The patent taxation system, like others, provides for a full report on the individual entrepreneur’s work. For each patent, an Income Accounting Book (ILR) is kept, reflecting the company’s monetary transactions for the tax period (clause 1, clause 6 of Article 346.53 of the Tax Code of the Russian Federation). In the absence of a book or its incorrect maintenance, penalties are imposed - 10,000 rubles, for a second violation - 30,000 rubles (Article 120 of the Tax Code of the Russian Federation). How to properly keep records of individual entrepreneurs on a patent and avoid penalties?

What is PSN: briefly about the mode

The patent system is designed for small businesses. It is allowed to be used by entrepreneurs whose activities are related to the provision of household services or the production of small volumes of goods. A complete list of directions is given in paragraph two of Article 346.43 of the Tax Code of the Russian Federation.

Mandatory conditions for the transition are:

- no more than 15 hired employees during the reporting period;a

- actual annual income from a taxable type of activity is up to 60 million rubles;

- waiver of partnership agreements or trust deeds.

In addition, representatives of the catering retail trade must comply with the limitation on the area of pavilions. Each point of sale should not be more than 50 square meters. m. If several objects are used in an activity, their total area may exceed the standard (parts 45 and 47 of paragraph 2 of Article 346.43 of the Tax Code of the Russian Federation).

The essence of the PSN comes down to the purchase of a special permit for a period of one month to a year. An entrepreneur must contact the tax authority at the place of business. This must be done 10 days before the expected launch of the project. The application must indicate the main characteristics of the business (sale area, number of employees, vehicles, etc.). If the regulatory authority does not see any obstacles to the application of the regime, the merchant will be issued a patent. The cost of the document will be calculated immediately based on the potential profitability approved in the region.

Patent tax system

The purpose of the patent regime is to help small and medium-sized businesses in our country.

This leads to restrictions on its use:

- Available exclusively to individuals who have received the status of Individual Entrepreneur;

- Limitation on the number of employees that a businessman can hire. At the moment, the upper limit corresponds to 15 employees;

- If you have your own shop, cafe or restaurant, then the area of the premises that you use for the above purposes should not exceed 50 square meters;

- Payment of taxes under the patent system is available only for 63 types of activities, including: repair services, tailoring, knitting of clothing and other textile products; shoe repair and sewing services; hairdressing activities; provision of cosmetic services; educational services; furniture repair services, retail trade; design services. You can find a general list of permitted activities in the Tax Code of the Russian Federation, Article 346.43, paragraph 2.

- For each patent, the entrepreneur is required to keep an income book; this book must be kept by the individual entrepreneur for 4 years after the patent regime was adopted. We will talk in more detail about this document a little later;

- Convenient patent payment system depending on the period of its application.

- The company's annual turnover is limited to 60 million rubles;

- The cost of a patent is not reduced by insurance payments.

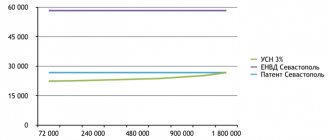

There are quite a lot of restrictions and disadvantages, but the patent system also has its advantages, for which 3.5% of Russian entrepreneurs choose it:

- Significantly eases the tax burden for a businessman. You transfer to the state only 6% of the potential income from your type of activity. Potential income is established by the authorities of the constituent entity of the Russian Federation;

- You can choose the validity period yourself;

- You are exempt from filing a tax return;

- The only extra-budgetary fund to which you will have to make payments is the Russian Pension Fund. Payments will be 20%;

- If you are on the patent system's list of eligible activities, you will remain on it until the end of your life. The authorities do not have the right to reduce this list;

You can use the Patent cost calculator.

Requirements for accounting and reporting

The rules for recording business transactions are enshrined in Article 346.53 of the Tax Code of the Russian Federation. Tax accounting of individual entrepreneurs on a patent comes down to recording the income actually received by the entrepreneur. Receipts are recorded throughout the entire period of validity of the patent. The accounting journal has the right to request territorial inspections as part of checking compliance with restrictions.

The form and rules for filling out the register were approved by Order of the Ministry of Finance of Russia No. 135-dated October 22, 2012. Revenue information is entered in chronological order. The lines record the serial number of the business transaction, details of the primary documents, their contents and the amount in rubles. It is permitted to maintain the register electronically. However, after the end of the reporting period, the magazine is printed on paper, the sheets are numbered and stitched.

Important! Order of the Ministry of Finance of Russia No. 135-also introduced a book of income and expenses for “simplified people”. The difference between the magazine for PSN is the absence of a section on costs. Patent holders do not document their expenses.

Entrepreneurs may not keep accounting records (clause 2 of Article 6 of Law No. 402-FZ of 12/06/11). Registration of business transactions is carried out by merchants on a voluntary basis. In this case, one should rely on the clarifications of the Ministry of Finance of the Russian Federation No. 64n dated December 21, 1998, No. PZ-3/2015 dated June 3, 2015, as well as numerous PBUs.

What reporting must be submitted by an individual entrepreneur who combines a patent and OSNO

When combining several tax regimes, an individual entrepreneur must submit reports for each of them. The patent does not require tax reporting, but if the income of an individual entrepreneur falls under OSNO, it is necessary to submit VAT and 3-NDFL returns.

In addition, when combining a patent and OSNO, the individual entrepreneur and employees submit all reporting forms that are required if there is staff.

VAT declaration

The VAT return can only be submitted in electronic format. The reporting period is a quarter, the declaration must be submitted within 25 days after its completion. It is filled out separately according to the amount of tax that the individual entrepreneur must pay for himself and for the counterparties for whom he acts as a tax agent.

A VAT return must also be filed if the individual entrepreneur acts only as a tax agent for this tax.

What you need to know about reporting

Tax returns are not provided for patent holders (Article 346.52 of the Tax Code of the Russian Federation). This is the main advantage of the mode. However, only entrepreneurs who do not use hired labor can count on complete exemption. All they need to do is keep a book of income and monitor the validity of the patent. There is no requirement to submit reports to extra-budgetary funds. Businessmen need to pay insurance premiums “for themselves” in a timely manner.

Other rules apply to the PSN payer and the employee. The conclusion of at least one employment contract or civil agreement with an individual gives rise to new responsibilities. Availability of personnel involves filling out a number of payment forms.

| Name | a brief description of | Link to normative act |

| 2-NDFL | Entrepreneurs must submit a certificate to the Federal Tax Service by April 1 of the year following the reporting year. The document reflects the amount of personal income tax withheld from employee benefits. | Chapter 23 of the Tax Code of the Russian Federation, orders of the Federal Tax Service of the Russian Federation No. ММВ-7-3/ [email protected] from 09.16.11, No. ММВ-7-11/ [email protected] from 10.30.15, No. ММВ-7-11/ [email protected] ] from 01/17/18. |

| If the number of employees exceeds 25 people, payments are accepted only in electronic format (Article 230 of the Tax Code of the Russian Federation). However, in this case the right to use PSN will be lost. | ||

| If it is impossible to withhold tax, the merchant is obliged to send a corresponding message to the inspectorate. This must be done before March 1st. | ||

| 6-NDFL | The declaration is submitted quarterly and contains information about the personal income tax of employees. The deadlines for sending reports are established by paragraph two of Article 230 of the Tax Code of the Russian Federation. The entrepreneur must provide information before the end of the month following the reporting quarter. | Chapter 23 of the Tax Code of the Russian Federation, order of the Federal Tax Service No. ММВ-7-11/ [email protected] dated 10.14.15 |

| SZV-M | Employers must send calculations to the Russian Pension Fund every month before the 15th. The forms reflect the INN, full name, and SNILS of each employee. | Clause 2.2. Article 11 of Law No. 27-FZ dated 04/01/96, Resolution of the Pension Fund of the Russian Federation No. 83p dated 02/01/16. |

| Calculation of insurance premiums | Information is submitted to the territorial tax authority quarterly within 30 days from the end of the period. | Clause 7 of Article 431 of the Tax Code of the Russian Federation, order of the Federal Tax Service of the Russian Federation No. ММВ-7-11/551 dated 10.10.16 |

| Average headcount | All employers are required to provide information to the tax office. The condition is to attract hired employees during the reporting period. The document must be submitted annually before January 20 at the place of registration. | Article 80 of the Tax Code of the Russian Federation, order of the Federal Tax Service of Russia No. ММВ-3-25 / [email protected] dated 03.29.07. |

| 4-FSS | Reporting deadlines depend on the format. Entrepreneurs with up to 25 employees can submit information to the FSS of Russia on paper. This fully applies to patent holders. They must submit the forms quarterly by the 20th of the following month. | Article 24 of Law 125-FZ of July 24, 1998, order of the Federal Tax Service of the Russian Federation No. 381 of September 26, 2016. |

It is difficult to discuss the advantages and disadvantages of reporting on PSN. Businessmen do not submit declarations directly related to the acquisition of a patent. The need to fill out approved forms arises only when personnel are involved.

Comments

Olga 04/09/2017 at 01:15 pm # Reply

Declaration of individual entrepreneurs on the simplified tax system and patent for 2016

Please tell me what kind of declaration should be filed by an individual entrepreneur who uses the simplified tax system and works on a patent? Zero? Thank you.

Natalia 04/09/2017 at 01:29 pm # Reply

Olga, good afternoon. If you receive all your income from activities on the patent tax system, then you need to submit a zero declaration to the simplified tax system.

08/02/2017 at 00:11 # Reply

Sergey

If the patent has employees, but it so happens that I work without. What reports do I need to submit, or do I not need to submit anything?

08/07/2017 at 15:16 # Reply

Good afternoon. If you have registered with the Pension Fund of Russia and the Social Insurance Fund as an employer, you are required to submit zero reports until you deregister as an employer with the Pension Fund of the Russian Federation and the Social Insurance Fund. You must submit Form 4-FSS to the Social Insurance Fund by the 20th day of the month following the reporting quarter. To the Federal Tax Service, the RSV form, by the 30th day of the month following the reporting quarter.

07/26/2018 at 12:16 pm # Reply

Filling out insurance calculations for individual entrepreneurs on a patent

Tell me how to correctly fill out in 1C Calculation of insurance claims for individual entrepreneurs on a patent? There, benefits apply to employee contributions. How can this be reflected correctly in the report?

Independent accounting

The patent holder can organize tax accounting without a qualified employee. In practice, there are no difficulties with recording income in the journal. The merchant will be required to be attentive and responsible in preparing documents. The basis will be statements from the current account and cash register reports.

If the activity is gaining momentum, it makes sense to think about setting up a simplified accounting system. Even minimal accounting reporting will significantly improve the quality of control over the movement of material assets and cash. The main directions will be:

- Salary. In this area, you will need to deal with calculating staff remuneration, withholding personal income tax, and calculating insurance premiums. Systematization of data will facilitate the calculation of vacation pay and streamline the reimbursement of travel expenses.

- Stock. Recording the remaining raw materials, finished products and materials will help optimize production processes. It will become easier for suppliers to submit requests. Regular inventory will eliminate the risk of theft and other abuses.

- Fixed assets. The entrepreneur cannot put the property on the balance sheet. The law does not separate the status of a commercial entity and an individual. However, it is quite possible to calculate the initial cost, control wear and tear and create reserves in case of major repairs.

- Accounts receivable and accounts payable. Regular analysis of the relationship between obligations and rights allows you to maintain the financial stability of your business. Availability of accounting information helps in planning.

Separate areas of accounting may include cash register, non-cash payments, government procurement, etc. The basis for independent construction of accounting becomes Law No. 402-FZ of 12/06/11 and the current rules. Numerous standards and regulations are presented in reference and legal systems. The provisions of regulations should be applied taking into account the entrepreneurial status.

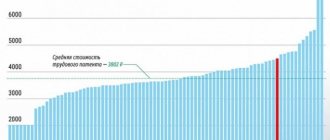

How much does a patent cost?

To obtain a patent, you must submit a corresponding application to the Federal Tax Service.

Having received it, the Federal Tax Service will calculate its value (tax amount) in accordance with the law of your subject of the Federation. All you have to do is pay the cost.

To pre-calculate the cost of a patent, use the “Patent Cost Calculation” service.

In addition to patent tax, individual entrepreneurs pay:

- insurance premiums for yourself;

- Personal income tax, insurance premiums for employees;

- tax on real estate used in activities on the PSN, only from the cadastral value.

Reporting procedure

Since the law does not provide for declarations on PSN, the question of how to interact with the tax inspectorate disappears. Upon expiration of the application period, the merchant has the right to submit an application again. The application form was approved by order of the Federal Tax Service of the Russian Federation No. ММВ [email protected] dated 07/11/17. It can be sent in writing or electronically.

The question of how to submit reports to entrepreneurs-employers is also not worth it. The transition to a special regime does not affect other obligations. Sending payments is permitted in person, through an authorized representative, or by mail. PSN payers are not required to use telecommunication channels. All documents are prepared on paper.

Reporting from individual entrepreneurs on PSN with employees

If an individual entrepreneur has employees, then, firstly, he may have all the responsibilities listed above, and secondly, the individual entrepreneur must report to:

- Federal Tax Service (providing there, in a timely manner, certificates of the average number of staff, forms 2-NDFL, 6 NDFL, ERSV);

- Pension Fund (providing there forms of persuance, for example SZV-M and SZV-TD);

- FSS (providing form 4-FSS there).

Note that against the backdrop of the general digitization of reporting, when a significant part of documents is provided by businesses to the state in electronic form (with associated costs for purchasing the necessary software and equipment), individual entrepreneurs have the advantage of being able to use traditional paper reporting - both when interacting with the Federal Tax Service and when sending documents to government funds. The advantage, of course, is not the most obvious - many individual entrepreneurs only welcome the opportunity not to visit the Federal Tax Service, but to interact with the department remotely.

The fact is that reporting to the Pension Fund of the Russian Federation is submitted electronically only if the individual entrepreneur has more than 25 employees, to the Federal Tax Service - if 25 or more (for personal income tax reporting), and also if there are more than 100 employees (for other reporting documents). Neither one nor the other is possible on PSN.