The concept of net assets

The term net assets characterizes the complex of company property that was acquired using its own funds or borrowed resources (provided that long-term loans predominate). With a constant positive value of this indicator, we can talk about the profitability of the activity.

Also see “What does return on net assets show: the formula.”

In turn, a negative net asset value indicates the presence of problems in the financial sector of the enterprise. This can manifest itself through:

- unprofitability of the organization;

- illiquidity of the company's resource base;

- lack of working capital for the implementation of current production processes.

Here's how founders can learn about management miscalculations and funding problems:

- the amount of short-term liabilities in relation to working resources is significantly overestimated;

- negative net assets are shown in the auditor's report and management accounting reports;

- the results of horizontal analysis indicate a constant reduction in the value of net assets.

Also see “Net Asset Turnover Formula”.

Results

The formation of negative net assets is fraught with negative consequences for the company, including liquidation. So as soon as net assets shrink in volume to the extent that they become less than the authorized capital, the owners and management of the company should take emergency measures to correct the situation.

Even if the tax inspectorate filed a liquidation claim in arbitration, a negative scenario can be avoided. If the taxpayer does not have large debts, the salary is paid regularly and in full, all taxes and fees are paid without delay, the judges take his side. Arbitrators will most likely consider the current situation not serious enough to liquidate the organization.

Negative net assets are formed when a business entity operates at a loss for several years. This circumstance can lead to dire consequences, including the liquidation of the organization. How to avoid this and what measures need to be taken first, you will learn from our article.

Net assets: general information

Guidelines for action if the value of net assets is less than the authorized capital

How to increase the value of assets

Why You Need to Track Net Assets

Adjusting your financial tactics can improve the situation. But if the management of the enterprise does not react promptly and does not change management methods, the result may be the liquidation of the company. The final loss of solvency and the absence of ways out of the crisis is evidenced by the negative value of net assets in relation to the authorized capital, which persists in the long term.

Forced liquidation is initiated if there is a need to adjust the valuation of capital to equalize it with the value of net assets with a minimum amount of capital. The company can challenge the decision of the regulatory authorities to terminate its activities in court. But if the court liquidated the company with negative net assets, this position will be final.

What to do if the value of net assets is less than the authorized capital

The formation of a company's net assets with a negative value entails the following problem: if for 2 years in a row the value of such assets continues to remain in the negative, the company is subject to liquidation.

Moreover, nothing will depend on the company, and liquidation will be carried out forcibly. The grounds for such actions are contained in paragraph 11 of Art. 7 Federal Law “On the tax authorities of the Russian Federation” dated March 21, 1991 No. 943-I. According to it, tax authorities have the right to initiate the liquidation of a legal entity through the court if its commercial activities have led to negative results. The organizational and legal form of the company cannot influence the decision of the tax authorities.

Important! Before the expiration of the 2-year period, the organization has the opportunity to take preventive measures and thereby avoid a negative scenario. As soon as net assets shrink to a value less than the capital specified in the charter, the owners must either increase the total volume of assets, or reduce the amount of authorized capital, or liquidate. The owners must make a decision within the first half of the year following the reporting year. These norms are enshrined in paragraph 4 of Art. 90 of the Civil Code of the Russian Federation for LLCs and clause 6 of Art. 35 Federal Law “On Joint Stock Companies” dated December 26, 1995 No. 208-FZ for joint-stock companies.

A reduction in the size of the authorized capital must be accompanied by notification of this event to creditors. In addition, the company is given 3 days to report the event to the tax authority.

If the authorized capital is at a minimum and net assets are in the red, there is a real threat of liquidation. The initiative in this case belongs to the tax inspectorate, which files a corresponding claim in the arbitration court. In the statement, the tax authorities justify their request, and the final verdict remains with the arbitration.

When considering each case, judges carefully analyze the situation in the organization. If it turns out that the taxpayer is able to fulfill its obligations to creditors and the budget, the arbitrators refuse liquidation. Confirmation of this can be found in the resolutions of the FAS Moscow District dated September 25, 2009 No. KG-A41/9762-09 and the FAS East Siberian District dated October 4, 2012 No. A33-20303/2011, as well as in the information letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated August 13, 2004 No. 84.

Ways out of the crisis

To improve a company's financial position, managers can use several methods. One of the simplest ways is to revaluate assets. This will lead to an increase in the cost of the company's working resources. The disadvantage lies in the need for regular revaluation in the future.

If the net assets are negative, the founder can find a way out in an additional injection of cash. When transferring the required amount to the company's current account, the owner of the company must indicate for what purpose this contribution is being made. In the purpose of the payment, we recommend that you specify that the money is transferred to a legal entity to increase the value of net assets.

When an enterprise has negative net assets, not everyone knows what management should do. Here's the general approach:

| 1 | Determine the reporting period in which the minus value of this indicator first appeared |

| 2 | If 2 years have not passed since the designated date, then it is necessary to promptly initiate a revaluation of assets or look for ways to increase the value of assets by attracting investors, through additional injections from the founders |

| 3 | At the end of the two-year period, the tax authorities will initiate liquidation of the company |

Also see “Increase in Net Assets by Founders and Entries.”

Read also

31.07.2018

But we should not forget that during the period in which the company has not yet taken measures to correct the negative equity capital and has not been liquidated, it is obliged to notify its creditors and counterparties about the insufficiency of property by submitting such a notification to the website https://fedresurs.ru/ to the Unified Federal Register of Information on the Facts of the Activities of Legal Entities (hereinafter referred to as EFRSFYUL, Fedresurs).

According to paragraphs. l.1 clause 7 art. 7.1 Federal Law No. 129 “On State Registration of Legal Entities and Individual Entrepreneurs”, the EFRSFYUL contains information about the occurrence of signs of insufficient property in accordance with the legislation on insolvency (bankruptcy).

According to Article 2 of Federal Law No. 127 “On Insolvency (Bankruptcy)”: “Insufficiency of property is the excess of the amount of monetary obligations and obligations to pay obligatory payments of the debtor over the value of the property (assets) of the debtor.”

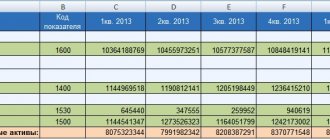

To determine the insufficiency of property, it is necessary to compare the book value of current and non-current assets with long-term and short-term liabilities.

Balance sections: (I+II) and (IV+V)

Balance lines: (1100+1200) and (1400+1500)

Line 1600 is the total book value of current and non-current assets; it is equal to the sum of sections I and II or the sum of lines 1100 and 1200.

Formula for determining insufficiency of property: 1600-(1400+1500)

If the sum of long-term and short-term liabilities (1400+1500) exceeds the book value of line 1600, this is an indicator of insufficient property.

In addition, the net asset value (NAV) is calculated using the formula:

1600-(1400+1500+1530+ZU), where:

1530 – deferred income;

ZU - debt of the founders for contributions to the management company (indicated in the balance sheet as part of accounts receivable (as part of line 1230).

In most cases, the values of line 1530 and the account balance have an insignificant or zero indicator, therefore, the value of net assets with a negative value or if it is less than the authorized capital almost always indicates insufficiency of property.

Also, organizations need to know that in the absence of mandatory notifications to the EFRSFYUL, in accordance with Parts 6-8 of Art. 14.25 of the Code of Administrative Offenses of the Russian Federation, administrative liability is applied to the violator in the form of a fine of up to 50,000 rubles, and in case of repeated violation, the official is disqualified from 1 to 3 years. In addition, in the event of bankruptcy of an organization that has not published mandatory statements in the Federal Resources Agency, the persons controlling it (manager, founders and other persons) risk being held vicariously liable, since such an organization hid important information about its condition from its creditors.

Now it remains to understand how to publish a notice of insufficient property on the Fedresurs website. Any publication in the Federal Resource is possible only with the help of a qualified electronic signature (qualified electronic signature), otherwise it is impossible to publish a notification in the Federal Resource. Currently, there are the following methods for publishing a message in Fedresurs:

Method 1 – Self-publish.

(recommended for legal entities)

You need to purchase a new CEP from a certification center (its cost, depending on the region, varies from 3000-4000 rubles), and together with the software it will cost 6000-7500 rubles. CEPs are not universal; the signature must have a special extension for use in Fedresurs. After purchasing the CEP and software, you need to install them on your work computer and configure them (be sure to use the help of an IT specialist!). Please note that CEP operates only from version 7 of Windows and higher, and only in browsers updated to the latest version. Internet Explorer is the most recommended to use. Next, you log into your personal account on the website https://fedresurs.ru/ then replenish your personal account with the amount of the state duty (from 04/01/2019 it remains 860.35 rubles + VAT). Funds arrive the next business day at approximately the same hour you made the payment. Then you select the required message, fill out the required fields in the form that opens (please note that all form fields must be filled out correctly, they must contain reliable information) and publish the notification.

This method of publication is quite lengthy and expensive, and is recommended if you do not have your own suitable CEP.

Method 2 – Use the fast message publishing service:

(recommended for legal entities, individuals and individual entrepreneurs)

The following Services for publishing notifications in Fedresource are the fastest and most reliable:

https://fedresurs.online https://fedresurs.com https://fedresurs.net

Responsibility measures for owners

First, you need to announce a reduction in your authorized capital to an amount not exceeding the value of your net assets, and register such a reduction in the prescribed manner. And if the value of net assets is less than the minimum amount of authorized capital established by the Law on the date of state registration of the company, the company should be liquidated. Such provisions are spelled out in Law No. 14-FZ (clause 3, article 20) and in the Civil Code of the Russian Federation (clause 4, article 90).

No measures of liability for failure to comply with the requirement (failure to make a decision to liquidate the company within a reasonable time) have been established directly for the founders. As a general rule, founders (participants) are not liable for the obligations of the company and bear the risk of losses associated with its activities, within the value of the contributions they made (clause 3 of article 56 of the Civil Code of the Russian Federation, clause 1 of article 2 of Law No. 14-FZ ).

However, in some cases, the legislation provides for the possibility of holding participants (founders) liable. Thus, in the event of bankruptcy of a company through the fault of its founders or other persons who have the right to give mandatory instructions, they may be subject to subsidiary liability for its obligations (clause 3, article 3 of Law No. 14-FZ, clause 4, article 10 of the Law N 127-FZ). That is, if the company’s property is not enough to satisfy the claims of creditors, the founders bear additional responsibility in this case.

A.S. Nestyurkina

Auditor

How to increase the value of assets

In order to increase the value of a company's net assets, it is necessary to take one of the following actions.

- Revaluation of existing assets, namely fixed assets and intangible assets. The point is that, as a result of the revaluation, the value of assets may increase and thus bring the net asset indicator out of the minus. After this procedure is carried out in accounting, the entire revaluation is reflected in the account. 83, thereby increasing additional capital, which, in turn, will affect the size of net assets.

IT SHOULD BE NOTED! When deciding to revaluate assets, an organization will have to carry it out on an ongoing basis, since isolated cases of such actions may be negatively assessed by regulatory authorities, who may subsequently impose sanctions on the company in accordance with the Tax Code of the Russian Federation and the Code of Administrative Offenses of the Russian Federation.

- Increasing assets by replenishing a current account with cash or adding additional property for the company to conduct its activities. In accounting, actions for depositing funds are reflected in other income (account 91), and for depositing property - in deferred income (account 98).