Transition to the linear method

For fixed assets that are depreciated using the non-linear method, from the beginning of the next tax period the organization has the right to switch to the linear method of calculating depreciation. However, this is possible no earlier than five years after the start of using the nonlinear method. This procedure is provided for in paragraph 1 of Article 259 of the Tax Code of the Russian Federation.

During the transition, you need to establish the residual value of each fixed asset. This indicator should be determined as of January 1 of the year, starting from which the organization will calculate depreciation using the straight-line method. Calculate the depreciation rate based on the remaining useful life of each asset. If, after the end of its useful life, the fixed asset is not fully depreciated, the organization has the right to continue accruing depreciation until its cost is completely written off. Such clarifications are contained in the letter of the Ministry of Finance of Russia dated July 21, 2014 No. 03-03-RZ/35549.

Determination of the norm of the indicator

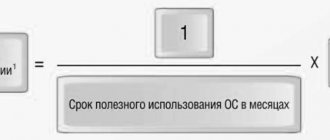

To carry out a linear calculation, you must first calculate the annual rate. This indicator reflects the amount of funds that are written off by inclusion in the cost of goods produced. Simply put, this is the percentage of the initial cost of the property that is written off in 1 year.

The formula for determining the annual rate is as follows:

- the K indicator expresses the annual depreciation rate;

- n – indicator reflecting the SPI.

By dividing the final result by the number 12, you can determine the monthly norm. This indicator reflects the percentage of the initial cost that must be depreciated over 1 month of operation of the facility.

Transition to a nonlinear method

When switching from a linear to a non-linear method, include fixed assets in the depreciation group (subgroup) at their residual value. Determine the residual value as of January 1 of the year from the beginning of which the accounting policy for tax purposes established the use of a non-linear depreciation method.

In this case, fixed assets must be included in depreciation groups based on the useful life established for these fixed assets when they were put into operation.

This procedure is provided for in paragraph 3 of Article 322 of the Tax Code of the Russian Federation.

Advantages and disadvantages of the method

The linear method is considered the most convenient for various taxation options. This has several important advantages.

It is most convenient to use this calculation option in cases where it is assumed that the object will become a source of equal profit throughout the entire period of use.

Table 1. Primary advantages and disadvantages of the method.

| Advantages | Flaws |

| the calculation is carried out once, the result obtained is valid until the end of the operational period; costs are transferred to cost evenly the depreciation period when using non-linear methods lasts longer; the method is simple when carrying out accounting operations, since each OS object is calculated. | not suitable for depreciation of objects with a short period of use; not convenient for equipment whose maintenance involves regular costs; not used in enterprises where property is constantly being updated. |

Under such conditions, the use of the straight-line method will lead to an increase in the depreciation period and associated tax costs.

Watch the video about depreciation methods:

Composition of depreciation groups

The composition of depreciation groups for calculating depreciation using the non-linear method is determined by the useful lives of fixed assets in accordance with the Classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1. If the procedure for calculating depreciation for fixed assets included in the same depreciation group, varies, within it one or more depreciation subgroups should be distinguished. For example, this should be done if part of the fixed assets with the same useful life is operated in an aggressive environment and depreciation on them is charged with an increasing factor (subclause 1, clause 1, article 259.3 of the Tax Code of the Russian Federation). Or if the organization uses certain fixed assets (except for buildings and structures) exclusively for R&D (clause 13 of Article 258 of the Tax Code of the Russian Federation).

Basic provisions

Depreciation in taxation is the transfer of costs incurred as a result of a purchase to the cost of goods and services produced by the enterprise. At its expense, funds spent on the purchase of equipment or construction of buildings are compensated.

Deductions in this area of the economy are made during the entire time of use of the device. The starting point is the moment of putting the equipment on balance, the final point is its removal. It does not matter whether the equipment was purchased new or used.

There are two methods for calculating depreciation - linear and non-linear. The owner of the enterprise is free to choose the method. The exception is acquisitions related to buildings and structures, which belong to 8-10 depreciation groups. They are subject to the linear method only.

The previously selected method could not be changed to another. Since the beginning of 2014, in connection with amendments to the law, the organization has the right to cancel the linear method at any time and replace it with another. But before this, it is necessary to make appropriate amendments to the company’s accounting policies. The transition from the nonlinear method is possible once every 5 years.

Depreciation calculation

To calculate depreciation using the nonlinear method, you need to determine:

1. Total balance of the depreciation group (subgroup). It is defined as the total cost of fixed assets that are included in the same depreciation group (subgroup). When determining the total balance, do not take into account the cost of fixed assets, for which depreciation can only be calculated using the straight-line method.

Initially, determine the size of the total balance on the 1st day of the tax period from which it was decided to apply the non-linear method. Subsequently, the total balance must be determined on the 1st day of each month. It is necessary to take into account that its size will change.

The total balance of the depreciation group (subgroup) may increase:

- when putting into operation new fixed assets included in this depreciation group;

- when the initial cost of fixed assets changes in the event of their completion, additional equipment, reconstruction, modernization, technical re-equipment.

The total balance of the depreciation group (subgroup) may decrease:

- upon disposal of a fixed asset;

- upon partial liquidation of a fixed asset.

In addition, the total balance is reduced monthly by the amount of accrued depreciation for this group of fixed assets for the previous month.

This is stated in paragraphs 2–4, 10 of Article 259.2, paragraph 1 of Article 322 of the Tax Code of the Russian Federation.

Determine the total balance on the 1st day of each month using the formula:

| The total balance of the depreciation group (subgroup) as of the 1st day of the month for which depreciation is calculated | = | Total balance of the depreciation group (subgroup) at the beginning of the previous month | + | Initial cost of fixed assets put into operation in the previous month | + (–) | The amount by which the initial cost of fixed assets increased (decreased) during completion, retrofitting, reconstruction, modernization, technical re-equipment, partial liquidation | – | The amount of accrued depreciation for the previous month (the amount of the residual value of the retired fixed asset) |

This procedure follows from the provisions of paragraphs 3, 4 and 10 of Article 259.2 of the Tax Code of the Russian Federation.

An example of determining the total balance of a depreciation group for calculating depreciation of a fixed asset using the non-linear method in tax accounting

The organization purchased five laptops in January. The cost of one laptop is 110,000 rubles. (without VAT). In accordance with the Classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1, the laptop belongs to the second depreciation group (useful life from two to three years).

The accounting policy for tax purposes determines that for fixed assets included in the second depreciation group, depreciation is calculated using a non-linear method.

As of January 1, the organization did not have fixed assets included in the second depreciation group. Therefore, the total balance of this depreciation group on January 1 is zero.

Laptops were put into operation in January. As of February 1, the total balance of the second depreciation group amounted to 550,000 rubles. (RUB 110,000 × 5 pcs.).

The depreciation rate for the second depreciation group is 8.8 percent.

The amount of accrued depreciation for February amounted to 48,400 rubles. (RUB 550,000 × 8.8%).

In February, the organization purchased another laptop worth RUB 102,000. (without VAT) and put it into operation in the same month.

The total balance of the second depreciation group as of March 1 is equal to: 550,000 rubles. + 102,000 rub. – 48,400 rub. = 603,600 rub.

The amount of accrued depreciation for March was: RUB 603,600. × 8.8% = 53,117 rub.

2. Depreciation rate. The depreciation rates that are applied under the non-linear method are defined in paragraph 5 of Article 259.2 of the Tax Code of the Russian Federation. For each depreciation group, fixed depreciation rates are established, which do not depend on the useful life of fixed assets (as with the straight-line method).

Calculate the monthly depreciation amount using the formula:

| Monthly depreciation amount | = | Total balance of the depreciation group as of the 1st day of the month | × | Depreciation rate for the corresponding depreciation group | : | 100% |

An example of calculating depreciation using the non-linear method in tax accounting

In January, the organization purchased a fixed asset - a laptop at a price of 102,000 rubles. (without VAT). The laptop was put into operation that same month. The accountant determined that, in accordance with the Classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1, the laptop belongs to the second depreciation group (useful life from two to three years). The useful life of the laptop is 36 months. The organization has no other fixed assets included in this depreciation group.

According to the accounting policy, for tax purposes, depreciation on computer equipment is calculated using a non-linear method.

The monthly depreciation rate for fixed assets included in the second depreciation group is 8.8 percent (clause 5 of Article 259.2 of the Tax Code of the Russian Federation).

Every month, the accountant determined the total balance of the depreciation group and the amount of depreciation for this group:

| Month | Total balance of the depreciation group at the end of the month | Amount of accrued depreciation by depreciation group |

| 2016 | ||

| January | 102,000 rub. | 0 rub. |

| February | RUB 93,024 (RUB 102,000 – RUB 8,976) | 8976 rub. (RUB 102,000 × 8.8%) |

| March | RUB 84,838 (RUB 93,024 – RUB 8,186) | 8186 rub. (RUB 93,024 × 8.8%) |

| April | RUR 77,372 (RUB 84,838 – RUB 7,466) | 7466 rub. (RUB 84,838 × 8.8%) |

| May | RUB 70,563 (RUB 77,372 – RUB 6,809) | 6809 rub. (RUB 77,372 × 8.8%) |

| June | RUB 64,353 (RUB 70,563 – RUB 6,210) | 6210 rub. (RUB 70,563 × 8.8%) |

| July | RUB 58,690 (RUB 64,353 – RUB 5,663) | 5663 rub. (RUB 64,353 × 8.8%) |

| August | RUR 53,525 (RUB 58,690 – RUB 5,165) | 5165 rub. (RUB 58,690 × 8.8%) |

| September | RUB 48,815 (RUB 53,525 – RUB 4,710) | 4710 rub. (RUB 53,525 × 8.8%) |

| October | RUB 44,519 (RUB 48,815 – RUB 4,296) | 4296 rub. (RUB 48,815 × 8.8%) |

| November | RUB 40,601 (RUB 44,519 – RUB 3,918) | 3918 rub. (RUB 44,519 × 8.8%) |

| December | RUB 37,028 (RUB 40,601 – RUB 3,573) | 3573 rub. (RUB 40,601 × 8.8%) |

| 2017 | ||

| January | RUB 33,770 (RUB 37,028 – RUB 3,258) | 3258 rub. (RUB 37,028 × 8.8%) |

| February | RUB 30,798 (RUB 33,770 – RUB 2,972) | 2972 rub. (RUB 33,770 × 8.8%) |

| March | RUB 28,088 (RUB 30,798 – RUB 2,710) | 2710 rub. (RUB 30,798 × 8.8%) |

| April | RUB 25,616 (RUB 28,088 – RUB 2,472) | 2472 rub. (RUB 28,088 × 8.8%) |

| May | RUB 23,362 (RUB 25,616 – RUB 2,254) | 2254 rub. (RUB 25,616 × 8.8%) |

| June | RUB 21,306 (RUB 23,362 – RUB 2,056) | 2056 rub. (RUB 23,362 × 8.8%) |

| July | RUB 19,431 (RUB 21,306 – RUB 1,875) | 1875 rub. (RUB 21,306 × 8.8%) |

After 18 months of using the laptop, the total balance dropped below 20,000 rubles. The organization did not put into operation any other fixed assets belonging to the second depreciation group.

In August 2021, the accountant included in non-operating expenses the entire amount of the residual value for this depreciation group in the amount of 19,431 rubles.

Tax accounting

In tax accounting, the amount of depreciation is calculated at the beginning of the period. The total balance is calculated for the group, i.e. the sum of the residual value for all objects of the subgroup. When a new facility is put into operation, it will increase, and when it is retired, it will decrease.

The amount of depreciation for the subgroup must be calculated using the formula:

- Amg – group depreciation per month

- SBg – total balance for the subgroup

- K – depreciation rate

Table 4. Norm of the indicator.

| Group | Norm |

| 1 | 14,3 |

| 2 | 8,8 |

| 3 | 5,6 |

| 4 | 3,8 |

| 5 | 2,7 |

| 6 | 1,8 |

| 7 | 1,3 |

| 8 | 1,0 |

| 9 | 0,8 |

| 10 | 0,7 |

Depreciation and tax accounting on video:

When giving preference to any of the wear methods, it is important to carefully analyze all the advantages and disadvantages for a particular enterprise. Changing the selected method is not possible during the period of calculating depreciation for the element taken into account

Write your question in the form below

Depreciation period

Accrue depreciation from the 1st day of the month following the month in which the property was put into operation (clause 4 of Article 259 of the Tax Code of the Russian Federation). In the same order, calculate depreciation on capital investments in the form of inseparable improvements to fixed assets received under lease agreements or gratuitous use (loans) (clauses 6, 7 of Article 259.2 of the Tax Code of the Russian Federation).

When depreservation, completion of reconstruction (modernization) of a fixed asset, as well as when returning a fixed asset transferred for free use, depreciation is calculated from the 1st day of the month following the month in which these events occurred (clause 9 of Article 259.2 of the Tax Code of the Russian Federation ).

Accrue depreciation for each depreciation group (subgroup) until its total balance is less than 20,000 rubles. In the month following the one in which this value was achieved (provided that in the next month the total balance of the depreciation group did not increase), the organization has the right to liquidate this depreciation group (subgroup) and write off its residual value as non-operating expenses. This procedure is provided for in paragraph 12 of Article 259.2 of the Tax Code of the Russian Federation.

Using odds

In some cases, when calculating depreciation using the linear method, additional coefficients can be applied to the basic depreciation rate, depending on which it:

- Increasing;

- Decreases.

The Tax Code of the Russian Federation determines in what cases and amounts they are applied.

A multiplying factor not higher than 2 is used in the following cases:

- When using equipment in an aggressive environment and with increased shifts. An aggressive environment means an explosive, poisonous, fire hazardous environment that can cause an accident, natural and artificial circumstances leading to increased wear and tear of an asset.

- For fixed assets of industrial agricultural enterprises.

- For the property of organizations with resident status of an industrial and production special economic zone.

- For equipment with high energy efficiency.

An increasing factor of no higher than 3 is used for the following objects:

- When the leased property wears out. The exception is assets that belong to depreciation groups numbered 1, 2, 3.

- For depreciation of funds that are intended for the implementation of scientific and technical activities.

- For equipment that is used when conducting activities related to the production of hydrocarbons in a new offshore hydrocarbon field.

Clause 10 of Article 259 of the Tax Code of the Russian Federation allows enterprises to establish reduced wear rates. They cannot be changed throughout the tax period. These coefficients must be specified in the accounting policy and applied from the beginning of the tax period.

Calculation for used OS

Many enterprises, in the course of their activities, acquire facilities that have previously been used. In addition to non-new property, items that were contributed as a contribution to the authorized capital are regarded as used. This category also includes property that remained at the enterprise after its reorganization.

Depreciation using this method for objects that have already been used is carried out in the same way as for new ones. Therefore, the calculation procedure is similar.

The exception is that used OSes will have a shorter service life. To calculate it, you need to subtract the number of years that the object was used by the previous owner from the service life indicator from the classifier. Further calculations are carried out using the previously described formulas.

Results

The concept of depreciation is used in accounting and is important in taxation. The value of the parameter is regulated by regulations. Due to the limit values, the company has the opportunity to reduce its tax liabilities. Management has the right to independently choose the method of calculation, however, in some situations that fall under exceptions, it is determined in accordance with the provisions of legislative acts. A business representative needs to take into account that in homogeneous groups of objects of value one calculation method should be used.

Linear method - what is it?

One of the simplest methods for calculating depreciation of fixed assets is the straight-line method. It implies that the full cost of the property accepted on the balance sheet will be written off evenly throughout the entire period of use. The specifics of using this method are reflected in paragraph 4 of Article 259 of the Tax Code of the Russian Federation.

To calculate depreciation, an accountant needs the following input parameters:

- Primary cost. Construction costs, if any, are added to the purchase price. If the enterprise has revalued the fixed assets, then instead of the primary value, the replacement value is used.

- Lifetime. To determine it, you can use a special classification list. There, all operating assets are divided into groups; you just need to find which of them the acquired property belongs to. If the asset cannot be classified into any depreciation group, then the enterprise independently calculates the service life, taking as a basis the planned physical wear and tear, the approximate time of use and operating conditions of the property.

Knowing these two parameters, you can calculate the depreciation rate and future charges.

Formulas for calculating depreciation using the straight-line method

The depreciation rate is a relative indicator that determines what part of the value of the property should be written off annually. Expressed as a percentage. The formula for calculation looks like this:

Where:

- K – depreciation rate for the year,

- n – number of years of use.

Enterprises most often use monthly rather than annual rates. In this case, the resulting value must be divided by another 12.

But to calculate depreciation, you need an absolute, not a relative indicator, that is, a specific number that will determine the amount of monthly depreciation deductions. In this case, you need to use the following formula:

Where C is the initial cost of the OS.

Calculation example

To make the calculation procedure more clear, let's consider a specific situation.

On April 5, 2021, a wood processing machine was purchased. Its initial cost is 216,000 rubles. It was at this price that the machine was put on the balance sheet of the enterprise without any additional expenses. How to determine the amount of future depreciation deductions?

First you need to refer to the OS classification reference book. According to it, the machine is included in the 4th depreciation group. It follows that its service life is 6 years. We have all the data for the calculation, now let’s determine the amount of monthly depreciation charges:

This means that for 6 years, every month 3,000 rubles will be applied to the organization’s expenses as depreciation charges.

Rules for calculating depreciation

Using the linear method involves following a number of rules. The organization should be guided by the following features:

- monthly depreciation should be calculated on the 1st;

- the first time depreciation is accrued only in the next month after the fixed assets are accepted onto the balance sheet;

- if the operating time has ended or the asset is no longer listed on the enterprise’s balance sheet, then depreciation charges stop starting from the next month;

- if a decision is made to preserve the asset for more than 3 months or it requires long-term repairs (more than 12 months), then during this time there is no need to make depreciation charges;

- even if there are losses, deductions must be made;

- Accounting for accruals must be done in the tax period in which they were made.

Innovations for 2021 related to depreciation of fixed assets

Since the beginning of the year, several innovations have appeared regarding property depreciation:

- if fixed assets are used in unfavorable conditions or they are involved in longer shifts, then the increasing factor is prohibited from applying to them (does not apply to property continuously used in accordance with its properties);

- an organization cannot use several increasing factors at once;

- Enterprises using the non-linear depreciation method can switch to the straight-line method.