At its core, leasing is a type of rental. Therefore, activities in this area are regulated by general rules of civil law, both in relation to leasing, and there are also special provisions relating specifically to leasing. In addition, leasing activities are regulated by Federal Law No. 164-FZ of October 29, 1998 “On financial lease (leasing)”.

Although the laws stipulate general rules for conducting activities in the field of financial leasing, the parties to such relations can independently establish different conditions of leasing agreements. Depending on these conditions, accounting for leasing transactions may vary significantly.

Perhaps the most important thing, which most affects both tax and accounting, is the condition on the balance sheet of which of the parties - the lessor or the lessee - the property will be taken into account.

Leasing agreement

Under a financial lease agreement, the lessor is obliged to purchase the property specified by the lessee and provide this property for use by the lessee. In this case, the latter independently determines from which specific seller this property should be purchased.

This is interesting

The total amount of the leasing agreement may include the redemption price of the leased asset. This is possible if the contract provides for the transfer of ownership of the property to the lessee.

In other words, the main difference between leasing and rental agreements is that the lessor purposefully buys property known in advance to lease it from a seller agreed upon by the parties. When renting, your own property is transferred, which is not specifically purchased for a specific tenant.

The subject of leasing agreements can be any non-consumable things, for example, buildings, structures, vehicles, equipment and other movable or immovable property. The exception is land plots and other natural objects, as well as property, the free circulation of which is prohibited by law.

It is worth noting that the ownership of the leased asset remains with the lessor throughout the duration of the contract. The lessee has the right only to temporary possession or use.

But at the same time, leased property can be taken into account on the balance sheet of either party. Consequently, depreciation will be calculated by the person who is the balance sheet holder. This condition is agreed upon by the parties when signing the contract.

The participants set the validity period of financial lease agreements independently and record it in the document. It is impossible to conclude such an agreement, unlike a lease, for an indefinite period, since leasing payments are tied to the duration of the agreement. It can only be extended, and the previous conditions may be changed or retained. The leasing agreement also stipulates the terms on the amount, method and frequency of payment of leasing payments.

Leasing payments mean the total amount of payments under the leasing agreement for the entire period of its validity, which includes:

- reimbursement of the lessor's costs for the purchase and transfer of the leased asset to the lessee;

- reimbursement of costs for services provided for in the leasing agreement;

- lessor's income.

Payments under leasing agreements can be established:

- in a fixed amount of payments made periodically or at a time;

- in the share of products, fruits or income received as a result of the use of leased property;

- in the provision by the lessee of certain services;

- in the transfer by the lessee to the lessor of a thing stipulated by the contract for ownership or temporary possession (use);

- in imposing on the lessee the costs of improving the leased asset.

Also, the parties may provide in the leasing agreement a combination of these forms or other forms of leasing payment. In addition, the parties can agree to change the amount of leasing payments. But you can change it no more than once every three months.

Shock absorption groups

In the work of each enterprise or organization, fixed assets are used, which are part of the organization’s property, used as a means of producing goods, services, work or any management needs of the enterprise for a long time. When an organization takes a fixed asset into account, its initial cost is determined based on the actual, objective costs of acquisition, manufacturing, construction, transportation, etc. excluding VAT.

To account for fixed assets during operation, their residual value is determined, which is the difference between the original cost and depreciation during operation.

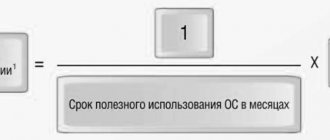

As you know, all property owned by an enterprise depreciates and wears out over time. Depreciation of fixed assets is considered to be the transfer of part of the cost of fixed assets to the cost of products, works or services. Depreciation is calculated over the entire useful life of the object, i.e. the period of time during which the application and use of an item of fixed assets can bring economic benefits to the organization. Each enterprise can determine the useful life independently or use the classification of fixed assets developed on the basis of OKOF - the All-Russian Classifier of Fixed Assets.

Further, depending on this indicator - SPI - the fixed asset can be assigned to one of the depreciation groups. The Tax Code defines only ten depreciation groups, and the classification of fixed assets included in a particular depreciation group is, in turn, approved by the Government of the Russian Federation.

Such a concept as “depreciation group” is used both for tax accounting purposes for calculating income tax, and for accounting purposes. The definition of depreciation of fixed assets for tax and accounting purposes differs.

Each depreciation group establishes a clear interval expressed by its useful life. It must be remembered that the lower limit of the interval of each depreciation group begins with the word “over”, that is, the lower limit is not included in the interval, and the upper limit ends with the word “inclusive”, that is, this figure is included in the interval of the depreciation group. For example, the third depreciation group is determined by a period of over 3 years and up to 5 years inclusive. That is, a fixed asset for which the SPI is established as 3 years is included in the second group, and with a SPI of 3 years 1 month in the third, at the same time, a fixed asset with an established SPI of 5 years will still belong to the 3rd depreciation group. For taxpayers who have a good profit, it is most beneficial to establish SPI as early as possible, which will make it possible to write off the cost of the object as expenses earlier. For example, for the same third depreciation group, it is most profitable to set the period to 3 years 1 month. The concept of “depreciation group” is formulated in paragraph 1 of Article 258 of the Tax Code of the Russian Federation and is used mainly for tax accounting purposes. The term “depreciation group” is not mentioned in accounting regulations. But in paragraph 1 of the Russian Federation Regulations dated January 1, 2002 No. 1, this classification of depreciable property, used for tax purposes, can also be used for accounting. The 2002 resolution also approved the Classification of fixed assets and defined depreciation groups. In the document, all types of fixed assets according to their useful lives are strictly distributed into their depreciation groups. The Classification indicates the OKOF code, as well as the name and necessary notes.

Depreciation groups include fixed assets, in turn grouped into subgroups: Household and industrial inventory, Machinery and equipment, Perennial plantings, Transport vehicles, Buildings, Working livestock, Dwellings, Transmission devices and structures.

If it is necessary to determine the useful life of intangible assets, then it is determined taking into account the validity period of the license or patent for the right to use the object. If it is impossible to determine the SPI in this way, the depreciation rate is established for a period of 10 years.

It happens that not a single depreciation group can include a fixed asset. In such a situation, the useful life is determined on the basis of these technical conditions or data sheets or taking into account the manufacturer’s recommendations.

In the event that the available property is leased, i.e. financial lease agreement, then it is included in depreciation groups by the party whose property is required to be accounted for under the agreement.

In a situation where it is necessary to use an increasing or decreasing factor for fixed assets, the useful life is proportionally reduced or increased accordingly. We should not forget that the property must be in the same depreciation group to which it would belong without taking into account the coefficients.

When an organization increases its useful life as a result of modernization, reconstruction or, say, technical re-equipment, it should also be taken into account that the useful life can only fluctuate within the limits established by the current depreciation group.

For groups 1-3 (most vehicles), the accelerated depreciation rate in leasing is not applied.

first group

- all short-lived property with a useful life from 1 year to 2 years inclusive;

second group

— property with a useful life of more than 2 years up to 3 years inclusive;

third group

— property with a useful life of more than 3 years up to 5 years inclusive;

fourth group

— property with a useful life of over 5 years up to 7 years inclusive;

fifth group

— property with a useful life of over 7 years up to 10 years inclusive;

sixth group

— property with a useful life of over 10 years up to 15 years inclusive;

seventh group

— property with a useful life of over 15 years up to 20 years inclusive;

eighth group

— property with a useful life of over 20 years up to 25 years inclusive;

ninth group

— property with a useful life of over 25 years up to 30 years inclusive;

tenth group

— property with a useful life of over 30 years;

Transfer of property to the balance of the lessee

As noted above, the lessor will have ownership of the property. But the lessee can take it into account on his balance sheet.

Dangerous moment

The lessor may write off lease payments from the current account without dispute if the lessee fails to pay them more than twice in a row.

The transfer of the leased asset is reflected in accounting on the basis of supporting documents - a transfer and acceptance certificate or another document that reflects the fact of transfer.

There is no document form specifically established for these operations. Although many use unified forms of the act of acceptance and transfer. Form No. OS-1 is used when transferring fixed assets, form No. OS-1a when transferring buildings and structures, and form No. OS-1b when transferring a group of fixed assets (all these forms are approved by Resolution of the State Statistics Committee of Russia dated January 21, 2003 No. 7) .

At the same time, participants in leasing relations can independently develop the form of the transfer document. The main thing is that it contains all the required details:

- Title of the document;

- date of document preparation;

- name of the organization on behalf of which the document was drawn up;

- content of a business transaction;

- natural and monetary expression of a business transaction;

- persons responsible for the transfer of property, indicating their positions;

- personal signatures of these persons.

The lessee can account for the property using the inventory number assigned by the lessor. To do this, you need a copy or extract from the lessor's inventory card for the fixed asset. In this case, it would be better if the lessee’s accountant opens new inventory cards for these objects based on the copies provided. The form of the inventory card is also unified - form No. OS-6.

Accounting with the lessee

Property on the lessor's balance sheet

This is perhaps the simplest and most common option. With it, the lessee, as in a regular lease, reflects the property on off-balance sheet account 001 “Leased fixed assets.”

The leased asset is reflected at the cost specified in the agreement. In this case, the accountant will reflect transactions for receiving property as follows:

DEBIT 001

– property was received on lease;

CREDIT 001

– the leased property is returned at the end of the lease agreement.

Analytical accounting for account 001 is carried out separately both for lessors and for each leasing object.

In this option, depreciation will be charged by the lessor, since the property is reflected on its balance sheet.

In addition, the leased object will also not be reflected in the recipient’s tax accounting. This again relates to the balance holder of the property. Example 1

Orbita LLC leased commercial equipment in March 2010.

In the leasing agreement, the cost of the leased asset is estimated at 1,700,000 rubles. The property is recorded on the lessor's balance sheet. The leasing agreement ended in March 2012. In the accounting records of Orbita LLC it is necessary to reflect: In March 2010: DEBIT 001

– 1,700,000 rubles.

– production equipment was leased. In March 2012: LOAN 001

– RUB 1,700,000. – commercial equipment is returned at the end of the lease agreement.

Property on the balance sheet of the lessee

With this option, the lessee accepts the property as a fixed asset. The initial cost is formed on account 08 “Investments in non-current assets”, on the sub-account “Property received on lease” in correspondence with account 76 “Settlements with various debtors and creditors” on the sub-account “Lease obligations”.

It is important

The transfer of leased property to the balance of the lessee is not subject to VAT. Since the lessor remains the owner, regardless of whose balance sheet the property is listed on, no sale operation occurs. This means that the value of the property in the lessee’s accounting is reflected without VAT.

The initial cost consists of the cost according to the leasing agreement plus the costs of bringing the property to a condition suitable for use.

The following entries must be reflected in the lessee's accounting:

DEBIT 08, subaccount “Property received on lease” CREDIT 76, subaccount “Rental obligations”

– reflects the cost of the leased property under the contract;

DEBIT 08 CREDIT 60 (76, 70, 69 and others)

– reflects the costs associated with obtaining leased property.

After accounting for the initial cost, the property is included in fixed assets. To do this, you should open a subaccount “Property received on lease” to account 01 “Fixed Assets”. Example 2

Let's use the conditions of example 1 and change them a little.

The property is recorded on the lessee's balance sheet. In addition, transportation of commercial equipment is carried out by Orbita LLC at its own expense. Transport costs amounted to 59,000 rubles, including VAT – 9,000 rubles. Transportation costs were paid in March 2010. The accountant needs to make the following entries (see table 1): Table 1

| Explanation of operation | Debit | Credit | Amount, rub. |

| The cost of leased equipment is reflected | 08-9 | 76-5 | 1 700 000 |

| Equipment delivery costs reflected | 08-9 | 60 | 50 000 |

| The amount of “input” VAT on the cost of delivery services is taken into account | 19 | 60 | 9000 |

| Leased equipment was put into operation | 01-9 | 08-9 | 1 750 000 |

| Accepted for deduction of VAT on the cost of transport services | 68-1 | 19 | 9000 |

| Transport services paid | 60 | 51 | 59 000 |

Since depreciation on the leased property is calculated by the balance sheet holder, then with this option the lessee will be able to depreciate it in accounting.

Depreciation can be calculated from the month following the month in which the object was accepted for accounting in account 01 “Fixed Assets”. For accounting purposes, the useful life can be taken as the duration of the leasing agreement.

This is interesting

If the validity period of the leasing agreement coincides with the useful life of the object in accounting, this will lead to a discrepancy with tax accounting. Therefore, it is more expedient to use in accounting the useful life that is established for tax accounting.

The lessee must reflect the accrued depreciation in accounting in the general manner, using production cost accounts, depending on the purposes of using the leased property in correspondence with account 02 “Depreciation of fixed assets”, under the subaccount “Depreciation of leased property”. In this case, the wiring is done:

DEBIT 20 (23, 25, 26, 44, 91) CREDIT 02-9

– depreciation has been calculated on the leased property.

It is worth noting that the amount of accrued depreciation is directly related to the accrual of lease payments. For accounting purposes, the lease payment is an expense, and it is recommended to reflect it by posting:

DEBIT 76, subaccount “Lease obligations” CREDIT 76, subaccount “Arrears on leasing payments”

– lease payment accrued for the reporting period.

However, in this case there will be no reflection of the expense for accounting purposes. In this regard, it is better to reflect the lease payment as an expense in the general manner, depending on the purpose of using the property:

DEBIT 20 (23, 25, 26, 44, 91) CREDIT 76 (6 0)

– lease payment accrued for the reporting period.

Moreover, if the lessee includes both the lease payment and depreciation in expenses, this will lead to double counting of expenses. So depreciation must be reflected by posting:

DEBIT 76, subaccount “Rental obligations” CREDIT 02, subaccount “Depreciation of leased property”

– depreciation was accrued for the reporting period.

Example 3

Let's use the conditions of example 2. Let's expand them.

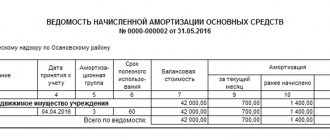

Let the useful life of commercial equipment be five years. Since the equipment was registered as a fixed asset in March 2010, depreciation must be calculated from April. The annual depreciation rate will be: 1: 5 years X 100% = 20%. The annual depreciation amount will be: RUB 1,750,000. X 20% = 350,000 rub. Therefore, the amount of depreciation for April will be 29,167 rubles. (RUB 350,000: 12 months). The following entries must be made in accounting (see Table 2): Table 2

| Explanation of operation | Debit | Credit | Amount, rub. |

| The cost of leased equipment is reflected | 08-9 | 76-5 | 1 700 000 |

| Equipment delivery costs reflected | 08-9 | 60 | 50 000 |

| The amount of “input” VAT on the cost of delivery services is taken into account | 19 | 60 | 9000 |

| Leased equipment was put into operation | 01-9 | 08-9 | 1 750 000 |

| Accepted for deduction of VAT on the cost of transport services | 68-1 | 19 | 9000 |

| Transport services paid | 60 | 51 | 59 000 |

| Depreciation accrued for April on leased property | 76-5 | 02-9 | 29 167 |

Items are on the balance sheet of the leasing recipient

The leasing recipient can account for leased assets on the balance sheet as fixed assets. The initial cost is created on the basis of total acquisition costs excluding VAT. The basis is clause 8 of PBU 6/01. In accounting, the useful life is the duration of the leasing agreement (clause 20 of the PBU).

Depreciation within the framework of tax accounting is carried out on the basis of Article 259 of the Tax Code of the Russian Federation. When determining income tax, depreciation and payments under the contract are considered the costs of the lease recipient. In this case, the accounted depreciation must be excluded from the amount (subclause 10 of clause 1 of Article 264 of the Tax Code of the Russian Federation). The useful life is calculated based on the rules of the Tax Code of the Russian Federation.

Let's look at the transactions that are needed when accepting leased objects onto the balance sheet of the leasing recipient:

- DT08 KT76. Creation of the initial cost of the leasing object based on accounting rules.

- DT01 KT08. The object is included in fixed assets.

- DT20, 25-26, 44, 91 KT02. Definition of depreciation.

- DT02 KT01. Write-off of an object for which depreciation has been accrued in full.

The asset is written off when the lease agreement has expired.

Accounting with the lessor

Under a leasing agreement, the lessor purchases property specifically for the lessee. To do this, he enters into a purchase and sale agreement with the equipment supplier. A purchase and sale agreement is required to complete a property leasing transaction.

The acquisition of property must be reflected in accounting.

In accounting, the initial cost is formed on account 08 “Investments in non-current assets”. Then the object is accepted for accounting in account 03 “Profitable investments in material assets”.

In this case, the lessor has the right to deduct VAT amounts from the cost of the acquired property.

After reflecting transactions for the acquisition of property and its acceptance for registration, transfer to the lessee is carried out.

Property on the lessor's balance sheet

The property should be reflected in account 03 “Income-generating investments in material assets” in the sub-account “Property leased”. At the same time, a second sub-account “Property intended for leasing” is also opened to this account.

The lease transfer is reflected by the following posting:

DEBIT 03, subaccount “Property leased” CREDIT 03, subaccount “Property intended for lease”

– the lessee’s property is leased.

Depreciation in this case is calculated according to the general rules.

The lessor will be able to calculate depreciation in accounting from the month following the one in which the object was accepted for accounting in account 03 “Profitable investments in tangible assets.”

The amounts of accrued depreciation on property leased will be reflected in accounting in the general manner, as for own property - on account 02 “Depreciation of fixed assets”. However, depreciation on leased property must be taken into account separately. To do this, you can open an additional subaccount “Depreciation on property leased.”

The depreciation entry will look like this:

DEBIT 20 CREDIT 02, subaccount “Depreciation on property leased”

– depreciation has been calculated on the property leased.

Example 4,000

Lada entered into a leasing agreement with Orbita LLC in March, according to which it purchased retail equipment.

The cost of the equipment was 1,770,000 rubles. (including VAT - 270,000 rubles). The property is accounted for on the lessor's balance sheet. Lada LLC paid the seller for commercial equipment in March. In the same month, the property was transferred to the lessee. The useful life is five years. The annual depreciation rate will be: 1: 5 years XX 100% = 20%. The annual depreciation amount will be: RUB 300,000. (RUB 1,500,000 X 20%). The depreciation amount for April will be: RUB 25,000. (300,000 rubles: 12 months). The accountant of Lada LLC will make the following entries (see table 3): Table 3

| Explanation of operation | Debit | Credit | Amount, rub. |

| The costs of purchasing equipment are reflected | 08 | 60 | 1 500 000 |

| VAT on purchased equipment has been taken into account | 19 | 60 | 270 000 |

| Payment for equipment has been made | 60 | 51 | 1 770 000 |

| Equipment for leasing accepted for accounting | 03-1 | 08 | 1 500 000 |

| Accepted for deduction of VAT on the cost of equipment | 68-1 | 19 | 270 000 |

| Equipment leased | 03-2 | 03-1 | 1 500 000 |

| Depreciation accrued for April on leased property | 20 | 02-1 | 25 000 |

Property on the balance sheet of the lessee

The question of how the lessor should account for property if it is on the lessee’s balance sheet is not resolved by law.

It is worth noting that it would be incorrect to use financial performance accounts (accounts 90 and 91) for accounting, since there is no transfer of ownership of the property. So you can’t simply write off the cost of the property as an expense.

The operation of transferring property under lease can be reflected on the lessee’s balance sheet in account 76 “Settlements with various debtors and creditors” (increase accounts receivable). That is, when transferring, you need to make the following wiring:

DEBIT 76 CREDIT 03

– the leased property is transferred to the balance of the lessee. The leased asset in this case is reflected at its original cost (the cost at which the object is listed on the lessor's balance sheet).

At the same time, the lessor reflects the transferred property on off-balance sheet account 011 “Fixed assets leased out.” The value of the property in this case is indicated according to the leasing agreement.

Posting for this operation:

DEBIT 011

– the value of the leased property transferred to the balance sheet of the lessee is reflected on the off-balance sheet account. Due to leasing payments, the value of the property will be written off as follows:

DEBIT 20 CREDIT 76

– expenses are reflected in relation to the cost of the property included in the lease payment for the current period.

Depreciation on leased property that is transferred does not need to be calculated. In tax accounting, depreciation will also not be charged.

The costs of acquiring leased property will be included in other costs associated with production and sales.

At the same time, such expenses must be taken into account in those reporting periods in which leasing payments are provided. In this case, these expenses are taken into account in an amount proportional to the amount of leasing payments (similar to accounting). Example 5

LLC Lada entered into a leasing agreement with LLC Orbita in March for three years (36 months), according to which it purchased commercial equipment.

The cost of the equipment was 1,180,000 rubles. (including VAT - 180,000 rubles). The property is recorded on the lessee's balance sheet. Payment for the equipment was made in March. In the same month, the property was transferred to the balance of the lessee. The total amount of lease payments for the entire leasing period is 1,699,200 rubles. (including VAT - 259,200 rubles). The cost of the property is equal to the total amount of lease payments and amounts to RUB 1,699,200. The lessee pays monthly lease payments of 47,200 rubles. (including VAT - 7,200 rubles). Lada LLC calculates income tax on a monthly basis. To determine the amount of costs associated with the purchase of equipment, which can be included in income tax expenses for March, you need to calculate the proportion: 40,000 rubles . : (RUB 1,699,200 – RUB 259,200) X 100% = = 2.7778%. Therefore, for March you can include in other expenses an amount of 27,778 rubles. (RUB 1,000,000 X 2.7778%). Lada LLC will reflect the following entries in its accounting (see Table 4). Table 4

| Explanation of operation | Debit | Credit | Amount, rub. |

| The costs of purchasing equipment are reflected | 08 | 60 | 1 000 000 |

| VAT on purchased equipment has been taken into account | 19 | 60 | 180 000 |

| Payment for equipment has been made | 60 | 51 | 1 180 000 |

| Equipment for leasing accepted for accounting | 03-1 | 08 | 1 000 000 |

| Accepted for deduction of VAT on the cost of equipment | 68-1 | 19 | 180 000 |

| The equipment was transferred to the balance of the lessee | 76 | 03 | 1 000 000 |

| The off-balance sheet account reflects the cost of leased equipment | 011 | 1 699 200 | |

| Lease payment accrued for March | 62 | 90-1 | 47 200 |

| VAT charged on lease payment | 90-3 | 68-1 | 7200 |

| Received leasing payment from the lessee for March | 51 | 62 | 47 200 |

| Expenses are reflected in terms of the cost of equipment included in the lease payment for March (RUB 1,000,000: 36 months) | 20 | 76 | 27 778 |

Depreciation in leasing - legal aspects

Civil relations of leasing transactions are regulated by Law No. 164-FZ of October 29, 1998; § 6 section 4 of the Civil Code (Articles 665-670). The accounting features of such business transactions are regulated by PBU 6/01 and Instructions by Order No. 15 dated February 17, 1997. For tax accounting purposes, leased goods are written off in accordance with the norms of the chapters. 25 NK – Art. 259.3, 264, 272 and others. Various objects can be transferred for financial lease, with the exception of lands and other natural resources (clause 1 No. 164-FZ).

Depreciation on leased property is calculated by the party that, according to contractual terms, accepts the object on its balance sheet (clause 10 of Article 258). In order to calculate depreciation amounts, the taxpayer independently determines the useful life (useful life) in accordance with the Classification of fixed assets. It is required to start writing off depreciation from the month following the period when the leasing object was put into operation.

Property tax

The party to the leasing agreement that has the property on its balance sheet will be charged and paid corporate property tax.

So, if the property is accounted for on the lessor’s balance sheet, then he reflects it in account 03 “Income-generating investments in tangible assets.” The lessee records the leased asset on the balance sheet in account 001 “Leased fixed assets”. In this case, property tax on leased items is paid by the lessor.

If the leased property is taken into account on the balance sheet of the lessee, then it is reflected in account 01 “Fixed Assets”. The lessor records the transferred property on the balance sheet in account 011 “Fixed assets leased out.” Therefore, the lessee pays the property tax.

At the end of the lease agreement, the tax must be paid by the person who becomes the owner of the leased asset. For example, if the purchase of property is provided, then the lessee will pay property tax.

Features of calculating depreciation of property during leasing

Lease items

Many accountants are interested in the question of the specifics of calculating depreciation of property during leasing, and the relationship between the lessor and the lessee. Studying the Tax Code and existing federal laws will help resolve emerging problems.

Accounting at enterprises

Property received/transferred for financial lease under a leasing agreement can be recorded on the balance sheet of both the lessee and the lessor. It is included in the corresponding depreciation group by the party whose property must be accounted for in accordance with the terms of the financial lease agreement (leasing agreement) (clause 7 of Article 258 of the Tax Code of the Russian Federation).

By accepting leased property for accounting, the lessee sets the useful life of the property received under the lease agreement on its balance sheet independently. The lessee can set the useful life of the leased asset based on the term of the contract (clause 20 of PBU 6/01). This makes sense if the property is returned after its completion. In this case, by the time of return, the cost of the property (in the amount of lease payments) will be completely written off as expenses through depreciation. In addition, the useful life of the property is set equal to the leasing term, if it is not returned to the lessor (becomes the property of the lessee) and the expected period of use of this fixed asset is equal to the leasing term.

In other situations, when the agreement provides for the subsequent transfer of ownership of the leased asset to the lessee, the latter sets the useful life, as in the case of its own fixed assets, based on the expected productivity, capacity and physical wear and tear of the object. For this purpose, the Classification of fixed assets included in depreciation groups, which was approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1, can be used.

The lessee will include depreciation charges on the leased fixed asset as expenses in accounting.

This is provided for by Federal Law No. 164-FZ and clause 9 of the Instructions on the reflection in accounting of transactions under a leasing agreement, approved by Order of the Ministry of Finance of Russia dated February 17, 1997 No. 15, while the legislator provides the possibility of using an accelerated depreciation mechanism (clause 1, 2, Article 31 of Federal Law No. 164-FZ). Depreciation is accrued in the general manner (in accordance with the provisions of PBU 6/01). A special coefficient may be applied to the basic depreciation rate for property that is the subject of a leasing agreement. In this case, the value of this coefficient cannot exceed 3 (clause 7 of Article 259 of the Tax Code of the Russian Federation). Choosing a method for accounting

In order to completely exclude claims from the tax authorities, you should remember the following: in accordance with Art. 31 of the Federal Law of October 29, 1998 No. 164-FZ “On financial lease (leasing)” the parties to the agreement have the right to apply accelerated depreciation of the leased asset by mutual agreement. And, despite the fact that the norms of the Tax Code of the Russian Federation do not directly require this, it is better to include such a condition in the agreement with the lessor.

In accounting, the use of an increasing factor is possible only if depreciation is calculated using the reducing balance method. The reducing balance method for determining the useful life is established in the case when the efficiency of using an item of fixed assets decreases with each subsequent year.

If an enterprise decides to use the reducing balance method in accounting, and in tax accounting uses the linear method, also with an acceleration factor of 3, this will give a significant reduction in tax payments, but will lead to discrepancies in accounting.

For passenger cars and passenger minibuses with an initial cost of more than 300 thousand rubles and 400 thousand rubles, respectively, the basic depreciation rate in tax accounting is applied with a special coefficient of 0.5. Organizations that have received or transferred the specified cars and passenger minibuses on lease include this property in the corresponding depreciation group and apply the basic depreciation rate (taking into account the coefficient used by the taxpayer for such property) with a special coefficient of 0.5.

In addition, it should be taken into account that, according to tax authorities, the acceleration factor can be applied until the leasing agreement expires (Clause 7, Article 259 of the Tax Code of the Russian Federation). The specified coefficient must be established on the date of putting the leased asset into operation, while it remains unchanged during the depreciation period (letter of the Ministry of Finance of Russia dated October 6, 2006 No. 03-03-04/1/682). In the future, depreciation should be calculated at the normal rate.

Since the use of accelerated depreciation is the right and not the obligation of the taxpayer, the decision to apply a special depreciation rate in relation to the leased asset must be enshrined in the accounting policy of the organization (letter of the Department of the Ministry of Taxes of Russia for Moscow dated April 13, 2004 No. 26-12/25162 ). Otherwise, it cannot be considered that the organization has made a decision to apply a special depreciation rate.

The amount of depreciation of the leased asset is recognized as an expense for ordinary activities (clauses 5, 8 of PBU 10/99 “Expenses of the organization”).

attention

Debit-credit

If the leased asset is taken into account on the balance sheet of the lessee, then he charges depreciation on this property (Clause 2, Article 31 of the Federal Law of October 29, 1998 No. 164-FZ “On financial lease (leasing)”). On a monthly basis, the amounts of accrued depreciation are reflected by a debit entry in the production cost accounts in correspondence with account 02 subaccount “Depreciation of fixed assets received on lease.”

Options are possible

According to tax authorities, in the case when the property at the end of the contract becomes the property of the lessee, payments should be divided into two components: the amount attributable to the redemption value of the leased asset, and the remaining funds. Only the second part of the specified payment can be included in expenses at a time. And the redemption price will form the future initial cost of the fixed asset and will be written off as expenses as it is depreciated (letter of the Ministry of Finance of Russia dated May 24, 2005 No. 03-03-01-04/1/288). In addition, it is possible that the lease agreement does not specify the redemption price, but simply states that the leased asset becomes the property of the lessee after payment of all lease payments. In this case, the specified amount should be considered as an expense included in the initial cost of the property after the transfer of ownership of it to the lessee (letter of the Ministry of Finance of Russia dated April 8, 2005 No. 03-03-01-04/1/174).

At the same time, in paragraphs. 10 p. 1 art. 264 of the Tax Code of the Russian Federation clearly states that leasing payments are included in other expenses. In order not to conflict with tax authorities, it is enough to establish a symbolic redemption amount in the leasing agreement.

In the event that the property is listed on the lessor's balance sheet, the lessee will begin to charge depreciation on this leased asset no earlier than the ownership of it is transferred to it.

Material provided by the magazine "Raschet"

Transport tax

The payer of transport tax is the person in whose name the vehicle is registered.

If the car is registered to the lessor, then he will be the payer during the term of the agreement. And if the repurchase of the property is not provided, then at the end of the contract.

If you decide to register the vehicle in the name of the lessee, then the following options are possible:

1)

temporary registration of the car to the lessee. In this case, upon purchase, the vehicle is first registered in the name of the lessor, and then registered in the name of the lessee for the duration of the contract. The lessor will still be the tax payer (letter of the Ministry of Finance of Russia dated May 16, 2011 No. 03-05-05-04/12);

2)

registration of the vehicle initially in the name of the lessee. In this case, the payer will be the lessee. Moreover, if the purchase of the car is not provided, then the obligation to pay tax at the end of the contract will pass to the lessor only after re-registration of the vehicle.

D. Nacharkin, expert editor

Benefits of Accelerated Depreciation

The main advantages of this procedure:

- minimizing property taxes;

- a significant reduction in the tax base;

- the opportunity to buy out the leased object at a residual price reduced to zero or a minimum.

Why is there a tax cut?

The basis for calculating the tax base for property tax is the residual value of the car owned by the organization. The use of accelerating factors in relation to a car allows you to reduce the residual value at a faster pace than with the linear method. Complete write-off of the cost of vehicles with 3-fold depreciation occurs 3 times faster. This mechanism significantly reduces property tax and the period for its payment on the property.

Minimization of income tax within the scope of the agreement

Calculating depreciation charges in a 3-fold amount allows you to reduce the income tax base, since they relate to the costs of the enterprise and are included in the cost of production. The above effect is applicable for the duration of the leasing agreement.

But when calculating tax savings, it is worth considering that the book value of a car is the same when leasing and when purchasing. As a result, the amount of depreciation transferred to costs will also be identical for all methods of calculating depreciation.

It’s just that when using accelerating factors, it will be written off faster. But when the lease agreement expires, the car is completely written off, depreciation is not included in costs, and with linear depreciation, the transfer of the cost of the car to costs over the entire useful life will be uniform.

Therefore, the use of accelerating factors requires careful monitoring of the total amount of expenses. The costs over the period of their application can be quite large (especially if an expensive car is purchased) and negatively affect the financial results of the company.

Buying a car at a minimum residual value

A leasing transaction is generally concluded for a period that makes it possible to completely write off the car using accelerating multipliers. For example, an organization entered into a deal with a company to lease trucks with a carrying capacity of over 5 tons. These cars belong to depreciation group 5. The useful life is from 7 to 10 years inclusive.

Using a 3-fold accelerated depreciation mechanism, it is written off from the balance sheet in 28 months, less than 3 years. When redeeming, its residual amount by law may be zero or conditional (for example, 1000 rubles). At this price, the car will be reflected on the balance sheet of the lessee organization, and at the same price it can sell the car. This model is often used by managers who buy cars after leasing for themselves.