The company's supplier requested that payment for the shipment of goods be transferred not to his bank account, but to his landlord. He explains this by saying that he must pay off his rent arrears, but currently has no available funds. Can a company in such a situation make payment for another legal entity? Yes, today there is nothing unusual in such a request. After all, the law allows business entities to pay their obligations not only directly. It is quite acceptable that another organization transfers funds on behalf of the debtor.

Legal basis

The debtor's right to transfer the obligation to pay for it to a third party is provided for by the Civil Code. This is stated in Article 313. A reservation is also made that this is legal in the event that any other laws or conditions of the paid obligation do not require that the debtor fulfill them strictly independently. Such conditions, for example, may be included in the contract. But most often there are no obstacles to attracting a third party to pay.

How safe is it in terms of audits of the paying organization? Will the Federal Tax Service inspectors have any complaints that the company made payments for another legal entity? Practice shows that if the operation is properly executed, inspectors usually do not have any questions. And if they do arise, they are very quickly “closed” with supporting documents.

What is this

A letter of payment for another organization is a document providing for payment to be made with the assistance of a third party. This procedure is carried out on the basis of current legislation.

The debtor has the right to ask the organization for help to pay the debt to the person providing the loan. Any company can ask an LLC to fulfill a promise in cash. To avoid difficulties and additional questions, it is recommended to write a letter. A legal entity that is a debtor must draw up a separate document. And the payer himself must also prepare a letter. There is a sample for correct preparation.

LLC "DOLZHNIK" INN 7800000000 KPP 780000000 OGRN 1080000000000 190000, St. Petersburg, st. Pochtamptskaya, 1 r/sch. 40702800000000000000 in OJSC “SuperBank” BIC 044000000 cor. sch. 30101800000000000000

How to make a payment for another legal entity?

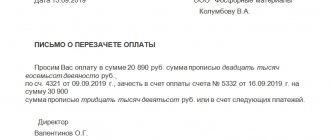

The legislation did not provide for any special form or type of document that would formalize the payment procedure under consideration. However, its implementation requires an agreement between the parties. To do this, the company whose obligations will be paid must send a letter to the head of the organization (or to the entrepreneur), which, at his request, will make the payment.

The letter is drawn up in free form, but it is mandatory to include the following data:

- the name of three persons: the debtor for whom payment will be made;

- payer (that is, the addressee of the letter);

- the person who will receive the funds (the debtor's creditor);

The company that draws up the specified letter is recommended to describe all the circumstances and parameters in as much detail as possible. And the addressee of the letter, that is, the paying organization, should receive its original.

So, the main document for making payment for another legal entity is a letter, a sample of which is presented in the following image.

How is debt payment carried out by a third party?

The debtor may entrust the fulfillment of contractual obligations to a third party, in accordance with Art. 313 of the Civil Code of the Russian Federation, unless the contract strictly stipulates that the debtor must personally fulfill the obligations.

The conditions for the participation of a third party must be documented. For this:

- The buyer sends a notice to the creditor indicating information about the third party who is subject to contractual obligations;

- The debtor sends a letter to the third party in which he describes the relevant contractual obligations.

All letters can be formatted in any form in accordance with the rules of a business letter, which details the details of the parties and complete information on calculations. The presence of written notifications allows you to avoid tax claims, since VAT and income tax have already been accrued and only the debt is paid.

How to make a debt adjustment when transferring debt, writing off debt and when offsetting advances in the 1C 8.3 program, read our article.

Reflection in tax accounting for the payer

The company has paid the obligations of its counterparty, and now this transaction must be reflected in the accounts. First, let's consider whether this will have any tax consequences for the payer.

If the company is on the OSN, then in some cases it can offset VAT on the transferred amount. The operation will not entail any other tax consequences. To offset VAT, the following conditions must be met:

- the company transferred funds for its supplier as an advance payment;

- the agreement on the basis of which the company and the supplier operate contains an advance payment clause;

- the supplier has given instructions to pay its obligations (the letter mentioned above) and issued an invoice;

- there is a payment document confirming the transfer of funds to the counterparty's creditor.

For a payer who uses the simplified tax system, accounting for the transaction will depend on the nature of the payment. If he had a debt to the person for whom he paid for the goods or services supplied, then it will be considered repaid (in whole or in part). In the event that the payer took out a loan with interest from his counterparty, they can be written off as expenses within the limits of the transferred amount.

Advance payment received from a third party

Source: Glavbukh magazine

Let's say your company has an agreement according to which the buyer must transfer you an advance. But in fact, the amount of advance payment to your current account was received not from the counterparty, but from a third party.

Indeed, the Civil Code of the Russian Federation allows the debtor to shift the payment of money to someone else. And the consent of your company, as a lender, is usually not required for this. Unless other conditions are specified in the contract. This is enshrined in paragraph 1 of Article 313 of the same code.

In this case, the payment order must indicate that the third party transferred the money at the request of your counterparty as an advance payment under the supply agreement. It is also advisable to receive a letter from the buyer in which he notified you that he has assigned his duties to pay the advance to another company.

How can you correctly account for the amount received? So, despite the fact that this money was transferred not by your counterparty, but by a third party, you still need to consider it an advance payment under the supply agreement. So calculate VAT on this amount. And issue an invoice. In this document, provide the details of the payment order. But be careful: in line 6 you must indicate the name of your buyer, and not the company that transferred the advance payment to you.

As usual, you will deduct the amount of advance VAT after you have shipped the goods to the buyer (clause 8 of Article 171, clause 6 of Article 172 of the Tax Code of the Russian Federation).

When calculating income tax, you do not include prepayment in income (subclause 1, clause 1, article 251 of the code). And in accounting, make the following entries: DEBIT 51 CREDIT 62 subaccount “Calculations for advances received” - an advance payment was received from a third company;

DEBIT 76 subaccount “Calculations for VAT on advances received” CREDIT 68 subaccount “Calculations for VAT” - VAT is charged on prepayments;

DEBIT 62 subaccount “Payments for sold goods” CREDIT 90 subaccount “Revenue” - revenue from sales is recognized;

DEBIT 90 subaccount “VAT” CREDIT 68 subaccount “Calculations for VAT” - VAT is charged on sales proceeds;

DEBIT 68 subaccount “Calculations for VAT” CREDIT 76 subaccount “Calculations for VAT on advances received” - accepted for deduction of VAT on prepayments;

DEBIT 62 subaccount “Settlements for advances received” CREDIT 62 subaccount “Settlements for goods sold” - the prepayment is credited towards the delivery of goods.

otchetonline.ru

Tax payments

You can pay for another person not only for the obligations that he or she has under an agreement with contractors. Recently, tax and other obligatory payments can be transferred in the same way. Previously, the tax service considered this option unacceptable - the taxpayer was obliged to pay his taxes independently. An exception was made only in very rare cases, for example, taxes for a reorganized entity could be paid by its legal successor.

However, at the end of 2021, amendments were made to the Tax Code that abolish this rule. So paying tax for another legal entity in 2021 is quite trivial. Thus, it is possible to pay tax payments, insurance premiums, state duties, both current accruals and debts for previous periods.

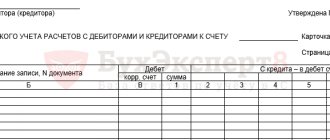

Payment for another organization - postings 1C 8.3 Accounting

The Organization has accounts payable to the supplier MICRON LLC in the amount of RUB 60,000. (including VAT 20%).

The supplier asked to transfer the entire amount of debt to LINASI LLC.

On March 01, the Organization transferred, on behalf of its creditor, the amount of 60,000 rubles to a third party.

| date | Debit | Credit | Accounting amount | Amount NU | the name of the operation | Documents (reports) in 1C | |

| Dt | CT | ||||||

| Transfer of payment to a third party | |||||||

| March 01 | 76.09 | 51 | 60 000 | 60 000 | Transfer of payment for a supplier to a third party | Debiting from the current account - Payment to the supplier | |

| Offset of payment against debt to the supplier | |||||||

| March 01 | 60.01 | 76.09 | 60 000 | 60 000 | 60 000 | Offset of payment against debt to the supplier | Debt adjustment - Offsetting advances |

Transfer of payment to a third party

On the day of transfer, issue a Debit from the current account (Bank and cash desk - Debit from the current account).

Fill out the document in the same way as for a regular payment to the supplier, indicating:

- The recipient is the third party to whom you actually transfer the money;

- Settlement/advance account — 76.09.

The payment is filled out in the same way as a regular payment to a supplier, with the difference that the Payment Purpose must indicate information by which a third party (payment recipient) could identify the payment.

More details Document Payment order transaction type Payment to supplier.

Postings

Offset of payment against debt to the supplier

After payment, close the debt to the supplier using Debt Adjustment (Purchases - Debt Adjustment).

As the Supplier (creditor), indicate the supplier to whom you owe. And in the New supplier - the one to whom you transferred the payment according to the supplier’s letter.

Automatically fill out the tabular part with existing balances under contracts with the supplier and delete extra lines if necessary.

In the New agreement , select the basis on which you transferred money to a third party.

Postings

Control

As a result of posting the document, both debts are closed - verify this using the Balance Sheet for Accounts 60 and 76 (Reports - Account Balance Sheet).

In SALT, both accounts must have a zero balance for these counterparties (and agreements with them).

Who can pay taxes for whom?

The law today does not establish any restrictions on who and under what conditions can pay tax for another person. Company taxes can be paid by any other organization, entrepreneur or just an individual.

The new rules make it possible to avoid sanctions for late payment of mandatory payments. For example, today is the last day to pay taxes, and the company does not have enough funds in its accounts. Just a year ago, such circumstances would have led to her having to pay late fees. Now, any person, for example, a director from his personal account, can fulfill the company’s obligation.

How to fill out a payment order?

There are several features in filling out a document to pay tax for another legal entity:

- in the payer field you should indicate the name of the organization (or the name of the individual) that makes the payment;

- in the fields “Taxpayer INN” and KPP, the relevant details of the organization for which the tax is paid are indicated;

- in the “Purpose of payment” field, you should first indicate the INN and KPP (if any) of the payer, and then, separated by two slashes (//), the name of the organization for which the payment is made, the name of the tax, period, type of payment and other important data;

- in field “101” the code “01” is entered - this means that the person for whom the payment is being made is a legal entity.

An example of how to fill out a “payment form” to pay taxes for another legal entity is shown in the following image.

In the above example, the individual K.I.V. makes an advance tax payment for U____ LLC in connection with the application of the simplified tax system.

Payment of advance by a third party

The organization has concluded a supply agreement containing an advance payment condition; the organization is the supplier. The advance payment for the buyer was paid by a third party; the payment documents indicate that the third party is making payment for the buyer, indicating the invoice number and the name of the organization for which the payment is being made. The third party also sent a notification that it was making payment for the buyer. The buyer did not send any relevant notifications. To whom should the supplier issue an advance invoice? Is it necessary to draw up a reconciliation report with the buyer or with the person who paid the advance?

Under a supply agreement, the supplier - seller engaged in business activities undertakes to transfer, within a specified period or terms, the goods produced or purchased by him to the buyer for use in business activities or for other purposes not related to personal, family, home and other similar use (Article 506 Civil Code of the Russian Federation).

By virtue of an obligation, one person (debtor) is obliged to perform a certain action in favor of another person (creditor), such as: transfer property, perform work, pay money, etc., or refrain from a certain action, and the creditor has the right to demand from the debtor fulfillment of his duties (clause 1 of Article 307 of the Civil Code of the Russian Federation).

In accordance with paragraph 1 of Art. 313 of the Civil Code of the Russian Federation, the fulfillment of an obligation may be entrusted by the debtor to a third party, if the law, other legal acts, the terms of the obligation or its essence do not imply the obligation of the debtor to fulfill the obligation personally. In this case, the creditor is obliged to accept the performance offered for the debtor by a third party.

As follows from this rule, in general, the consent of the creditor for the fulfillment of an obligation by a third party is not required. In this case, the creditor is obliged to accept the performance. If the creditor refuses to accept the fulfillment of the obligation in this way, the creditor will be considered overdue and bear responsibility in the form of compensation for losses caused by the delay (Article 406 of the Civil Code of the Russian Federation).

Current legislation does not oblige the debtor to notify the creditor of the fulfillment of an obligation by a third party. By virtue of the law, the creditor is also not obliged to notify a third party when contacting him directly in order to repay the debtor’s debt, but business customs recommend this.

When entrusting execution to a third party, the debtor does not leave the legal relationship, in contrast to the transfer of debt, the result of which is the replacement of the debtor (Article 391, Chapter 24 “Change of persons in an obligation” of the Civil Code of the Russian Federation). When transferring a debt, the obligation passes to the new debtor. The debtor's transfer of his debt to another person is permitted only with the consent of the creditor.

From the above provisions of the Civil Code of the Russian Federation it follows that in the case under consideration, the buyer for whom an advance payment under the supply agreement has been paid by a third party does not withdraw from the legal relationship that arose when concluding the supply agreement.

In accordance with paragraph. 2 p. 1 art. 168 of the Tax Code of the Russian Federation, in the event that a taxpayer receives amounts of payment, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights realized on the territory of the Russian Federation, the taxpayer is obliged to present to the buyer of these goods (work, services), property rights the amount tax calculated in the manner established by clause 4 of Art. 164 Tax Code of the Russian Federation.

According to paragraph 3 of Art. 168 of the Tax Code of the Russian Federation, when selling goods (work, services), transferring property rights, as well as upon receiving amounts of payment, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights, the corresponding invoices are issued no later than five calendar days days, counting from the day of shipment of goods (performance of work, provision of services), from the date of transfer of property rights or from the date of receipt of payment amounts, partial payment on account of upcoming deliveries of goods (performance of work, provision of services), transfer of property rights.

Mandatory details of the invoice issued upon receipt of payment, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights are listed in clause 5.1 of Art. 169 of the Tax Code of the Russian Federation. Such invoice must indicate, in particular:

— name, address and identification numbers of the taxpayer and buyer (clause 2, clause 5.1, article 169 of the Tax Code of the Russian Federation);

- the amount of tax imposed on the buyer of goods (works, services), property rights, determined on the basis of the applicable tax rates (clause 7, clause 5.1, article 169 of the Tax Code of the Russian Federation).

From the rules for filling out an invoice used in calculations for value added tax, approved by Decree of the Government of the Russian Federation dated December 26, 2011 N 1137 (hereinafter referred to as the Rules), it follows that the relevant invoice details are filled out based on information about the buyer (clauses "i", "k", "l" clause 1 of the Rules).

Taking into account the above, upon receipt of payment or partial payment from a third party for future deliveries of goods, an invoice must be issued to the buyer under the supply agreement. The mere fact that payment for the buyer was made by a third party does not indicate a change of persons in the obligation.

Regarding the need to draw up in this case an act of reconciliation of mutual settlements with the buyer and the third party who paid the advance for the buyer under the supply agreement, we inform you as follows.

In general, drawing up reconciliation reports with counterparties is not mandatory; such an obligation is not established at the legislative level.

Drawing up an act of reconciliation of mutual settlements can be considered a business practice. This is an established and widely used rule of behavior in any area of business activity, not provided for by law (Article 5 of the Civil Code of the Russian Federation).

In addition, the reconciliation act is not a primary document; it helps to identify errors in settlements with counterparties, that is, its preparation is not mandatory, but rather of an auxiliary nature (letter of the Federal Tax Service of Russia dated December 6, 2010 N ShS-37-3/16955, FAS resolution Ural District dated November 10, 2009 N F09-8688/09-S3).

Thus, the supplier is not required to prepare settlement reconciliation statements. At the same time, in order to avoid errors in settlements with counterparties, it is advisable for the supplier to reconcile mutual settlements with both the buyer and a third party by completing reconciliation reports (in any form).

Please note that settlements with debtors and creditors are reflected by each party in its financial statements in amounts arising from the accounting records and recognized by it as correct (clause 73 of the Regulations on accounting and financial reporting in the Russian Federation, approved by order of the Ministry of Finance of Russia dated July 29, 1998 N 34n). In other words, in the reconciliation report, the organization indicates exactly the data that is reflected in its accounting on the basis of available primary documents.

In the act of reconciliation with the buyer, when reflecting the amount of the paid advance, the number and date of the payment document of the organization that paid the advance for the buyer, indicating its name, should be indicated. We believe that it would not be superfluous to also make a link to the letter (notification) of this organization.

In the act of reconciliation with a third party (the organization that paid the advance for the buyer), you should indicate the number and date of his payment document, you can make a link to the details of the letter (notification), and you should also indicate that in this case there was a payment for the buyer organization ( provide the name of this purchasing organization) and that the parties have no claims against each other.

It also seems advisable to have documents confirming payment of an advance payment for the buyer by a third party, one of which may be, in particular, a letter from the buyer requesting that the third party’s funds received into the supplier’s current account be offset against the buyer’s debt (see also the FAS resolution Central District dated April 15, 2010 N F10-145/09 in case N A08-4001/2008-12-5).

In the situation under consideration, due to the lack of notification to the buyer, confirmation of the will of a third party to pay the buyer’s debt is the fact that it sent a corresponding notification to the supplier, and in the purpose of payment in the payment documents there is a reference to the invoice issued by the supplier to the buyer (see also the resolution of the Federal Antimonopoly Service of the Ural District dated July 22, 2011 N F09-3921/11 in case N A76-19878/2010) (www.garant.ru)

lawedication.com

Let's sum it up

So, paying an obligation to a third party is a completely common and safe operation. It does not entail any negative consequences either for the payer or for the one for whom he makes the payment. It does not matter whether the payer and the debtor are in a contractual relationship or not. At the same time, this is very convenient, since it allows you to avoid unnecessary operations, delays in fulfilling obligations and related troubles. In this way, you can pay not only under contracts with counterparties, but also pay taxes.