What is an advance report

In the very phrase “advance report” one hears a decoding of the meaning - a report on the advance payment issued. An advance is issued to the accountable person for the intended use of funds, confirmed by properly completed primary documents.

Reported funds are provided for the following purposes:

- Economic needs of the organization;

- Travel expenses;

- Entertainment expenses.

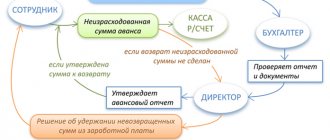

The advance report is filled out by the accountable person himself, checked, as a rule, by an accountant (or manager) and signed by the head of the organization. Based on the data of the approved advance report, the accountant writes off the accountable funds.

The accountable person may be:

- Employees of the organization;

- Freelance employees who have entered into civil legal relations with the company.

Correct completion of the report is very important, because... otherwise, the tax office may have questions about the validity of accepting the spent amounts for tax accounting.

The deadline for the employee to submit a report on accountable amounts is set at 3 working days, however, if this day falls on a weekend (sick day, business trip), then the date of the report will be considered the day the accountable person goes to work.

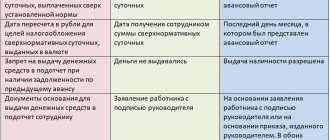

To provide advance funds, the accountant writes an application for the issuance of money, where he specifies the amount and period for which they are required, as well as information about the absence of debt on the previous report. The signature of the manager and the date on such an application are mandatory details.

If an employee has not reported on a previously issued advance, a new one cannot be issued to him. However, if the employee has not returned the balance of unspent amounts, this does not serve as a basis for non-issuance of the next accountable funds.

When the employee presents supporting documents for the advance report, the final payment is made: the accountable person either returns the unspent part of the money or reimburses the organization for the overexpenditure.

At the same time, it is necessary to explain to the accountable person that in addition to checks issued by the store, he must request invoices, delivery notes and other documents.

For the right to sign on acceptance of goods, a power of attorney is issued to the accountable person. Without receipts, you should not accept invoices and other primary documents, since it will not be possible to confirm expenses without them.

What taxes can be reduced

An advance report makes it possible to reduce the tax base for organizations using the simplified tax system (15%) and reduce the amount of VAT.

For the simplified tax system of 15%, this is explained by the fact that the taxpayer takes into account the expenses incurred, confirming them with receipts and primary documentation for the purchased goods (services).

When purchasing goods and services subject to VAT, the taxpayer has the right to reduce the amount of tax by the specified VAT on checks.

Representation expenses can reduce the tax base when calculating income tax. But not completely: the amount limit is 4% of labor costs in the corresponding tax period. In this case, it is necessary to have supporting documents: an order for the event, a report on the event, an estimate, etc.

Documented travel expenses are exempt from insurance premiums and are taken into account when calculating income tax. Also, daily allowance

in the amount of no more than 700.00 rubles for each day on a business trip in Russia and no more than 2,500.00 rubles for each day on a foreign business trip

are not subject to personal income tax

.

Personal income tax will have to be charged on the amount of excess expenses. It is important to note that food costs are included in the daily allowance and cannot be taken into account separately

.

If the employee has not provided supporting documents for the business trip, then the expenses cannot be taken into account when calculating income tax, and insurance premiums must also be charged on them. But according to the law, you can save on personal income tax and not charge it within the established limits of taxable expenses (700.00 and 2500.00 rubles).

If the employee has not reported on the advance (has not provided an advance report), the previously issued amounts are subject to salary taxes (insurance contributions and personal income tax).

How to accept checks from an accountant

When accepting checks from an accountable person, you must make sure that the expenses are made for the needs of the organization and not in the interests of the individual.

Documents confirming expenses are:

- Cash register receipt;

- Sales receipts/invoices;

- Receipts, strict reporting forms;

- Passenger tickets/boarding passes.

Since July 2021, a QR code has become a mandatory element of the new cash receipt. This detail makes it possible to check the legality of the organization and the purchase being made. In some cases, sellers are allowed to issue a strict reporting form. The tax office may find fault with the completed cash receipt (or BSO) and charge taxes on these amounts. Therefore, you need to review checks for the following points:

- Number, date of the check;

- Time, place of payment;

- Name of organization (full name of individual entrepreneur);

- Taxpayer INN;

- Applicable tax regime, tax rate;

- Sign of payment (payment from the buyer; refund to the buyer, etc.);

- Name of goods (services, works);

- Amount and form of payment (cash/non-cash);

- The position and surname of the person who made the settlement with the buyer;

- CCP registration number;

- Serial number of the fiscal drive model;

- Serial number of the fiscal receipt;

- Shift number;

- Fiscal message sign.

If the check was sent to the buyer by email, the check will contain the sender's email address and the buyer's email address (or subscriber number).

How to draw up a regulation on accountable persons Procedure for drawing up

The unified form AO-1 consists of three parts:

- facial;

- negotiable;

- tear-off receipt.

| Form AO-1 | Details to fill out | Who fills it out |

| Front part of the form |

| Accountant |

| Information about the accountable person (full name, personnel number, position, structural unit) | Accountable person | |

| Tear-off part of the form (receipt) | Details of the accepted advance account | Accountant |

| Reverse side of the form |

| Accountable person |

We spend expenses correctly

First of all, when preparing documents, you must enter the date and number of the advance report. It has been in ordinal terms since the beginning of the year. We register the accountable person and the amount of the advance report.

On the front side please indicate:

- the balance or overspending of the reporting person from the previous advance;

- the amount of the advance received by the accountable person (indicate cash issued and transferred to the card in different lines);

- the amount of funds spent equal to the amount in columns 7-8 of the advance report;

- the amount of the balance or overexpenditure taking into account the previous advance report;

- numbers of accounts (subaccounts) corresponding to column 9 of the reverse side of the advance report.

- in the line “Attachment of documents on sheets” - the number of documents and sheets on which these documents are drawn up;

- the amount of the report for approval (in words and figures).

All lines of the expense report must be completed. If the accountable person is an employee of the organization, then we indicate the structural unit in which he works, personnel number and position. If the advance report is filled out by another individual, then these lines remain empty.

Write down the purpose of the advance. In the names of the indicators, indicate information about previously issued funds: the balance of the amount, or overexpenditure (if any).

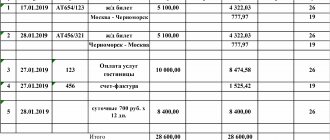

It is important to specify how money is issued: from the cash register, or to a bank card (employee, or corporate card of the organization). Below, write down the final balance, taking into account the previously issued advance and the amounts already spent. In the case of the example, the employee was given 40,000.00 rubles, of which he spent 33,355.27 rubles. He returned the balance in the amount of 6,644.73 rubles to the cashier in the same number with which he filled out the advance report. In the attachment, he provided documents on 2 sheets (the number of checks issued).

The receipt is confirmation that the documents of the accountable person have been accepted and he does not owe funds for the amount for which reasonable expenses were incurred. It indicates the number of documents, the total amount of expenses in figures and words, the date and the person who accepted the documents. In this case, it is the accountant who signs the tear-off part of the first page of the report and affixes the date. This part is detachable and issued to the accountable person.

On the reverse side of the expense report, in columns 1-5, the date and document number, type of document (check, copy of a check) and amount are indicated under the serial number. Lines 7-9 indicate the amounts of expenses accepted for accounting and the numbers of accounts (subaccounts) that are debited for these amounts. Usually this information is provided by an accountant or the head of the organization. If accounting is kept in 1C, then when setting up the program, it will enter the accounting accounts itself. The employee does not fill out these lines.

The accountable person puts his signature only on the reverse side of the expense report. The advance report is drawn up for the amount for which the documents are provided and only this amount will be displayed on the reverse side.

In the advance report, it is necessary to check the intended use of the funds spent, the presence of supporting documents (checks, copies of checks), the correctness of filling out the documents and the correctness of the calculation of the specified amount in the report. That is, you need to look at the receipts to see what exactly was purchased and calculate the amounts of the receipts.

A receipt without indicating goods and materials will only confirm expenses and will not allow goods to be delivered on receipt, so it is necessary to request primary documents from the seller confirming the purchase of goods.

Step-by-step instruction

In an organization, the reporting employee and accountant are responsible for filling out the advance report.

The employee who received the advance funds fills out the front side. Information required:

- short, full name of the organization, its code in accordance with the OKPO classification;

- details of the document - its number and date;

- next, it is necessary to leave a place for the head of the company to endorse the statements - after checking the document by an accountant, the head puts his signature, date and indicates the accountable amount in words;

- last name, first name and patronymic of the accountable person, his position, personnel number and structural unit;

- purpose of the amount issued under the report.

After entering the primary information, the reporting employee must fill out the tabular part of the report.

If you are guided by form AO-1, then the employee must enter information in the left and right tables.

The left table shows data on advances:

- total amount;

- advance monetary unit - ruble or foreign currency;

- balance or overrun (if any).

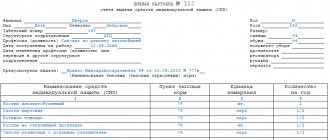

The right table provides accounting information: accounts and subaccounts for which the advance is made, indicating the exact amounts of costs. This part is completed by the accountant.

Next, you need to register supporting documentation: the number of checks and receipts confirming expenses.

The front part of the document contains space for the resolution of the chief accountant. After checking the table information and documents submitted on time, the chief accountant writes down the reporting amount in figures and words.

If there is an overexpenditure on the advance payment or, conversely, a balance of funds, reflect this in the reporting. The incoming (outgoing) cash order on the basis of which transactions with balances were carried out is also indicated.

After the tabular part, the accountant, cashier and chief accountant sign.

Next, fill out the back side.

First of all, the table contains the details and names of all applications - supporting documentation (checks, invoices, tickets, receipts). Write down not only their number and date, but also the exact accounting amount and accounts, sub-accounts on which transactions will be carried out. The tabular part of the reverse side is certified by the signature of the person who received the advance.

At the end, an accountant's receipt is issued, which is cut off and given to the employee. The cut-off part confirms the fact that the employee accounted for the advance payment and provided all the necessary documents. The accountant fills in the following information under his signature: Full name. the responsible employee, details of JSC-1, the amount of the advance in words, the number of supporting documents and the date on which the employee reported. The accountant signs the document only if the reporting is submitted on time.