also be drawn up freely: it can be written on an ordinary blank sheet of paper or on the company’s letterhead, both on a computer and in handwritten form.

After the contents of the order have been formulated, it must be signed by the director or his deputy/representative, who has the power of attorney to sign documents (in this case, the use of facsimile, i.e. printed by any method, autographs is unacceptable, i.e. the signature must be “live”).

In addition, the employees responsible for its implementation should be familiarized with the order against signature.

Today, it is only necessary to certify an order using stamps (stamps and seals) in one case - if this rule is enshrined in the local regulatory documents of the organization. The order is always written in one copy, but if necessary, you can make additional, properly certified copies. The completed order must be registered in the administrative documentation journal.

Order on accounting policies for tax purposes (sample form)

____________________________________________________

(name of company)

ORDER N ___

on accounting policies for tax purposes

for ____ year

g. ________________ "__"__________ ____ g.

Based on the Tax Code of the Russian Federation and other legislative and regulatory acts, I order:

1. Apply the _________ taxation system with the object ______________.

2. Maintain tax accounting registers electronically (on paper).

3. Tax accounting is maintained separately from accounting.

4. Tax accounting is carried out within the framework of accounting.

5. Tax accounting is maintained in a separate tax chart of accounts.

6. Responsibilities for maintaining tax records are assigned to ______________.

7. Responsibilities for interaction with tax authorities are assigned to _____________.

8. List of registers that must be formed on paper without fail: _______________________.

9. List of events serving as the basis for making changes to the accounting policy:

— changes in legislation on taxes and fees (corresponding changes can be adopted during the year);

— a significant change in the operating conditions of the publishing house (corresponding changes in accounting policies will be adopted starting from the next reporting year);

— the beginning of new types of activities by the publishing house (from the moment the new types of activities begin);

— __________________________________________________________________.

10. Entrust control over compliance with the accounting policies to the chief accountant _________________.

11. Approve the statement of accounting policies.

12. Approve a methodology for maintaining separate accounting, the provisions of which should not contradict regulatory and legislative acts.

13. For value added tax:

— exemption from the duties of the taxpayer (not) to receive.

— for the following transactions that are not subject to taxation (exempt from taxation), tax benefits (not) apply: ____________________;

— ensure separate accounting of tax amounts for purchased goods (works, services), property rights that are used in the production of taxable and non-taxable products;

— approve ______________ (position, full name) responsible for maintaining tax registers for VAT (purchase book, sales book, log of invoices received, invoices issued);

— approve the list of officials who have the right to sign on issued invoices:

— __________________ (position, full name);

— __________________ (position, full name);

- apply a deduction for periods when the costs of producing non-taxable goods (work, services) did not exceed 5% of total expenses: the entire amount of tax is subject to deduction (or the tax is distributed between costs and settlements with the budget).

14. For income tax, approve:

— the procedure for paying advance payments: based on the amount of the advance for the previous reporting period (or based on the actual profit received since the beginning of the year);

— indicator used for the purpose of calculating and paying income tax (for organizations with separate divisions): ____________________;

— distribution of profits for each separate division (not) to be carried out.

15. For depreciable property, establish:

— the maximum limit for classifying fixed assets as inventories (no more than 20,000 rubles);

— depreciation method: (non)linear;

— application of reduced depreciation rates for ____________ with coefficients _________________;

— the procedure for determining the depreciation rate for used objects: taking into account the service life of the previous owners (another algorithm);

— application of depreciation bonus: __________ (in the amount of no more than 10 percent).

16. For inventories, establish:

— method of assessment when writing off raw materials: _______________________;

— the procedure for forming the cost of goods: ___________________________________;

— method of evaluating purchased goods during their sale: ____________________.

17. For loans and credits, establish:

— method of accepting interest for accounting: ___________________________________;

— procedure for determining the comparability of debt obligations: ___________.

18. For financial investments, establish:

— method of writing off the value of retired securities: ______________________;

— method of estimating the value of the estimated share price: _________________________.

19. To classify income, establish:

— procedure for recognizing income and expenses: ________________________________;

— the procedure for recognizing income (for income relating to several reporting (tax) periods, and in the event that the relationship between income and expenses cannot be clearly defined): ___________________________;

— the procedure for recognizing income from the sale of work (services) for production with a long (more than one tax period) technological cycle, if the terms of the concluded contracts do not provide for the phased delivery of work (services): ________________________________________________.

20. To classify expenses, set:

— list of direct expenses: _____________________________________________________;

— the procedure for distributing direct expenses for work in progress and for products manufactured in the current month (work performed, services rendered), taking into account the correspondence of the expenses incurred for manufactured products (work performed, services rendered): ____________________________;

— a mechanism for distributing direct costs to a specific production process (using economically feasible indicators): ___________;

— the procedure for distributing costs that can equally reasonably be attributed simultaneously to several groups of costs: ______________________;

— procedure for recognizing direct expenses (for taxpayers providing services): _______________________________________;

— mechanism for determining the share of expenses for the development of natural resources for each subsoil plot: _________________________________________;

— expenses for the maintenance of rotational and temporary camps in organizations operating on a rotational basis or working in field (expeditionary) conditions (if the standards are not approved): ________________;

— the procedure for recognizing expenses for the acquisition of rights to land plots: ___________________________.

21. For reserves, set:

— types of reserves created: _________________________________________________;

— reservation procedure: ______________________________________________.

22. For excise taxes, establish the following procedure for organizing separate accounting in relation to excisable goods for which different tax rates are established: ________________________.

23. For the mineral extraction tax, establish the following method for determining the amount of extracted minerals: ____________________.

Applications:

1. Accounting policy.

2. Methodology for maintaining separate accounting.

Supervisor: ____________________ ________________/________________