How to calculate the average cost of an OS

Mathematically, the average annual value is the arithmetic average of the desired type of value of property assets

But sometimes you need accounting that will take into account not a fixed indicator for a certain period, but the moments of entry and exit from the balance sheet of fixed assets. Depending on this, the calculation method and formula for determining the average annual cost of fixed assets are selected

Method 1 (does not take into account the time of fund dynamics)

It provides average calculation accuracy, but in many cases it is quite sufficient.

To calculate the average annual cost of fixed assets, it is enough to know its value at the beginning and end of the annual period, that is, on January 1 and December 31 of the reporting year. These data are shown in the balance sheet. The residual value of the funds based on the balance sheet is used for the calculation.

If the residual value of the fixed assets at the end of the year has not yet been derived, it can be determined using the formula:

ST2 = ST1 + STpost. – ST list.

Where:

- ST2 – residual value of fixed assets at the end of the year;

- ST1 – the same indicator at the beginning of the year;

- STpost. – cost of received OS;

- STlist. – the cost of written-off fixed assets (removed from the balance sheet).

Then you need to find the arithmetic average of two indicators: ST1 and ST2, that is, the book value of the fixed assets at the beginning and end of the year. This will be the approximate value of the average annual cost of fixed assets.

STav.-year. = (ST1+ ST2) / 2

Method 2 (taking into account the month of placement on the balance sheet and deletion from the balance sheet)

This is a more accurate method; one of its varieties is used to calculate the tax base for paying property tax.

IMPORTANT! It is not permitted by law to use any other method of calculation for this purpose. With this calculation method, the number of months that have passed since the balance change (the adoption of a new operating system or the disposal of the old one) is taken into account.

Depending on the purpose, one of the following types of such calculation can be used

With this calculation method, the number of months that have passed since the balance change (the adoption of a new operating system or the disposal of the old one) is taken into account. Depending on the purpose, one of the following types of such calculation can be used

Formula for the average annual cost of fixed assets to assess the effectiveness of their use

To calculate capital productivity, capital intensity, profitability and other important indicators of the efficiency of the company's fixed assets, you need to know exactly how many full months have passed since the time the fixed asset was added or removed from the balance sheet. And, of course, you will need an initial cost indicator (as of January 1 of the reporting year) - ST1.

STav.-year.= ST1 + FMpost. / 12 x STpost. - ChMlist. / 12 x STspis

Where:

- ChMpost. – the full number of months from the date of putting the asset on balance sheet until the end of the current year;

- ChMlist. – the full number of months from the date the fixed assets are written off from the balance sheet until the end of the year.

Formula for the average annual cost of fixed assets based on the chronological average

It is considered the most accurate of the methods, which takes into account the entry and exit of fixed assets. It looks for the arithmetic average of the value of funds for each month, naturally, taking into account input and write-offs, if they occurred. The results are then added and divided by 12.

ST average-year = ((ST1NM + ST1KM) / 2 + (ST2NM + ST2KM) / 2 … + (ST12NM + ST12KM) / 2) / 12

Where:

- ST1NM – cost of fixed assets at the beginning of the first month of the year;

- ST1KM – cost of fixed assets at the end of the first month, and so on.

Formula for determining the average annual value of fixed assets for calculating corporate property tax

It is specifically provided exclusively for determining the property tax base. It applies the residual value indicator at the beginning of each month constituting the tax period. You will also need a final residual value at the end of the entire tax period. When we divide the resulting amount by the number of months, we will need to add 1 to the number that makes up the reporting period. That is, if you need to calculate the amount for an annual payment, you will need to divide by 13, and for quarterly payments, respectively, by 4, 7 , 10.

ST average-year = (ST1NM + ST2NM + … + ST12NM + STKNP) / 13

Where:

- ST1NM – indicator of the residual value of assets on the 1st day of the 1st month of the tax period;

- ST2NM – indicator of the residual value of assets as of the 1st day of the 2nd month of the tax period;

- ST12NM – indicator of the residual value of assets as of the 1st day of the last month of the tax period;

- STKNP – final residual value at the end of the tax period (its last date is December 31 of the reporting year).

5.How is the amount of property tax calculated at the end of the tax period?

The amount of tax payable to the budget at the end of the tax period is determined as the difference between the amount of tax calculated at the end of the tax period and the amounts of advance tax payments calculated during the tax period.

1. Name the special tax regimes provided for by the Tax Code of the Russian Federation.

1) taxation system for agricultural producers (unified agricultural tax);

2) simplified taxation system;

3) taxation system in the form of a single tax on imputed income for certain types of activities;

4) taxation system for the implementation of production sharing agreements;

5) patent taxation system.

2.What is the fundamental difference between special tax regimes and the general taxation regime?

The fundamental difference between all special tax regimes, including the simplified tax system, and the general regime is the replacement of the payment of a number of taxes with one tax. Differences in the procedure for paying taxes, submitting reports, and maintaining tax records. Specialist. tax regimes are aimed at reducing the tax burden for taxpayers, simplifying taxation and administration procedures.

3.

What types of taxes are exempted from a taxpayer who has been transferred to pay a single tax on imputed income?

Profit tax, property tax, VAT (except for VAT at customs), personal income tax and property tax for individuals

4. What is the object of taxation when applying the simplified taxation system?

you can choose the object of taxation: income or income reduced by the amount of expenses incurred

5. What are the tax rates if the object of taxation is:

- income

6%,

;

income reduced by expenses

15%

1. The concept of tax burden.

The totality of all tax obligations of a subject that affect the financial condition of the taxpayer

2. What are the indicators of the tax burden at the micro level, how are they calculated?

To calculate the tax burden on an organization, four indicators are used. The calculation of the first indicator is carried out according to the formula: Br = Np:B, where Np are taxes paid by the organization; B is the organization’s revenue. The second indicator is calculated using the formula: Br = Np:Pch, where Pch is the net profit remaining after taxes. The third indicator is determined by the formula: Br = Np: Ds, where Ds is added value, which, in turn, can be presented in the following form: Ds = Am + Zp + Np (Am - depreciation; Zp - labor costs ). Fourth indicator: Br = Нп:Св, where Св is the newly created value.

3. What are the general and specific disadvantages of the tax burden on an organization?

None of the presented indicators of the tax burden on organizations is universal, since the burden of direct and indirect taxes is distributed between the seller and the buyer depending on market fluctuations.

4.The essence of tax planning.

Tax planning is the choice of certain taxpayer actions permitted by law, aimed at optimizing taxation in order to reduce the tax burden.

5. Tax optimization, methods.

tax optimization is the actions of the taxpayer aimed at reducing the tax burden through methods permitted by law, such as, for example:

Tax benefits;

Special tax regimes;

Offshore zones;

Contractual methods;

Accounting policies, etc.

6. State the procedure for calculating the value of a patent.

Payment of the cost of a patent is made by the taxpayer at the place of registration with the tax authority in the following order:

If the patent was received for a period of up to six months - in the amount of the full amount of tax no later than 25 calendar days after the patent began to be valid;

If the patent is received for a period of six months to a calendar year:

In the amount of 1/3 of the tax amount - no later than 25 calendar days after the start of the patent;

In the amount of 2/3 of the tax amount - no later than 30 calendar days before the end of the tax period.

Option 2

1. Who sets property tax rates? Are there any restrictions on their size?

are established by the laws of the constituent entities of the Russian Federation and cannot exceed 2.2% of the tax base.

To determine the tax base when calculating property tax, it is necessary to reliably generate the average value of fixed assets for the reporting quarter and the average annual value of fixed assets for the tax period, which is a calendar year. In your case, you need to determine the average cost of fixed assets for half a year and 9 months as follows: to calculate for half a year, you need to determine the residual value for the dates 01.01, 01.02, 01.03, 01.04, 01.05, 01.06, 01.07; to calculate for 9 months, you need to determine the residual value for dates: 01.01, 01.02. 01.03, 01.04, 01.05, 01.06, 01.07, 01.08, 01.09, 01.10. The residual value of fixed assets is determined by subtracting from the book value of fixed assets the amount of accrued depreciation on the corresponding dates, that is, the debit balance on account 01 minus the credit balance on account 02. Next, you need to sum up the residual values of fixed assets formed on the dates and divide by the number of dates , which are taken for calculation, in the case of calculating the tax for six months, we sum up the residual values from 01.01 to 01.07 and divide by 7, in the case of calculating the tax for 9 months, we sum up the residual values from 01.01. to 01.10 and divide by 10. The resulting amount will be the taxable base for calculating property tax. Next, the tax base is multiplied by the property tax rate and divided by 4. Using this algorithm, advance payments for property tax payable for 1 quarter, half a year and 9 months are calculated. Regarding water transport facilities, the tax on which is paid at the place of their registration, we explain that when calculating property tax, their average annual value is calculated similarly, but is taken into account separately and reflected in the tax return for property tax, which is submitted at the place of their registration. When writing off fixed assets from the balance sheet of an organization, this operation is not reflected separately in the property tax return; it will be taken into account when determining the average annual cost of fixed assets by reducing the balance on accounts 01 and 02, after business transactions for writing off. The property tax rate is determined by each subject of the Russian Federation independently, but cannot exceed 2.2%. If the property is written off the balance sheet, but not deregistered with the state registration authorities, then property tax will have to be paid and declarations submitted in the usual manner.

- Tax and accounting changes in 2021

- Since 2021, a lot has changed in the work of accountants. Read about the latest changes in this section.

- New BCCs for insurance premiums and simplification were approved

- The rules for filling out field 101 in a payment order have changed.

- Insurance premiums were transferred to the tax authorities.

- New reporting has appeared - calculation of insurance premiums, SZV-STAZH and others.

- Now we need to confirm in a new way.

- I want to be aware of all changes >>

Lyubov Kotova answers,

Head of the Department of Legal Regulation of Insurance Premiums of the Department of Tax and Customs Policy of the Ministry of Finance of Russia

“Now on the title page of the calculation there are fields “Code according to OKVED”, “Number of working disabled people”, “Number of workers engaged in work with harmful and dangerous factors.” Previously, you indicated this data in section II. The new report form does not have either Section I or Section II. Instead there are six tables. How to fill them out? Read the recommendations. There you will also find a ready-made calculation example.”

The rationale for this position is given below in the materials of the Glavbukh System

Property tax is calculated and paid independently by:*

- Russian organizations;

- foreign organizations operating in Russia through permanent representative offices;

- foreign organizations that own real estate in Russia;

- foreign organizations that own real estate on the continental shelf and in the exclusive economic zone of Russia.

Calculation procedure

When calculating property tax, use the following algorithm: 1) determine the object of property tax; 2) check the availability and possibility of applying property tax benefits; 3) determine the tax base; 4) determine the tax rate; 5) calculate the amount of tax payable to the budget.

Object of taxation

For Russian organizations, the object of taxation is movable property recorded as part of fixed assets before January 1, 2013, and real estate, which is reflected in accounting as part of fixed assets (including objects transferred for temporary possession, use, disposal, trust management and joint activities). At the same time, movable property that was in use and accepted for accounting starting from January 1, 2013, is exempt from taxation, regardless of the fact that the previous owner also accounted for it as part of fixed assets. This follows from the provisions of paragraph 1 and subparagraph 8 of paragraph 4 of Article 374 of the Tax Code of the Russian Federation. The same conclusion can be drawn from letters of the Ministry of Finance of Russia dated March 11, 2013 No. 03-05-05-01/7108, dated February 25, 2013 No. 03-05-05-01/5322, dated February 18, 2013 No. 03-05-05-01/4307, dated February 7, 2013 No. 03-05-05-01/2766.

A similar composition of taxable objects is established for foreign organizations that have a permanent representative office in Russia. They are required to keep records of fixed assets according to the rules of Russian accounting, that is, in accordance with PBU 6/01. This procedure is established by paragraph 2 of Article 374 of the Tax Code of the Russian Federation.

Foreign organizations that do not have a permanent representative office in Russia are taxed only on real estate that is located on the territory of Russia (clause 3 of Article 374 of the Tax Code of the Russian Federation).

- property for which benefits are established;

- property that is not recognized as an object of taxation (land plots, natural resources, property of law enforcement agencies, etc.).

Such rules are established by paragraph 4 of Article 374 of the Tax Code of the Russian Federation.

Preferential property is excluded from the calculation of the tax base. Property that is not subject to taxation is not indicated on the tax return at all.*

The tax base

For Russian and foreign organizations with permanent representative offices in Russia, the tax base for property tax is:*

- average cost of fixed assets for the reporting period;

- average annual cost of fixed assets for the tax period.

Foreign organizations that do not have a permanent establishment in Russia must calculate tax based on the inventory value of real estate. This indicator is determined annually by the technical inventory authorities as of January 1. Before March 1, this information is sent to the tax inspectorates (clause 9.1 of Article 85 of the Tax Code of the Russian Federation, order of the Federal Tax Service of Russia dated February 11, 2011 No. ММВ-7-11/154). Technical inventory authorities are not required to provide payers with such information. Therefore, foreign organizations must independently find out the inventory value of real estate.

Such rules are established by paragraph 2 of Article 375 and paragraph 5 of Article 376 of the Tax Code of the Russian Federation.

Russian organizations determine the tax base separately in relation to:*

- property located at the location of the head office of the organization;

- property of each separate division with a separate balance sheet;

The tax base should be determined separately for property used within the framework of a simple partnership agreement (clause 1 of Article 377 of the Tax Code of the Russian Federation).

Foreign organizations determine the tax base separately in relation to:

- property located at the place of tax registration of each permanent establishment;

- each geographically remote property;

- property taxed at different tax rates.

Such rules are established by paragraph 1 of Article 376 of the Tax Code of the Russian Federation.

A special procedure for determining the tax base applies to real estate located on the territory of several constituent entities of the Russian Federation (pipelines, electrical networks, railways, etc.). In this case, the tax base must be determined separately. The share of the tax base that relates to a particular region should be calculated in proportion to the portion of the cost of the property located in the corresponding region. This is stated in paragraph 2 of Article 376 of the Tax Code of the Russian Federation.

Determining the average value of property

When calculating the average value of property for the reporting period, use the formula:*

When calculating the average annual value of property for the tax period, use the formula:*

Determine the residual value of the property using the formula:*

Determine the residual value of the property using accounting data.*

When determining the residual value of fixed assets at the end of the year, take into account transactions that influence the formation of this indicator and are reflected in accounting during December 31.

Such rules are established by paragraph 1 of Article 375 and paragraph 4 of Article 376 of the Tax Code of the Russian Federation and are explained in the letter of the Ministry of Finance of Russia dated July 14, 2010 No. 03-05-05-01/26.

An example of determining the average (average annual) value of property for calculating property tax. The organization operates during a full calendar year

CJSC "Alfa" is located in Moscow. The organization does not have real estate in other regions of Russia. According to accounting data, the residual value of fixed assets recognized as objects of property tax is:

- as of January 1 – 6,000,000 rubles;

- as of February 1 – RUB 5,950,000;

- as of March 1 – RUB 5,800,000;

- as of April 1 – RUB 5,750,000;

- on May 1 – 5,700,000 rubles;

- as of June 1 – RUB 5,650,000;

- as of July 1 – RUB 5,500,000;

- as of August 1 – RUB 5,450,000;

- as of September 1 – RUB 5,400,000;

- as of October 1 – RUB 5,350,000;

- as of November 1 – RUB 5,200,000;

- as of December 1 – RUB 5,150,000;

- as of December 31 – (taking into account transactions reflected in accounting during December 31) – RUB 5,100,000.

The average cost of property for the first quarter is equal to: (6,000,000 rubles + 5,950,000 rubles + 5,800,000 rubles + 5,750,000 rubles): (3 + 1) = 5,875,000 rubles.

The average property value for the first half of the year was:

5,500,000 rub.) : (6 + 1) = 5,764,285 rub.

The average cost of property for nine months was: (RUB 6,000,000 + RUB 5,950,000 + RUB 5,800,000 + RUB 5,750,000 + RUB 5,700,000 + RUB 5,650,000 + RUB 5,500,000 + RUB 5,450,000 + RUB 5,400,000 + RUB 5,350,000) : (9 + 1) = RUB 5,655,000

The average annual value of property for the year was: (6,000,000 rubles + 5,950,000 rubles + 5,800,000 rubles + 5,750,000 rubles + 5,700,000 rubles + 5,650,000 rubles: (12 + 1) = RUB 2,680,769

Situation: from what moment to calculate property tax do you need to take into account objects included in fixed assets (income investments in material assets) on the 1st day of the current month

Such objects should be included in the calculation of the average property value starting from the next month.

When determining the average value of property that is recognized as an object of taxation, indicators of the residual value of fixed assets are taken into account on the 1st day of each month of the reporting period and the 1st day of the month following the reporting period (clause 4 of Article 376 of the Tax Code of the Russian Federation). Since the basis for calculating property tax is accounting data (clause 1 of Article 374 of the Tax Code of the Russian Federation), these indicators must be formed in accordance with the established procedure for maintaining accounting and preparing financial statements.

The reporting date for the preparation of financial statements is the last calendar day of the reporting period (month, quarter, year) (clause 12 of PBU 4/99). That is, the reporting must contain information about all business transactions carried out for the period from the beginning of the year to this day inclusive. Business transactions performed starting from 00:00 the next day are not reflected in the reporting for the past period. Information about them is included in the reporting for the next reporting period.

Taking into account the above, fixed assets accepted for accounting on the 1st day of the current month are not included in the calculation of the residual value of the property for the previous month. Such objects are taken into account when calculating property tax only from the next month. For example, if the property was reflected in accounting as part of fixed assets on March 1, then its residual value should be taken into account when determining the average value of the property only starting from April 1.*

Similar clarifications are contained in the letter of the Ministry of Finance of Russia dated December 16, 2011 No. 03-05-05-01/97.

Property tax rate

The property tax rate is set by regional authorities within the maximum amount determined by Article 380 of the Tax Code of the Russian Federation - 2.2 percent. If tax rates have not been determined by regional authorities, the tax is calculated at the rates specified in paragraphs 1 and 3 of Article 380 of the Tax Code of the Russian Federation (clause 4 of Article 380 of the Tax Code of the Russian Federation). The maximum property tax rates are established, in particular, in Moscow and the Moscow region (Article 2 of the Moscow Law of November 5, 2003 No. 64, Art. 1 of the Moscow Region Law of November 21, 2003 No. 150/2003/OZ ). Organizations that have separate divisions with separate balance sheets or geographically distant real estate in different regions must apply the rates established in the corresponding regions when calculating property tax (Articles 384, 385 of the Tax Code of the Russian Federation).

Tax calculation by Russian organizations

The amount of advance payments for property tax for the reporting period by Russian organizations and foreign companies with permanent representative offices in Russia must be determined using the formula:*

The amount of property tax that is payable to the budget at the end of the year is determined by the formula:

This procedure is established by Article 382 of the Tax Code of the Russian Federation.

An example of calculating property tax by a Russian organization

CJSC "Alfa" is located in Moscow. The organization does not have real estate in other regions. The average value of fixed assets recognized as objects of property tax based on the results of reporting periods is equal to:

- for the first quarter RUB 205,000;

- for the first half of the year 190,000 rubles;

- for nine months 113,500 rubles.

The average annual value of property for the year is 160,000 rubles.

The amounts of advance payments for property tax accrued based on the results of the reporting periods are:

– for the first quarter: RUB 205,000. ? 2.2%: 4 = 1128 rubles;

– for the first half of the year: 190,000 rubles. ? 2.2%: 4 = 1045 rubles;

– for nine months: 113,500 rubles. ? 2.2%: 4 = 624 rub.

At the end of the year, Alpha transferred to the budget: 160,000 rubles. ? 2.2% – 1128 rub. – 1045 rub. – 624 rub. = 723 rub.

Preferential property

If an organization has privileged property, calculate the tax in a special manner.

The average (average annual) cost of preferential fixed assets must be calculated separately in column 4 of section 2 of the calculation of advance payments and column 4 of section 2 of the tax return, approved by order of the Federal Tax Service of Russia dated November 24, 2011 No. ММВ-7-11/895. This indicator is determined in the same manner as the average (average annual) value of property to which benefits do not apply.

Determine the amount of the advance payment for property tax that the organization enjoying the benefit must transfer to the budget using the formula:

This procedure is provided for in subclause 10 of clause 5.3 of the Procedure for filling out the calculation of advance payments, approved by order of the Federal Tax Service of Russia dated November 24, 2011 No. ММВ-7-11/895.

The amount of property tax that is payable to the budget at the end of the year is determined by the formula:

This procedure is provided for in subclause 3 of clause 4.2 and clause 5.3 of the Procedure for filling out the declaration, approved by order of the Federal Tax Service of Russia dated November 24, 2011 No. ММВ-7-1/895.

An example of calculating property tax by an organization entitled to a tax benefit

CJSC "Alfa" is registered in Moscow. The main activity is the production of pharmaceutical products. "Alpha" has a license for the production of veterinary immunobiological drugs. In addition, the organization rents out a building it owns. Equipment that is used in the production of veterinary immunobiological drugs is exempt from property tax (clause 4 of article 381 of the Tax Code of the Russian Federation). A leased building is part of fixed assets, so you must pay tax on its residual value.

The property tax rate in Moscow is 2.2 percent.

The residual value of all fixed assets of Alpha for the first quarter is:

- as of January 1 – 1,720,000 rubles;

- as of February 1 – 1,700,000 rubles;

- as of March 1 – 1,680,000 rubles;

- as of April 1 – RUB 1,660,000.

The residual value of equipment used in the production of pharmaceutical products is equal to:

- as of January 1 – 790,000 rubles;

- as of February 1 – 780,000 rubles;

- as of March 1 – 770,000 rubles;

- as of April 1 – 760,000 rubles.

The average cost of all Alpha property for the first quarter is: (1,720,000 rubles + 1,700,000 rubles + 1,680,000 rubles + 1,660,000 rubles): (3 + 1) = 1,690,000 rubles.

The average cost of the organization's preferential property for the first quarter is equal to: (790,000 rubles + 780,000 rubles + 770,000 rubles + 760,000 rubles): (3 + 1) = 775,000 rubles.

Based on the results of the first quarter, Alpha must transfer to the budget: (RUB 1,690,000 – RUB 775,000) ? 2.2%: 4 = 5033 rub.

E.Yu. Popova State Advisor of the Tax Service of the Russian Federation, 1st rank

2. Article:

Costs of official transport: from purchase to write-off

7.1.1. Objects of taxation

The types of vehicles on which transport tax must be paid are listed in paragraph 1 of Article 358 of the Tax Code of the Russian Federation. These include self-propelled land (cars, motorcycles, scooters, buses, etc.), air (airplanes, helicopters, and others) and water (motor ships, yachts, boats, motor boats, jet skis, and others) vehicles registered in the manner prescribed by law. .*

Some types of transport are exempt from tax. These include, in particular:

- rowing boats, as well as motor boats with engines up to 5 hp. With.;

- cars for disabled people;

- fishing sea and river vessels;

- tractors, self-propelled combines of all brands, special vehicles (milk tankers, livestock trucks, etc.) used by agricultural producers to produce agricultural products.

A complete list of tax-exempt types of vehicles is given in paragraph 2 of Article 358 of the Tax Code of the Russian Federation.

The table below will help you understand difficult situations when it is not clear whether to pay transport tax or not.

Controversial situations when it is not obvious whether a company should pay transport tax or not

| Situation | Should I pay tax or not? |

The property tax of organizations in the Russian tax system is one of the main ones established by federal legislation. The object of taxation is the funds present on the balance sheet of organizations. Payers of property tax are organizations operating on the territory of the country; tax is paid on property on the balance sheet of this organization. The tax period is considered to be a calendar year, in which there are three reporting periods: three, six and nine months. How is corporate property tax calculated? Transactions for the calculation and payment of taxes are presented below. How is tax paid? What is the object of taxation? Below you will find an example of calculating property taxes. What changes in the calculation of this tax occurred in 2014? We will look at the answers to these questions in the article below.

Formula for calculating property tax:

Taxpayers are organizations that own property. The funds of this organization are the object of taxation.

Formula:

Tax = tax base * tax rate / 100%

Tip 1: How to determine the average annual cost of fixed assets

D84 “Retained earnings (uncovered loss)” or 83 “Additional capital” K01 “Fixed assets” - the initial fixed assets were reduced; D02 “Depreciation of fixed assets” K84 “Retained earnings (uncovered loss)” or 83 “Additional capital” - the amount of depreciation charges has been reduced. D01 “Fixed assets” K83 “Additional capital” or 84 “Retained earnings (uncovered loss)” - the initial fixed assets have been increased; D83 “Additional capital” or 84 “Retained earnings (uncovered loss)” K02 “Depreciation of fixed assets” - the amount of depreciation charges has been increased.

What types of fixed asset values are subject to accounting?

The same fixed asset may have different values at a given time of acquisition and at different periods of operation. Other production factors may also affect the cost. To achieve the above goals, use the value of one of 4 types of value of the company's main assets.

The initial cost is the one at which the asset is placed on the balance sheet

It consists of: expenses incurred by the entrepreneur for the acquisition of an asset, its transportation to the place of operation, and, if necessary, installation work, setup, commissioning, etc.; those costs incurred by the entrepreneur if the asset was created by his own efforts; monetary valuation approved by all participants, if the fixed asset is the authorized capital or part thereof; the cost of the valuables that made up the exchange fund - during barter; valuation of the asset at market prices, current on the day of transfer - when donating a fixed asset. The original cost of fixed assets is taken into account when calculating property taxes and when accounting for depreciation. NOTE! The initial cost can be changed if the reason for the revaluation was a global change in the fixed asset (reconstruction, upgrade, completion, alteration, partial liquidation, etc.), as well as if the process of accounting revaluation has been officially initiated.

The replacement cost of fixed assets is a number that reflects how much the asset was worth at the time of its last revaluation. This can happen: if the property fund was reconstructed or otherwise changed, which affected the change in its primary value; the property was revalued; It turned out that a markdown of the asset was necessary.

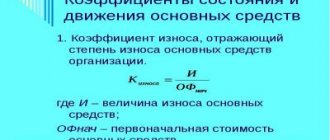

Residual value shows how much of the value of the fixed asset has not yet been transferred to the product

Essentially, this is the difference between the original (replacement) cost of the asset and the amount of depreciation. This indicator helps to understand how old the asset has already served its purpose, which directly affects the planning of updates to fixed assets, and therefore the financial indicators of costs.

Liquidation value reflects the financial “remainder” that remains attached to a fixed asset after its useful life has come to an end. An asset that has exhausted its depreciation does not always lose value to 0, most often there remains an amount for which it can be sold (for example, the useful life of a computer is 5 years, but even after this period it may well work properly and be sold for adequate amount).

Why do you need to calculate the average value of property?

Property (fixed assets) constantly changes its residual value, gradually transferring it to the products produced by the organization or the work performed or services provided. At the same time, their material, “material” form is preserved. Therefore, constant accounting and adjustment of their value in the balance sheet is necessary, which will reflect both the form of the asset and the amount of “transferred” value (depreciation).

In addition, since fixed assets (fixed assets) are dynamic, during the reporting period they can:

- change your qualitative state;

- get an “upgrade” and thereby increase the value;

- become obsolete physically and morally;

- change the total volume (the organization wrote off, sold or acquired property assets).

IMPORTANT!

It follows that at the beginning of the reporting year, the residual value of fixed assets may differ sharply from the indicators at the end of this period. That is why average values are used in calculations, which increases the accuracy and reliability of accounting and reflection of the value of funds on the balance sheet.

In addition to the immediate tasks of accounting, the value of the organization’s property, determined as the average value for the selected period, is used for taxation purposes. This indicator represents the taxable base for corporate property tax. On its basis, the amount of advance quarterly payments and the final annual payment is calculated (clause 1 of Article 375 of the Tax Code of the Russian Federation), it forms the basis of the declaration for this tax.

Average annual total book value of fixed assets - formula

To determine the average annual full accounting value of the PF, use the common complete formula:

Average annual full cost = (Full average annual cost as of 01.01 + Full average annual cost as of 31.12) / 2 + (Cost of introduced PF x Number of months of operation) / 12 – (Cost of retired PF x Number of months of disposal) / 12.

When calculating, all indicators are used at the original cost, which is added up at the time of acquisition in the relevant periods, unless revaluation has been carried out. If the company revalued its property, the value is taken as of the date of the last revaluation.

To determine the average value of property for calculating the tax on it, value indicators are taken at the beginning and end of the period. The calculation does not include months of asset disposal and commissioning. The following basic formula is applied:

Average cost = (Cost at the beginning of the period + Cost at the end of the period) / Number of months in the period.

For a year, the total number of reporting months is taken to be equal to the number 13, for 9 months - to the number 10, for a half-year - 7, for a quarter - 4. The indicators are taken from the balance sheet data. The calculation can be used to determine property tax or financial ratios - profitability, capital productivity, etc.

Results

The average and average annual cost of fixed assets, calculated from their residual value, are needed when determining the property tax base. The average cost is used in calculations for reporting periods, and the annual average is used when calculating the amount of tax for the year. The algorithms for determining them are identical: the residual value of the fixed assets is summed up for the first months of the period and on its last day, and then divided by the number of terms involved in the calculation. In this case, the zero values of the amounts must also be used.

Sources: Tax Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Most viewed words

- Strategic enterprise (organization)

- Release of products into circulation

- Engineering support networks

- Aircraft emergency

- Legitimacy of the document

- Public roads

- Total floor area

- Mobilization task

- Notice of entering a tax return (calculation) in electronic form

- Road maintenance

- Address certificate

- Crypto tool

- Industrial facility

- Information machines and equipment

- Interdepartmental request

- Production activities

- Production equipment

- Military personnel

- Post-production works

- Descent guide railway track

Analysis of the dynamics of the availability of fixed assets at the end of the reporting year at full accounting value

If, on the contrary, significant disposals occurred at the beginning of the year, and receipts at the end of the year, then the average annual value may in some cases be less than the value at the beginning and end of the year. If the average annual cost goes beyond the above-mentioned interval, appropriate explanations must be given in the annex to the form sent to the state statistics body.

- home

- DECREE of the State Statistics Committee of the Russian Federation dated December 27, 2002 N 225 “ON APPROVAL OF INSTRUCTIONS FOR FILLING OUT THE FEDERAL STATE STATISTICAL OBSERVATION FORM N 11 “INFORMATION ON THE AVAILABILITY AND MOVEMENT OF FIXED FUNDS (FUNDS) AND OTHER NON-FINANCIAL JSC TIVOV”

When and at what rates should organizations pay tax on OSNO?

The tax rate is set by the regions: it can be a single rate or differentiated rates depending on the category of taxpayer and type of property. There are limits for the rate - no more than 2.2%, unless Article 380 of the Tax Code of the Russian Federation establishes another limit.

For real estate that is assessed at cadastral value, regional rates apply. In 2021 and 2021, the limit for the tax rate is 2%.

Important ! If a region has not established its tax rates, we are guided by the Tax Code.

The tax period for payments is the same for everyone - 1 year. The declaration for the year must be submitted by March 30 (in 2021 - by April 1). The deadlines for advance payments and quarterly settlements are also set by the regions. The deadline is stated in Art. 386 of the Tax Code of the Russian Federation - the 30th day of the month following the reporting quarter.

Important ! In your region there may not be a division into reporting periods, then submit reports and pay tax once a year.

Who takes Form 11 (statistics)

All legal entities report on their fixed assets and other non-financial assets using Form No. 11. In this case, the type of activity, form of ownership and legal form do not matter. Even when working on the simplified tax system you will have to report.

Only non-profit organizations and small businesses fall under the exception. Also, consumer cooperation organizations, whose work is mainly costly, submit a report in Form No. 11 (short).

Organizations subject to bankruptcy proceedings submit the form in the general manner until they are liquidated.

Fixed assets renewal ratio: definition

Fixed assets of most enterprises are a component of property, which is characterized by such criteria as high cost and duration of use in the production sector. These assets, as means of labor, support the production process, participating in it directly (as production equipment) or indirectly (as premises, PCs, etc.). Therefore, the organization must maintain a normal state of fixed assets, which would continue to ensure the operation of the company and bring economic benefits.

This process can be ensured by reconstruction, technical re-equipment, major repairs of facilities, and replacement with more efficient and modern ones. This process is called updating the formatting object.

If the company is aimed at increasing capacity and expanding production, it begins to acquire new fixed assets, replenishing existing assets. The indicator that records the receipt and commissioning of acquired OS objects is the renewal coefficient.

Calculation of OS update intensity

It is not enough for an economist to calculate the OS renewal coefficient; it is necessary to assess the degree of intensity of operation of the introduced objects when replacing those that served previously. Intensity is calculated by the ratio of the amount of retired funds to the value of PF renewed throughout the year. The update intensity coefficient is calculated using the formula:

Kio = Svyb / Sofv

The optimal Kio value is less than 1. It shows the degree of release of capital for the acquisition of new fixed assets and indicates an expansion of the scale of production. An increase in the ratio indicates a reduction in the time of use of PF and the disposal of assets that have become unnecessary for the enterprise.

How to determine the average annual cost of fixed assets on the balance sheet in thousand rubles.

The balance sheet is an excellent source for determining and analyzing the return on assets.

The average annual value of property is often used for analysis. To do this, you need to take the figures recorded in Section I of the balance sheet under the line “Fixed assets”. For comparison, two years are taken, for example the reporting year and the previous one.

SGS = (Gotch + Gpred) / 2, where

Gotch - the cost of the OS at the end of the current year;

Gpred - the cost of the operating system at the end of the previous year.

Let's consider an example of calculating the GHS from the balance sheet. Auto-jazz LLC repairs premium cars. Auto-jazz has repair equipment on its balance sheet. The cost of the operating system on the balance sheet as of December 31, 2017 is 983,000 rubles, and as of December 31, 2018 - 852,000 rubles.

To get the GHS, we use the above formula:

GHS = (983,000 + 852,000) / 2 = 917,500 rubles.

Example of calculating property tax

Let us give an example of calculating corporate property tax based on the average annual cost.

Example condition

| Reporting date | Residual value (RUB) |

| As of 01/01/2017 | 2500000 |

| As of 02/01/2017 | 2225000 |

| As of 03/01/2017 | 2150000 |

| As of 04/01/2017 | 2700000 |

| As of 05/01/2017 | 2550000 |

| As of 06/01/2017 | 2400000 |

| As of 07/01/2017 | 2250000 |

| As of 08/01/2017 | 2100000 |

| As of 09/01/2017 | 1950000 |

| As of 10/01/2017 | 1800000 |

| As of 11/01/2017 | 1650000 |

| As of 12/01/2017 | 1500000 |

| As of 12/31/2017 | 1350000 |

Solution

Step 1. Calculate the average annual value of the property

(2500000 + 2225000 + 2150000 + 2700000 + 2550000 + 2400000 + 2250000 + 2100000 + 1950000 + 1800000 + 1650000 + 1500000 + 1350000)/13 = 20 RUR 86,538.46

Step 2. Calculate the annual tax amount

For our example, let's take the maximum property tax rate - 2.2%.

2086538.46 rub. x 2.2% = 45903.85 rub.

Since taxes are paid in full rubles (clause 6 of Article 52 of the Tax Code of the Russian Federation), the payer, taking into account rounding, must transfer 45,904 rubles to the budget. corporate property tax.

Step 3. Calculate the average value of the property to calculate the advance amount for the first quarter

(2500000 + 2225000 + 2150000 + 2700000)/4 = 2393750 rub.

Step 4. Calculate the advance payment for the first quarter

2393750/4 x 2.2% = 13166 rub.

Step 5. Calculate the average value of the property to calculate the amount of the advance for six months

(2500000 + 2225000 + 2150000 + 2700000 + 2550000 + 2400000 + 2250000)/7 = 2396428.57 rub.

Step 6. Calculate the advance payment for the six months

2396428.57/4 x 2.2% = 13180 rub.

Step 7. Calculate the average value of the property to calculate the amount of advance payment for 9 months

(2500000 + 2225000 + 2150000 + 2700000 + 2550000 + 2400000 + 2250000 + 2100000 + 1950000 + 1800000)/10 = 2262500 rub.

Step 8. Calculate the advance payment for 9 months

2262500/4 x 2.2% = 12444 rubles.

Step 9. Calculate the amount of tax to be paid additionally to the budget at the end of the year

45904 - (13166 + 13180 + 12444) = 7114 rubles.

In our state, with the correct process of accounting, as well as for compliance with tax standards for organizations, a significant role is played by the regulation of the value of tangible and intangible assets that are exploited in the economic activities of the enterprise and are on its independent balance sheet. In application of Part 1 of Art. 375 of the Tax Code of the Russian Federation, in order to establish the taxable base, it is necessary to calculate the average annual value of property, provided that the calculation of the enterprise property tax is not carried out at the cadastral value.

How to calculate the average annual accounting value of fixed assets

To understand how to calculate the average annual total book value of fixed assets, it is necessary to consider the differences between the total indicator and the average. The latter is calculated without taking into account the dates of disposal or, conversely, commissioning of assets - the values at the beginning and end of the period are important here. Additionally, the number of months in a given reporting period (to calculate advance payments) and tax period (to calculate the final amount of tax liabilities for the year) is used as a denominator.

The methodology for calculating the average annual full accounting value of fixed assets/assets makes it possible to obtain a more detailed, in-depth understanding of the price. In this case, the value at the beginning of the year is taken from the company’s balance sheet, and then this value is adjusted to the average indicators of retired and put into operation property. In accordance with clause 24 of Section I of Order No. 563, the calculation of the average full accounting value of fixed assets for the year is carried out by dividing by 12 months. the sum of half of the incoming and outgoing costs, taking into account the revaluations made in this period and the cost of the fixed assets at the beginning of each of the remaining months, taking into account the depreciation. If the business is liquidated, the calculation is still made for the year as a whole. The same procedure applies to organizations formed in the middle of the year. In this case, the periods are rounded to full months and, accordingly, the cost indicators of the PF are taken. To understand the essence of this issue, let us turn directly to the formulas and examples.

Average annual cost of OPF: formula for calculating the balance sheet

To determine the indicator, it is necessary to use the data that is present in They must cover transactions not only for the period as a whole, but also separately for each month. How is the average annual cost of open pension fund determined? The balance formula used is as follows:

X = R + (A × M) / 12 - / 12, where:

- R - initial cost;

- A is the value of the introduced funds;

- M is the number of months of operation of the introduced OPF;

- D is the liquidation value;

- L is the number of months of operation of retired funds.

Calculation of average values of the cost of fixed assets for non-production purposes

In addition to production fixed assets, enterprises often have fixed assets intended for transfer to tenants for use. They are taken into account on the account. 03 “Profitable investments in assets”, and their cost is indicated in line 1160 in the original price and its average value can be calculated from the balance sheet in the same way as the average cost of fixed assets:

SGSdv = (BSn + BSk) / 2

or taking into account the receipts and disposals of such objects, using in the calculation both information from the balance sheet and data from accounting registers:

SGSdv = BSn + (P x M1) / 12 – (B x M2) / 12.

If during the year objects of profitable fixed assets were put into operation or retired, then the second formula is involved in the analysis of the efficiency of use of this property.

When an analyst is faced with the task of calculating the total amount of fixed assets in a company, the data from lines 1150 and 1160 are combined.

How to calculate the amount of tax payable

According to cadastral value

If you pay tax based on cadastral value, first request the value of the property as of January 1 of the reporting year from the Rosreestr office.

If you own a premises, and Rosreestr gave you information only on the cost of the building, calculate the cadastral value of the premises as a share of the entire building by area.

You will also need a coefficient (K) - the ratio of months of ownership (full and incomplete) to the number of months in the reporting period. Let's say you owned the premises from May to the end of the year, then K = 8/12. Now calculate the tax amount:

Tax amount = Cadastral value × Tax rate × K

Example. Ochkarik LLC owns premises in the administrative building. The cadastral value of the premises has not been determined, but it is known that it occupies ¼ of the building's area. According to a certificate from Rosreestr, the cadastral value of the building as of January 1, 2018 is 23 million rubles.

Cadastral value of the premises = 23 million rubles / 4 = 5,750 thousand rubles.

The tax amount for the year is 5,750 thousand rubles × 2.2% = 126,500 rubles.

Advance payments will be 126,500: 4 = 31,625 rubles per quarter.

At average annual cost

The tax amount is calculated based on the residual value of the property. Advance payments must be made quarterly. Let's look at the calculation of tax based on the average annual cost using an example.

Example. Alpha LLC owns a packaging tape with an initial cost of 440,000 rubles. The average annual cost of the tape (we calculated above) was 380,000 rubles.

The amount of tax to be paid is 380,000 rubles × 2.2% = 8,360 rubles.

Let's calculate advance tax payments:

1st quarter:

- Tax base = (440,000 + 430,000 + 420,000 + 410,000): (3+1) = 425,000 rubles.

- Advance payment = 425,000 × 2.2%: 4 = 2,337.5 rubles.

2nd quarter:

- Tax base = (440,000 + 430,000 + … + 390,000 + 380,000): (6+1) = 410,000 rubles.

- Advance payment = 410,000 × 2.2%: 4 = 2,255 rubles.

3rd quarter:

- Tax base = (440,000 + 430,000 + … + 360,000 + 350,000): (9+1) = 395,000 rubles.

- Advance payment = 395,000 × 2.2%: 4 = 2172.5 rubles.

Final payment:

Additional payment = 8,360 − 2,337.5 − 2,255 − 2,172.5 = 1,595 rubles.

Why it is necessary to consider the value of fixed assets

This is not only about the fact that accounting of fixed assets is required by the current legislation and the authorities controlling the entrepreneur. Constant monitoring of the value of fixed assets helps solve many pressing problems:

- clarification of costs associated with the acquisition of assets, as well as the integration of this information into the system;

- accurate tracking of operations based on the dynamics of fixed assets, since all changes are reflected in the documentation;

- assessment of the operating efficiency of each group of fixed assets;

- financial results of the loss of fixed assets (sales, disposal, write-off, etc.);

- obtaining various types of information about fixed assets, necessary not only for reporting, but also for internal awareness and analysis.

Tags: asset, balance sheet, accountant, inventory, capital, coefficient, tax, expense, means, formula

Capital-labor ratio

The capital-labor ratio reflects the security of workers

enterprise fixed assets and is calculated using the following formula:

Capital-labor ratio = Average annual cost of fixed assets / Average number of employees.

It is possible to draw conclusions about changes in this indicator only if it is linked to the value of labor productivity. If the growth rate of labor productivity lags behind the growth rate of the capital-labor ratio, this indicates an irrational use of the enterprise's resources. Perhaps we are talking about the large number of the organization’s management apparatus or the unmotivated growth of the passive part of fixed assets.

Analysis of these three simple indicators will allow you to promptly recognize problems that threaten the profitability of the enterprise and find ways to eliminate them.

On this page:

For accounting and tax collection and payment purposes, it is necessary to constantly monitor the book value of the organization’s property. For some important taxes, such as, for example, the key is the average value of fixed assets for the reporting period, and for filing a return for this tax - for the year.

Let's look at the nuances of calculating the average value of property based on the latest legislative acts, give formulas, and look at how this is done using specific examples.