Patent Eligible Businesses

The patent taxation system (PTS) applies only to individual entrepreneurs: LLCs and cannot use patents.

There are strictly defined businesses that fall under it. Individual entrepreneurs on a patent can carry out the following types of activities for 2018:

- activities for the repair and sewing of leather and fur products, as well as clothing;

- shoe repair, painting, cleaning and sewing business;

- provision of hairdressing and cosmetic services;

- dry cleaners and laundries;

- activities related to the production of street signs, keys and other metal haberdashery;

- maintenance and repair of household appliances and manufacturing of metal products;

- activities related to road freight transportation;

- activities related to the transportation of passengers;

- renovation of apartments, houses and other buildings;

- provision of welding, installation, electrical and plumbing services;

- entrepreneurial activity in cutting mirrors and glass, glazing work on loggias and balconies and artistic glass carving;

- organization of reception of non-ferrous metal and glassware (but not scrap metal);

- provision of veterinary services;

- delivery of non-residential and residential premises, land plots, summer cottages owned by individual entrepreneurs;

- creation of folk arts and crafts;

- other production services (woodworking, grain peeling, hide dressing, fencing manufacturing, boat manufacturing, and so on);

- restoration and production of carpets;

The list is quite long.

The most common patents are a patent for cargo transportation for individual entrepreneurs, and a patent for individual entrepreneurs, the purpose of which is retail trade of certain goods.

back to menu ↑

Patent for individual entrepreneurs in 2021: permitted types of activities + answers to frequently asked questions about changes

Good afternoon, dear individual entrepreneurs!

I started collecting summary data on changes for individual entrepreneurs on PSN for 2020.

I would like to emphasize right away that the article will be updated as new laws and other changes for the PSN are approved. And there will be many changes, especially related to mandatory labeling. Therefore, it is better to immediately subscribe to blog news so as not to miss important changes:

Also watch short video reviews on these important innovations, which are in the article below. I specifically wrote them down, since the same questions are asked from readers =) Therefore, before asking questions, look at them carefully.

What will change in 2021?

Yes, changes are already being prepared for 2021 for individual entrepreneurs on PSN. Even though 2021 has not yet begun, I brought this news here because it is very important.

The most important. It will be prohibited to use PSN when trading three groups of goods that are subject to mandatory labeling

Here, be more careful, since a law has already been adopted that prohibits for individual entrepreneurs on PSN (and for UTII, by the way, too) the trade of three groups of goods that are subject to mandatory labeling:

- medicines;

- footwear goods;

- items of clothing and accessories made of natural fur.

This restriction comes into force on January 1, 2021. I wrote a separate note about this very important change:

A law banning trade for PSN and UTII in goods that are subject to mandatory labeling (but not all) has been adopted

I also recommend watching a short video on this issue:

That is, if you trade (or are going to trade) three groups of goods that are subject to mandatory labeling, you will have to apply a different tax system.

Two more important changes

- The rules for calculating the PSN tax have changed.

- The maximum number of hired employees for individual entrepreneurs on PSN, which combines a patent with other tax systems, is being clarified

Let me remind you that for a long time they wrote and said that for an individual entrepreneur with a patent, the average number of employees should not exceed 15 people. Even if there is a combination with other tax systems (for example, simplified tax system + PSN).

But in the fall of 2021, an interesting letter from the Ministry of Finance dated September 20, 2021 N 03-11-12/67188 appeared, in which it was reported that for individual entrepreneurs on the simplified tax system + PSN there may be more than 15 hired employees. Provided that separate records are maintained and no more than 15 people work in the activity for which the patent was purchased.

Now this rule is spelled out in the Tax Code of the Russian Federation.

Read more about these two changes here:

What else will change for individual entrepreneurs on a patent?

Dear readers, I have a separate section for individual entrepreneurs on a patent, which I also advise you to look at, since in it I talk about other nuances of applying this tax system:

So, let's move on to the main topic of this article.

Individual entrepreneurs who want to minimize reporting to the Federal Tax Service, as a rule, choose a patent tax system. Indeed, reporting for individual entrepreneurs on PSN is minimal compared to other taxation systems.

This system is also most understandable for novice entrepreneurs.

But there is also bad news - the fact is that it is not possible to choose a PSN for any type of activity. This list of activities is quite short and currently consists of 63 activities.

What types of activities are available for the transition of an individual entrepreneur to PSN?

- Firstly, this list is indicated in the Tax Code of the Russian Federation (Article 346.43) and contains 63 types that are allowed throughout Russia.

- Secondly, local authorities can add additional types of activities that are permitted in the constituent entity of the Russian Federation. For example, at the beginning of 2021, Moscow allowed the purchase of patents for those individual entrepreneurs who are engaged in vending (that is, selling through vending machines). Therefore, check the list of current activities for individual entrepreneurs on a patent for 2021 at your tax office. Or look for changes to the relevant laws for individual entrepreneurs on PSN on the official websites of local authorities.

Let's consider the first list, which is specified in Article 346.43 of the Tax Code of the Russian Federation

- Repair and sewing of clothing, fur and leather products, hats and textile haberdashery products, repair, sewing and knitting of knitwear;

- Repair, cleaning, painting and sewing shoes;

- Hairdressing and beauty services;

- Dry cleaning, dyeing and laundry services;

- Manufacturing and repair of metal haberdashery, keys, license plates, street signs;

- Repair and maintenance of household radio-electronic equipment, household cars and household appliances, watches, repair and manufacture of metal products;

- Furniture repair;

- Services of photo studios, photo and film laboratories;

- Maintenance and repair of motor vehicles and motor vehicles, machinery and equipment;

- Provision of motor transport services for the transportation of goods by road;

- Provision of motor transport services for the transportation of passengers by road;

- Repair of housing and other buildings;

- Services for installation, electrical, sanitary and welding works;

- Services for glazing balconies and loggias, cutting glass and mirrors, artistic glass processing;

- Services for training the population in courses and tutoring;

- Services for the supervision and care of children and the sick;

- Services for receiving glassware and secondary raw materials, with the exception of scrap metal;

- Veterinary services;

- Leasing (hiring) of residential and non-residential premises, dachas, land plots owned by an individual entrepreneur by right of ownership;

- Production of folk arts and crafts;

- Other production services (services for processing agricultural products and forest products, including grain grinding, peeling cereals, processing seed oil, making and smoking sausages, processing potatoes, processing customer-supplied washed wool into knitted yarn, dressing animal skins, combing wool , grooming of domestic animals, repair and production of cooper's ware and pottery, protection of gardens, vegetable plots and green spaces from pests and diseases; production of felted shoes; production of agricultural implements from customer's material; engraving work on metal, glass, porcelain, wood, ceramics; production and repair of wooden boats; repair of toys; repair of tourist equipment and inventory; services for plowing vegetable gardens and sawing firewood; services for repair and production of eyeglasses; production and printing of business cards and invitation cards for family celebrations; binding, stitching, edging, cardboard work; charging gas cartridges for siphons, replacing batteries in electronic watches and other devices);

- Production and restoration of carpets and rugs;

- Repair of jewelry, costume jewelry;

- Chasing and engraving of jewelry;

- Monophonic and stereophonic recording of speech, singing, instrumental performance of the customer on magnetic tape, CD, dubbing of musical and literary works on magnetic tape, CD;

- Residential cleaning and housekeeping services;

- Residential interior design and decoration services;

- Conducting physical education and sports classes;

- Porter services at railway stations, bus stations, air terminals, airports, sea and river ports;

- Paid toilet services;

- Services of chefs for preparing dishes at home;

- Providing services for the transportation of passengers by water transport;

- Providing services for the transportation of goods by water transport;

- Services related to the marketing of agricultural products (storage, sorting, drying, washing, packaging, packing and transportation);

- Services related to the maintenance of agricultural production (mechanized, agrochemical, land reclamation, transport work);

- Green farming and decorative floriculture services;

- Management of hunting and hunting;

- Engagement in medical activities or pharmaceutical activities by a person licensed for these types of activities;

- Carrying out private detective activities by a licensed person;

- Rental services;

- Excursion services;

- Ritual services;

- Funeral services;

- Services of street patrols, security guards, watchmen and watchmen;

- Retail trade carried out through stationary retail chain facilities with a sales floor area of no more than 50 square meters for each trade facility;

- Retail trade carried out through stationary retail chain facilities that do not have sales floors, as well as through non-stationary retail chain facilities;

- Catering services provided through public catering facilities with a customer service area of no more than 50 square meters for each catering facility;

- Catering services without a customer service area;

- Services for slaughter, transportation, distillation, grazing;

- Production of leather and leather products;

- Collection and procurement of plants, including medicinal ones;

- Drying and processing of fruits and vegetables;

- Production of dairy products, bakery products;

- Production of fruit and berry planting materials, growing vegetable seedlings and grass seeds;

- Production of bakery and flour confectionery products;

- Commercial and sport fishing and fish farming;

- Silviculture and other forestry activities;

- Translation and interpretation activities;

- Activities caring for the elderly and disabled;

- Collection, processing and disposal of waste, as well as processing of secondary raw materials;

- Cutting, processing and finishing of stone for monuments;

- Provision of services (performance of work) for the development of computer programs and databases (software and information products of computer technology), their adaptation and modification;

- Repair of computers and communication equipment;

In addition to restrictions on types of activities, an individual entrepreneur must fulfill several more conditions:

- The average number of employees should NOT exceed 15 people;

- Income during a calendar year should not exceed 60 million rubles;

How much does a patent cost for 2021?

The official calculator from the Federal Tax Service has been in operation for a long time, where you can quickly calculate the cost of a patent. Read about how to use it here:

https://dmitry-robionek.ru/soft-for-biz/kalkulator-cena-patenta-ip-fns.html

I note that data for 2021 in the official calculator should appear around December 2021 (this was the case in previous years).

How to switch to PSN?

In order to switch to PSN, you must submit an application to the Federal Tax Service in 10 working (not calendar!) days in accordance with form No. 26.5-1.

Please note that changes to this application are currently being prepared and it is better to take the current form from the official website of the Federal Tax Service.

https://www.nalog.ru/rn77/ip/ip_pay_taxes/patent/#title5 (this same link has a lot of other useful information for individual entrepreneurs on PSN)

Update. Please note that a new patent form has been introduced starting in 2021. Read more in a separate article:

The new patent application form 26.5-1 is valid from September 29, 2021

Where exactly should this application be submitted? Which inspection?

- If the activities of an individual entrepreneur will be carried out at the place of residence (i.e. according to registration in the passport), then we submit an application to our “native” tax office;

- But if vigorous activity takes place in another region (not at the place of registration), then we submit an application at the place of future activity (this is important);

Is it possible to combine PSN with other taxation systems?

Yes, you can. For example, you can combine simplified taxation system + PSN. But here it is worth remembering that you will have to report according to two taxation systems at once. It is clear that a declaration cannot be submitted under the PSN, but under the simplified tax system you will have to submit it, even if it is zero.

For those who combine simplified taxation system + PSN, I highly recommend reading the following articles:

- Should an individual entrepreneur with a patent submit an annual declaration? And if there is a combination of simplified taxation system + PSN?

- At what annual income does an individual entrepreneur using the simplified tax system + PSN lose the right to apply a patent?

Important point

You also need to take into account the fact that by purchasing a patent, you are not automatically removed from the previous taxation system.

For example, you are an individual entrepreneur on the simplified tax system of 6% and bought a patent.

This means that you began to combine the simplified tax system 6% + PSN. This means that you will have to report both under the simplified tax system 6% and under the PSN. To avoid this hassle, you will have to deregister according to the simplified tax system (which is possible only from January 1, upon application). But, in fact, there is no need to give up the simplified taxation system, since if you lose the right to use the simplified taxation system, you will be forced to use the simplified taxation system, which is better than the special taxation system.

How to pay for a patent in 2021?

According to Article Article 346.51 of the Tax Code of the Russian Federation:

- If the patent was received for a period of up to six months - in the amount of the full amount of tax no later than the expiration date of the patent;

- If a patent is purchased for a period of 6 to 12 months, then payment occurs in 2 stages:

- in the amount of one third of the tax amount no later than ninety calendar days after the patent begins to be valid;

- in the amount of two-thirds of the tax amount no later than the expiration date of the patent.

What happens if the patent term is not extended on time?

One of the main concerns of the individual entrepreneur on the PSN was to extend the validity of the patent for the next period in time. If someone did not have time to do this within the prescribed period, then it was believed that the individual entrepreneur automatically began to apply the GST (general taxation system). In the case of combining the simplified tax system + PSN, the entrepreneur “flew” to the simplified tax system.

Fortunately, this practice has been canceled since 01/01/2017, as reported in the information letter from the Federal Tax Service No. SD-19-3/ [email protected] dated 02/06/2017

Read more here:

Is it possible to return money for a patent if the individual entrepreneur is closed and the patent has not expired?

Quite a common question that regularly appears in the comments. I’ll put it in a separate note, it will be more convenient.

So, if an individual entrepreneur on PSN is deregistered as an individual entrepreneur and winds down his activities, then you can return the money for a patent that has not expired. This is reported in the letter of the Ministry of Finance dated March 1, 2021 N 03-11-09/13546.

Read more here:

What if I terminated my patent activities ahead of schedule?

Individual entrepreneurs on PSN who cease operations often have questions about the return of money that was paid for the patent. Of course, the question arises if the activity is terminated before the patent expires.

Read the answer to this question here:

Is it possible to use PSN for an online store?

No you can not. This question is so common that I had to write a separate article on this subject:

https://dmitry-robionek.ru/im/kakuju-sistemu-nalogooblozhenija-vybrat-dlja-internet-magazinaija.html

IP contributions for 2021

I made a new video about individual entrepreneurs’ contributions “for themselves” for 2021, I advise you to watch:

I remind you that you can subscribe to my video channel on Youtube using this link:

https://www.youtube.com/c/DmitryRobionek

How to calculate 1% of an amount exceeding 300,000 rubles of annual income for an individual entrepreneur on PSN?

Questions are also very often asked about how to calculate 1% with an income of over 300,000 rubles per year.

Read the answer here:

How to calculate 1% of an amount exceeding 300,000 rubles of annual income for an individual entrepreneur on PSN?

How to calculate the contributions of an individual entrepreneur “for himself” if the individual entrepreneur worked for less than a full year?

I have a calculator for individual entrepreneur contributions for 2021.

You can do the math, just read the instructions carefully, please. Or watch this short video:

Preliminary result:

I repeat once again that this article is summary and will be updated with new details as new changes become available.

Best regards, Dmitry Robionek

Receive the most important news for individual entrepreneurs by email!

Stay up to date with changes!

By clicking on the “Subscribe!” button, you consent to the newsletter, the processing of your personal data and agree to the privacy policy.

Dear readers!

A detailed step-by-step guide to opening an individual entrepreneur in 2021 is ready. This e-book is intended primarily for beginners who want to open an individual entrepreneur and work for themselves.

This is what it's called:

“How to open an individual entrepreneur in 2021? Step-by-Step Instructions for Beginners"

From this manual you will learn:

- How to properly prepare documents for opening an individual entrepreneur?

- Selecting OKVED codes for individual entrepreneurs

- Choosing a tax system for individual entrepreneurs (brief overview)

- I will answer many related questions

- Which supervisory authorities need to be notified after opening an individual entrepreneur?

- All examples are for 2021

- And much more!

Find out the details!

Dear readers!

I analyzed all the questions that were asked to me over 8 years of blogging. And I selected the TOP 70 most frequent questions that almost all beginning entrepreneurs ask.

The book is small, reading time will be approximately 1 hour. In fact, I answer them in this small e-book. And it's called like this:

“Answers to the most frequently asked questions from start-up entrepreneurs without employees”

More about the book

Dear readers, a new e-book for individual entrepreneurs is ready for 2021:

“Individual Entrepreneurs on the simplified tax system 6% WITHOUT Income and Employees: What Taxes and Insurance Contributions must be paid in 2021?”

This is an e-book for individual entrepreneurs on the simplified tax system of 6% without employees who have NO income in 2021. Written based on numerous questions from individual entrepreneurs who have zero income and do not know how, where and how much to pay taxes and insurance premiums.

Find out the details!

Dear entrepreneurs!

A new e-book on taxes and insurance contributions for individual entrepreneurs on the simplified tax system of 6% without employees is ready for 2021:

“What taxes and insurance premiums does an individual entrepreneur pay under the simplified tax system of 6% without employees in 2021?”

The book covers:

- Questions about how, how much and when to pay taxes and insurance premiums in 2021?

- Examples for calculating taxes and insurance premiums “for yourself”

- A calendar of payments for taxes and insurance premiums is provided

- Frequent mistakes and answers to many other questions!

Find out the details!

Conditions that must be met to switch to PSN

PSN is a special tax regime for small businesses. To obtain the right to work under PSN, you must fulfill a number of requirements:

- Only persons engaged in individual entrepreneurship can work under a patent. The issue of the possibility of an organization purchasing a patent has been discussed many times, but no precedent has ever been reached. LLCs can take advantage of the alternative tax system. Her name is UTII.

- An individual entrepreneur cannot employ more than 15 people. In this case, not only employees engaged in activities that are in the list of PSN are considered, but also other tax systems. For example, if a person carries out entrepreneurial activities on the simplified tax system and already employs 10 people, then when purchasing a patent he will be able to hire no more than 5 employees to his enterprise.

- The maximum amount an individual entrepreneur can earn on a patent is 60 million rubles. When combining PSN with other types of tax regimes, the income is summed up.

back to menu ↑

How to obtain a patent at the same time as registering an individual entrepreneur

And now, as promised, we’ll tell you about obtaining a patent when opening an individual entrepreneur. This opportunity is provided by Article 346.45 of the Tax Code of the Russian Federation: “If an individual plans, from the date of his state registration as an individual entrepreneur, to carry out business activities on the basis of a patent in a constituent entity of the Russian Federation, on the territory of which such person is registered with the tax authority at his place of residence , the application for a patent is submitted simultaneously with the documents submitted for state registration as an individual entrepreneur .”

From this norm it becomes clear that the main condition for obtaining a patent when registering an individual entrepreneur is to conduct business on a PSN in the same subject of the Russian Federation where the entrepreneur is registered.

In letter dated 01/09/2014 No. SA-4-14/69, the Federal Tax Service developed special regulations for the simultaneous acceptance of form P21001 and a patent application:

- The registering tax inspectorate, upon receipt of documents from the applicant, is obliged no later than 11 a.m. on the next working day to send an application for a patent to the inspectorate at the place of activity.

- Within the period established by law (on the fourth working day after receiving the documents), the registration inspectorate informs the Federal Tax Service, where the patent application was previously submitted, of its decision to register the individual entrepreneur or to refuse it.

- If the entrepreneur is successfully registered, the Federal Tax Service at the place of business must issue a patent or a notice of refusal within five days. In the first case, the patent begins to be valid from the date of registration of the individual entrepreneur. In the second, the inspection must provide the reason for the refusal.

Patent cost

Before you decide to purchase, you need to calculate the cost of a patent for an individual entrepreneur for 2021 and conduct a comparative analysis of the obtained price with other systems, such as UTII and the simplified tax system.

PSN differs from other systems in that its tax calculation is based on potential rather than actual income.

In other words, when calculating the tax, the state proceeds from how much revenue an entrepreneur can receive by engaging in specific activities in a specific region.

The amount of possible income is determined based on the laws of the region, so a patent in two different areas may cost differently. Sometimes this difference reaches several times.

For example, a hairdresser in Moscow brings in up to 990 thousand rubles per year, and in Kaluga and the Kaluga region - 270 thousand rubles.

This difference consists of differences in the number of clients and the pricing policy of the city.

In addition, you should take into account the impact of physical indicators on the final cost of purchasing a patent for individual entrepreneurs for 2021.

We are talking about how many retail outlets, employees, vehicles are used in the enterprise, etc.

Now let's summarize the above. So, let's go!

To calculate the amount of tax on PSN and decide whether it is worth buying a patent, you need to understand what potential income you can count on when doing your chosen business.

It's best to understand this with an example. Let's take the necessary information from Moscow City Duma Law No. 53 of October 31, 2012 and calculate the patent for individual entrepreneurs.

back to menu ↑

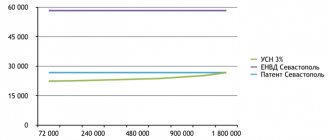

Tax rate and patent value

The tax rate on PSN in Russia is 6%. In Sevastopol, rates are lower, and in the regions a 0% rate may be set - the so-called tax holiday.

Individual entrepreneurs who have registered activities in the scientific, industrial and (or) social spheres, as well as in the spheres of consumer services to the population, have the right to tax holidays. And such a benefit can be applied for no more than two tax periods continuously within two calendar years. The tax period in this case is the period of validity of the patent, not exceeding a calendar year.

The cost of a patent is actually a tax, but paid in advance.

To avoid doing the math yourself, you can use a calculator to calculate the cost of a patent on the tax website, where you need to indicate the region, type of activity and period for which you are purchasing the patent.

Don't forget about insurance premiums. The fees are paid in addition to the cost of the patent, without reducing this value. They are calculated in the same way as on the simplified tax system. Moreover, in order to calculate 1% on an amount exceeding 300 thousand, you take into account not the actual income received, but the amount of potential income.

Calculation example

Let's look at several ways in which you can calculate the cost of an individual entrepreneur patent for 2021.

The first method is to use a special calculator developed by the Federal Tax Service. It can be easily found on the Internet.

Let's calculate how much you will need to pay to acquire a patent to provide hairdresser services in the capital for six months.

We enter into the calculator the validity period of the patent, what activity we plan to engage in and the place where we are going to carry out the activity.

After the data is entered, all you have to do is click “Calculate”. In total, for this case, you will need to pay 29,700 rubles. tax

The terms of payment for a patent depend on the amount of the payment made:

- if the payment made is 9,900 rubles, then it must be paid no later than 90 days from the moment the patent came into effect;

- if the payment made is 19,800 rubles, then it must be paid before the patent expires.

back to menu ↑

When is it more profitable to buy a patent?

Dividing 29,700 by the number of months in a half-year (6), we get that 4,950 rubles will need to be transferred to the budget monthly.

A Moscow hairdresser can earn it in a day. However, it must be taken into account that the amount of insurance premiums paid by an entrepreneur does not affect the size of the final tax burden.

Such benefits can only be obtained on the simplified tax system and UTII. On the simplified tax system, this benefit is expressed in the difference between income and expenses; insurance premiums are considered expenses, thus reducing the tax base for the final calculation.

Let's conduct a comparative analysis and find out what the income should be so that it would be more profitable to buy a patent rather than work according to a simplified scheme.

We will take the annual income of the individual entrepreneur as the basis for the calculation.

Let a Moscow hairdresser cost 59.4 thousand rubles for a year’s patent. In addition, he needs to pay insurance premiums: 32,385+(990,000 – 300,000)*1%= 39,285 rubles.

It should be remembered that on PSN, insurance premiums do not affect the amount of tax. Then, the total tax burden of individual entrepreneurs will be 59,400 + 39,285= 98,685 rubles.

Now let’s calculate what the amount of income received by an entrepreneur under the simplified procedure should be so that the tax burden is comparable to the amount received.

If during the year an individual entrepreneur earned 1 million 650 thousand rubles, then on the simplified tax system 6%: 32,385 + (1,650,000 – 300,000)*1%) = 53,115 rubles.

This amount will need to be paid additionally. Thus, the tax burden will be equal to 45,885 + 53,115 = 99,000 rubles.

back to menu ↑

Conclusion

Based on the calculations given above, we can conclude that in this case the transition to PSN is justified, provided that the hairdresser earns more than 1,650,000 rubles per year.

With further income growth, the patent value will not increase, but the tax burden on the simplified tax system will increase.

If your income is less than the above amount, then working under a simplified scheme would be a more profitable option.

Important: Before choosing a taxation system, it is better to first consult with 1C specialists on how to calculate the tax burden. In the future, this can help significantly save money.

back to menu ↑

Free patent

In some cases, an individual can expect to receive a patent free of charge.

If he registered for the first time as an individual entrepreneur, then, according to the law on tax holidays, he has the right to 2 years of work under a free patent.

To receive this benefit, you need to decide on the direction of business needed by local authorities for the development of the region.

back to menu ↑

Purchasing a patent

To switch to the patent system, you must submit to the local Federal Tax Service an application for a patent for individual entrepreneurs for 2021, completed according to.

If you are at the stage of initial registration of an individual entrepreneur and intend to conduct business in the same place where you are registered, the application must be submitted simultaneously with the application for registration of an individual entrepreneur.

In such cases, the patent is issued simultaneously with the entrepreneur's certificate.

Sample patent application for individual entrepreneurs

If you plan to conduct business in another region, and not according to registration, then filing an application for a patent will be possible only after you register an individual entrepreneur.

In addition, in this case it will need to be submitted in advance (10 days before the expected start of work).

The types of patents for individual entrepreneurs for 2021 are different. Each business area is issued its own patent.

The duration of the patent and the territory in which it will be valid are also taken into account.

For example, if an individual entrepreneur plans to engage in cargo transportation and retail trade, he will have to acquire 2 patents. They are also paid separately from each other.

back to menu ↑

How much does a patent cost for an individual entrepreneur?

Before purchasing a permit, it is important to calculate its exact cost. Based on the data obtained, you can compare whether it is profitable to work under the PSN or whether it is easier to use another tax regime. One of the features of the patent system is the upfront payment of the cost of permission. The contribution amount is calculated not based on the actual income received, but on the potential income. The amount of expected revenue is determined by local legislation for each specific type of activity.

In addition to the expected income, other indicators influence the cost of the permit:

- validity period of the document;

- number of employees;

- number of vehicles;

- presence of several retail outlets.

Tax calculation procedure

The cost of a certain type of patent for an individual entrepreneur for 2021 depends on the basic income, the amount of which is calculated individually for each type of business in a particular region, as well as the calendar period for which the permit is issued. The annual tax rate is fixed at 6%. Based on this, the calculation formula will look like this:

- SP = BD x 6%, where;

- SP – patent cost;

- DB – basic profitability.

Provided that the individual entrepreneur acquires a permit for a period of less than one year, the result obtained is divided by 12 (the number of months in the year), and then multiplied by the required number of periods:

- SP = BD x 6% / 12 x KM, where;

- SP – patent cost;

- BD – basic profitability;

- KM – number of months.

Example:

A businessman from Moscow plans to repair shoes in 2021. The basic profitability according to the law is 660 thousand rubles. The cost of a permit for a year will be:

- 660,000 x 6% = 39,600 rub.

If the activity falling under the patent, the individual entrepreneur will be carried out for only 6 months, the result obtained must be divided by 12 and multiplied by 6:

- 39,600 / 12 x 6 = 19,800 rub.

If it is difficult to make the calculation yourself, you can use the online calculator located on the official portal of the Federal Tax Service. It can be used by any citizen who wants to obtain information about the cost of a patent, regardless of whether it is registered or not. The scheme of working with the calculator does not cause any particular difficulties and consists of filling out the following fields:

- Period. The calendar year in which the business is expected to be conducted is selected.

- Period of use. Here you enter the number of months per year during which the entrepreneur will work.

- Federal Tax Service. You must select the name of the tax office, for example, 77 - Moscow city.

- Municipality. The specific area in which the business will be conducted is determined.

- Kind of activity. From the list you must select the direction in which the merchant will work.

- Meaning. Filled in when selecting certain types of activities, for example, to indicate the number of trade objects, etc.

- Calculate. After filling out all the fields, you need to click the “Calculate” button, after which the program will issue the amount required for payment.

Example:

- Eyelash lamination at home - how to do it. Recipe for gelatin lamination of eyelashes at home, video

- Chicken roll in a bottle: recipes with photos

- Turpentine baths according to Zalmanov at home

An entrepreneur from Moscow plans to engage in rental services in 2018 for 7 months. Enter data:

- period – 2018;

- period of use – 07;

- Federal Tax Service - 77 - Moscow city;

- municipal formation - for example, Administration of the municipal formation of Tverskoy;

- type – rental services.

After clicking the “Calculate” button, information will appear on the screen that the cost of the patent for this period is 34,650 rubles, and the tax is paid in two parts:

- RUB 11,550 – within 90 calendar days from the date of issue of the patent;

- RUR 23,100 - until the permit expires.

Tax holidays

Russian legislation may establish a zero tax rate – tax holidays. A free patent is issued for a period of 2 years from the date of opening your own business, provided that:

- a citizen is registered as an individual entrepreneur for the first time;

- activities are carried out in the social, scientific and production spheres, including the provision of consumer services to the population.

Tax holidays are in effect until 2021. In addition, for merchants engaged in business in the Republic of Crimea and the city of Sevastopol, until 2021, the tax contribution rate for all types of commercial activities or individual positions can be reduced to 4% (instead of the legally established figure of 6%). Such a relaxation for individual entrepreneurs is recorded in the Tax Code of the Russian Federation - clause 2 of Art. 346.5.

Patent duration

The convenience of PSN is that it is not declarative. The only thing you need to keep is an income book. It is not submitted to the Federal Tax Service, but the inspector may request the CUD.

However, this advantage is negated by the limited duration of the patent.

At most, a patent can be valid for a year, after which it will need to be applied to the inspection authorities again.

If the patent was issued for 2-3 months, then with each renewal you will need to write an application.

Therefore, PSN is both convenient and inconvenient. For each specific case, you need to calculate the tax burden, as was done above, in order to assess the profitability.

Note! If the patent began to be valid on December 1, 2017, then the individual entrepreneur has the right to apply the PSN, but a fine and penalties will be imposed on him.

back to menu ↑

What documents are required

The basic list of requirements for conducting a patent procedure and preparing documents is enshrined in the Civil Code of the Russian Federation, Order of the Ministry of Economic Development No. 316. A patent application must contain:

- a statement with information about the developer, applicant, representative;

- description of the technical solution;

- formula;

- drawings and other materials, if they are needed to fully disclose the essence of the object (the specified block may include images, tabular forms, diagrams, etc.);

- abstract, i.e. shortened version of the description.

It is better to entrust the preparation of the application to professional specialists - patent attorneys, especially if you do not have patenting experience. Each form included in the application is subject to special requirements set out in Order No. 316.

In addition to the documents immediately included in the application, the applicant will have to submit other forms. For example, already at the initial stage of contacting FIPS, you need to fill out consent to the processing of personal data. To conduct expert activities and provide priority, applications must be submitted. Separate applications are submitted when changes are made to the original documentation, to transform the application, or in other cases.

The content of the application for inventions and utility models is identical. For industrial designs the situation is different, since the essence of such objects lies in deciding the appearance. Therefore, the application will include an application, a general drawing, a description of the sample, and a set of images.

The completeness of the submitted documents will be checked at the formal examination stage. If the applicant has not submitted any forms or forms, or violates the procedure for filling them out, FIPS experts have the right to send a request. If all the requirements set out in the request are met, patenting will continue according to the general rules. If the request remains unanswered or the comments are not eliminated, the patent procedure is terminated.

Below we will look at how the description and other documents in the application are compiled, taking into account the requirements of Order No. 316.

Patent renewal

To renew an individual entrepreneur's patent as of 2021, it is necessary to submit an application to the Federal Tax Service. This must be done no later than December 20.

At the same time, the details for which payment must be made will remain unchanged.

The deadlines must be strictly adhered to, otherwise you will be transferred to the main tax system and you will only be able to resubmit your application next year.

This is stipulated in Article TC No. 346.45. The same measures apply to those who are late in payment.

back to menu ↑

How to buy and apply for a patent

The first step is to make sure that the types of work chosen by the entrepreneur are covered by a patent in the given region.

Payment for a patent has the following features:

- when purchasing it for a period of 1 to 6 months, the individual entrepreneur pays the entire amount until its expiration;

- purchase from 6 to 12 months involves payment in 2 stages: the third part is paid into the budget within 90 calendar days from the start of work, the remaining 2/3 - before the expiration date.

No documents are needed to obtain an IP patent 2021 except an application.

It can be submitted in the following order:

- bring it in person (have your passport with you);

- transfer through a representative with a power of attorney executed by a notary;

- send by mail, attaching a description of the attachment;

- by email to the Federal Tax Service website (certification with an electronic signature is required!).

When filling out an application for purchasing a patent, an entrepreneur, in addition to personal information (full name, INN, OGRNIP, if already available), must indicate:

- your postal code;

- inspection code;

- one of the names of the types of activities selected by the individual entrepreneur;

- start and end dates;

- identification code (also for business activities);

- registration address (as in the passport);

- if future work is related to transport, then information about it, as well as about the objects of proposed trade, repair, services, etc.

The document must be filled out in block letters and legibly.

An application for an individual entrepreneur patent for 2021 can be submitted at the time of registration of the individual entrepreneur with the Federal Tax Service (but under such conditions the 10-day period is not observed).

Within 5 working days, the entrepreneur will receive either a refusal (the reason is indicated) or a patent, and work can begin as soon as the business documents are ready. The issuance of a patent must be carried out strictly on the territory of the municipality where its activities will be carried out!

If an individual entrepreneur decides to voluntarily cease business activities with a PSN, he will also submit an application to the Federal Tax Service, and within 5 days he will be deregistered.

Application for loss of the right to use PSN

Sometimes it is simply impossible to switch to PSN. Factors that prevent this from happening are:

- The annual income exceeded 60 million rubles.

- The company employs more than 15 people.

- The entrepreneur did not have time to pay the tax in full or was late in payment.

If one of these points is true in your case, and you do not want to transfer to OSNO, you will need to submit a statement that you have lost the right to use PSN.

This is done according to form 26.5-3. It must be submitted within 10 days. If a businessman decides to stop his activities before the patent expires, he will need to fill out a patent form for individual entrepreneurs in form 26.5-4, relevant for 2021.

It must be submitted no later than 5 days after the completion of business activity. A sample of both forms can be taken on our website.

back to menu ↑

How to start working on a patent

For an individual entrepreneur to work on the PSN, an application must be submitted no later than 10 working days before the start of the year from which you want to use this system (this is for those who are already an individual entrepreneur and want to switch to a patent or continue to use it in the next year).

For 2018, the last date for submission is December 15, 2021. But I advise you to do this much earlier: if you suddenly make a mistake in your application (and on this basis you are refused), you can submit it again. Otherwise you will have to wait until next year.

The application is submitted using a special form, which is posted on the tax website.

Transition of individual entrepreneurs to online cash registers

The first edition of Law No. 54-FZ stated that individual entrepreneurs with a patent must make the transition to online cash registers by 2021.

However, Law No. 337-FZ of November 27, 2017 made it possible for most entrepreneurs to postpone this until 2021, as well as UTII.

As a result, the transition to online cash registers in 2021 became mandatory only for some individual entrepreneurs with a patent:

- for those who are engaged in retail trade and have hired employees on their staff (Article 346, paragraph 2, paragraphs 45-46 of the Tax Code of the Russian Federation);

- those who own public catering outlets and hire hired workers to work in them (Article 346, paragraph 2 of Article 346 of the Tax Code of the Russian Federation);

- owners of cafeterias and retail stores working there independently. When hiring an employee, such individual entrepreneurs must switch to online cash registers no later than 30 days after signing the employment contract.

back to menu ↑

KBK codes for patents

KBK are budget classification codes that are necessary to group government items. budget.

They must be indicated when you pay for the patent. The BCC value for each patent for 2021 is determined based on the scale of the region in which the individual entrepreneur operates:

| Region | KBK |

| St. Petersburg, Moscow, Sevastopol | 182. 1. 05. 04030. 02. 1000. 110. |

| Urban districts | 182. 1. 05. 04010. 02. 1000. 110. |

| Urban districts with intra-city divisions | 182. 1. 05. 04040. 02. 1000. 110. |

| Municipalities | 182. 1. 05. 04020. 02. 1000. 110. |

| Districts within the city | 182. 1. 05. 04050. 02. 1000. 110 |

Important! The transition to PSN does not make the entrepreneur free from paying compulsory insurance premiums (both for his employees and for himself). In addition, personal income tax must be paid for each employee. In this case, income tax, ordinary insurance premiums and “accident” contributions are paid according to their own BCC, which are established for each of the listed types of payments.

back to menu ↑

How do individual entrepreneurs report on a patent (with hired workers)

PNS implies hired labor, including under civil contracts.

But the total number of involved workers is limited to 15 people in total in all areas of business conducted by the individual entrepreneur.

The tax rate is 6%.

Individual entrepreneur reporting is divided into three components:

- Reporting to the Federal Tax Service Inspectorate (Federal Tax Service Inspectorate).

- Reporting to the pension fund.

- Reporting to the social insurance fund.

Let's look at this question in more detail:

Reporting to the INFS occurs as follows:

- There is no need to submit a tax return;

- Before January 20, you must submit a certificate about the average number of employees on the list. Rented once every 12 months;

- keep records of income and expenses. If there are several patents, such a book must be created for each of them. It can be provided either electronically or in writing. There is no need to certify the book;

- before April 1, you must provide a certificate of personal income tax 2 (once every 12 months);

- provide a certificate in form 6-NDFL every quarter (in the 1st quarter - no later than 30.04, in the 2nd - no later than 31.07, in the 3rd - no later than 31.10, in the 4th - no later than 30.01);

- provide quarterly information on the unified social insurance tax (terms are similar to 6-NDFL).

Reporting to the pension fund occurs as follows:

- every month it is necessary to provide information about persons with C3B-M insurance (no later than the 15th day of the month);

- annually (before March 1) provide information on the length of service of workers (C3B-experience and EDV-1);

Reporting to the Social Insurance Fund (SIF):

- submit Form 4 FSS every quarter;

- annually submit a certificate confirming your main activity.

In the case where there are no hired workers, reporting is much simpler. The tax rate remains the same (6%).

For INFS, you only need to maintain a cash flow book. There is no need to report to the Pension Fund and the Social Insurance Fund, since there are no employees as such.

back to menu ↑

Patenting procedure

The registration of patent rights in Russia is carried out by a special service - FIPS. It is to this office that an application for an invention, utility model or industrial design is submitted. The patent procedure is carried out according to the following rules:

- the inventor must prepare a set of application documentation and submit it in written or electronic form to the patent office;

- received documents are registered and the relevant information is published in the Rospatent Bulletin;

- The mandatory stages of patenting include 2 examinations - formal and substantive;

- if the expert activities ended positively, a decision will be made to register and issue a patent form;

- after all registration actions are completed, information about the object and the copyright holder is entered into the register, and the applicant will receive a patent.

It is recommended to conduct a preliminary search of the registries before submitting an application. To do this, it is better to contact the patent office, since independent verification will take much longer and does not guarantee the objectivity of the search result. Based on the results of the preliminary search, the application for an invention can be clarified or supplemented in order to eliminate in advance the claims and comments of FIPS experts.

The developer, the customer, or an authorized representative can apply for a patent. A patent attorney or another person who has a notarized power of attorney has the right to act as a representative. The representative will be able to defend interests at all stages of patenting, including when considering objections from interested parties or other disputes.

Taxes and fees

An individual entrepreneur with a patent must pay taxes to the authority where he is registered. At the same time, the following is true for individual entrepreneurs with hired workers:

- If the patent is valid for up to six months, then the tax is paid in full no later than the 25th day after the patent came into force.

- If the patent is valid for six months or more, then 1/3 of the tax is paid no later than 25 days after the patent comes into force, and the remaining 2/3 is paid after another 5 days.

- Insurance contributions to the Compulsory Medical Insurance Fund and the Pension Fund of the Russian Federation depend on the amount of income. If it does not exceed 300 thousand rubles. for the year, they must be paid before December 31 of the current year. You can pay monthly or quarterly.

- If the income exceeds the declared amount, the payment deadline is shifted. In this case, contributions must be paid no later than April 1 of the following year.

- 13% personal income tax is deducted from the salary of each employee. The transfer must be made the next day after the payment of the salary.

- Contributions to the pension fund must be made for each employee no later than the 15th day of the following month. Individual entrepreneurs who are employers pay reduced insurance premiums, unless we are talking about renting out real estate or trading in public catering outlets.

Important: Chapter 26.5 of the Tax Code of the Russian Federation, which regulates PSN, does not provide for a reduction in the price of a patent by the amount of mandatory insurance contributions.

If the individual entrepreneur did not hire hired workers, then only 1-2 points from this list are valid for him.

back to menu ↑

What duties do you need to pay?

The patenting procedure is paid, so the applicant will have to make the following payments:

- when submitting and registering application documentation – 3,300 rubles, 700 rubles each. for each point of the formula over the first 10;

- for consideration of the application and conducting an information search - 9500 rubles, 6200 rubles each. for each claim above 1;

- for a decision based on the results of a substantive examination - 12,500 rubles, 9,200 rubles each. for each claim above 1;

- for issuing a completed patent – 1,500 rubles. (there is no need to pay a separate fee for additional claims at this stage).

The indicated payment amounts came into force in October 2021. For other objects of industrial property (utility models, industrial designs), the composition and amount of duties will be different.