Dismissal of an employee is an operation without which no organization can function. Let's consider the features of reflecting in 1C settlements with an employee upon dismissal, as well as the procedure for calculating and paying compensation for unused vacation.

You will learn:

- when should a settlement be made with a dismissed employee;

- what document is used to document the calculation of compensation?

- how to withhold and pay personal income tax to the budget from compensation for vacation pay;

- how and when insurance premiums are calculated.

Step-by-step instruction

September 05 Kolokoltsev I.F. wrote a letter of resignation at the employee's initiative. On the same day, an order was issued for his dismissal on September 19.

The employee has worked for the Organization since December 26, 2016. Last October, Kolokoltsev was on vacation and fully used his right to annual paid leave of 28 calendar days.

On September 19, Kolokoltsev received the following calculation:

- compensation for unused vacation;

- wages for September.

On the same day, the funds, according to the calculation, were transferred to I.F. Kolokoltsev’s personal card. taking into account the fact that on August 26 he received an advance payment for September in the amount of 16,000 rubles. In addition, personal income tax was paid to the budget.

Step-by-step instructions for creating an example. PDF

| date | Debit | Credit | Accounting amount | Amount NU | the name of the operation | Documents (reports) in 1C | |

| Dt | CT | ||||||

| Dismissal of an employee | |||||||

| 05 September | — | — | — | Order to dismiss an employee | Dismissal | ||

| Calculation of an employee upon dismissal | |||||||

| September 19 | 26 | 70 | 26 000 | 26 000 | 26 000 | Payroll | Payroll |

| 26 | 70 | 29 400 | 29 400 | 29 400 | Calculation of compensation for unused vacation | ||

| 70 | 68.01 | 7 202 | 7 202 | Withholding personal income tax | |||

| 26 | 69.01 | 1 606,60 | 1 606,60 | Calculation of contributions to the Social Insurance Fund | |||

| 26 | 69.03.1 | 2 825,40 | 2 825,40 | Calculation of contributions to the FFOMS | |||

| 26 | 69.02.7 | 12 188 | 12 188 | Calculation of contributions to the Pension Fund | |||

| 26 | 69.11 | 110,80 | 110,80 | Calculation of contributions to NS and PP | |||

| Paying salaries to an employee’s personal card | |||||||

| September 19 | — | — | 32 198 | Formation of payment statement | Statement to the bank - To employees' accounts | ||

| 70 | 51 | 32 198 | 32 198 | Salary payment | Debiting from a current account - Transferring wages to an employee | ||

| Payment of personal income tax to the budget | |||||||

| September 19 | 68.01 | 51 | 7 202 | Payment of personal income tax to the budget | Debiting from a current account – Tax payment | ||

Regulatory regulation

Providing compensation

Upon termination of the employment relationship, the employee is entitled to compensation for all days of unused vacation during all years of work in the organization (Article 127 of the Labor Code of the Russian Federation).

Leave to employees must be granted annually with preservation of their place of work (position) and average earnings (Article 114, Article 120 of the Labor Code of the Russian Federation).

In some cases, it is possible to replace annual leave with monetary compensation. For employees who continue to work in the organization, payment of compensation is possible only for additional vacation days exceeding 28 calendar days in the working year (Part 1 of Article 126 of the Labor Code of the Russian Federation).

Calculation of compensation upon dismissal

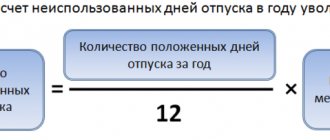

Compensation for unused vacation upon dismissal is calculated using the formula:

Compensation for unused vacation is subject to personal income tax (clause 1 of Article 210 of the Tax Code of the Russian Federation, clause 3 of Article 217 of the Tax Code of the Russian Federation) and insurance contributions (clause 2 of clause 1 of Article 422 of the Tax Code of the Russian Federation).

Number of unused vacation days

If an employee has worked part-time, the number of vacation days due to him is calculated based on the months worked during the working year:

Working year - a full 12 months worked by an employee from the date of his hiring to the date preceding the start of the new working year (clause 1 of the Rules on regular and additional leaves, approved by the People's Commissariat of Labor of the USSR 04/30/1930 N 169, Letter of Rostrud dated 12/18/2012 N 1519-6-1).

In this case, a month is considered fully worked if the employee worked half the days or more in it. If less than half a month is worked, it is not counted (clause 35 of the Rules on regular and additional leaves, approved by the People's Commissariat of Labor of the USSR on April 30, 1930 N 169: valid to the extent that does not contradict the Labor Code of the Russian Federation).

In our example, we will calculate the number of days for which the employee is entitled to vacation. Working years of Kolokoltsev I.F.:

- 1 year - from December 26, 2016 to December 25, 2017, 28 cal. days used;

- Year 2 - from December 26, 2017 to December 25, 2018, 28 cal. days used;

- 3rd year - from December 26, 2018 to September 19, 2019, of which worked: 8 full months (from December 26, 2018 to August 25, 2019);

- 25 calendar days of the ninth month of the working year (from 08/26/2019 to 09/19/2019). This is more than half a month: therefore, the ninth month is counted in full.

Calculation of days of unused vacation Kolokoltseva I.F.:

- 28 days / 12 months x 9 months = 21 days

If, as a result of calculating the number of days of unused vacation, a fractional number is obtained, labor legislation does not require rounding it. However, if the employer decides to round the number of vacation days, arithmetic rules cannot be applied: they always round in favor of the employee (Letter of the Ministry of Health and Social Development of the Russian Federation dated December 7, 2005 N 4334-17).

Average daily earnings

The average daily earnings of an employee are calculated based on the salary actually accrued to him and the time actually worked by him for the 12 calendar months preceding his dismissal (Article 139 of the Labor Code of the Russian Federation), according to the formula:

29.3 is the average monthly number of calendar days established by the Government for calculating the average daily earnings for paying vacations and compensation for unused vacations (clause 10 of the Regulations on the specifics of the procedure for calculating average wages, approved by Decree of the Government of the Russian Federation of December 24, 2007 N 922) .

During the specified 12 months, there are periods excluded from the calculation: such when (clause 5 of the Regulations on the specifics of the procedure for calculating average wages, approved by Decree of the Government of the Russian Federation of December 24, 2007 N 922):

- the employee retained his average earnings in accordance with the law, for example, during business trips, vacations;

- the employee did not work due to downtime;

- the employee was absent due to temporary disability or pregnancy and childbirth;

- the employee was on vacation at his own expense and others.

In these cases, the average daily earnings are calculated using the formula:

When calculating compensation for unused vacation or changing the minimum wage in the accrual period, it is necessary to compare the average monthly earnings (to calculate compensation) with the minimum wage: it cannot be lower than the federal minimum wage in force on the date of accrual of compensation (clause 18 of the Regulations, approved by the Decree of the Government of the Russian Federation dated 12/24/2007 N 922).

More information about the compliance of average monthly earnings with the minimum wage

Let us determine the average daily earnings of an employee according to our example, taking into account that in Kolokoltsev’s billing period there are payments and days excluded from the calculation.

Let's calculate the number of days actually worked by the employee during the billing period. Days must be counted in calendar days, taking into account the daily average established by the Government of the Russian Federation (29.3).

- During the billing period, I. F. Kolokoltsev worked for 11 full months. The number of days actually worked during this period was: 11 x 29.3 = 322.3 cal. day

- In October he went on vacation for 28 calendar days, so the number of days of work in October is:

31 days in October - 28 days of vacation = 3 cal. day

- They must be recalculated taking into account the average monthly number of calendar days:

29.3 x 3/31 = 2.84 cal. day

- Total days worked in the billing period:

322,3 + 2,84 = 325.14 cal. days

- The amount of earnings in the billing period is 455,196 rubles.

- Calculation of average daily earnings:

RUB 455,196 / 325.14 cal. days = 1,400 rub.

Now let's calculate the amount of compensation for unused vacation.

- The number of days of Kolokoltsev’s unused vacation is 21 days .

- Compensation for unused vacation was: 1,400 rubles. x 21 days = 29,400 rub.

How to calculate vacation compensation upon dismissal

After the organization is convinced of the need for payment, it faces the question: how to calculate compensation for unused vacation?

In accordance with the general rule, an employee who decides to leave the company has the right to receive monetary compensation for unused vacation in proportion to the total months worked in the company for which these days were accrued (clause 28 of the Vacation Rules, approved by the People's Commissariat of Labor of the USSR on April 30, 1930 No. 169, hereinafter referred to as the Rules).

However, if an employee decides to leave his previous place of work not of his own free will, but due to the occurrence of the circumstances listed in clause 28 of the Rules (for example, there was a reduction in staff), then the employer will have to pay him compensation in the amount of the full year worked , but only on condition that such an employee managed to work in the company from 5½ to 11 months (clause 28 of the Rules).

IMPORTANT! The above rule applies only if the employee has not worked for the company for a whole year. Otherwise, upon dismissal, compensation for unused vacation will be calculated according to the general procedure, i.e., in proportion to the time worked.

Other employees (who left the company not due to circumstances specified in clause 28 of the Rules) can also count on full compensation (as for a whole year), but only if on the date of leaving the organization they managed to work for 11 months, but did not complete the full year.

Dismissal of an employee

In order to correctly reflect in 1C the operations for calculating final wages and compensation for unused vacation, first of all, it is necessary to fire the employee.

The Dismissal document is created from the section Salaries and Personnel – Personnel Records – Personnel Documents – Create – Dismissal.

Study in detail the dismissal procedure and filling out the document using the example

Calculation of compensation for unused vacation upon dismissal: formula

In general, the formula for calculating compensation for unused vacation upon dismissal is as follows:

Rcompens. = Number of unused days × SRdnZr,

where: Rcompens. - amount of compensation ;

Number of non-users days — number of unused vacation days;

SRdnZr - employee’s earnings on average for 1 working day.

In order to determine the value of the SRdnZr, you need to have information about what salary was accrued to the employee who decided to leave the company during the last 12 months (before the dismissal). In addition, you should know exactly how many days out of these 12 months the employee actually performed work functions (clause 5 of the Decree of the Government of the Russian Federation “On the calculation of average wages” dated December 24, 2007 No. 922).

Calculation of an employee upon dismissal

Settings in 1C for calculating compensation

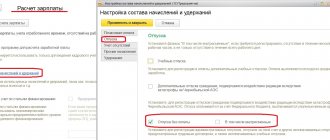

When installing the 1C program in the database, a predefined accrual type should be automatically created the Accruals : Leave compensation upon dismissal under the code KOT .

If it turns out that this accrual does not exist, then you should enter it into the Accruals from the section Salaries and Personnel - Directories and Settings - Salary Settings - Payroll - Accruals.

Please pay attention to filling out the fields:

Personal income tax section :

- switch - taxable ;

- income code - 2013 - Amount of compensation for unused vacation;

- Income category - Other income from work .

Section Insurance premiums :

- Type of income - Income entirely subject to insurance premiums ;

Section Income tax, type of expense under Art. 255 Tax Code of the Russian Federation :

- switch - taken into account in labor costs under article : - pp. 8, art. 255 of the Tax Code of the Russian Federation - Monetary compensation for unused vacation in accordance with the labor legislation of the Russian Federation;

- The checkbox Included in the basic accruals for calculating the “Regional coefficient” and “Northern bonus” accruals does not need to be set for the Accrual Compensation for unused vacation , since these accruals are already taken into account in the earnings that are used to calculate compensation.

Section Reflection in accounting :

- The method of reflection is not established. In this case, the compensation will be charged to the expense account set in the Expense Accounting the Employees directory for the salary of the employee to whom it is accrued. PDF

Compensation for an employee's unused vacation must be accounted for in the same cost account in which his salary is recorded.

The method of reflection in the Accruals takes precedence over the method specified in the Expense Accounting in the Employees . there is no need to set separate method of reflection in the Compensation for unused vacation (Accrual) .

Compensation for unused vacation is part of the salary, therefore, in accounting accounting, compensation is reflected as part of labor costs (clause 8 of PBU 10/99):

- Dt of the cost account, according to which the employee’s salary is calculated;

- CT “Settlements with personnel for remuneration” (chart of accounts 1C).

In NU, compensation for unused vacation is also taken into account in labor costs (clause 8 of Article 255 of the Tax Code of the Russian Federation) as part of direct or indirect expenses. The attribution of compensation costs to direct or indirect expenses depends on where the basic salary of the dismissed employee is allocated, according to the accounting policy.

In 1C, compensation for unused vacation will be reflected in the salary account specified in the Employees in the Expense Accounting .

Learn in more detail the definition of salary accounting methods (main postings)

Calculation of an employee upon dismissal

Compensation calculation is not automated in 1C and is reflected in the Payroll document in the Salaries and Personnel section - Salary - All accruals - Create button - Payroll calculation.

The document states:

- Salary for - the last month of work of the employee.

- from — the employee’s last day of work.

By clicking the Add , you must select the employee with whom the settlement is being made. The program will calculate wages based on the employee’s salary and the time worked by him on the date of dismissal.

Accrue button to select Accrual Compensation for unused vacation and indicate the calculated amount. The calculation of compensation must be done independently, for example, in an Excel table.

All amounts accrued to an employee can be viewed and, if necessary, adjusted in the Accruals , which opens by clicking on the link in the Accrued .

In the Accrual Payment Date column for accrual of Salary Payment is set automatically as the last day of the accrual month and cannot be adjusted.

To calculate Compensation for unused vacation, the payment date will be automatically set according to the date of the Payroll .

- Personal income tax - the amount of calculated personal income tax.

personal income tax link in the personal displays the calculation of personal income tax on an accrual basis for the employee for the current tax period.

The date of actual receipt of income in the form of wages, including compensation for unused vacation, is considered to be the last day of work for which income was accrued to the resigning employee (paragraph 2, paragraph 2, article 223 of the Tax Code of the Russian Federation).

In the personal income tax Salary Accrual document, the date will be recorded Date column

- actual receipt of income for both types of accrual - in the Dismissal Date Dismissal document . PDF

- personal income tax withholding - according to the date of the Payroll , which accrues wages and compensation.

Postings according to the document

The document generates transactions:

- Dt Kt - salary calculation for the last month of work;

- Dt Kt - calculation of compensation for unused vacation;

- Dt Kt 68.01 - calculation of personal income tax on the amount of wages and compensation;

- Dt Kt 69.01 - calculation of contributions to the Social Insurance Fund;

- Dt Kt 69.03.1 - calculation of contributions to the FFOMS;

- Dt Kt 69.11 - calculation of contributions to NS and PZ;

- Dr Kt 69.02.7 - calculation of contributions to the Pension Fund.

Despite the fact that the Salary Accrual was issued on the last day of the employee’s work, the calculation of salaries and contributions in the BU and NU accounts in 1C is carried out on the last day of the month.

Documenting

The organization must approve the forms of primary documents, including for calculating payments upon dismissal. As a basis, you can take form T-61 “Note-calculation upon termination (termination) of an employment contract with an employee (dismissal)” (approved by Resolution of the State Statistics Committee of the Russian Federation dated January 5, 2004 N 1).

- Excel

Income tax return

In our example, the salary of I.F. Kolokoltsev is taken into account on account 26 “General business expenses” and in tax accounting refers to indirect (other) expenses.

In the income tax return, the costs of wages and compensation for unused vacation, as well as insurance premiums accrued from them, will be reflected in indirect expenses only after the Closing of accounts 20, 23, 25, 26 is carried out in the Closing of the month procedure: PDF

- Sheet 02 Appendix No. 2 page 040 “Indirect costs - total”: wages;

- compensation for unused vacation;

- insurance premiums;

- insurance premiums.

See also What to do so that page 041 is filled in automatically

How to calculate compensation upon dismissal: counting the days

First of all, you need to find out what the “vacation” length of service of the employee who decided to quit is. That is, for how many full months of performing his duties in the company he is entitled to the corresponding number of vacation days.

Rarely does anyone have an exact number of months worked at the time of dismissal. Much more often in practice, a different situation is common: on the day of dismissal, a month has not been fully worked. How to calculate compensation upon dismissal in this situation is described in paragraph 35 of the Rules:

- if more than half a month has been worked, you need to count such a month as a full month;

- if less than half a month is worked, such period is not taken into account.

For calculation purposes, a month is understood not as a separate calendar month, but as the month of actual performance of labor functions by an employee in a specific company from the moment he was hired by the company (for example, from June 16 to July 16).

A practical example prepared by ConsultantPlus experts will help you correctly calculate your length of service. You can watch it right now with free access to the system.

After determining the “vacation” period, the accountant must calculate the number of days of unused vacation. How to calculate compensation upon dismissal depends on which days the employee’s vacation was accrued—calendar or working days.

If leave was granted in calendar days, then you need to proceed as follows.

For each month of work, the employee is accrued 2.33 days of vacation (letter of Rostrud dated October 31, 2008 No. 5921-TZ). Next, by multiplying the value of 2.33 and the “vacation” experience, the total number of vacation days is calculated. After this, those days that the employee has already taken off work before are subtracted from the total value.

This is discussed in more detail in the article “How to calculate the number of vacation days upon dismissal.”

Important! The exception is those persons who managed to work in the company for more than 11 months, but decided to leave it without working for the company for a year. In such cases, the organization pays compensation in full annual amount, i.e., as if the entire year had been worked.

The formula for calculating unused vacation days looks like this:

Number of non-users days = Number of months slave. × 2.33 – Disp.,

Where:

Number of non-users days _ — number of unused vacation days;

Number of months slave. — the number of months during which the employee was registered with the company;

Disp. — the number of vacation days used by the employee.

Important! When calculating compensation, the days remaining from vacation must be rounded in favor of the employee (up), and not according to arithmetic rules. For example, an employee was hired by the organization on March 27, 2020, and left on June 4, 2020. In this case, the number of days of unused vacation is 4.66 calendar days (2.33 calendar days for the period from March 27, 2020 to April 26, 2020 and 2.33 calendar days for the period from April 27, 2020 to May 26, 2020. Period from May 27 to 04.06 is not taken into account since it is less than half a month).

Let's look at how to calculate vacation compensation upon dismissal if an employment contract was concluded with the employee for the period of seasonal work. In this case, vacation is accrued according to the Labor Code of the Russian Federation in working days (Article 295). For 1 month of work, in this case, not 2.33 calendar days are required, but 2 working days of vacation (Article 139 of the Labor Code of the Russian Federation).

Therefore, the formula for calculating the remaining vacation days will be slightly different:

Number of non-users days = Number of months slave. × 2 – Disp.

Payment of personal income tax to the budget

Personal income tax on compensation for unused vacation is paid no later than the day following the day it is paid to the employee (clause 6 of Article 226 of the Tax Code of the Russian Federation).

Payment of personal income tax to the budget is reflected in the document Write-off from the current account transaction type Tax payment in the Bank and cash desk section - Bank - Bank statements - Write-off button.

The document states:

- Transaction type - Tax payment ;

- Tax - personal income tax when performing the duties of a tax agent ;

- Type of liability - Tax ;

- for - September 2019 , the month of income accrual (payments upon dismissal).

Learn more about reflecting personal income tax payments to the budget

Postings according to the document

The document generates the posting:

- Dt 68.01 Kt - payment of personal income tax to the budget for September.

Is compensation for unused vacation calculated upon dismissal in 2021?

In practice, situations often arise when an employee does not have time to take all the paid leave due to him under the Labor Code.

And if such an employee suddenly decides to leave the company, the question will arise: what to do with the unused part of the vacation? Should I take the remaining days off or can I receive monetary compensation for them? In addition, does the reason for which the employment contract was terminated matter? And how will compensation for unused vacation be calculated upon dismissal? The Labor Code of the Russian Federation clearly answers: the employer must pay the former employee compensation for unpaid vacation upon dismissal, i.e. for each unused day.

The period from 03/30/2020 to 05/11/2020 has been declared non-working due to the spread of coronavirus infection. Is it possible to fire an employee on non-working days and what risks are possible for the employer, ConsultantPlus experts explained.

Get trial access to the system and upgrade to the ready-made solution for free.

An employee’s right to calculate compensation for unused vacation and its payment upon dismissal does not depend on the basis on which the employment contract was terminated (letter of Rostrud dated July 2, 2009 No. 1917-6-1).

6-NDFL

Tax amounts are calculated by tax agents on the date of actual receipt of income on an accrual basis from the beginning of the tax period (clause 3 of Article 226 of the Tax Code of the Russian Federation). In the reporting, the date of receipt of income is reflected on page 100 of Section 2 of Form 6-NDFL. Its definition depends on the type of income. For compensation for unused vacation and other amounts upon dismissal, income will be received on the day it is paid to the taxpayer (clause 1, clause 1, article 223 of the Tax Code of the Russian Federation).

In 1C, for our example, the date of actual receipt of income is indicated in the Date of the document Write-off from the current account . PDF

In Form 6-NDFL, the accrual and payment of annual leave is reflected in:

Section 1 “Generalized indicators”:

- line 020 - 55,400, amount of accrued income;

- pp. 040 - 7 202, amount of calculated tax;

- pp. 070 - 7 202, amount of tax withheld.

Section 2 “Dates and amounts of income actually received and withheld personal income tax”: PDF

- page 100 - 09.19.2019, date of actual receipt of income;

- page 110 - 09/19/2019, tax withholding date.

- page 120 - 09/20/2019, tax payment deadline.

- pp. 130 - 55,400, the amount of income actually received.

- pp. 140 - 7,202, amount of tax withheld.

Compensation for unpaid leave upon dismissal: payment procedure

As a general rule, the company must calculate compensation for unused vacation upon dismissal and pay it to the resigning employee on his last day of work (Article 140 of the Labor Code of the Russian Federation).

Important! If the resigning employee for any reason was not at work on his last working day, the company is obliged to pay all amounts due no later than the next day after the dismissed employee submitted a request for payment.

Therefore, on the last working day, an employee who decides to leave his place of work must receive compensation from the company for unpaid vacation.

Compensation for unpaid leave can be documented using a form developed by the employer independently, or unified form No. T-61.

For more information about form No. T-61, see the article “Unified form No. T-61 - form and sample.”

Checking mutual settlements

Mutual settlements with an employee

You can check mutual settlements with an employee using the report Balance sheet for the account “Settlements with personnel for wages” in the Reports section - Standard reports - Account balance sheet.

It is logical to generate the report on the date of dismissal: in our example it is September 19. However, entries in accounting for calculating compensation and wages upon dismissal in the account “Settlements with personnel for wages” were generated only on September 30. Therefore, the report must be generated on this date.

The report shows that there is no debt to the dismissed employee at the end of the month.

Mutual settlements with the budget for personal income tax

To check the calculations with the budget for personal income tax, you can generate the report Analysis of account 68.01 “Personal income tax when performing the duties of a tax agent” in the section Reports - Standard reports - Account analysis.

In our example, payment of compensation and wages was carried out on September 19, the deadline for transferring personal income tax was September 20, i.e. the day following the day of payment. But in the accounting system, under the credit of account 68.01 “Personal income tax when performing the duties of a tax agent,” personal income tax, like wages, was accrued on September 30.

The absence of a final balance in account 68.01 “Personal income tax when performing the duties of a tax agent” means that there is no debt to pay personal income tax to the budget.

The accountant is used to this report, but it does not give an up-to-date picture of mutual settlements with the budget for personal income tax, since data on withheld and transferred personal income tax is accumulated in personal income tax registers, and not in accounting accounts. Therefore, we recommend that you use the report Control of personal income tax payment deadlines . In our opinion, it is more informative.

Control of personal income tax payment deadlines

To check the calculations with the budget for personal income tax, as well as the deadlines for payment, you can generate a report Control of deadlines for personal income tax payment in the section Salaries and personnel - Salary - Salary reports - Control of deadlines for personal income tax payment.

In our example, payment of compensation and wages was carried out on September 19, the deadline for transferring personal income tax was September 20, i.e. the day following the day of payment. We will generate a report for the period September 19-20 for Kolokoltsev I.F. To generate the necessary data, use the Settings to set:

- View - Advanced .

Selections tab by clicking the Add selection :

- Field - Individual ;

- Condition - Equal to ;

- Meaning - Kolokoltsev Ivan Fomich ;

- — In the header of the report.

Fields and sorting tab - do not change the existing settings.

Structure tab on the Add :

- Grouped fields - Recorder , check the box.

After completing the setup of the Personal Income Tax Payment Deadline Control , you must click the Close and generate . The program will generate a report.

- Write-off from the current account dated 09.19.2019 N 5 - a document of payment to the employee of amounts upon dismissal, established the deadline for paying the debt to the budget - 09.20.2019.

- Write-off from the current account dated September 19, 2019 N 6 - personal income tax payment document, repaid the debt to pay tax to the budget.

The absence of a final balance on the personal income tax payment due date indicates that personal income tax was paid to the budget on time.

Test yourself! Take a test on this topic using the link >>

See also:

- Salary settings in 1C

- Payroll

- Accrual of vacation pay

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

- Payroll Let's consider the features of calculating wages and insurance premiums in 1C....

- Test No. 60. Compensation for unused vacation upon dismissal...

- Amounts of the minimum wage, benefits, insurance premium rates in 2018-2020 Amounts of the minimum wage, benefits, insurance premium rates in 2018-2020...

- Accrual of vacation pay Let's consider the features of reflecting in 1C the accrual and payment of vacation pay to an employee....

How to calculate compensation for unused vacation upon dismissal, if the vacation is additional

There are often situations where an employee who has decided to leave the company did not have time to take not only his annual leave, but also did not take advantage of the days of additional leave.

Such leave is provided to the employee under a collective agreement. For example, a collective agreement may stipulate that upon reaching a certain length of service in the company, an additional few days of vacation are granted.

In such a situation, it is important to remember that days of additional leave must be compensated in accordance with the general procedure (described above), i.e., as if these were days of regular annual leave. This conclusion follows from Art. 127 of the Labor Code of the Russian Federation, which states that when an employee is dismissed, the employer must compensate him (in monetary terms) for all unused vacations.

Therefore, when calculating compensation for unused vacation upon dismissal in 2021, it is important to strictly follow the general procedure described above.

We described in detail about compensation for unused vacation without dismissal here.

In addition to compensation for missed vacation, the employer is obliged to pay the employee wages. Find out how to calculate it correctly here.