What is KBK and where should it be indicated?

The budget classification code (BCC) shows where the state receives its revenues and where its expenses are directed. The KBK system was created to regulate financial flows; with their help, a budget program is drawn up at the level of the state and constituent entities.

Organizations and entrepreneurs using the simplified tax system should also know and use KBK in payments. Whether the tax authorities will take this payment into account or not depends on the correctness of filling out the order. If the tax office does not see the tax on time, it can collect it unilaterally and charge penalties. In 2021, as in the past, field 104 is provided in the payment form for KBK.

The simplified single tax is paid for the quarter in the form of advance payments until the 25th of the next month. Tax for the year is paid by organizations until March 31 and until April 30 by individual entrepreneurs. To transfer tax, fill out the payment form correctly and indicate the correct BCC depending on the object of taxation and the purpose of the payment.

Purpose of payment under the simplified tax system “income”

Identification of tax according to the taxable object used by the payer is carried out not only by the “purpose of payment” field, but also by the budget classification code, therefore, in field 104 of the payment order, the corresponding BCC should be indicated.

The purpose of payment for this object corresponds to KBK 182 1 05 01011 01 1000 110.

In the “purpose of payment” field when paying the simplified tax system for 2021, the following entry should be reflected: “Tax paid in connection with the application of the simplified taxation system (USN, income) for 2016.”

KBK simplified tax system "income" in 2021 and 2021

For the simplified tax system “income”, a standard rate of 6% and an increased rate of 8% are applied (the standard rate may be lower - we wrote about rates in the regions here). It only taxes the income of the organization. The Ministry of Finance made the latest changes to the list of codes by order No. 297n dated December 7, 2021, but the BCC for the simplified tax system of 6% remained the same. The codes for taxes, penalties and fines are different.

- Tax and advance payments - 182 1 0500 110

- Penalty — 182 1 0500 110

- Interest — 182 1 0500 110

- Fines - 182 1 0500 110

For tax not paid on time, the Federal Tax Service charges penalties for each day of delay. There is a special KBK for their payment, as well as for fines. The differences between these codes are only in characters 14 to 17. Tax - 1000, penalties - 2100, fine - 3000.

Where to find KBK for simplified tax system

Budget classification codes are generated by the Ministry of Finance, so you need to look for them in the current orders of this department. In 2020, the BCC from orders No. 85n dated 06/06/2019 and N 207n dated 11/29/2019 applies to individual entrepreneurs and legal entities. Both orders were edited on March 10, 2020.

The first order describes the procedure for generating codes, their structure and principles of purpose, and the BCCs themselves are listed in order N 207n. Since these documents are freely available, you can always check in them whether the details for payment to the budget are correct.

There are two different objects of taxation on the simplified tax system: “Income” and “Income minus expenses”. They have different budget classification codes, so choose the appropriate table for yourself. Please also note that the codes of one version of the simplified tax system are different for tax payments, penalties and fines.

However, the presence or absence of employees, as well as the organizational and legal form of the taxpayer, does not matter. Therefore, for example, KBK USN Income for transfer of tax payment - 182 1 0500 110 - must be indicated by entrepreneurs without employees, individual entrepreneurs, and organizations in this mode.

KBK USN Income for 2021

| Purpose of payment | KBK payment |

| Tax and advance tax payments | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

| Penalties for late payment of taxes | 182 1 0500 110 |

KBK USN Income minus expenses for 2021

| Purpose of payment | KBK payment |

| Tax and advance tax payments | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

| Penalties for late payment of taxes | 182 1 0500 110 |

*The minimum tax is credited to the same BCC as the tax calculated in the usual way, this procedure is valid from 2021

For existing simplifiers, there is nothing new in these codes, because Order of the Ministry of Finance N 207n dated November 29, 2019 left the majority of BCCs for tax payments unchanged.

However, it is worth paying attention to the new budget classification codes that have been added for fines for various tax offenses. Previously, they all went to a single KBK (182 1 16 03010 01 6000 140), but now this code does not work.

Regardless of which version of the simplified tax system you work on - simplified tax system 6 or 15 percent - penalty payments are transferred to these BCCs:

- unsubmitted declaration – 182 1 1602 140;

- violated method of filing declarations and settlements - 182 1 16 05160 01 0003 140;

- gross violation of accounting standards – 182 1 1605 140;

- information not provided for tax control – 182 1 16 05160 01 0007 140;

- documents submitted by the tax agent with false information – 182 1 1608 140.

KBK simplified tax system “income minus expenses” in 2021 and 2021

The cloud service Kontur.Accounting helps generate payment orders with current BCCs for paying taxes. Get free access for 14 days

The simplified version with the object “income minus expenses” has other BCCs, which depend on the purpose of the payment. There have been no changes to the KBK simplified tax system of 15% in 2021, so please indicate the following codes in the payment order:

- Tax and advance payments - 182 1 0500 110

- Penalty — 182 1 0500 110

- Interest — 182 1 0500 110

- Fines - 182 1 0500 110

As you can see, the codes for different taxation objects are practically the same. 19 out of 20 digits match, the difference is only in the 10th digit. When transferring tax on the “income minus expenses” object, always make sure that the 10th digit is the number “2”.

KBK codes according to the simplified tax system “income” 6% in 2019–2020

Incorrect indication of the income code should not lead to major troubles. After all, even if the BCC is incorrect, the money will go to the budget, and this payment details can always be clarified.

However, the fact that a mistake will not entail sanctions should not discourage you. In any case, this is a waste of time and nerves. Therefore, changes in the BCC need to be monitored. Moreover, it is not at all difficult for payers using the simplified tax system to do this with the object “income”: the codes for them have not changed since 2014.

The BCC for the simplified tax system for 2014–2017 for various taxation objects (including the BCC for the simplified tax system of 15% for 2014–2017) can be clarified in reference books. We are now only interested in the BCC under the simplified tax system of 6% for 2019–2020. They are shown in the table.

IMPORTANT! The list of BCCs for 2021 is determined by Order of the Ministry of Finance dated November 29, 2019 No. 207n, and for 2021 it was established by Order of the Ministry of Finance dated June 8, 2018 No. 132n. Find out which BCCs have changed since 2021 here.

Codes according to the simplified tax system “income” 6% for 2019–2020

| Year | Tax | Penalty | Fines |

| 2019 | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| 2020 | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

As you can see, the KBK according to the simplified tax system “income” of 6% for 2021 for each type of payment is no different from the KBK according to the simplified tax system “income” for 2019 for the same types of payments. The difference in the codes for the main tax, penalties and fines is only in one digit - in the 14th digit, which characterizes the subtype of budget revenues.

Instructions for filling out payment slips for the payment of advance payments under the simplified tax system, as well as tax for the year, including samples of payment slips, were prepared by K+ experts. If you have access to K+, go to the Ready Solution. If you don't have access, get it for free.

KBK simplified tax system 2021 for minimum tax

For simplifiers with the object “income minus expenses”, it is mandatory to pay a minimum tax. When the tax amount for the year does not exceed 1% of your income, you will have to pay a minimum tax of 1% of income.

When filling out a payment order, please note that from 2021, the same BCC is applied to transfer the minimum tax as for advance payments on the simplified tax system of 15%. Therefore, when transferring the minimum tax, in field 104 indicate KBK 182 1 0500 110. The codes have been combined to facilitate the work of the Federal Tax Service. They can now automatically count advance payments made for the year toward the minimum tax.

KBK 2021 IP USN "Revenue"

Budget classification codes for paying tax fees under the simplified taxation system “Income” in 2021 remained the same as they were in 2021. It must be taken into account that the main payment, penalties and fines for late or incomplete payment of tax must be transferred to different codes. Otherwise, the payment will be credited to the wrong account.

KBK USN "Income" IP 2021:

- 182 – payment administrator Federal Tax Service;

- 105 – tax system “USN”;

- 0101101 – payment is sent to the Federal budget, subgroups, code, income subitem;

- 1000 – tax (basic payment), for penalties – “2100” and fines – “3000”;

- 110 – tax revenues.

Table KBK simplified tax system “Income” 2021 IP

| Purpose of payment | KBK |

| Basic payment | 182 1 0500 110 |

| Fine | 182 1 0500 110 |

| Penalty | 182 1 0500 110 |

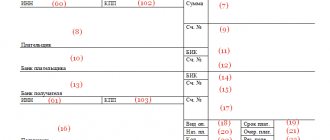

In the payment order, the budget classification code is indicated in field “104”. If the BCC is incorrect, the funds will be credited to the wrong account. As a result, the company will be subject to penalties. They must be paid as quickly as possible, having previously clarified the details. To do this, you must submit an application to the Tax Service.

The form of the payment order is given in Appendix 2 to Bank of Russia Regulation No. 383-P dated June 19, 2012. For ease of filling out, each field is assigned a number (a form with numbered fields is given in Appendix 3 to the specified Regulations). The payment order for tax payment must be filled out in accordance with the filling rules given in Appendices No. 1, 2, 5 to Order of the Ministry of Finance of Russia No. 107n dated November 12, 2013 (as amended on April 5, 2017).

KBK simplified tax system for individual entrepreneurs

The cloud service Kontur.Accounting helps generate payment orders with current BCCs for paying taxes. Get free access for 14 days

Individual entrepreneurs using the simplified tax system are wondering which KBK they should use to pay a single tax. According to Art. 346.21 of the Tax Code of the Russian Federation, individual entrepreneurs pay tax in the general manner. For individual entrepreneurs, the simplified tax system does not provide for separate BCCs; they are the same for individuals and legal entities. The only difference is the timing of tax payment; individual entrepreneurs can pay the final tax payment for the year before April 30, and not until March 31, like an organization.

KBK according to the simplified tax system in 2021 for LLCs and individual entrepreneurs

The article contains all the BCCs according to the simplified tax system for 2021 for LLCs, JSCs and individual entrepreneurs.

In the article you will find:

- BCC for simplified tax system “Income” 6% in 2021 for individual entrepreneurs and legal entities (JSC and LLC)

- BCC for the simplified tax system “Income minus expenses” 15% for individual entrepreneurs and legal entities (JSC and LLC)

- Minimum tax codes

- Codes for penalties and fines

There is no difference between the BCC for LLCs and individual entrepreneurs using the simplified taxation system. The key point is only the object of taxation.

Download table with codes

What are the consequences of an incorrect KBK in a payment order?

The absence or incorrect indication of the code may result in the payment being among the unknown. The responsibility for indicating the correct BCC lies with the taxpayer, since the codes are enshrined in law. If you indicated the wrong code, but the payment was received by the budget, send an application to the Federal Tax Service to clarify the payment. The tax authority will recalculate penalties for the period from the date of payment until the payment is clarified. In Art. 45 clause 4 of the Tax Code of the Russian Federation specifies two types of errors in which the payment will not be counted: an incorrect treasury account number or an error in the name of the recipient bank. In this case, a different procedure for correctly determining the payment applies.

Values

KBK USN “6” in 2021 is used the same as in previous years. Although the Order on approval of budget classification codes is issued by the Ministry of Finance annually, the values themselves may not change with such frequency. For 2021, the list of indicators was approved by Order of the Ministry of Finance dated 06/08/2018 No. 132n.

| Payment | Tax | Penalty | Fine |

| Fulfillment of the financial obligation to pay a single fee under the simplified taxation system, object “income” | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| simplified tax system, object “income minus expenses” (incl. minimum tax) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

Payment period

So, we have determined where in the payment order to enter the BCC for individual entrepreneurs using the simplified tax system “6”; In 2021, tax payment is made in four payments per year. Advances must be transferred based on the results of the quarter, half a year, nine months and make the final payment for the year. Advance payments, according to Art. 346.21 of the Tax Code of the Russian Federation, are transferred until the 25th day of the month following the reporting one, the final fee according to the simplified tax system - until March 31 of the year following the reporting one (that is, for 2021 - until 03.31.2019). In 2021, the payment deadline has been postponed to April 1 due to the fact that March 31 falls on a Sunday.

Table of payment deadlines

| Reporting period | Deadline for payment |

| 2018 | 01.04.2019 |

| I quarter | 25.04.2019 |

| I half of the year | 25.07.2019 |

| 6 months | 25.10.2019 |

| 2020 | 31.03.2019 |