Typical transactions for issuing a loan from the founder

The founder issues an interest-bearing loan:

- Debit 66 (67) Credit 50 ().

Percentages are expressed by writing:

- Debit 91.2 Credit 66 (67).

Interest on accounts 66 is accounted for in a separate subaccount.

As a loan, the founder can pay the debt of his organization:

- Debit 60 Credit 66.

This type of operation is not prohibited by civil law. Difficulties and disputes arise when accounting for VAT.

When providing an interest-free loan by the founder, the transactions are the same, only the agreement must stipulate that interest is not charged for the use of money or property.

When the founder decides to “forgive” the organization’s debt, his share in the authorized capital must be taken into account. If the founder's share is more than 50%, then no taxable profit arises.

An organization can pay off its debt not only with money, but also with its products: First, revenue from the sale of products is reflected against the debt to the founder:

- Debit 76 Credit 91.

VAT must be charged on sales:

- Debit 90.3 Credit 68.02.

Debt offset:

- Debit 66 Credit 76.

Loan repayment

Returns are simple. The key points are:

- What we took, we return. You cannot return goods with money, you cannot return a cash loan with finished products and other material goods.

- If the loan is overdue or used for other purposes, the lender has the right to demand compensation and full return of the loaned funds.

- The contract may not establish a specific return period. Then the LLC returns the loan to the founder within 30 days after the lender submits a written request for the return of the borrowed funds.

- The debt can be forgiven. For the organization, this will not be operating income, which is taxed at the appropriate rate, depending on the taxation regime.

- It is impossible to immediately stipulate in the contract that the loan will be irrevocable, since this contradicts the very nature of the borrowing relationship. But nothing will prevent you from obtaining debt forgiveness literally a week after issuance - if such are the wishes of the lender.

Example of transactions for issuing an interest-free loan from the founder

The sole founder issued an interest-free loan to the company in the amount of 200,000 rubles. for 10 months. The interest rate on the loan is 2% per annum.

Postings:

| Account Dt | Kt account | Wiring Description | Transaction amount | A document base |

| Received a loan from the founder | 200 000 | Bank statement | ||

| 91.1 | 66 Percent | Reflection of interest accrual for using a loan | 3333 | Accounting information |

| Loan debt transferred to founder | 200 000 | Payment order ref. | ||

| Interest transferred | 3333 | Payment order ref. |

How to apply

Applying for the loan itself is not a complicated procedure. It is better to issue a loan through an agreement. It is imperative to indicate what the money is needed for, that is, what it is supposed to be spent on.

The form of the contract is not established by law. But the following points must be indicated:

- How is the loan provided?

- In what time frame?

- What is the interest rate and payment schedule?

- How are borrowed funds repaid?

Providing a loan is possible in several ways. Money can be transferred by bank transfer or in cash. Refunds can also be made using any convenient option.

The contract does not specify a period when the borrower must return the money. But another period is indicated - during which time he is obliged to pay the loan on demand. This is usually given for a period of 1 month.

It is important to consider that an agreement of this type comes into force only after the transfer of funds.

If funds are issued at interest, then the rate must be specified in the agreement. In the absence of this clause, the contract is automatically considered interest-free. The repayment schedule must also be included in the contract.

The scheme for repaying the loan to the founder is prescribed in a separate paragraph. You can do this in several ways:

- return the goods;

- transfer through a current account/card – cashless;

- give in cash;

- assets.

In each individual case there are nuances that must be taken into account when filling out the papers. Any return option must be detailed, including all information.

Issuing a loan to the founder

The issuance of a loan to the founder, if it is interest-free, is reflected by the posting:

- Debit 76 (73) Credit 50 ().

At the same time, the founder receives a benefit from interest savings (material), with which it is necessary to pay personal income tax. Account 73 is used if the founder is an employee of the company.

If the loan is with interest, then the issuance of money is formalized:

- Debit 58 (73) Credit 50 ().

When issuing a loan in the form of property:

- Debit 58 (73) Credit 01, 41, ...

Interest on the loan for the founder is reflected by the entry:

- Debit 76 (58.73) Credit 91.1.

Loan repayment: what to consider first?

Before deciding whether to return the interest-free loan to the founder on the card, you need to check:

- the founder-lender has no debt to contribute a share to the authorized capital - if the founder has not contributed his “authorized” share in a timely manner or has not transferred it to the company in full, the borrowed funds received will be used to pay off such debt, and there will be nothing to return to his card;

- the presence in the loan agreement of a condition allowing the use of a method of returning borrowed money to the founder’s card;

- compare the types of borrowed funds received by the company from the founder and the funds returned by it under the loan agreement.

If you received a batch of building materials under a loan agreement, then there can be no question of any return to the loan card in cash. Borrowing relationships presuppose a single rule: “what you borrow, return it” (Clause 1, Article 807 of the Civil Code of the Russian Federation).

Thus, having ensured against mistakes at the stage of agreeing on the terms of the loan agreement and having made sure that the loan can be repaid in money to the card of the founder-lender, you can proceed directly to the procedure for returning the borrowed funds (see below).

Interest-free loan from the founder

Here it is important to explicitly state in the contract that the loan is interest-free. Otherwise, interest is accrued “by default” based on the key rate of the Central Bank (clause 1 of Article 809 of the Civil Code of the Russian Federation).

However, it should be noted that this condition applies only to a cash loan. If the loan is issued in goods, then, on the contrary, “by default” it is considered interest-free. But this form of borrowing is rather “exotic” and is rare.

In this case, it is impossible to recognize a loan between Russian counterparties as a controlled transaction - after all, there is no income from the transaction.

But there is another side - the company receiving the loan. She does not pay interest, but otherwise (if the borrower were a “third party”), interest would be paid. Those. there is material gain.

However, the Tax Code of the Russian Federation does not establish the procedure for taxing such benefits when calculating profit tax (letter of the Ministry of Finance of the Russian Federation dated 02/09/2015 No. 03-03-06/1/5149).

Material interest benefits are not provided for when calculating other “current” taxes paid by legal entities, i.e. USN and Unified Agricultural Tax.

Thus, if both parties to the transaction are residents of the Russian Federation, then an interest-free loan does not entail tax consequences at all.

Loan from the founder, issued with interest

When issuing a loan with interest, you need to specify in the contract not only the interest rate, but also the calculation procedure. Otherwise, interest will be calculated monthly “by default” (clause 3 of Article 809 of the Civil Code of the Russian Federation).

If the loan agreement provides for the payment of interest, then for the founder it will be income. The taxation procedure for this income depends on the status of the creditor:

- An individual resident of the Russian Federation will pay personal income tax at the “regular” rate of 13%.

- Interest income of a foreign founder will be subject to income tax at a rate of 30% (clause 3 of Article 224 of the Tax Code of the Russian Federation).

- For a Russian legal entity, interest will be included in the income tax base or the “special” tax (USN, Unified Agricultural Tax).

- Interest income of a foreign organization is also subject to income tax.

In all cases when a foreigner receives income, the organization paying the interest must independently withhold the tax and transfer it to the budget.

Often the interest rates on loans that founders issue to their companies are set below market levels.

The question arises: can tax authorities recalculate interest income and force the owner to pay additional tax on lost profits?

The key point here is whether the owner and his company are interdependent persons. To do this, the founder must own more than 25% of the authorized capital, or directly participate in the management of the organization (Article 105.1 of the Tax Code of the Russian Federation).

But interdependence alone is not enough. In order for the tax authorities to recalculate the interest, the transaction must still be recognized as controlled.

If the founder and his subsidiary are residents of the Russian Federation, then for this it is necessary that the amount of income on the transaction (i.e. interest on the loan) for the year exceed 1 billion rubles. (clause 3 of article 105.14 of the Tax Code of the Russian Federation).

If the owner of the company is a foreigner registered in one of the offshore zones, then the transaction will be controlled for any amount (clause 3, clause 1, article 105.14 of the Tax Code of the Russian Federation).

The company receiving the loan recognizes interest on it as an income tax expense (USN, Unified Agricultural Tax) “on a general basis.”

Getting a loan with interest

Let's look at a simple example. A commercial company received 200,000 rubles from the founder, Vyacheslav Yakovlevich Salimgareev. According to the terms, the money was issued at 8% per annum. The return period is 12 months.

It is required to reflect the corresponding loan acceptance transactions and interest calculations. In addition, you need to reliably show the withholding of personal income tax, payment of monthly fees and debt.

If a company took money based on certain requirements, the accountant must create a settlement order in 1C 8.3. First of all, select the “Receiving a loan from a counterparty” section. In the window that appears, you need to enter current information:

- name of the organization and the corresponding date;

- the name of the organizer who issued the money;

- total loan amount.

Important! It is necessary to reflect the information using settlement account 66.03, because in the above situation the loan was taken out for a short-term period.

The following is the accounting entry: Dt 51 Kt 66.03 (credit funds were credited to a commercial company).

The loan reflects the amount of the company's total debt to the relevant person. Registration of funds for personal needs is available to the company in cash. In such a situation, an electronic document is created in 1C 8.3 “Cash receipt”. To do this, select the item “Receiving a loan from a counterparty.”

Calculation and accrual of interest on the loan

There is no uniform documentation for calculating interest charges. For this reason, you can only create a manual entry:

- go to the Operations item, then Accounting - Operations entered manually.

- Then click “Create” with the mouse.

- Here is the necessary accounting entry: Dt 91.02 Kt 66.04, for the amount of interest expenses for the month.

Important! The credit reflects interest calculated to be paid over 30 days. It is necessary to indicate the founder and the agreement.

A similar method will be used to calculate income for other periods. For general accruals, it is necessary to timely withhold personal income tax from an individual at a rate of 13% per annum. In this case, we will create a transaction manually using the posting: Dt 66.04 Kt 68.01 for the amount of personal income tax from the founder.

The accountant must enter this entry every month.

At the same time, in order to reflect the personal income tax in the financial statements, it is necessary to create an electronic document “Personal Income Tax Accounting Operation”:

- While in the “Salaries and Personnel” menu, go to “Personal Income Tax - All personal income tax documents”;

- Click on “Personal Tax Accounting Operation”.

In electronic form, you must provide information about your income, as well as the amounts of calculated and withheld personal income tax. A similar document should be created in subsequent months.

Transfer of interest to the founder

To return to a legal entity the money that is owed to it, you need to create a “Write-off from the current account” order. In this case, the link “Return of loan to counterparty” should be used.

The reporting form should indicate:

- what is the name of the company itself (select from the list);

- the individual or legal entity who founded the company;

- contract number;

- income interest part minus calculated personal income tax.

You can enter the information in the table as follows: Dt 66.04 Kt 51 for the payment amounts under the loan agreement. The debit reflects expenses paid to the company.

In subsequent months, interest is paid in the same way. Any of the actions must be performed strictly within the specified time frame.

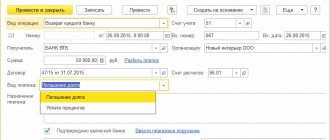

Repayment of the loan amount

At the end of the credit period, the principal amount of the debt must be transferred to the founder in full. For these purposes, it is important to make a document in the 1C 8.3 program “Write-off from a current account.”

When filling out the document we write down:

- name of the organization, date of compilation;

- parent company and contract number;

- the amount of the principal debt;

- In the Type of payment column, select “Debt repayment”.

Here is the current posting: Dt 66.03 Kt 51 for the amount of the repaid principal debt. The debit of the account reflects the paid loan to the founder.