The legal topic is very complex, but in this article we will try to answer the question “Which depreciation group does a washing machine belong to in 2021?” Of course, if you still have questions, you can consult with lawyers online for free directly on the website.

When registering, PF objects are assigned to a specific depreciation group. There are 10 of them in total; they are listed in the OS Classification by depreciation groups. The main criterion for combining units of property into any of the depreciation categories is the useful life (USI) of the object. It is determined by enterprises for each PF facility, based on the expected useful period, operating conditions and regulations governing the use of the property.

Depreciation groups: useful life

- Machinery and equipment, incl. office, tunneling, hay harvesting machines, technological equipment for various industries (OKOF codes 330.28);

- Vehicles with OKOF codes 310.29.10;

- production and economic equipment (sports facilities 220.42.99);

- perennial plantings (520.00.10).

Related publications

The third depreciation group combines assets whose life expectancy varies from 3 to 5 years. The range of assets that wear out within these periods is noticeably wider in comparison with the two above groups. In addition to the listed types of property, depreciation group 3 contains:

Depreciation groups of fixed assets are a breakdown of fixed assets into groups based on their useful life. It is used to calculate depreciation. The division of this property is carried out on the basis of the All-Russian Classifier of Fixed Assets (OKOF 2021). Based on the period, the depreciation rate is calculated. In the article you will find a table and a Directory of all OS groups current for 2021.

Depreciation group of fixed assets 2021

Step 3. Establish the exact service life of the object. After all, according to the OKOF code, the classifier gives a “fork” in terms of service life. For example, for passenger cars from the third depreciation group - over three years and up to five years inclusive. The company sets the exact period of use of the object itself - within the terms according to the Classifier.

Classifier of fixed assets by depreciation groups 2020

Depreciation groups of fixed assets are a breakdown of fixed assets into groups based on their useful life. It is used to calculate depreciation. The division of this property is carried out on the basis of the All-Russian Classifier of Fixed Assets (OKOF 2020). Based on the period, the depreciation rate is calculated. In the article you will find a table and a Directory of all OS groups current for 2021.

The OKOF 2021 classifier is a table that includes 22 groups. Groups include codes and names of fixed assets. The code has the following structure: ХХХ.ХХ.ХХ.ХХ.ХХХ. Each group of symbols contains certain information about the OS object.

The most widespread practice is to use a general standard based on dividing fixed assets into single depreciation groups. The most detailed classification, logically related to grouping by age, by natural material, is called the OKOF classification.

Important Notes

Simply put, there is no need to re-determine the depreciation group of an asset purchased earlier, even if, according to OKOF-2020 with decoding and group, the useful life of such an object would have to change.

This type of mixture is also called warm, and it is prepared using bitumen, which has a reduced viscosity. All cars require registration. It is paid by the legal entity. If you have to work outside in winter, then your clothing must match. Budget characteristics for 2021 and 2021

This indicates the introduction of other operational periods for them, and, consequently, a change in the period for writing off their original cost in tax accounting. Innovations apply only to operating systems introduced on January 1 of the year. There is no need to re-determine the depreciation group of fixed assets available to the enterprise.

Application of depreciation groups of fixed assets according to OKOF in 2021

Step 2. Find this OKOF code in the current edition of the Classifier of fixed assets by depreciation groups 2021. For example, a passenger car with the OKOF code 310.29.10.2 is listed as part of the transport in the “Third depreciation group” section of the Classifier.

Depreciation group of fixed assets 2021

Step 3. Establish the exact service life of the object. After all, according to the OKOF code, the classifier gives a “fork” in terms of service life. For example, for passenger cars from the third depreciation group - over three years and up to five years inclusive. The company sets the exact period of use of the object itself - within the terms according to the Classifier.

We recommend reading: Who is entitled to free travel on the train in St. Petersburg from April 27, 2021

Not all OKOF codes are in the Classification; many assets are not in OKOF at all. For such objects, it is worth first determining the useful life and establishing a depreciation group for it. To find out this period, refer to the technical documentation for the fixed asset. For example, a technical passport or warranty card (clause 6 of Article 258 of the Tax Code of the Russian Federation). The algorithm of actions when choosing a depreciation group depends on whether the asset is in the Classification. There are three possible courses of action.

Do not throw away documents on depreciable assets, despite the fact that the Ministry of Finance advises keeping them for only four years. Financiers considered the situation only from the point of view of tax accounting. There are other norms.

How to determine the depreciation group of a fixed asset in 2021

When an object is not in the Classification, you need to focus on OKOF codes that are assigned to higher-level groupings. The OKOF code has the following structure: XXX.XX.XX.XX.XXX. To determine the depreciation group of a fixed asset, first replace the last digit in the OKOF code with zero. The result will be a grouping of a higher level. Check if it is in the Classification.

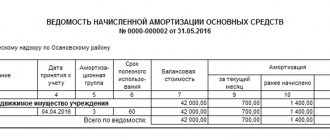

If the institution has registered property objects and groups of fixed assets, then the accountant is obliged to charge depreciation on a monthly basis, that is, transfer the cost of fixed assets in parts based on their wear and tear. Depreciation deductions are made during the operational period of the main asset, starting from the first day of the month following the month the fixed asset was accepted for accounting (clause 21 of PBU 6/01). In tax accounting, depreciation is charged on fixed assets and their groups from the first day of the month following the month the asset was put into operation (clause 4 of Article 259 of the Tax Code of the Russian Federation). Depreciation charges in accounting are calculated in one of 4 ways - linear, reducing balance, write-off of value in proportion to the volume of goods, work, services, write-off of cost by the sum of the number of years of the joint venture.

Fishing tools for eliminating drilling accidents; tools and devices for cutting off second trunks; drilling tools (except rock cutting tools); a tool for screwing-unscrewing and holding tubing pipes and rods suspended during the repair of production wells; fishing tools for production wells; tool for drilling geological exploration wells; tools for oilfield and geological exploration equipment, other

How to use the fixed asset classifier

Mobile scraper belt conveyors; equipment, tools and fixtures, fastening devices for the production and installation of ventilation and sanitary products and products; mechanisms, tools, devices, instruments and devices for electrical installation and commissioning work on equipment for industrial enterprises

Fixed assets (FPE) of an organization, depending on their useful life (SPI), for profit tax purposes are assigned to one or another depreciation group (Clause 1, Article 258 of the Tax Code of the Russian Federation). The useful life of the OS is determined by the organization itself, taking into account the classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1 (Resolution No. 1).

We recommend reading: How to change the GKP to a nursery

How to determine the SPI of an object

Determining the SPI of an object occurs in several stages:

Stage 1. Establishing the depreciation group to which the object belongs.

For tax purposes, the Classification determines:

- Depreciation group. There are ten groups in total, property is distributed among them depending on the private investment property.

- SPI. It must be within the deadlines set for a particular group.

The depreciation group can be determined by OKOF. This is done as follows:

- In the first column of the classifier, the type of property to which the object belongs is searched;

- In the first column of the Classification, you need to check the code written in OKOF;

- If the code is in the Classification, you can see which group the OS belongs to.

If the Classification does not contain the code of the required asset, the depreciation group can be determined in one of two ways:

- By OS subclass code;

- By OS object class code.

Stage 2. Definition of SPI. If there is no mention of an object in the OKOF, the SPI is determined based on the period of use of the object, which is indicated in the manufacturer’s recommendations and technical documents.

Stage 3. Fixing SPI in the object’s inventory record card. If accounting and tax accounting are maintained differently, then the corresponding column must be added to the second section of the inventory card.

Similar articles

- All-Russian classifier of fixed assets 2021

- Useful life of fixed assets – 2017 classifier

- Accrual of depreciation of fixed assets in 2021

- Calculation of depreciation of fixed assets

- All-Russian classifier of fixed assets by depreciation groups

Depreciation groups of fixed assets: how to determine in 2021

The property subclass code differs from the property type code in that the seventh digit in it is always zero. For example, a rotary pump belongs to subclass 14 2912021 (centrifugal, piston and rotary pumps). If this code is not included in the OS classification, determine the depreciation group using the second method.

How to determine the useful life of an OS

- In the first column of OKOF, find the type of property to which the OS belongs (9 digits).

- Check the code specified in the OKOF in the first column of the OS classification.

- If there is a code in the OS classification, look at which depreciation group the OS belongs to.

An error when choosing a depreciation group for a fixed asset can lead to the additional charge of two taxes at once - on profit and on property. Inspectors very often find such errors: this was recently confirmed by the Federal Tax Service in a review of typical violations. Download a cheat sheet that will help you always accurately determine the depreciation group.

Depreciation groups of fixed assets in 2021: how to determine according to OKOF

The organization determines the useful life of a fixed asset in order to calculate depreciation in accounting and tax accounting. From 12 May 2021, accountants will apply the updated Classification of Property, Plant and Equipment. Let's tell you in more detail what has changed and how to determine depreciation groups in 2021.

Express courses

Intensives on hot topics at Kontur.School

Schedule

Fixed assets (FPE) of an organization, depending on their useful life (SPI), for profit tax purposes are assigned to one or another depreciation group (Clause 1, Article 258 of the Tax Code of the Russian Federation). The useful life of the OS is determined by the organization itself, taking into account the classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1 (Resolution No. 1).

In 2021, all depreciation classification groups have changed, except the first. The changes apply to legal relations arising from January 1, 2021.

Most of the amendments are in the subsection “Structures and transmission devices” of the second to tenth groups. The list of fixed assets in the “Machinery and Equipment” subsection of the second and ninth groups has been expanded.

Classifier of fixed assets by depreciation groups with examples of fixed assets:

Depreciation group number Useful life of fixed assets Example of fixed assets belonging to the depreciation group

| 1 | From 1 year to 2 years inclusive | General purpose machinery and equipment |

| 2 | Over 2 years up to 3 years inclusive | Liquid pumps |

| 3 | Over 3 years up to 5 years inclusive | Radio-electronic communications |

| 4 | Over 5 years up to 7 years inclusive | Fences (fences) and reinforced concrete barriers |

| 5 | Over 7 years up to 10 years inclusive | Forest industry buildings |

| 6 | Over 10 years up to 15 years inclusive | Water intake well |

| 7 | Over 15 years up to 20 years inclusive | Sewerage |

| 8 | Over 20 years up to 25 years inclusive | Main condensate and product pipelines |

| 9 | Over 25 years up to 30 years inclusive | Buildings (except residential) |

| 10 | Over 30 years | Residential buildings and structures |

The All-Russian Classifier of Fixed Assets (OKOF), which determines the depreciation group of fixed assets, remains unchanged. Since January 1, 2017, OKOF OK 013-2014 (SNS 2008), approved by Rosstandart order No. 2018-st dated December 12, 2014, has been in effect. The same classifier will be in effect in 2021.

Stage 1 - establish the depreciation group of the fixed asset according to the classification approved by Resolution No. 1

The classification of fixed assets is a table in which, for each depreciation group, the names of the fixed assets included in it and the corresponding codes of the All-Russian Classifier of Fixed Assets are listed.

For tax accounting purposes, according to the classification of fixed assets, the following is determined:

- depreciation group to which the fixed asset belongs. All depreciable property is combined into 10 depreciation groups depending on the useful life of the property (clause 3 of Article 258 of the Tax Code of the Russian Federation). Depreciation groups are also important in determining the amount of depreciation bonus that can be applied to a specific asset;

- the useful life must be within the limits established for each depreciation group (Letter of the Ministry of Finance of Russia dated July 6, 2016 No. 03-05-05-01/39563). Choose any period within the SPI, for example the shortest, in order to quickly write off the cost of the fixed assets as expenses (Letter of the Ministry of Finance of the Russian Federation dated July 6, 2016 No. 03-05-05-01/39563).

You can set an entire OS group in the classification. A transcript of the group is presented in OKOF.

Define the depreciation group of the fixed asset as follows:

- In the first column of OKOF, find the type of property to which the OS belongs (9 digits).

- Check the code specified in the OKOF in the first column of the OS classification.

- If there is a code in the OS classification, look at which depreciation group the OS belongs to.

If there is no code in the OS classification, determine the depreciation group in one of the following ways:

Method 1 - by property subclass code

The property subclass code differs from the property type code in that the seventh digit in it is always zero. For example, a rotary pump belongs to subclass 14 2912010 (centrifugal, piston and rotary pumps). If this code is not included in the OS classification, determine the depreciation group using the second method.

Method 2 - by property class code

The property class differs from the property type code in that the seventh, eighth and ninth digits in it are always zeros. For example, a rotary pump belongs to class 14 2912000 (pumps and compressor equipment).

Example . Determination of depreciation group using OKOF code

The rotary pump code according to OKOF is 14 2912113. In the OS Classification, such a code, as well as subclass code 14 2912010 (centrifugal, piston and rotary pumps) are not indicated.

However, it contains class code 14 2912000 (pumps and compressor equipment). It belongs to the third depreciation group (property with a useful life of more than three years up to five years inclusive).

This means that the rotary pump must be included in the third shock-absorbing group.

Step 2: Consult technical documentation

If the fixed asset is not mentioned in the classification and OKOF, establish the SPI from the operating life of the OS specified in the technical documentation or manufacturer’s recommendations (clause 6 of Article 258 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of Russia dated June 18, 2018 No. 03-03-20/41332) .

Stage 3. Record the SPI in the asset accounting inventory card (Form No. OS-6)

If the tax and accounting SPI are different, then add section 2 of form No. OS-6 with the corresponding column.

Example. The organization purchased a Gazelle cargo truck (carrying capacity 1.5 tons). Let's determine the SPI of the car.

According to the OS classification, general purpose trucks with a carrying capacity of over 0.5 and up to 5 tons inclusive are included in the 4th depreciation group.

The SPI range for the 4th depreciation group is over 5 and up to 7 years inclusive. Therefore, the minimum possible SPI in months is 61 (5 years x 12 months + 1 month), the maximum is 84 months. (7 years x 12 months).

The organization has the right to establish any vehicle SPI in the range from 61 to 84 months inclusive.

Please note when accounting for OS

- In tax accounting, the cost criterion for recognizing an asset is 100,000 rubles, in accounting – 40,000 rubles.

- Maintain accounting of fixed assets in 2021 in the same order as before: take into account the fixed assets on the date of bringing them to a state of readiness for operation. If you sell an operating system, then include the remuneration received as income, and the residual value of the operating system as expenses. Similar rules apply to the sale of unfinished properties.

- In accounting, an organization is not obliged to adhere to depreciation groups, but for convenience it can determine the period according to the classification of fixed assets. This is convenient, as it brings accounting closer to tax accounting.

- If the object meets all the criteria named in clause 4 of PBU 6/01, then in accounting it should immediately be transferred to fixed assets, that is, capitalized on account 01. The actual use of the object, unlike tax accounting, is optional.

Source: https://School.Kontur.ru/publications/1479

Which depreciation group does a passenger car belong to?

Now let's figure out how car depreciation is calculated. To make the calculation, first determine the useful life of the fixed asset. To do this, use tables with depreciation groups.

Depreciation period of a passenger car

The depreciation period is the useful life, i.e. the period of time when the machine brings benefits to the company. It is during this period that you will charge depreciation. Determine the deadline for the date of commissioning.

If the vehicle falls into one of these groups, then the organization determines the SPI within the period provided for the corresponding group. For example, for a passenger car with an engine capacity of over 3.5 liters, the SPI can be set from 85 months to 120 months inclusive.

Depending on the useful life (SPI), depreciable property (fixed assets and intangible assets) is distributed into depreciation groups (clause 1 of Article 258 of the Tax Code of the Russian Federation). We will tell you which depreciation groups vehicles belong to in our consultation.

How to determine the depreciation group of a car?

Depreciation groups of fixed assets, incl. vehicles are determined in accordance with the Classification of fixed assets included in depreciation groups (Government Decree No. 1 of 01.01.2002). In this Classification, fixed assets are distributed into depreciation groups from I to X. Depreciation group I includes fixed assets with a fixed income of more than 1 year to 2 years inclusive, and X includes fixed assets with a fixed income of more than 30 years. We talked more about the updated Classification of fixed assets, which is valid from 01/01/2021, in our consultation.

We recommend reading: How to calculate maternity leave 2021 in Bashkiria

The borrower's accountant determined that the resulting building, according to the Classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1, belongs to the eighth depreciation group (useful life - from 20 to 25 years). The useful life is set at 250 months. As a result of the reconstruction of the building, the useful life did not change.

The safest (from the point of view of calculating income tax) is to follow the second position. Since a decrease in the useful life of a fixed asset after its transfer to non-residential assets (the first option) will entail a faster (compared to the second option) transfer of the cost of the object to the organization’s expenses. Therefore, during an audit, the tax office may not agree with this approach and may not recognize part of the depreciation deductions. In this case, the organization will have to defend its position in court. Arbitration practice on the issue under consideration has not yet developed.

Documenting

The following arguments can be given in favor of the first option. In the situation under consideration, when a property is transferred to non-residential use, its use does not cease, and the property itself remains on the balance sheet of the organization. Only the purpose of the object and the nature of its operation change. Consequently, the organization has grounds to, without changing the overall useful life of the object, exclude from it the period during which the object was part of the housing stock. From this point of view, depreciation on such an object must be accrued over the remaining useful life minus the period of its actual operation as a residential property. This conclusion does not contradict the provisions of Article 258 of the Tax Code of the Russian Federation.

- this is owned property (unless otherwise provided by Chapter 25 of the Tax Code of the Russian Federation);

- used to generate income;

- the cost of property is repaid gradually, by calculating depreciation;

- the price exceeds 100 thousand rubles;

- The SPI is at least 1 year.

Download the full classifier of fixed assets by depreciation groups

All property assets whose value does not exceed 40,000 rubles are immediately written off as inventories. At the discretion of the accountant, they are registered in the fixed assets group and depreciation is calculated. All objects costing over 40,000 rubles are accounted for as a group of fixed assets. They are subject to monthly depreciation.

How to calculate depreciation on fixed assets

Mobile scraper belt conveyors; equipment, tools and fixtures, fastening devices for the production and installation of ventilation and sanitary products and products; mechanisms, tools, devices, instruments and devices for electrical installation and commissioning work on equipment for industrial enterprises

Fixed assets (FPE) of an organization, depending on their useful life (SPI), for profit tax purposes are assigned to one or another depreciation group (Clause 1, Article 258 of the Tax Code of the Russian Federation). The useful life of the OS is determined by the organization itself, taking into account the classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1 (Resolution No. 1).

Fixed assets were not found in any depreciation group: how to determine the useful life

If the fixed assets are not found in the mentioned classification and are not included in any of the depreciation groups, then according to clause 6 of Art. 258 of the Tax Code of the Russian Federation, SPI can be installed according to technical specifications or according to the manufacturer’s recommendations. Moreover, the simultaneous use of both classification and technical conditions is excluded. That is, if an asset is assigned to a certain depreciation group, then its SPI is established exclusively within this depreciation group and it is prohibited to determine it according to the manufacturer’s technical conditions.

How to determine the useful life of an OS

The All-Russian Classifier of Fixed Assets (OKOF), which determines the depreciation group of fixed assets, remains unchanged. Since January 1, 2020, OKOF OK 013-2014 (SNS 2008), approved by Rosstandart order No. 2020-st dated December 12, 2014, has been in effect. The same classifier will be in effect in 2021.

Stage 1 - establish the depreciation group of the fixed asset according to the classification approved by Resolution No. 1

The rotary pump code according to OKOF is 14 2912113. In the OS Classification, such a code, as well as subclass code 14 2912010 (centrifugal, piston and rotary pumps) are not indicated. However, it contains class code 14 2912000 (pumps and compressor equipment). It belongs to the third depreciation group (property with a useful life of more than three years up to five years inclusive). This means that the rotary pump must be included in the third shock-absorbing group.

According to Article 258 of the Tax Code of the Russian Federation, the useful life is the period during which an object of fixed assets serves to fulfill the goals of the organization's activities. The same article of the Tax Code of the Russian Federation describes the basic rules for determining the useful life of fixed assets available in an organization.