Let's find out the meaning of the term. This is an event in any organization, in wholesale and retail trade, to search for discrepancies between the fixed working capital recorded in the accounting register and their actual availability. Discrepancies often cause difficulties for the chief economist, because he will have to cover the shortfall in assets from employees in equal shares. And the excess can be used in the manner prescribed in the company’s charter. The incident is recorded in the ledger in the reporting period when the inspection took place. Let's figure out together what it is to capitalize surpluses during inventory, posting, why they appear and how to properly capitalize them.

Audit nuances and purpose

A comparison of information about the material base put on the balance sheet and reflected in the original document and their condition on the day when the reconciliation occurred is mandatory. The timing and procedure of the operation is determined by the manager, except in cases where this is prescribed by the Law of the Russian Federation “On Accounting” No. 402 and Order of the Ministry of Finance No. 34-n of 1998. If there are discrepancies, then measures are prescribed to eliminate the difference that can be taken according to a pre-drawn up and approved plan.

The fact of excess is noted in the accounting department, warehouse papers, where the discrepancy was revealed.

For what reasons do they appear?

Inspection helps to detect discrepancies between the recorded money and its actual availability today. They can be in the form of money, valuables, raw materials for production, movable and immovable property. The inventory commission, not interested in financial turnover, draws up a statement and submits it to the director for consideration. And he, in turn, sets the accounting department the task of ensuring that the department correctly capitalizes and records the excess in the accounting book. An eyeliner is needed when taking inventory of identified surplus fixed assets and materials.

The procedure for recording identified surpluses

If, based on the results of the inventory, excess materials, goods or fixed assets are identified, data about this is entered into the matching statements. These are special documents filled out if deviations between actual and accounting data are identified.

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

The forms of statements (as well as other documents necessary for conducting an inventory) are approved by Decree of the State Statistics Committee of the Russian Federation dated August 18, 1998 No. 88. For fixed assets and intangible assets, the INV-18 form is used, for other goods and materials - INV-19.

These documents contain information about all detected deviations, both up and down. After considering them, the head of the organization decides to reflect deviations in accounting. Shortages can be written off or attributed to the perpetrators; if surpluses are discovered, there can be only one option - capitalization.

A special case is the so-called regrading. It occurs if an inspection simultaneously reveals shortages in some items and surpluses in others. In this case, by decision of the manager, it is allowed to offset surpluses and shortages of homogeneous types of inventory items stored by one materially responsible person (MRP). This procedure is established by clause 5.3 of the Guidelines for inventory of property and financial obligations, approved by Order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49 (hereinafter referred to as the Guidelines for Inventory).

If such a decision has been made, then the capitalization of the surplus is made after offsetting the “homogeneous” shortages.

Business Solutions

- shops clothing, shoes, groceries, toys, cosmetics, appliances Read more

- warehouses

material, in-production, sales and transport organizations Read more

- marking

tobacco, shoes, consumer goods, medicines Read more

- production

meat, procurement, machining, assembly and installation Read more

- rfid

radio frequency identification of inventory items More details

- egais

automation of accounting operations with alcoholic beverages Read more

Main reasons:

- If the reconciliation was carried out inaccurately.

- Large production volumes can lead to errors. When distributing products in a warehouse to customers, there is a high probability of unaccounted deliveries.

- An insufficient amount of working finance is introduced.

- Errors in warehouses when taking into account the issue of materials and products. That is, they issued a smaller batch than expected.

- During the release of goods, some models were accidentally replaced by others.

Verification steps

Everything must be carried out according to the plan drawn up by the leader. Moreover, the stages are observed in the following order:

- Preparation period. An order from the director is issued, which specifies the deadline for carrying out what is considered. A special commission of several people is created, where a chief is appointed. Those persons who will be responsible if inconsistencies are found during the inspection are determined.

- It all starts with creating an inventory of existing production property with a description of its appearance today.

- A comparison sheet is created, which reflects the information obtained during the inspection, as well as the information captured in the original documents.

- In case of discrepancy, a report is drawn up where everything will be indicated.

- Based on the data received, a certificate is issued. In addition, changes are made to the balance sheet, where missing money or other valuables are written off. And capitalized surpluses identified during inventory in a budgetary institution, VAT and profit are reflected by the accountant’s posting.

The inventory company must report at each stage to the head of the company and the chief economist.

Capitalization of surplus during inventory: registration

The inventory is regulated by the Methodological Instructions of the Ministry of Finance of the Russian Federation (approved by order No. dated June 13, 1995). The main stages of this procedure are:

- preparation and publication of an order determining the composition of the inventory commission;

- carrying out inspections, preparing inventories;

- documentary summing up of results with their reflection in reconciliation statements.

When surpluses are identified, after comparing actual data with accounting data, the inventory commission finds out the prerequisites for the appearance of “extra” assets, requests explanations from financially responsible persons, analyzes methods for reflecting inventory results, and the manager issues an order to accept the surplus for accounting. This document becomes the basis for the accountant’s actions; it reflects the list of asset positions subject to capitalization.

Why is the inspection carried out?

It solves multiple problems that arise during the operation of an enterprise and its employees:

- The financially responsible person should be replaced periodically.

- It's no secret that large plants and factories sometimes employ "unclean" employees. If premises and workshops are not equipped with a security camera, then frequent reconciliations help to identify facts of theft.

- Force majeure also occurs when a farm suffers from various natural disasters (hail, flood, fire due to lightning).

- Questions when there is a change of management, sale of movable and immovable property, leasing, rental of premises or vehicles.

- Before drawing up the annual report, there must be control.

In addition to the above reasons for conducting a recount, the most common is constant monitoring of the condition and quantity of property of the enterprise. Therefore, a schedule for the procedure is drawn up in advance once a year. Typically this includes three to four inspections throughout the year.

Who is appointed to the verification commission?

For maximum objectivity and to avoid collusion between inspectors, uninterested specialists from different fields of activity are usually invited. For example, if a warehouse is being inspected, then a warehouse worker who knows what is located and where is allowed to be present. In addition to him, two people working in other departments are involved. This could be: a workshop foreman, a commodity specialist or a finance specialist. Recently, third parties are often invited for examination, since for a reward they will not commit a crime and will conduct a high-quality inspection.

What to do if the inspection reveals excess

When discrepancies are discovered, the established inspection committee carefully studies the audit extracts, finds out the reasons for this, and draws up a report of violations. Next, the employees draw up a protocol, which states the results of the work done, the reasons, explanatory notes from the financially responsible persons and the conclusions of the specialists.

Next, the document is referred to the manager who studies the issue. And he decides with the chief accountant how best to carry out the postings. The reporting indicates the data that was recorded during the comparisons. The annual report must also reflect and document the surpluses identified in the cash register during the inventory.

If there are discrepancies, then funds should be accounted for at the market price valid for today. All invoices received from contractors are raised. If there are none, then you can find out prices in another way, for example, look at advertisements or request information from the statistics department.

For correct reporting, the accountant should capitalize the received data using postings.

Audit

The process is carried out in stages, compliance is strictly regulated:

- A commission of three people who are not interested in money circulation is formed.

- The director's order will contain items on the composition of the inspection committee, the reasons for the process, and the date of implementation of audit actions.

- Next is an inventory of all property.

- The last one is a comparison of established facts and information reflected in the balance sheet. The results are written down in a separate form, which refers to the manager to determine further orders.

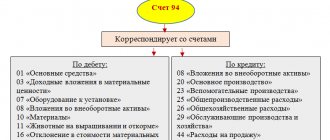

Accounting and posting - postings

A copy of the INV-15 act is sent to the accounting department to perform the necessary accounting actions. The accountant makes the necessary postings (account correspondence).

Cash surpluses are recorded by accounting in the month of completion of the relevant check and, if an inventory was carried out, are accounted for on the date of acceptance of the detected cash.

If an annual audit was carried out, its results are reflected in the annual reports.

Identified excess cash in the cash register is reflected in accounting entries using the following entries:

| Operation (description) | Debit | Credit |

| Reflects cash revenue identified upon verification of cash register systems. | 50 | 90 |

| Cash surplus is capitalized as other income of the organization | 50 | 91 |

Business Solutions

- the shops

clothes, shoes, products, toys, cosmetics, appliances Read more

- warehouses

material, in-production, sales and transport organizations Read more

- marking

tobacco, shoes, consumer goods, medicines Read more

- production

meat, procurement, machining, assembly and installation Read more

- rfid

radio frequency identification of inventory items More details

- egais

automation of accounting operations with alcoholic beverages Read more

What to do if found

This situation occurs when accounting is incorrect. Rarely, but thefts are detected. You need to properly understand all the documentation. To do this, the accounting department writes off the shortage or enters it into the “Expenses” section, and the excess is capitalized. It is very important to carry out the entire procedure on the day of control. In addition, the director’s order to initiate an inspection is the main document for resolving the issue.

A sample order for the posting of surplus during inventory is not provided by government agencies. Therefore, the form can be varied and approved in accordance with the internal charter of the enterprise.

How the director's instructions are carried out

How to correctly capitalize surplus fixed assets identified during inventory, liners: D 10, 41, 01, 50 K 91-1 9 (they are used for correct reporting).

- If misgrading occurs, then it is possible to offset the missing and excess goods.

- If there is a lack of finances, they are repaid by the efforts of people who are endowed with financial responsibility. You can act in other ways; the difference in amounts is sent to account 91-1 marked “Other expenses”. Keep in mind that this is done at the time of audit and market value is taken into account.

Posting and timing of capitalization of surplus in accounting

Surplus property identified during inventory is included in other income (account 91.1). The corresponding account depends on what type of value is accounted for:

Dt 01 (08, 10, 41, 43, 50) Kt 91.1.

If the inventory is carried out to confirm the reliability of the annual report, then the posting of identified surplus materials as a result of the inventory is made no later than the reporting date, i.e. December 31 of the corresponding year.

In other cases (for example, when changing the MOL), the posting must be made in the same month in which the inventory was completed (clause 5.5 of the Inventory Guidelines).

What to do with excess materials, raw materials and goods

Often, excess raw materials or products delivered to wholesale warehouses remain in production. The last day on which you can capitalize excess materials (cash or accrual method) in the annual report is no later than the 31st day of the last month.

In this case, the accounting department has to decide how to reflect the surplus during inventory and at what price to capitalize it. To do this, they include non-operating expenses in the cost of excess items, and also compare invoices or study offers on the market in a specific area.

Capitalization of surplus during inventory: postings using examples

We present examples of the receipt of the value of property identified by inventory.

Example 1

On March 15, 2019, during an audit of cash in the company’s cash desk, a surplus of 15,000 rubles was identified, which should be capitalized on the date of the inventory. The accountant recorded this transaction with the following entry:

Dt 50 Kt 91/1 in the amount of 15,000 rubles.

Example 2

The inventory on March 20, 2019 revealed an unaccounted fixed asset item - a milling machine worth 100,000 rubles. (price is determined based on current market prices). The surplus was capitalized during inventory. Wiring:

Dt 01 Kt 91/1 – in the amount of 100,000 rubles.

Example 3

On March 22, 2019, excess materials worth RUB 12,000 were installed at the company’s warehouse. The amount of surplus is determined based on the market price of inventory items on the inventory date. Their acceptance for accounting is accompanied by posting:

Dt 10 Kt 91/1 – 12,000 rub.

Excess production materials

The law of the Russian Federation very clearly states that an enterprise can include no more than 24 percent of the price of goods or raw materials from the market price in costs. You will not hear specific demands from Federal Tax Service employees. The only thing that needs to be taken into account is the impossibility of including in the enterprise’s expenses the entire cost of excess materials identified by the commission. You will most likely have to sell them off. And to avoid problems with the tax authorities, take into account the previously established price on the sales market.

Fixed Asset Usage Details

Control means not only a comparison of the information obtained in the process about the product, materials, raw materials base with the information recorded in the primary statutory documentation, but also the recalculation of fixed capital.

In this case, a completely different technique is used:

- Excesses are classified as unrealized income.

- Assets that are under repair are described in a statement in the INV/10 form, which indicates the price of repair work.

- For property leased or for temporary storage, a document is drawn up, in which all relevant papers from the counterparty will be attached, confirming the legality of the action.

- A special commission draws up a report on operating systems that cannot be restored and are unsuitable for use.

- If the book price of capital has changed in one direction or another, then this fact is also displayed.

- The funds must be equated to the income that could not be realized, and appropriate depreciation must be charged on it within the limits of the value declared by the market and actual depreciation.

Acceptance of surplus property into accounting

As a result of the inventory, excess property may be identified in the company.

These may be fixed assets, intangible assets, materials, finished products and goods. How to accept such inventory “fruits” for accounting and taxation? Inventory in order

Inventory can be carried out at the company on a voluntary or mandatory basis. Cases when a company must necessarily check property are spelled out in paragraph 2 of Article 12 of the Law of November 21, 1996 No. 129-FZ “On Accounting” and paragraph 27 of the Regulations on Accounting and Financial Reporting (approved by order of the Ministry of Finance dated July 29, 1998 No. 34n). For example, this must be done before drawing up annual financial statements (in this case, fixed assets can be checked no more than once every three years), when changing financially responsible persons, when facts of theft are detected, in the event of a fire, etc.

At its discretion, the company can conduct an inventory at any time. The number of inventories for the reporting year, the timing of their implementation and the list of inspected property (liabilities) must be established by the head of the company (by order).

The general procedure for conducting an inventory is set out in detail in the Methodological Guidelines for the Inventory of Property and Financial Liabilities (approved by Order of the Ministry of Finance dated June 13, 1995 No. 49, hereinafter referred to as the Guidelines). The selected verification mechanism must be fixed in the accounting policy of the company (clause 2 of PBU 1/98, approved by order of the Ministry of Finance dated December 9, 1998 No. 60n).

The results of the inventory are documented in an inventory list or an inventory act (clause 2.5 of the Methodological Instructions). For each type of property, its own form of such a document is filled out (clause 1.2 of Goskomstat Resolution No. 88 of August 18, 1998 “On approval of unified forms of primary accounting documentation for recording cash transactions and recording inventory results”). For example, when registering the results of an inventory of fixed assets - INV-1, intangible assets - INV-1a, inventory items in storage locations - INV-3.

In addition, if the inspection reveals excess property, you must also fill out a matching statement. The matching statement is drawn up only for those assets for which deviations from the accounting data have been identified (clause 4.1 of the Methodological Instructions). For example, when a surplus of fixed assets is detected, a matching statement INV-18 is drawn up, and a matching statement of inventory items is compiled - INV-19.

Inventory “fruits”

The surplus identified by the results of the inventory must be accepted for accounting. They must be taken into account at market value. This requirement is contained in subparagraph “a” of paragraph 28 of the Regulations on Accounting and Reporting. In this case, the market value is understood as the amount of money that can be received as a result of the sale of these assets. Information about the level of current market prices must be confirmed by documents or through an examination. This follows from paragraph 10.3 of PBU 9/99 (approved by order of the Ministry of Finance dated May 6, 1999 No. 32n).

In the accounting accounts, surpluses are reflected at the time of completion of the inventory (drawing up an inventory list, act) or on the date of drawing up the annual financial statements (clause 5.5 of the Methodological Instructions).

The following wiring is done:

Debit 01, 10, 41, 43... Credit 91-1 - reflects the cost of surpluses identified during inventory.

When surpluses are used in activities or when they are sold, the market price of these assets is written off as expenses. This is reflected by the following entry:

Debit 20, 26, 25, 29, 44, 90-2 Credit 02, 10, 41, 43…

When calculating income tax, surplus inventories and other property that are identified as a result of inventory are recognized as non-operating income (clause 20 of Article 250 of the Tax Code).

Since income was received in kind (surplus property), when determining the tax base, they must be taken into account based on market value (clause 5 and clause 6 of Article 274 of the Tax Code). In tax accounting, the market price of surplus must be determined following the requirements of Article 40 of the Tax Code.

Thus, if a company has identified a surplus of property (goods, finished products) that it sells, the market value can be established based on market prices for identical (homogeneous) goods that the company sells under comparable conditions (clause 9 of Article 40 of the Tax Code). In this case, it is necessary to take into account only those transactions that are concluded between persons who are not interdependent (the grounds for the interdependence of firms are specified in Article 20 of the Tax Code). If a company has identified a surplus of property that it does not sell itself (fixed assets, intangible assets, materials), it is necessary to use prices for similar products on the market (clause 9 of Article 40 of the Tax Code). To do this, you can use the price list of a company selling similar products (letter of the Ministry of Finance dated January 5, 1999 No. 04-02-05/1). For example, the prices of the supplier from whom the surplus property was purchased.

Both when calculating income tax using the accrual method and when using the cash method, the market value of the surplus must be included in income at the time it is accepted for accounting. That is, on the date of completion of the inventory. This follows from paragraph 1 of Article 271 and paragraph 2 of Article 273 of the Tax Code.

So, in tax accounting, surpluses identified based on inventory results form income. What about expenses?

Paragraph 1 of Article 252 of the Tax Code establishes that firms have the right to reduce the income received by the amount of expenses incurred (except for the expenses specified in Article 270 of the Tax Code). Expenses are recognized as justified and documented costs incurred by the organization. Thus, if a company intends to use the identified surplus for revenue-generating activities, its value must be included as an expense.

However, this issue is not so simple.

Material surplus

The Tax Code allows only the cost of surplus inventories (MPI) to be clearly included in the reduction of taxable profit. When used in production (when performing work, providing services), they can be written off as material expenses. But not in the full market value, but only in the amount of 24 percent (the amount of income tax) of the non-operating income that it generated.

The formula for calculating the value of surplus inventories, which can be included in the reduction of taxable profit, is as follows:

| The cost of surplus inventories, which is included in expenses when calculating income tax | = | Non-operating income in the amount of the market value of identified surplus inventories | × | Income tax rate |

According to the Ministry of Finance, the same calculation procedure can be applied in the case of the sale of surplus inventories (letters of the Ministry of Finance dated December 18, 2006 No. 03-03-04/1/841 and dated March 2, 2007 No. 03-03-06/1 /146).

Let us remind you that in accounting there are no such restrictions on writing off surpluses as expenses. As a result, a constant difference arises between the accounting and tax costs, with which a permanent tax liability must be calculated (clauses 4 and 7 of PBU 18/02, approved by order of the Ministry of Finance of November 19, 2002 No. 114n).

Example 1

In February 2008, Gamma OJSC carried out an inventory. Based on its results, a surplus of raw materials in the amount of 100 kg was identified. Its market value is 1000 rubles/kg. In the same month, excess raw materials were transferred to production.

In February 2008, Gamma’s accountant made the following accounting entries:

Debit 10-1 Credit 91-1 - 100,000 rubles. (100 kg × 1000 rub./kg) - surplus raw materials were capitalized in accordance with the matching sheet of inventory results;

Debit 20 Credit 10-1 - 100,000 rub. — reflects the transfer of raw materials to production.

Gamma pays income tax monthly. In February 2008, the accountant included 100,000 rubles in taxable income and 24,000 rubles in expenses. (RUB 100,000 × 24%).

Thus, in accounting, expenses are equal to 100,000 rubles, and in tax accounting - 24,000 rubles. Since the difference is 76,000 rubles. (100,000 rubles – 24,000 rubles) is not taken into account in tax accounting in any reporting period; a permanent difference arises in accounting. Based on this, the Gamma accountant recorded a permanent tax liability:

Debit 99 Credit 68 - 18,240 rub. (RUB 76,000 × 24%) - reflects a permanent tax liability.

Other property

As for accounting for excess other property (fixed assets, intangible assets, goods, finished products) in expenses, this issue is not clarified in the legislation. However, the Ministry of Finance recently expressed its position on this matter. It concerns the write-off as expenses of used surplus fixed assets and intangible assets worth more than 20,000 rubles.

Thus, in a new letter dated January 25, 2008 No. 03-03-06/1/47, employees of the financial department made a disappointing conclusion. The Tax Code does not provide a mechanism for taking into account the cost of excess depreciable property in the tax cost.

The fact is that in order to write off the cost of such surpluses as expenses, it is necessary to establish their original cost. This is required to calculate depreciation on them. However, tax law does not explain how to do this. It is also impossible to recognize the identified surplus as property received free of charge (for which a special procedure for determining the value is prescribed). This is due to the fact that for profit tax purposes, property is considered to be received free of charge if its receipt is not associated with the occurrence of a counter-obligation on the part of the recipient (clause 2 of Article 248 of the Tax Code). That is, gratuitous receipt presupposes the presence of two parties: the recipient and the transmitter. And when surpluses are identified, there is no transmitting party.

Consequently, the initial cost of depreciable property identified by inventory results cannot be established. Therefore, it should be considered equal to zero. Accordingly, depreciation is not accrued in tax accounting (clause 1 of Article 256 of the Tax Code).

Since in accounting the cost of excess depreciable property can be gradually expensed (depreciated), but not in tax accounting, a permanent difference will arise. A permanent tax liability must be accrued from it (clauses 4 and 7 of PBU 18/02).

Example 2

In February 2008, Gamma OJSC carried out an inventory. Based on its results, a surplus of fixed assets was identified in the amount of 1 unit. grinding machine. Its market value is 22,000 rubles. In the same month, the surplus fixed assets were put into use.

Depreciation of fixed assets in accounting is calculated using the straight-line method. The useful life of the machine is set at 5 years (60 months).

In February 2008, Gamma’s accountant made the following accounting entries:

Debit 01 Credit 91-1 - 22,000 rubles. — surplus fixed assets are capitalized in accordance with the matching statement of inventory results.

Starting from March 2008 (during the entire useful life of the fixed asset), Gamma’s accountant reflected the depreciation charge:

Debit 20 Credit 02 - 367 rub. (RUB 22,000: 60 months) - depreciation was accrued on the fixed asset.

Gamma pays income tax monthly. In February 2008, the accountant included 22,000 rubles in taxable income. But he did not begin to charge depreciation on the commissioned machine.

Thus, in accounting, the company’s expenses monthly starting from March 2008 amount to 367 rubles, and in tax accounting - 0 rubles. Since the monthly difference is 367 rubles. is not taken into account in tax accounting in any reporting period, a permanent difference arises in accounting. Based on this, the Gamma accountant records a permanent tax liability on a monthly basis:

Debit 99 Credit 68 - 88 rub. (RUB 367 × 24%) - reflects a permanent tax liability.

This position of officials is not controversial. As a general rule, part of the property used as means of labor for the production and sale of goods (work, services) is classified as fixed assets (clause 1 of Article 257 of the Tax Code). However, Article 256 of the Tax Code does not prohibit the depreciation of such objects identified as a result of the inventory.

As for the initial value of surplus property, the Ministry of Finance previously allowed it to be determined in the same way as for assets received free of charge (letter of the Ministry of Finance dated June 20, 2005 No. 03-03-04/1/7). Namely: at market value (paragraph 2, paragraph 1, article 257 of the Tax Code). That is, in the same assessment that supplemented the firm’s non-operating income as the price of surplus. Based on this value, depreciation can be calculated in tax accounting.

In arbitration practice, although not related to the Moscow District, there was also a precedent when the court recognized the right of a company to determine the initial cost of fixed assets identified during an inventory in the same manner as for property received free of charge (see, for example, the FAS resolution East Siberian District dated April 16, 2007 No. A33-8921/2006-F02-1794/2007). So the company has a chance to defend this approach in court.

Let us note that regarding the sale of surplus property, the position of officials is also unchanged. When any surplus other property is sold, it is treated as goods for tax purposes. The rules for writing off the value of these assets when calculating income tax are prescribed in Article 268 of the Tax Code. It says that when selling goods, you can take into account the costs of their acquisition to reduce the tax base. However, the Tax Code, in analogy with fixed assets, does not contain explanations of what to take as the cost of acquiring surplus other property (goods, finished products). Therefore, the controlling services also recognize this amount as zero. This is stated in letters from the Ministry of Finance dated February 15, 2008 No. 03-03-06/1/97 and UMNS for Moscow dated February 9, 2004 No. 26-12/08042. In this case, income from sales is required to be reflected.

Please note: if an organization sells property identified as a result of an inventory, VAT must be charged on such a transaction. But when using “excess” property in production, you do not need to pay VAT. This conclusion is confirmed by the letter of the Ministry of Finance dated September 1, 2005 No. 03-04-11/218.

Conclusion

We tried to tell you and show you with specific examples what inventory surplus is, how capitalization occurs and how income tax and VAT are calculated. We recommend that you use software, for example, from . The program will help you organize your workplace correctly and prevent fatal failures in reporting. Qualified specialists will provide free consultations on installation and configuration.

Here is a visual demonstration of property inventory in organizations using Mobile SMARTS and a set of equipment.

If your enterprise uses “1C: Accounting” in any delivery, “1C: UPP” or 1C for a construction organization, and you plan to carry out inventory only on barcodes (you will not use RFID), then a special driver for inventory is completely suitable for you from Cleverens, the delivery package of which includes all the programs and processing necessary for both printing labels and working with the data collection terminal.

If you are planning to implement RFID, then another program is suitable for you - Cleverence: Property Accounting. Number of impressions: 6175

Not too much extra

As a result of the inventory, surpluses may be identified that must be capitalized. Many accountants have problems with this. You need to start by valuing the goods at market value at the time of discovery.

This is reflected by the following wiring:

Debit 41 Credit 91.1 – surplus goods are capitalized.

The main thing you need to pay attention to is tax accounting. The fact is that, in accordance with paragraph 250 of the Tax Code, surpluses identified as a result of inventory must be included in the company’s non-operating income. This means that they must be taken into account when calculating income tax. In addition, in accordance with paragraph 2 of Article 254 of the Tax Code, when determining the amount of material expenses, the cost of the surplus is determined as the amount of income tax calculated from non-operating income. That is, it will be possible to write off as losses not the entire market value of capital assets, but only the amount of income tax paid in connection with the found inventory.