In what case is it possible to use two special modes?

Let us recall that Federal Law No. 325-FZ dated September 29, 2019 added three groups of goods subject to mandatory labeling to the list of goods that cannot be sold within the framework of imputation.

As a result, from January 1, a ban is introduced on the use of UTII in the retail trade of labeled medicines and fur products, and from March 1 - in labeled footwear. In this regard, the following question becomes relevant: can a taxpayer retain the right to UTII for retail if he also applies the “simplified system”, within which he takes into account income from the sale of labeled products. Keep records and prepare reports on UTII for free in 2021, taking into account new deflator coefficients

Recently, the Ministry of Finance admitted that this is quite acceptable. But “subject to the provisions of Chapters 26.2 and 26.3 of the Code” (letter dated November 13, 2019 No. 03-11-11/87500). And this is where problems await taxpayers.

Conditions for combining UTII and simplified tax system

The fact is that, on the basis of paragraph 4 of Article 346.12 of the Tax Code of the Russian Federation, organizations and individual entrepreneurs that have switched to paying UTII for one or more types of activities have the right to apply the simplified tax system only in relation to other types of activities they carry out. This means that for the same type of activity (for example, retail trade through stores with a sales area of no more than 150 square meters for each facility), carried out on the territory of one municipal district or on the territory of several districts of one urban district, cities federal significance, it is impossible to apply UTII and simplified tax system at the same time. Such clarifications were repeatedly given by both the Ministry of Finance (letters dated 08/09/13 No. 03-11-11/32275 and dated 07/24/13 No. 03-11-11/29241) and the Federal Tax Service (letter dated 08/01/13 No. ED-4-3/ [email protected] ).

At the same time, officials note that the taxpayer has the right to switch to “imputation” for retail outlets that are located in one municipal area (city district, federal city), and at the same time apply the simplified tax system for retail outlets located in another municipality, where for this type of activity he is not registered as a UTII payer (letters from the Ministry of Finance dated 01.07.13 No. 03-11-06/3/24980 and dated 20.12.12 No. 03-11-06/3/89).

With this approach, is it possible to combine UTII for retail and the simplified tax system for trade in “non-retail” goods specified in Article 346.27 of the Tax Code of the Russian Federation (excise motor oil, gas, buses, goods of own production, etc.)?

Yes, it is possible, since trade in “non-retail” goods is, in principle, not an “imputed” type of activity. This means that in this case it cannot be said that the combination is carried out for the same type of activity - we are talking about two different types. Therefore, one of them may be on the “imputation”, and the second on the “simplified” (letter of the Ministry of Finance dated September 11, 2012 No. 03-11-11/276). It does not matter where “imputed” retail and trade on the simplified tax system are carried out - in the same or in different municipalities. This combination is possible even if “retail” and “non-retail” goods are sold in the same store.

Keep records for LLC using UTII or simplified tax system (three months as a gift)

Changes since the beginning of 2021

However, from January 1, 2021, this logic will no longer work. Law No. 325-FZ introduced a norm into paragraph 2.3 of Article 346.26 of the Tax Code of the Russian Federation, the meaning of which is as follows: a “retail dealer” who has made at least one “non-retail” sale loses the right to use this special regime. That is, according to the new rules, the possibility of combining UTII and the simplified tax system for trade in “non-retail” goods (including those mentioned in Article 346.27 of the Tax Code of the Russian Federation, which are subject to mandatory labeling) depends not only on whether the types of activities carried out are recognized as the same type, but also on whether the taxpayer carries them out on UTII.

Let us recall that the taxpayer is a UTII payer in the municipal district (urban district, federal city) where he carries out activities transferred to “imputation” and where he is registered as a UTII payer for this type of activity. This follows from the provisions of paragraphs 1 and 2 of Article 346.28 of the Tax Code of the Russian Federation.

Thus, combining UTII for retail trade in goods not subject to mandatory labeling and the simplified tax system for trade in goods subject to mandatory labeling (including unlabeled remnants of such goods) will only be possible if these types of activities are carried out in different municipal areas (urban districts, federal cities). The sale of labeled goods through a retail facility located in a municipality where the taxpayer is not registered as a “retail dealer” will not deprive him of the right to UTII for a retail facility located in another municipality.

If all retail outlets are located in one municipality, then the sale through at least one of them of goods subject to labeling (including unlabeled remnants of such goods) will lead to a complete loss of the right to use UTII for all retail outlets located in this municipality education.

This approach is applicable when deciding on the possibility of combining the simplified tax system and UTII for trade in all “non-retail” goods named in paragraph 12 of Article 346.27 of the Tax Code of the Russian Federation, and not only those that are subject to mandatory labeling.

Restrictions for working under UTII and simplified tax system

• Let's start with the simplified tax system. A company wishing to operate under the “simplified” system should not have more than 100 employees on its staff. In addition, there are restrictions in the financial part: its annual income should not exceed 60 million rubles. and the residual value of intangible assets and fixed assets cannot exceed 100 million rubles. Another limit is related to the share of other legal entities in the authorized capital of the enterprise - this figure is limited to 25%. • Not everyone can work under UTII either. In particular, there is the same prohibition for enterprises and organizations with more than 100 employees and shares in the authorized capital of other legal entities exceeding 25%.

A taboo on the use of UTII is also imposed on those trade organizations and catering establishments whose customer service areas exceed 150 square meters in area. meters.

In addition, state budgetary institutions that are obliged to organize public catering as part of their activities do not have the right to operate under UTII.

Important: Both the simplified tax system and the UTII have a number of subtleties when applied. To know for sure whether it is possible to use each of these tax systems for a particular enterprise, it is advisable to carefully study the section of the Tax Code of the Russian Federation on this part or consult the nearest tax office.

Combining “retail imputation” with wholesale trade

Note that exactly the same consequence - complete loss of the right to “retail imputation” - will occur in a situation if the retail UTII taxpayer conducts wholesale trade in the same municipality (within the framework of the simplified tax system or OSNO). The new version of paragraph 2.3 of Article 346.26 of the Tax Code of the Russian Federation states that the right to UTII for retail trade is lost by taxpayers who “sell goods not related to retail trade” in accordance with Article 346.27 of the Tax Code of the Russian Federation. And Article 346.27 of the Tax Code of the Russian Federation names the type of contract under which goods are sold as the main feature of retail trade. This can only be a retail purchase and sale agreement. (The article “Drawing up trade transactions: what is the difference between a supply agreement, a purchase and sale agreement and a retail purchase and sale agreement” will help you avoid making mistakes when drawing up a retail purchase and sale agreement).

Thus, after January 1, the “retail imputator” must take into account the following. As soon as he enters into another agreement for the sale of goods (purchase and sale or supply), he will not only have to pay taxes on this transaction under a different taxation system (as is happening now), but also completely leave the “retail” UTII.

Find out the tax system of the counterparty and the amount of taxes paid by him

Payment procedure under the simplified tax system (for individual entrepreneurs with employees)

Let us remind you that the presence of employees plays a role only under the simplified tax system “income”. Let's take a closer look at this diagram.

An entrepreneur who hires workers retains the right to reduce the amount of tax by the amount of fixed contributions. Only a reduction of up to 50% is allowed.

In accordance with Article 346.21 (clause 3.1) of the Code, the tax (advance) payment under the simplified tax system “income” can be reduced by the amount:

- insurance payments made for employees;

- paid sick leave;

- payments made to employees in accordance with voluntary insurance contracts.

If an individual entrepreneur uses the labor of employees throughout the year, then he cannot completely reduce the tax burden on fixed payments. From the moment an entrepreneur acquires his first employee, restrictions begin to apply. Considering that the simplified tax is calculated using cumulative totals, the 50% limit when deducting contributions will apply for the entire period.

Do I need to deregister as a UTII payer?

Another problem for those who combine or plan to combine UTII and the simplified tax system is related to the new rule on the need to switch to a common taxation system in the event of a “failure” from the “imputation” due to the sale of “non-retail” goods. At the same time, legislators did not make any exceptions for taxpayers under the simplified tax system (new edition of clause 2.3 of article 346.26 of the Tax Code of the Russian Federation). This means that if we interpret this norm literally, it will not be possible to remain on the “simplified” system in such a situation.

In our opinion, most likely this is a mistake by legislators who simply forgot to correct this part of the norm. This is evidenced, in particular, by the fact that for those who apply the PSN, in the same situation, the possibility of switching to the simplified tax system is directly enshrined in the Tax Code of the Russian Federation (new edition of clause 6 of Article 346.45 of the Tax Code of the Russian Federation).

But since there are no official clarifications on this matter yet, we advise those who plan to carry out “non-retail” sales in 2021 and have decided, in this regard, to switch to the simplified tax system for retail, to officially abandon the “imputation”. Otherwise, when the first “non-retail” operation appears, you will have to forcibly leave the UTII, and then there may be problems with the continued use of the “simplified” tax.

Let us remind you that in order to voluntarily leave the “imputation” in connection with the transition to the simplified tax system, you need to submit an application to the tax authority at the place of registration as a UTII taxpayer. Individual entrepreneurs submit such an application in the form of UTII-4, organizations - in the form of UTII-3. The filing deadline is no later than January 15, 2021 (clause 3 of article 346.28, clauses 6 and 7 of article 6.1 of the Tax Code of the Russian Federation). The application must indicate 01/01/2020 as the date of termination of the application of UTII.

Submit an application in the UTII-3 form via the Internet, submit reports according to the simplified tax system and UTII

Transition to the simplified tax system: when to submit a notification?

When switching from “retail” UTII to the simplified tax system, the question also arises of at what point it is necessary to submit to the Federal Tax Service (at the location of the organization or place of residence of the individual entrepreneur) a notification about the application of the “simplified tax system”. Here you need to consider the following points.

If previously a taxpayer (organization or individual entrepreneur) sent a notice of transition to the simplified tax system and did not officially refuse this special regime, then as of January 1, 2021, he will be listed as a payer of a single “simplified” tax. Additionally, submitting a notification in form No. 26.2-1 (approved by order of the Federal Tax Service dated November 2, 2012 No. MMV-7-3 / [email protected] ) in connection with the termination of the use of UTII from January 1, 2020 is not required. Such taxpayers are not subject to the income limit established by paragraph 2 of Article 346.12 of the Tax Code of the Russian Federation. That is, those whose total revenue (from activities on UTII and the simplified tax system) for 9 months of 2019 exceeded 112.5 million rubles can also refuse UTII and remain only on the simplified tax system.

A taxpayer who has not previously notified his tax office about the transition to the simplified tax system must submit a notification in form No. 26.2-1. Moreover, it is better to do this before December 31, 2021. An organization or individual entrepreneur submits this notification not in the status of a UTII taxpayer. Therefore, in the “Taxpayer Identification (code)” field, you should enter the number 3. When filling out the cell “switches to a simplified taxation system,” you need to indicate the number 1 (clause 1 of Article 346.13 of the Tax Code of the Russian Federation).

Submit a free notification of the transition to the simplified tax system and submit a declaration under the simplified tax system via the Internet

Will it be possible to switch from UTII for retail to the simplified tax system not from January 1, but from another date during 2021 (after the first “non-retail” sale occurs)? In our opinion, there may be problems in this case. The fact is that the norm of paragraph 2 of Article 346.13 of the Tax Code of the Russian Federation, which allows organizations and individual entrepreneurs that have ceased to be “imputed” to switch to the simplified tax system within a year, is formulated ambiguously. The regulatory authorities believe that this rule is not applicable in a situation where the UTII taxpayer has lost the right to this special regime due to a violation of the conditions established by the Tax Code (letter of the Ministry of Finance dated November 24, 2014 No. 03-11-09/59636 and the Federal Tax Service dated February 25, 2013 No. ED-3-3/ [email protected] ).

This means that UTII taxpayers who in 2021 will sell “non-retail” goods (including goods subject to mandatory labeling) and, therefore, lose the right to “imputation” may have difficulties with the simultaneous transition to the simplified tax system. It is likely that they will not be able to start using the “simplified tax” from the month in which they stopped paying UTII. It is possible that the inspectorate, having received form No. 26.2-1 with number 2 in the “Taxpayer Identification (code)” field and number 3 in the “switches to a simplified taxation system” box, will send the taxpayer a message about the impossibility of applying the simplified tax system.

Therefore, it is better not to wait until the UTII is released, but to notify the tax authorities of your intention to apply the simplified tax system before the beginning of 2020. Let us also recall that when switching to the “simplified” version from a “pure” UTII (that is, UTII formally combined with OSNO), when determining the revenue limit, income from “imputed” activities is not taken into account (clause 4 of Article 346.12 of the Tax Code of the Russian Federation, letter from the Ministry of Finance dated 02.20.08 No. 03-11-04/2/42).

What should shoe sellers do?

Let us separately consider the situation with the sale of shoes, which are subject to mandatory labeling.

Order an electronic signature to work in mandatory marking systems Receive in an hour

Recently, the Ministry of Finance recognized that the possibility of using UTII when trading such goods remains until March 1, 2021 (letter dated November 28, 2019 No. 03-11-09/92662). However, now the “impossible” people who sell shoes need to make a decision about the future of this business. There are three options.

The first is to continue to apply UTII in the first quarter of 2021, and from March 1 to tax income from the sale of shoes within the framework of the general taxation system. With this option, no measures are required to be taken this year. No later than March 6, 2021, you will need to submit an application to deregister as a UTII taxpayer.

The second option is to transfer the relevant activity to the simplified tax system. In this case, you need to abandon UTII from January 1, 2021. You should also submit a notice of transition to the simplified tax system by the end of December 2021 (if the taxpayer has not previously sent such a document to the Federal Tax Service). In this case, it will not be possible to switch from “imputation” to “simplified” directly from March 1, 2021 - this is prevented by the provision of paragraph 1 of Article 346.28 of the Tax Code of the Russian Federation. Let us remind you that this norm allows UTII taxpayers to change the tax regime starting from the next calendar year. Accordingly, during the year the transition from UTII to the simplified tax system without cessation of the “imputed” type of activity is impossible.

A third option follows from this provision - to leave the retail trade of shoes on UTII until March 1, 2021, after which to completely “curtail” this business, continuing to apply the simplified tax system for the rest of the activity. In this case, those who are not yet a taxpayer of the simplified tax system must remember to submit a notice of transition to this special regime before December 31, 2021. And no later than March 6, 2021, you will have to send an application for deregistration as a UTII taxpayer in connection with the termination of the relevant activity from 03/01/2020.

Accounting for “transition” expenses and income

In conclusion, let us recall the procedure for accounting for “transitional” income and expenses by those taxpayers who decided to abandon UTII for retail in favor of the simplified tax system.

Explanations on this matter are given, in particular, in letters of the Ministry of Finance dated 04/01/19 No. 03-11-11/22190 and dated 08/21/13 No. 03-11-06/2/34243. It follows from them that the “simplified tax” does not take into account in income payments received for goods shipped during the period of application of UTII, as well as prepayment for goods received during the period of application of the “imputed tax”, even if the shipment took place after the transition to the “simplified tax”.

Accordingly, the costs of paying the purchase price of these goods, previously purchased for resale, are not included in expenses when calculating tax according to the simplified tax system. It does not matter at what point the cost of these goods was transferred to suppliers (before or after the transition to the “simplified system”). In any case, this expense relates to activities taxed under UTII (clause 8 of Article 346.18 of the Tax Code of the Russian Federation).

For other products, a simple rule applies. If they were purchased and paid for during the period of application of UTII, then their purchase price is not taken into account as expenses when determining the object of taxation according to the simplified tax system. At the same time, revenue from the sale of these goods received during the period of being on the simplified market is included in income in the general manner (letters from the Ministry of Finance dated 04/23/18 No. 03-11-11/27126 and dated 07/03/15 No. 03-11-06 /2/38727). As for the cost of goods received during the period of application of UTII, but paid after leaving this special regime, it is taken into account as expenses when calculating the single tax according to the simplified tax system on a general basis.

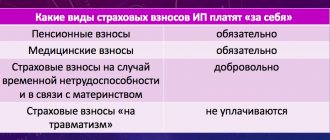

Calculation procedure for UTII (for individual entrepreneurs without employees)

If the taxpayer works on UTII and does not hire employees, he can reduce the calculated tax by the actual contribution transferred. At the same time, the amount of deduction is not limited; an entrepreneur can fully cover his tax burden through the insurance premium.

The single tax can be reduced by the amount actually transferred, not exceeding the amount of the calculated contribution. Thus, an entrepreneur cannot deduct from tax more contributions than he is required to pay during the year. Also, you cannot reduce it by the amount that you only plan to pay in the future.

UTII is calculated only quarterly; each quarter is a tax period. Accordingly, fixed contributions are taken into account within the quarter. It is not allowed to transfer the unaccounted contribution amount when calculating the tax for the quarter to the next period (unlike the simplified tax system, where it can be transferred within the year).