What is the useful life of buildings and structures

Serious engineering communications, such as buildings and structures, as a rule, serve as fixed assets for a long time: years and decades. They slowly lose properties useful for use. But the concept of “long” is very vague. In each specific case, the useful life (USI) can vary greatly. How exactly to set this deadline and document it correctly, what points to pay attention to when regulating, read in this article.

Why determine SPI

Useful lives are established for adequate accounting purposes. But in accounting and tax accounting, the features of their establishment are different, since the goals are different:

- SPI for accounting. It is necessary in order to correctly determine the decrease in the value of a fixed asset and correctly calculate depreciation on it. PBU 6/01 in paragraph 20 says that the organization can set this period at its discretion, taking into account the following key parameters:

- how long it is planned to actively use the building or structure;

- what factors influence physical wear and tear in this particular case;

- what degree of wear is acceptable;

- Are there any special restrictions for a specific property (for example, staying in a rental, leasing, etc.).

- SPI for tax accounting . It is established to classify fixed assets according to the time of their useful operation (clause 1 of Article 258 of the Tax Code of the Russian Federation). For this purpose, all fixed assets are divided into groups, the composition of which is fixed in the classification table. This document was approved by the Government of Russia in Resolution No. 1 of January 1, 2002. The table shows codes according to the classifier adopted for fixed assets (OKOF) and the distribution of fixed assets by groups. For each group, a time range is established within which the SPI can be assigned for each asset (including “long-term” ones, such as buildings and structures).

This is important to know: Non-residential premises management agreement

NOTE! When maintaining accounting records, it is convenient to use the Tax Classification to determine the SPI of real estate: in this case, the calculations will be the same, that is, depreciation deductions will be calculated at a minimum. But it is also possible to set a smaller SPI in accounting.

The method for determining SPI must be recorded in the accounting policies of the organization.

How is the SPI of structures as fixed assets determined?

In accounting and tax accounting, the rules for establishing the service life of fixed assets differ.

In accounting, a company has the right to independently determine SPI using the provisions of clause 20 of PBU 6/01.

To correctly establish the period for depreciation of a building, structure or premises for any purpose, the following parameters must be taken into account:

- the period during which the company plans to operate the asset with the required return;

- planned physical wear and tear, taking into account the totality of influencing factors;

- restrictions that exist for a specific asset depending on the situation, for example, this may be the rental or leasing period - depreciation during leasing.

The tax authorities should take into account the provisions of clause 1 of Article 258 of the Tax Code of the Russian Federation, which states that for fixed assets the period is set in accordance with the depreciation group to which the asset belongs.

The groups are presented in the Classification approved by Decree of the Government of the Russian Federation No. 1 of 01/01/2002. It contains OKOF codes (according to the classifier of fixed assets), names of fixed assets and notes on them with distribution by depreciation groups.

For each, a range of years is prescribed within which the useful life can be selected.

It is convenient to use the Classification developed for tax purposes when determining the SPI for real estate or a building in accounting.

In this case, the period for calculating depreciation on the structure will be the same in both tax and accounting. This is very convenient and allows you to minimize discrepancies in depreciation charges.

It is recommended that the method for establishing the period of use be specified in the accounting policy, especially if tax classification is used for accounting.

The useful service life established when a building was accepted for registration may change during its capital improvements, modernization, completion, or reconstruction. Accounting for depreciation after modernization.

Is SPI established for land?

Depreciation groups of buildings and structures

According to the Classification, various types of real estate in the form of buildings and structures can be classified into several groups for calculating depreciation - from 4 to 10. Each group includes buildings of certain, strictly defined types, for which different time intervals are provided for. Table 1 shows various immovable objects with the SPI periods established for them.

Table. Depreciation groups for buildings and structures

| № | Depreciation group | Features of the property | Sample SPI |

| 1 | 4 | Film non-residential structures, mobile structures, kiosks made of various materials (metal, glass, plastic, pressed plates) | 5 – 7 |

| 2 | 5 | Prefabricated and mobile structures not intended for housing | 7 – 10 |

| 3 | 6 | Residential buildings of lightweight construction (frame, reed, etc.) | 10 – 15 |

| 4 | 7 | Various non-residential buildings (frame and panel) made of wood, wood and metal, panels, adobe, etc. | 15 – 20 |

| 5 | 8 | Frameless buildings with lightweight walls made of stone, timber, logs with floors, columns, pillars made of various materials (not intended for housing) | 20 – 25 |

| 6 | 9 | Stone warehouses for vegetables/fruits (reinforced concrete or brick columns are allowed) | 25 – 30 |

| 7 | 10 | Other non-residential buildings and structures (brick objects, etc.). Residential buildings and premises | Over 30 |

Depreciation period of buildings

- Walls and foundation: 100 - 150 years;

- Floors made of various materials: 70 - 150 years;

- Staircase structures: 80 - 100 years;

- Floor coverings: 80 - 100 years;

- Internal non-load-bearing foundations: 40 - 150 years;

- Load-bearing elements of various building structures: 100 - 150 years;

- Roofing coverings: 10 – 80 years;

- Door and window structures: 20 - 30 years;

- Sewage system: 30 years;

- Heating and ventilation systems: 30 years;

- Gas installations: 20 years;

- Freight elevators without a conductor: 20 years.

- Service life of interior and exterior finishing of buildings:

- External cladding of buildings: 125 years;

- Tiling: 60 - 75 years;

- Internal cladding of buildings: 40 years;

- Painting of structures: 20 – 45 years.

- Viability is the process of preserving the physical and other properties of structures, which are determined during the creation of the structure design and guarantee its use throughout the entire period of operation with established control and regular maintenance;

- Durability is the ability of objects and structures to perform specified tasks throughout the entire period of use;

- Design service life is the estimated period of operation of an object, determined by building codes or design goals, depending on the purposes of its construction with established regular technical inspection and maintenance of equipment and individual functional elements;

- A construction site is an object that falls under the category of residential or public premises, as well as a service or engineering building.

* By order of Rosstandart dated December 23, 2010 No. 1059-st, GOST R 54257-2010 was put into effect on September 1, 2011. In connection with the approval and entry into force of GOST R 54257-2010, the use of GOST 27751-88, included in the “List of national standards and codes of practice (parts of such standards and codes of practice), as a result of which, on a mandatory basis, compliance with the requirements of the Federal Law “Technical Regulations on the Safety of Buildings and Structures”, approved by Decree of the Government of the Russian Federation dated June 21, 2010 No. 1047-r (hereinafter referred to as the List of Mandatory Use). When state registration of rights to a land plot, the annual tax amount can be contributed to the budget of one of the parties (by agreement).

Subsequently, the tax amount is from January 1 of the current year to the beginning of the month in which he transfers the land plot. The subsequent payer calculates the amount of tax for the period from the beginning of the month in which he acquired the right to the land plot.

- persons awarded orders and medals of the former USSR for selfless labor and impeccable military service in the rear during the Great Patriotic War, persons who worked (served) for at least six months from June 22, 1941 to May 9, 1945 and were not awarded orders and medals of the former USSR for selfless labor and impeccable military service in the rear during the Great Patriotic War; The fourth depreciation group (useful life over 5 years and up to 7 years) includes “Buildings (except residential)” - “Buildings made of film materials ( air-supported, pneumatic frame, tent, etc.); mobile all-metal; mobile wood-metal; kiosks and stalls made of metal structures, fiberglass, pressed plates and wood” (OKOF code 210. 00. 00. 00. 000). * By order of Rosstandart dated December 23, 2010 No. 1059-st, GOST R 54257-2010 was put into effect on September 1, 2011. In connection with the approval and entry into force of GOST R 54257-2010, the use of GOST 27751-88, included in the “List of national standards and codes of practice (parts of such standards and codes of practice), as a result of which, on a mandatory basis, compliance with the requirements of the Federal Law “Technical Regulations on the Safety of Buildings and Structures”, approved by Decree of the Government of the Russian Federation dated June 21, 2010 No. 1047-r (hereinafter referred to as the List of Mandatory Use). Design service life is the period of use of a construction project for its intended purpose, established in building codes or in a design assignment, until major repairs and (or) reconstruction with the required maintenance. The estimated service life is counted from the start of operation of the facility or the resumption of its operation after major repairs or reconstruction (clause 2.11);

- Viability is the process of preserving the physical and other properties of structures, which are determined during the creation of the structure design and guarantee its use throughout the entire period of operation with established control and regular maintenance;

- Durability is the ability of objects and structures to perform specified tasks throughout the entire period of use;

- Design service life is the estimated period of operation of an object, determined by building codes or design goals, depending on the purposes of its construction with established regular technical inspection and maintenance of equipment and individual functional elements;

- A construction site is an object that falls under the category of residential or public premises, as well as a service or engineering building.

When state registration of rights to a land plot, the annual tax amount can be contributed to the budget of one of the parties (by agreement). Subsequently, the tax amount is from January 1 of the current year to the beginning of the month in which he transfers the land plot. The subsequent payer calculates the amount of tax for the period from the beginning of the month in which he acquired the right to the land plot.

How to determine SPI: algorithm

When a company acquires a fixed asset - any kind - it needs to be depreciated, for which it is necessary to know the period of its planned useful use. In the table it is given in approximate time frames, but for each object it must be indicated precisely. The algorithm is as follows:

- Compare with the left column of the Classification table - determine which depreciation group your building and structure belongs to.

- Specify the established deadline in the text of the Order signed by the head of the organization.

- For accounting, set the SPI yourself or also use the Classification (this is much more convenient).

SPI for parts and the whole

What if the room for which the SPI needs to be determined is part of the building? There are accepted rules regulating quite common situations in determining the SPI of buildings and structures:

- each individual residential premises in a common residential building (for example, an apartment building) receives the same SPI as the entire building as a whole - as a rule, for at least 30 years;

- if there is a non-residential premises (hall, office, etc.) in a residential building, then it acquires the same SPI as the entire house (also, as a rule, from 30 years).

SPI upon change of owner

A piece of real estate may change its owner and end up in the hands of a new owner not new. How to determine the useful life in this case?

It is necessary to correctly establish depreciation, and from here calculate the depreciation period. This must be done separately for tax and accounting purposes.

SPI of used objects for tax accounting

The tax legislation of the Russian Federation provides for the possibility of reducing the SPI of a non-new property for the period during which it was used by the former owner (clause 7 of Article 258 of the Tax Code of the Russian Federation). This time can be easily determined from the accompanying documentation (transfer and acceptance certificate OS-1a) when purchasing a fixed asset.

IMPORTANT! If it is not possible to establish this period from the documents, then it is legally impossible to reduce the SPI. Even if such confirmation exists, a reduction in SPI is not necessary.

If there is no documentary evidence of the operation of the building, it will be considered new from the point of view of tax accounting. To determine its SPI, the above algorithm should be used.

This is important to know: Licensing of activities for managing apartment buildings: how to obtain

If you purchase a building or structure that has been in use for more than 30 years, it may end up being completely depreciated. In this case, the new owner evaluates the condition of the object according to safety regulations and sets a reasonable SPI for it at his own discretion.

SPI of non-new objects for accounting

There are no legislative regulations here, other than those prescribed in the accounting policies of the organization itself. By establishing SPI for accounting, the owner can:

- follow the requirements of the Classification (duplicate tax accounting);

- Having thoroughly assessed the object, set another appropriate period.

From a letter to the editor:

“When calculating depreciation during the operation of fixed assets in 2014, the organization encountered the following situations.

Situation 1. The organization’s balance sheet includes 2 buildings built in 1969:

– depreciation of one building was completed in 2012;

– depreciation of the second building has not been completed. The useful life is set equal to the standard one and is 50 years, the actual service life is 45 years. Accordingly, the remaining useful life in 2014 was 5 years.

In May 2014, the reconstruction of these 2 buildings was completed, which significantly improved their technical condition and functional characteristics.

Situation 2. The organization’s balance sheet also includes a building built in 1990. The useful life is set equal to the standard - 50 years. The reconstruction of the building was completed in March 2014. The useful life after the reconstruction was not revised.

The following questions arose regarding the establishment and revision of depreciation periods for these buildings:

1. Are there any restrictions on establishing the maximum and minimum useful life after completion of the reconstruction of a fully depreciated building?

2. Is it possible, when reviewing the useful life after completion of reconstruction, to go beyond the range of useful life established in Appendix 3 to Instruction No. 37/18/6*? ___________________________ * Instructions on the procedure for calculating depreciation of fixed assets and intangible assets, approved by Resolution of the Ministry of Economy, Ministry of Finance and Ministry of Construction and Architecture of the Republic of Belarus dated February 27, 2009 No. 37/18/6 (hereinafter referred to as Instruction No. 37/18/6).

For example, in situation 1, is it possible to set the remaining useful life of the second building to 30 years, if in fact the total useful life is 75 years (45 + 30) and is outside the useful life range (with a standard useful life of 50 years, the useful life will be from 40 to 60 years)?

3. If after the reconstruction of the building the useful life was not revised (not extended), does the organization have the right to revise the useful life from January 1, 2015 downward, taking into account the fact that the building was previously reconstructed?

Galina Sergeevna, accountant"

What are the conditions for determining the useful life

Standard service life of fixed assets, incl. previously in operation, is determined upon acquisition by each balance holder or owner from the date of their acceptance for accounting upon commissioning in years (the corresponding number of months) (clause 18 of Instruction No. 37/18/6).

For objects that were previously in operation, the organization’s commission for implementing depreciation policy (hereinafter referred to as the organization’s commission) has the right to:

– determine the standard service life twice as low as the corresponding values given in the classification of depreciable fixed assets, but not lower than 3 years for buildings, structures and transmission devices and 2 years for other fixed assets;

– if the period of actual use of the object on the date of acquisition, the transition to the use of standard service lives established by Resolution of the Ministry of Economy of the Republic of Belarus dated September 30, 2011 No. 161, turns out to be equal to or more than the corresponding value given in the classification of depreciable fixed assets, determine for the purpose of depreciation the paid cost of the acquired object fixed assets have a standard service life independently taking into account the technical condition of the facility, safety requirements and other factors for a period of at least 1 year (clause 18 of Instruction No. 37/18/6).

Let me remind you that the useful life is the expected or estimated period of operation of fixed assets and intangible assets in the process of business activity (clause 19 of Instruction No. 37/18/6).

The useful life is established in years (the corresponding number of months) within the limits between the lower and upper limits of the ranges (accurate to 2 decimal places) for groups of depreciable fixed assets and intangible assets in accordance with Appendix 3 to Instruction No. 37/18/6.

At the same time, there is a general requirement for establishing a useful life: the lower limit of the useful life range cannot be less than 1 year (clause 21 of Instruction No. 37/18/6).

An exception to this requirement is the case of the resumption of depreciation on previously depreciated fixed assets after completion of modernization, reconstruction, additional equipment, completion of them, technical diagnostics and inspection, for which the useful life is determined by the organization’s commission taking into account the technical condition of the object and safety requirements and other factors.

The organization's commission has the right to revise the standard service life and (or) useful life of fixed assets with mandatory reflection in the accounting policy of the possibility of their revision from the beginning of the reporting year, as well as in cases of completion of modernization, reconstruction, partial liquidation, additional equipment, completion, technical diagnostics. and surveys, formalized as capital investments by acts of acceptance of work performed, in cases of revaluation with the involvement of an appraiser, in the cases listed in paragraphs. 25, and 46 of Instruction No. 37/18/6 (clause 24 of Instruction No. 37/18/6).

Taking into account these standards, we will consider approaches to establishing and revising useful life in these situations.

How to determine the useful life after reconstruction of a fully depreciated object

In the case of modernization, reconstruction, additional equipment, or completion, the depreciable cost is subject to change: it increases by the amount of the corresponding costs (clause 9 of Instruction No. 37/18/6).

Thus, after the reconstruction, the building already has a residual (under-depreciated) value, which must be depreciated in the generally established manner. Depreciation should be resumed from the month following the month of completion of reconstruction and commissioning of the facility.

In this case, the organization’s commission determines the remaining useful life of the object. In this case, it independently establishes the period of expected operation of the fixed asset after reconstruction. I note that Instruction No. 37/18/6 does not provide for any restrictions when establishing the useful life of a previously depreciated building after its reconstruction.

The organization's commission has the right to choose any depreciation period for the residual value. Such a period can be set for a period of less than 1 year (for example, several months).

For reference: the lower limit of the range cannot be less than 1 year, with the exception of the case of resumption of depreciation on previously depreciated fixed assets after completion of their modernization, reconstruction, additional equipment, completion, technical diagnostics and inspection, for which the useful life is determined by the organization’s commission taking into account the technical condition of the facility, safety requirements and other factors (clause 21 of Instruction No. 37/18/6).

The maximum (upper) limit of the useful life after reconstruction of a fully depreciated fixed asset is not regulated. In your case, it may be recommended that when establishing a useful life, you should still remain within the upper limit of the range of useful life for a new similar building (with a standard service life of 50 years, this maximum useful life will be 60 years). This is explained by the fact that improving the characteristics of a building as a result of its reconstruction can hardly extend its service life more than for a new similar facility.

The only necessary condition is that the useful life must be reasonable and take into account the technical condition of the object, the period of its possible safe use, and other factors affecting the possibility of using the object in the organization. Such a conclusion can be made only taking into account the opinion of representatives of technical services that are part of the organization’s commission.

Revision of useful life after completion of reconstruction

If depreciation of an object is not completed, then after reconstruction the organization’s commission has the right to revise the useful life of the object (clause 24 of Instruction No. 37/18/6).

It should be noted that Instruction No. 37/18/6 does not stipulate the procedure for revising the useful life after reconstruction and the need to comply with the useful life ranges during such a revision.

In this case, it is advisable to take into account that the reconstruction of fixed assets involves increasing the technical level of objects, obtaining higher qualitative and quantitative indicators of their use (Appendix 5 to Instruction No. 37/18/6). This may lead to an increase in the period of possible operation of the object in the organization, i.e. useful life.

Taking into account the possible improvement in the quality characteristics of the object after reconstruction, the residual useful life can be increased by decision of the organization’s commission, taking into account the possible (longer) period of further operation of the object. In this case, the total useful life may go beyond the ranges established in Appendix 3 to Instruction No. 37/18/6.

In the situation under consideration, it is legal to set the residual useful life to 30 years, if such a period, in the opinion of the organization’s commission, corresponds to the technical condition of the object and the period of its possible safe use. This revision is legal within the framework of the law, despite the fact that the total useful life will be 75 years and will be outside the useful life range.

Revision of useful life from the beginning of the year

I note that reviewing the useful life after reconstruction is the right, and not the obligation of the organization (clause 24 of Instruction No. 37/18/6). Accordingly, in situation 2, the organization has the right not to revise the useful life after completion of reconstruction in March 2014.

Clause 24 of Instruction No. 37/18/6 also establishes the organization’s right to review the useful life from the beginning of the reporting year. An organization can take advantage of this right regardless of the previously carried out work on the reconstruction of the building and its results. Revision of useful life from the beginning of the year can be carried out either upward or downward. In this case, Instruction No. 37/18/6 contains no restrictions.

Thus, regardless of the fact that reconstruction work was carried out on the building (completed in March 2014), the organization will have the right to review the useful life from January 1, 2015, incl. in the direction of decrease.

Sincerely yours, Olga Pavlovna

Features of SPI for certain real estate objects

Each building and structure has a set of unique characteristics that affect the period of its possible use as a fixed asset. But there are some features that allow you to group objects to establish an adequate SPI. Let's consider the most common types of buildings and structures from the point of view of classifying them into one or another depreciation group.

Brick buildings

Brick is a very strong and durable material that is little subject to wear. Buildings constructed from it serve regularly for many decades without losing any significant characteristics. Whether they are residential buildings or other structures, their SPI will be the longest of those provided for in the Classification table. The rubricator provides for group 10 for them, according to which you can set any period over 30 years. Which one, the organization has the right to determine itself.

Garages

Schools

This type of structure is not residential: 24-hour stays are not planned there. If the school is capital, it is most often classified as group 10: these structures last more than 30 years.

How to determine the useful life of a non-residential building

In tax accounting, depreciate property over its useful life. Determine the useful life of a fixed asset yourself using the following rules: Determine the useful life of used fixed assets in a special manner, see How to calculate depreciation of used fixed assets in tax accounting. The validity of this conclusion is confirmed by arbitration practice, see. You can determine the depreciation group and useful life by submitting a corresponding request to the Ministry of Economic Development of Russia.

Building without a confirmed service life

This conclusion follows from paragraph 1 of Article 256 of the Tax Code. Depreciable property is distributed among depreciation groups in accordance with its useful life. Useful life is the period during which an item of fixed assets or an item of intangible assets serves to fulfill the goals of the taxpayer's activities.

The useful life is determined by the taxpayer independently on the date of commissioning of this depreciable property object, taking into account the Classification of fixed assets, approved by Decree of the Government of the Russian Federation dated January 1, 2002 No. 1 (hereinafter referred to as Classification). This is indicated by paragraph 1 of Article 258 of the Tax Code of the Russian Federation.

To which depreciation group can non-residential premises be classified for the purpose of calculating income tax?

Each of them includes buildings taking into account their structural characteristics. Thus, the useful life of the building is determined in the range specified for each depreciation group. Moscow from Thus, in the case under consideration, documents confirming operation may be:. The third group includes fixed assets with a useful life of no more than five years.

Further calculations are carried out in exactly the same way. In a non-linear way, the cost of buildings is written off much faster than in a linear way. The method is convenient to use in organizations that prefer accelerated depreciation. Peculiarities of depreciation calculations for re-opened and reconstructed buildings When buildings are mothballed for a period exceeding three months, depreciation is paused.

Useful life of the building

The organization purchased a building that was in use. There is an extract from the technical passport of the BTI, according to which the year of construction is the Previous owner is an individual entrepreneur using the simplified tax system. Among the documents containing data to determine the actual life of the building by the previous owners, there is a purchase and sale agreement, an acceptance certificate not in the OS-1 form and an extract from the technical passport of the BTI. The building belongs to the 1st group of the Classification of fixed assets. The method of calculating depreciation is linear.

How to find out the depreciation rate for a non-residential building

Please enable JavaScript for a better site experience. Many enterprises have buildings and structures on their balance sheets, for which depreciation charges are calculated. According to it, buildings and structures belong to groups for which the maximum useful life is set at and over 30 years, respectively. Regardless of the commissioning period, to calculate depreciation for buildings and structures, use the linear accrual method, in which the cost of a fixed asset decreases evenly over the entire period of use. Accrue depreciation on the building in accordance with the depreciation rate that is determined for this object, taking into account its useful life.

They are close to those for accounting, but still different. The useful life is the period during which an item of fixed assets or an item of intangible assets serves to fulfill the goals of the taxpayer's activities. The useful life is determined by the taxpayer independently on the date of commissioning of this depreciable property item.

Tip 1: How to calculate depreciation on a building

An indispensable real estate assistant. Rubric question - answer related to real estate. The organization acquired the following real estate assets under a purchase and sale agreement for the amount of 2 rubles: a warehouse with a total area of 7 sq. m. When transferring property, the cost of each individual inventory item will be specified by the seller.

This is important to know: List of organizations for managing an apartment building: temporary management company

WATCH THE VIDEO ON THE TOPIC: Depreciation by the sum of numbers of years - Calculation of depreciation using an example - Accounting - Methods of depreciation of fixed assets

In the classification of fixed assets included in depreciation groups, code Non-residential buildings can include objects such as warehouses, garages and industrial buildings, commercial retail buildings, buildings for entertainment events, hotels, restaurants, schools, hospitals, prisons, etc. Prison premises , colonies, pre-trial detention centers, barracks for prisoners, barracks for military personnel, dormitories of correctional and educational colonies, medical correctional institutions, schools and hospitals are considered as non-residential buildings, despite the fact that they may serve as a place of residence. The object of classification of this type of fixed assets is each individual building. If buildings are adjacent to each other and have a common wall, but each of them is an independent structural unit, they are considered separate objects. External extensions to the building that have independent economic significance, separate boiler house buildings, as well as outbuildings, warehouses, garages, fences, sheds, fences, wells, etc., are independent objects.

Correct depreciation calculation for buildings

It is generally accepted that the ratio of the cost of a building and accumulated depreciation deductions is the degree of its depreciation, but practice shows that in fact this is not always the case. The amount of depreciation payments is rather a mathematical and normative indicator, where there is some dependence on the useful life of buildings and structures. These deductions for the building will comply with legal standards only if the following parameters are correctly calculated:

- The final cost of assets related to fixed assets. It ultimately consists of the costs of purchasing and constructing buildings and all related operations (increases with additional valuation or completion).

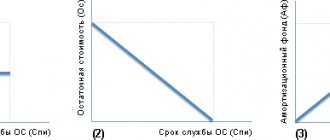

- The period of useful use of the depreciation object.

- The amount of depreciation on the building that was accrued before the transfer to the current owner.

- Method of calculating depreciation charges. Which, in turn, depends on the taxation system used and the legal form of the organization.

There are also additional parameters that affect depreciation deductions depending on the useful life of buildings and structures. These include:

- SPI increased through modernization and reconstruction. The additional amount of which the company calculates independently depending on the costs incurred. The useful life of a building that has been in use, on the contrary, can be reduced by the current owner.

- SPI increases due to major repairs and conservation for three months. No depreciation will be charged during this period.

To ensure that depreciation amounts do not raise questions among regulatory authorities, all additional information from the previous paragraphs must be entered into the building’s inventory card. To the question of what is the useful life of a brick building, the answer will be given by the classification of depreciation groups.

Depreciation calculation: basic provisions

Question: An organization purchased non-residential premises for an office on the first floor of a panel residential apartment building. To which depreciation group can this non-residential premises be classified for the purpose of calculating income tax? Answer: An office non-residential premises acquired by an organization, located on the ground floor of a panel residential apartment building, for the purposes of determining the useful life and calculating income tax, in our opinion, from January 1. Rationale: In tax accounting according to paragraph. The useful life is recognized the period during which an object of fixed assets serves to fulfill the goals of the taxpayer’s activities. The useful life is determined by the taxpayer independently on the date of commissioning of the depreciable property in accordance with the provisions of Art. The list of property that belongs to fixed assets is established by OKOF. Until January 1

We draw your attention to the Letter of the Ministry of Finance of Russia dated April 21. In it, employees of the financial department expressed the opinion that depreciation accrued on depreciable property not used by the taxpayer in activities aimed at generating income does not reduce the income received when calculating the tax base for corporate income tax. That is, if the apartment purchased by the organization is not occupied by seconded employees for some periods, then there is a high probability that the organization will not be able to take into account expenses in the form of accrued depreciation for these periods for profit tax purposes. The new procedure for writing off the value of fixed assets can only be applied to those objects that were acquired after January 1.

Depreciation in accounting: basics

The starting element in the methodology for calculating depreciation is the useful life (LPI) of real estate assets. It is installed following the data of the “Classification of fixed assets included in depreciation groups.” It operates in accordance with government decree in 2002. It is also necessary to take into account the changes made on 07/07/2016. Their action began in January of this year.

The SPI is the period during which the building is able to serve productively as an asset and contribute to the accomplishment of the taxpayer's objectives.

The enterprise determines it itself, based on the date the building was put into operation and information about the OS classification: (click to expand)

| OS groups (buildings incl.) | SPI (years) | |

| over | up to (inclusive) | |

| 4th | 5 | 7 |

| 5th | 7 | 10 |

| 7th | 15 | 20 |

| 8th | 20 | 25 |

| 9th | 25 | 30 |

| 10th | 30 | |

The buildings belong to the 4th and 5th, as well as to 7-10 groups. The enterprise independently determines which of them its real estate should be classified as. The characteristics of each set of buildings provide a clue.