Which Federal Tax Service Inspectorate should I submit payments for contributions from 2021?

Since 2021, control over reporting on insurance premiums has come under the control of the Federal Tax Service (Chapter 34 of the Tax Code of the Russian Federation). Therefore, starting from 2021, submit calculations of insurance contributions for compulsory pension (social, medical) insurance to the tax office. You must report according to the new form approved by Order of the Federal Tax Service of Russia dated October 10, 2021 No. ММВ-7-11/551. See “Calculation of insurance premiums (DAM) for the 1st quarter of 2021: example of filling out.” At the same time, pay attention to some features of the reporting direction.

General approach

Calculations for insurance premiums from 2021, as a general rule, must be submitted to the Federal Tax Service at the location of the organization or the place of residence of the individual entrepreneur.

Separate units

A separate division of an organization must pay its employees if it independently accrues payments and rewards to them. In this case, the division submits the calculation to the Federal Tax Service at its location. In the calculation itself, the checkpoint of the separate unit is then indicated.

If the separate division does not meet these criteria, data on the employees of the separate division should be reflected in the calculation for the parent company (parts 11 and 14 of Article 431 of the Tax Code of the Russian Federation). Also see “How can separate divisions pay insurance premiums and submit reports to the Federal Tax Service from 2021.”

Largest taxpayers

The largest taxpayers transfer insurance premiums and submit settlements for them in 2021 to the Federal Tax Service at their location:

- the organization itself (not at the place of registration as the largest payer);

- its separate divisions (if they themselves accrue payments and benefits to employees) - subclause 7 of clause 3.4 of Article 23 and clause 11 of Article 431 of the Tax Code of the Russian Federation.

Starting from 2021, there is no need to submit calculations for insurance premiums to the Federal Tax Service at the place of registration of the largest taxpayer. In relation to calculations for insurance premiums, paragraph 7 of paragraph 3 of Article 80 of the Tax Code of the Russian Federation does not apply. This is confirmed by letters of the Federal Tax Service of Russia dated January 23, 2021 No. BS-4-11/993 and dated January 10, 2021 No. BS-4/11-100.

How to enter the code at the place of registration for UTII in the declaration in 2018

In order to correctly report to the tax authority, the code at the location (accounting) is indicated in the appropriate line. The indicator is entered in digital format according to Appendix 3 and filled out from left to right. Entering dashes, indicating zeros or missing data in cells is not allowed. Why?

First of all, for the reason that any imputed taxpayer is required to first register with the Federal Tax Service. And it doesn’t matter what legal status we are talking about - a legal entity or an individual entrepreneur. To transfer your activity to UTII, you must first submit an application to the tax office. And only after obtaining the appropriate permission, the use of this special regime is allowed. Since imputation reporting is submitted at the place of business, indicator values have been developed to clarify the responsible control body.

UTII - tax calculation in 2021, example

Values of accounting codes (places of presentation) for the UTII declaration:

- 120 – indicated by those entrepreneurs who submit a declaration to the tax authorities at their address of residence.

- 214 – code 214 at the location (registration) is intended to be indicated by Russian legal entities that are not recognized as major taxpayers.

- 215 - intended for successor companies that are not recognized by the largest taxpayers.

- 245 – indicated by foreign companies when submitting a declaration to the address of conducting the imputed activity through a representative office (permanent).

- 310 – indicated by Russian companies when submitting a declaration at the address of the imputed activity.

- 320 – code at the place of registration 320 in UTII, or more precisely in the declaration of imputation, is used in the case of submitting a report to the address of conducting activities in a special regime.

- 331 – indicated by foreign companies when submitting a declaration to the address of conducting the imputed activity through a branch of such a business entity.

Note! The imputed accounting code at the location for an LLC and an individual entrepreneur will differ. After all, registration of individual entrepreneurs is carried out with reference to the address of his residence (120) or the place of actual conduct of the imputed business (320). At the same time, the accounting of legal entities will depend on whether it is a Russian or foreign company; whether the enterprise is considered the largest taxpayer, and whether reorganization procedures have been carried out.

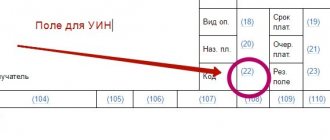

Code “by location” on the title page

On the title page of the calculation of insurance premiums, approved by Order of the Federal Tax Service of Russia dated October 10, 2021 No. ММВ-7-11/551, there is a field called “At the location (accounting) (code)”. It must indicate the code for the place of reporting. The codes are taken from Appendix No. 4 to the Procedure for filling out the calculation. Here is a table of codes with decoding.

| Code | Where is the payment submitted? |

| 112 | At the place of residence of an individual who is not recognized as an individual entrepreneur |

| 120 | At the place of residence of the individual entrepreneur |

| 121 | At the place of residence of the lawyer who established the law office |

| 122 | At the place of residence of the notary engaged in private practice |

| 124 | At the place of residence of the member (head) of the peasant (farm) enterprise |

| 214 | At the location of the Russian organization |

| 217 | At the place of registration of the legal successor of the Russian organization |

| 222 | At the place of registration of the Russian organization at the location of the separate division |

| 335 | At the location of a separate division of a foreign organization in the Russian Federation |

| 350 | At the place of registration of the international organization in the Russian Federation |

Thus, if in 2021 the payment is submitted, for example, at the location of a Russian company, enter the code “214”. Accordingly, on the title page it will look like this:

Keep in mind

Until 2021, in calculations according to the RSV-1 form, there was no field for codes “At location (accounting)”.

Read also

06.02.2017

Why do you need a code at the place of registration for UTII 2021?

When transferring the entire activity or its individual areas to imputation, the taxpayer must submit a declaration to the territorial division of the Federal Tax Service Inspectorate. This obligation applies to both legal entities and entrepreneurs, subject to the use of the designated special regime. If an entity simultaneously works on several tax systems, it will be necessary to prepare separate reports. The list of forms varies depending on the modes.

The current imputation declaration form for 2021 was approved by the Federal Tax Service in Order No. ММВ-7-3 / [email protected] dated 07/04/14. Here is the form of the document, as well as the procedure for its preparation with a breakdown of the requirements into sheets and sections. When a declaration is filled out, the code at the location (registration) is entered in accordance with the values in Appendix 3 of the Order. The information is indicated in a special column on the title of the report. At the same time, data is entered into other lines according to the current order.

Note! Since coding of indicators is necessary to simplify the reporting processing procedure, all imputed taxpayers without exception are required to fill out these lines. Error-free entry of values will not only help tax authorities quickly post data, but will also protect companies from providing incorrect information.

Basic designations for accounting

Having studied all the tables in detail, you can notice that organizations that are not the largest taxpayers and apply the general taxation system indicate the same numbers in all reports - 214. The difference is only for the “simplified”: in reporting according to the simplified tax system, organizations enter 210. And individual entrepreneurs indicate 120 in all reports they submit. Thus, the main values used are:

- 214 - for companies;

- 120 - for individual entrepreneurs.

Legal documents

- By Order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/ [email protected]

- By Order of the Federal Tax Service of Russia dated October 10, 2016 No. ММВ-7-11/ [email protected]

- By Order of the Federal Tax Service of Russia dated July 4, 2014 No. ММВ-7-3/ [email protected] (as amended on October 19, 2016)

- By Order of the Federal Tax Service of Russia dated February 26, 2016 No. ММВ-7-3/ [email protected]

- By Order of the Federal Tax Service dated October 19, 2016 No. ММВ-7-3/ [email protected]

- By Order of the Federal Tax Service dated October 29, 2014 No. ММВ-7-3/ [email protected]

- By Order of the Federal Tax Service of Russia dated July 28, 2014 No. ММВ-7-3/ [email protected] (as amended on February 1, 2016)

- By Order of the Federal Tax Service of Russia dated May 10, 2017 No. ММВ-7-21/ [email protected]

- By Order of the Federal Tax Service of Russia dated March 31, 2017 No. ММВ-7-21/ [email protected]

- By Order of the Federal Tax Service of Russia dated December 5, 2016 No. ММВ-7-21/ [email protected]

What to indicate in declarations and calculations

Let's take a closer look at what numbers need to be indicated in different types of reporting.

Code of location of registration in 6-NDFL

The values are given in Appendix No. 2 to the Procedure for filling out the calculation, approved by Order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/ [email protected]

In form 6-NDFL, location code 214 is the most widely used. It is affixed by organizations that are not the largest taxpayers, that is, most companies. Code 214 at the location (registration), however, is not the only one. A total of 11 values can be used when completing this reporting. Therefore, when entering the code for the place of registration in 6-NDFL, remember that entrepreneurs, farmers, lawyers, notaries, major taxpayers, separate divisions (for more details, see the table) indicate different numbers.

6-NDFL - codes by location (2018) in table form:

Value in calculation of insurance premiums

To fill out the DAM form at your location (registration), the code can be found in Appendix No. 4 to the Procedure approved by Order of the Federal Tax Service of Russia dated October 10, 2016 No. ММВ-7-11/ [email protected]

Location (accounting) - code 120 is entered by individual entrepreneurs, and individuals who are not individual entrepreneurs indicate the value 112. Organizations, in the same way as when filling out form 6-NDFL, enter 214.

The rest of the values are clearly shown in the table:

In the UTII declaration

Numerical values are given in Appendix No. 3 to the Procedure approved by Order of the Federal Tax Service of Russia dated July 4, 2014 No. ММВ-7-3 / [email protected] (as amended on October 19, 2016).

Code at the place of registration 320 in UTII means that the report is submitted by an individual entrepreneur where he carries out his activities and does not live. Reporting occurs in this way if the individual entrepreneur works in a different city or region in which he lives.

If an individual entrepreneur carries out activities and submits reports in the same place where he lives, he puts 120.

Organizations (not the largest) still indicate 214, as in the examples above.

The remaining values can be found in the table.

Code at the place of registration (UTII 2020):

In the simplified tax system declaration

Appendix No. 2 to the Procedure approved by Order of the Federal Tax Service of Russia dated February 26, 2016 No. ММВ-7-3/ [email protected] contains the numbers necessary to fill out the simplified tax system declaration. Compared to other reports, there are not many options to choose from - only three. They are intended for individual entrepreneurs, for a Russian organization and for the legal successor of a Russian organization.

Location code 210 indicates small companies using the simplified tax system, and 120 indicates entrepreneurs. See the table for all values.

Declaration of the simplified tax system - code at the location (accounting):

In the income tax return

Appendix No. 1 to the Procedure approved by the Order of the Federal Tax Service of October 19, 2016 No. ММВ-7-3/ [email protected] includes all the necessary numbers that the declaration may contain. Based on the location of the accounting for an ordinary Russian organization, this is 214, with a total of nine values. The table shows more details:

In the VAT return

Appendix No. 3 to the Procedure approved by the Order of the Federal Tax Service dated October 29, 2014 No. ММВ-7-3 / [email protected] contains the numbers that the taxpayer indicates depending on the location. There are especially many of them in VAT reporting - 17.

In the declaration for the unified agricultural tax

Appendix No. 3 to the Procedure approved by Order of the Federal Tax Service of Russia dated July 28, 2014 No. MMV-7-3 / [email protected] (as amended on February 1, 2016), includes the necessary numbers for the declaration of the unified agricultural tax. For organizations, the standard number has been retained - 214.

j

In land tax reporting

Appendix No. 3 to the Procedure approved by Order of the Federal Tax Service of Russia dated May 10, 2017 No. ММВ-7-21/ [email protected] includes the necessary information.

In the property tax report

The data is contained in Appendix No. 3 to the Procedure approved by Order of the Federal Tax Service of Russia dated March 31, 2017 No. ММВ-7-21/ [email protected]

For transport tax

Appendix No. 3 to the Procedure for filling out a tax return for transport tax, approved by Order of the Federal Tax Service of Russia dated December 5, 2016 No. ММВ-7-21/ [email protected] , includes only three designations:

- for the largest taxpayers;

- their legal successors;

- and at the location of the transport.

Where and when to use

How to find out OKATO IP by TIN: what is it and why is it needed

At the location of the registration, the code for individual entrepreneurs is used in all tax returns submitted.

Note! It does not matter whether the entrepreneur is on a simplified tax regime or on the main tax regime.

The code is selected on the title page of the report:

- VAT. The only suitable code for an individual entrepreneur is 116. It is chosen when a businessman works and submits reports at the place where the entrepreneur is registered. The remaining codes are important for organizations and non-profit entities with their own characteristics.

- USN. The declaration for individual entrepreneurs using the simplified regime has 3 options to choose from. In accordance with the goal of making accounting more understandable, the codes correspond to the status of the taxpayer - individual entrepreneur, organization and legal successor. The individual entrepreneur chooses code 120. The code at the location or registration for the individual entrepreneur whose simplified tax system is indicated on the title page, as in other declarations.

- RSV. Entrepreneurs and employees submit to the Federal Tax Service a calculation of insurance premiums, which includes information on pension, medical and temporary disability accruals. This document offers more choice by code. However, only 120 is suitable for individual entrepreneurs.

- 6-NDFL. Calculation of withheld personal income tax must be submitted by entrepreneurs who have employees and work with individuals. The regulation on the rules for filling out the calculation describes 11 code options for various taxpayers. Organizations, farmers, notaries, and major taxpayers have different codes. An individual entrepreneur, as in the case of declarations under the simplified tax system, RSV and 6-NDFL, indicates number 120 “at the place of residence of the individual entrepreneur.”

- UTII. Taxpayers of imputed tax can be registered in regions other than their place of registration. Therefore, UTII declarations will be submitted to other tax authorities. In this regard, the individual entrepreneur must choose option 120 if he works in the same region where he lives. Number 320 is suitable for entrepreneurs who conduct their commercial activities in areas other than their place of registration.

- 3-NDFL. The individual entrepreneur does not file an income tax return. Instead, income is declared in the 3-NDFL calculation. However, it does not provide a location code.

When calculating 6-NDFL for individual entrepreneurs, you need to indicate code 120

List of codes for calculating insurance premiums by location

Each organization must know the code for calculating insurance premiums at its location, since without this point the entire form will not be accepted. The code is the most important part of any document that must be submitted to the tax service.

The document itself and its delivery form will constantly undergo changes, since the new form was adopted only in 2021. Although the form has been approved, its improvement is inevitable.

The deadlines for submitting documentation will constantly change every new year. Because of this, it is necessary to know the rules for rescheduling and the exact deadlines for submitting the form.

New reporting

Starting from 2021, the rules for submitting reports have changed; now insurance premiums are regulated by the tax office, which is prescribed in the Tax Code. For this reason, for the first quarter of 2021, all data on pension insurance must be sent to the Federal Tax Service. The forms for calculating insurance premiums have also changed; the innovations were accepted for implementation by the tax service itself at the end of 2021.

This plan shows the addition that the Federal Tax Service made - this is the third section containing information about each of the insured persons individually. Previously, this section was contained in the RSV-1 form.

Any organization that pays funds to hired workers, according to an employment contract or a civil law contract, is required to submit documents to the tax office. Not only organizations and enterprises that have employees are required to submit reports, but also farms, in which responsibility falls on the head of the community.

After it became necessary to submit reports to the tax office, the deadlines for submission and their volumes also changed.

Any person obligated to pay taxes on wages issued to their employees must submit a report to the Federal Tax Service no later than the thirtieth day of the month following the period in question in the report. If the last day falls on a weekend or holiday, then the deadline is moved to the next working day, for example, the 30th is Sunday, which means the report must be submitted no later than Monday.

The reporting periods are: first quarter of the year; half year; nine month; year. More precise dates will be specified in the table below.

If a company or enterprise pays money to less than 25 individuals, then it is allowed to draw up reports on paper, which will be handed over personally by the payer or through an authorized representative. If payments are accrued to more than 25 individuals, then he is allowed to submit the form only electronically. This is done for the convenience of both parties, both the payer and the service.

| Reporting period | Deadline for submitting a report on insurance premiums in 2018 |

| For the first quarter | Until May 2 |

| For half a year | Until July 31 |

| In nine months | Until October 30 |

| For the entire year 2021 as a whole | Until April 30, 2021 |

Location on the title page of codes for calculating insurance premiums at the location

Composition of RSV-1

From now on, the new calculation form containing information on insurance premiums consists of the following pages:

- Title page (title page).

- A sheet with information about a person who is not an individual entrepreneur.

- Data on the obligations of who must pay insurance premiums (first section):

- the first appendix, which contains a calculation of the amounts required to pay compulsory pension and health insurance;

- the second appendix, which takes into account the calculation of the amounts required to pay for social insurance in the event of a citizen’s temporary incapacity or pregnancy;

- the third appendix, which includes the costs required for compulsory insurance for temporary loss of the ability to work, as well as for maternity expenses;

- the fourth application, which contains payments made from the federal budget;

- fifth appendix with calculations subject to a reduced tariff of insurance premiums under subparagraph 3 of paragraph 1 of Article 427 of the Tax Code;

- sixth appendix with calculations subject to a reduced tariff of insurance premiums under subparagraph 5 of paragraph 1 of Article 427 of the Tax Code;

- seventh appendix with calculations subject to a reduced tariff of insurance premiums under subparagraph 7 of paragraph 1 of Article 427 of the Tax Code;

- the eighth appendix with information subject to a reduced tariff of insurance premiums under subparagraph 9 of paragraph 1 of Article 427 of the Tax Code;

- the ninth appendix, which takes into account all the information necessary for applying the tariff for insurance premiums, according to subparagraph 2 of paragraph 2 of Article 425 of the Tax Code;

- the tenth appendix, with information that is necessary for the payment of remuneration for full-time students in professional institutions;

- Data on the obligations of those payers who are heads of farms (second section):

- the first application with calculations of the amounts for insurance premiums to be paid by the head and members of the farm.

- Information about each of the insured persons separately (third section).

Article 427. Reduced rates of insurance premiums

Filling procedure

The calculation consists of a title page and three sections with appendices.

Anyone required to file a claims report must include these parts on the form:

- Title page.

- First section.

- First subsection of the first application.

- Second subsection of the first application.

- Second application.

- Third section.

The remaining applications and sections are required to be completed only if the relevant data is available. Payments must be made strictly in the national currency (ruble). If there is a cell in which there is nothing to fill, then a dash is placed. All words must be capitalized.

For convenience, you should fill out the reports in the following order:

- First, you should turn to the personalized information in the third section, which includes data about each individual individual.

- Next, go to subsection 1.1 of Appendix 1 in the first section. To do this, you need to sum up all the indicators for each employee from the third section.

- Then fill out subsection 1.2 of Appendix 1 in the first section. This is done because only here the data for health insurance premiums is indicated.

- Now you can fill out Appendix 2 of the first section.

- Then fill out the free section 1, where you enter the full amount required to pay as insurance premiums.

- Now you can fill out the remaining sections if there is information on them.

- The last step is to number the sheets.

Since responsibility and control over the amounts paid for insurance premiums has come under the control of the Federal Tax Service, accordingly, reporting must be submitted to one of the divisions of this service.

The approach that works for most legal entities involves submitting reports to the Federal Tax Service, located at the location of the organization or at the place of residence of the entrepreneur.

If the submission of documents is carried out by the largest taxpayer, then contributions are transferred and forms are sent to the Federal Tax Service either at the location of the organization itself, or at the location of each of the divisions.

Since the conditions for submitting calculations for insurance premiums have changed in 2021, it was decided to cancel the submission of forms for registration of the largest taxpayer. This point has been confirmed at the legislative level.

If an organization has separate divisions, then each of these branches of the company is required to pay insurance premiums. Since the legislation implies that payments must be made in the same place where reports are submitted - at the location of the unit.

There are situations when the OP does not have the rights to pay funds to individuals, which automatically relieves this department from this type of reporting in full. It is enough only to pay insurance premiums at the place of registration of the organization itself.

If the OP is endowed with rights that allow it to pay funds to individuals, then reporting will be submitted not only at the place of registration of the unit, but also at the location of the organization. The amount that must be paid at the place of registration of the unit will entirely depend on the size of the base for calculating these contributions.

The amount that the unit must pay to the tax office is determined by the difference between the total amount of insurance premiums to be paid by the organization and the total amount of insurance premiums in the aggregate.

There is one exception to the rules, which is spelled out in the tax code itself; it applies only to enterprises located outside the territory of the Russian Federation. Despite the fact that the OP can independently calculate and send data on insurance premiums and their payments, the responsibility for this still falls on the organization, which must submit the relevant document to the tax service at its location.

| Code | Place of payment for insurance premiums |

| 112 | A person who is not an individual entrepreneur - rented at the place of residence of the individual |

| 120 | Persons who are individual entrepreneurs - at their place of residence |

| 121 | If there is a lawyer’s office, then at the place of residence of the founding lawyer |

| 122 | If the report was filled out by a notary engaged in private practice, then at his place of residence |

| 124 | If the report is submitted by a member or head of a farm, then at his place of residence |

| 214 | At the location of the organization located on the territory of the Russian Federation |

| 217 | At the place of registration of the legal successor of the organization from the Russian Federation |

| 222 | If the organization has separate divisions, then at their location |

| 335 | At the location of the OP from a foreign organization located on the territory of the Russian Federation |

| 350 | At the place of registration of an international organization located in the Russian Federation |

Since the conditions for submitting calculations for insurance premiums have changed in 2021, it was decided to cancel the submission of forms for registration of the largest taxpayer. This point has been confirmed at the legislative level.

The calculation form for insurance premiums 2021 was approved by Order of the Federal Tax Service dated October 10, 2016 No. ММВ-7-11/551, KND code - 1151111. It is called “Calculation of insurance premiums” (DAM, ERSV).

The RSV contains information on payments for compulsory insurance:

- compulsory pension insurance (CPI), including at an additional rate, as well as additional social security;

- compulsory health insurance (CHI);

- compulsory social insurance in case of temporary disability and in connection with maternity (VNIM).

How and in what form a declaration is submitted by a tax agent

The VAT return is submitted by each tax agent before the 25th day of the month following the reporting period.

In this case, the reporting period is a quarter. The declaration must be submitted by the tax agent in electronic form (clause 5 of Article 174 of the Tax Code of the Russian Federation). There is an exception to this. Important! Tip from ConsultantPlus If you are a tax agent, you can submit a VAT return on paper only if the following conditions are simultaneously met... Read more about the conditions under which a tax agent can report on paper in K+, having received a trial demo access to the system. It's free.

You can find out who is a tax agent for VAT from the article “Who is recognized as a tax agent for VAT (responsibilities, nuances)”.

The declaration is submitted by the tax agent to the Federal Tax Service at its registered address. On the title page of the declaration in the line “At location (accounting)”, tax agents, if they apply VAT exemption or work under a special regime, indicate code 231, in other cases they enter code 214 in this line.

For more details, see the article “How to correctly fill out a VAT return for a tax agent?” .

Deduction codes in the 2-NDFL certificate

Help 2-NDFL: tax deduction codes

Certificate 2-NDFL is a document that can be obtained from the accounting department of the organization in which an individual works.

The certificate contains information about the tax agent (employer), the income of an individual for a certain period of time, as well as accrued and paid personal income tax to the budget.

Tax deduction codes in the 2-NDFL certificate may be contained in the third and (or) fourth paragraphs.

As you know, tax deductions can be obtained at the end of the year through the tax office, or through the employer during the year, according to the statement.

The following tax deduction codes are currently in effect:

- Codes of tax deductions that may be present in paragraph 3 of the 2-NDFL certificate: - 201 - 210 , deductions for transactions with securities and for transactions with derivative financial instruments; — 211, 213 , deductions for repo transactions, the object of which are securities; - 215 - 241 , deductions for securities lending transactions; - 250 - 252 , deductions for transactions on IIS; - 403 - 405 , deductions for civil contracts, copyright or other remuneration; - 501 - 510 , deductions from the cost of gifts from individual entrepreneurs and organizations, from the cost of prizes at contests and competitions, from the amount of financial assistance from the employer, from the amount of reimbursement for medications by employers, from the cost of winnings and prizes (at competitions held for advertising purposes), from the amount of financial assistance to disabled people, from the amount of assistance to WWII veterans, from the amount of financial assistance at the birth of a child, from the amount of income from agricultural producers, from the amount of insurance premiums paid by the employer for employees; — 601 , deductions for income in the form of dividends; - 620 , other deductions.

- Codes of tax deductions that may be present in paragraph 4 of the 2-NDFL certificate: - 104, 105 , deductions for the taxpayer himself (WWII veterans, disabled people of groups I and II, etc.); - 126 - 149 , deductions for children, 114 - 125 , excluded; - 311 - 312 , property tax deductions (for the purchase of housing, including a mortgage); — 320, 321 , social deductions for education of yourself, brother/sister, children; - 324 - 326 , social deductions for treatment (including expensive treatment, as well as the amount of contributions under voluntary personal insurance contracts); — 327 , deductions under contracts of non-state pension provision, voluntary pension insurance, voluntary life insurance; — 328 , deductions regarding paid additional insurance contributions for funded pension; — 618 , investment tax deductions, 617 excluded Open all currently valid deduction codes Open all currently valid income codes

It should also be borne in mind that tax deductions under paragraph 3 of the 2-NDFL certificate always correspond to a specific income code, and deductions under paragraph 4 of the 2-NDFL certificate are not tied to any specific income codes.