Features of transport tax for legal entities

Transport tax for legal entities, as well as for individuals, is calculated using a simple formula:

Tax base × tax rate.

In addition, decreasing/increasing coefficients can also be added to this formula, and the tax rate in the region can be reduced or increased in relation to the basic values specified in paragraph 1 of Art. 361 Tax Code of the Russian Federation. But the tax rates established in the constituent entities of the federation cannot differ from the base ones by more than 10 times - such a limitation is specified in paragraph 2 of Art. 361 Tax Code of the Russian Federation.

Read more about the procedure for calculating transport tax for cars in our article “How to calculate transport tax for a car?” .

For expensive cars, the cost of which exceeds 3 million rubles, an increasing factor is applied. This coefficient can be found in paragraph 2 of Art. 362 of the Tax Code of the Russian Federation. Its value depends not only on the cost of the car, but also on the period of its use after release. Prices for luxury cars are updated annually and are available for viewing on the official website of the Ministry of Industry and Trade.

Taxpayers who are legal entities, unlike individuals, must calculate their taxes independently. Despite the fact that tax returns for 2020 have been canceled for organizations, and the Federal Tax Service must send them messages with the amount already calculated, legal entities must still calculate the tax themselves. First, they must know the amount in order to make advance payments throughout the year (if they are established in the region). And secondly, the message from the tax office is more of an informational nature, so that the company can compare its accruals with those made according to the tax authorities. After all, she will receive it after the deadline for paying advances (see, for example, letter of the Ministry of Finance dated June 19, 2019 No. 03-05-05-02/44672).

The message from the Federal Tax Service will indicate the object of taxation, tax base, tax period, rate and amount of calculated tax.

Important! Recommendation from ConsultantPlus Compare the amount of tax calculated by the inspectorate with the amount you calculated and paid yourself. If they are equal, then the tax was calculated and paid correctly. If the amounts differ, check:... What to check and what to do in case of an error (yours or the tax authorities), see K+. Trial access to the system can be obtained for free.

ATTENTION! If you do not receive the notification, you are required to independently inform the tax authorities about your taxable property. Read about the nuances in the material “Organizations will have to report transport and land plots to the tax authorities.”

What is the corporate income tax (CIT) rate?

Corporate income tax is a monetary levy levied on the profits made by legal entities. The role of taxpayer is not only corporations, as one might think based on the name, but also any enterprises that have the status of legal entities. In the Russian Federation, an analogue is the income tax.

Foreign countries actively use CIT to fill the state budget. The tax rate varies depending on the country of application of the tax and is (in descending order):

- 40.55% – used in Egypt for the oil industry. However, insurance companies, investment funds and banks pay 40% CIT in this country. The base rate is considered to be 20%.

- 37% – for Thailand. In this country it is progressive in nature and in its minimum expression is 10%.

- Spain charges 35%. Small businesses here pay either 30% or 20%. It all depends on how profitable the company was in the current year. A 20% tax rate is provided for cooperatives, and 10% for mutual funds.

- 33.48% - in Japan. Prefectural and municipal allowances are also added here.

- 33.99% is the basic CIT rate in Belgium. A progressive taxation system is used.

- 33% is collected in Turkey.

- 30% - in the UK for businesses that received a total income during the year of more than 300,000 pounds. Tax rates here change annually depending on the profit received by the company. If income is less than 300,000, then the rate is reduced to 20%.

- 28.5% - in Luxembourg. However, this already includes a municipal tax and a contribution to the fund for non-working citizens. In its pure form the rate is 21%. 15% tax is taken from the amount of dividends paid. Interest income is not subject to taxation.

- 28% is equal to the CIT in Finland.

- 27–25% is the fee in Portugal. For small businesses whose annual income is less than the established limit, the CIT rate is reduced to 20%.

- 25.5% is collected from legal entities in the Netherlands if the annual profit exceeds 200,000 euros. If the company's income is 40–200 thousand euros, they pay 23.5%. When earned less than 40,000 euros – 20%. Dividends are not taxed.

- 25% is the base rate in Ireland, Barbados and Austria. All Austrian businessmen pay CIT at a single interest rate. Whereas in Ireland it was decided to set it for trading companies at 12.5%. The Government of Barbados is interested in attracting large international companies to the country, so the tax for them is 1%-2.5%. Small businesses in this country pay 15%.

- 20% is paid in Slovenia. On the territory of this state there are special economic zones, which must pay a 10% tax.

- 17.5% percent is CIT on basic income in Kazakhstan. This country has adopted a system of dividing income by categories. In addition to the main one, it includes: income from local sources (15%), profit from the sale of agricultural products (10%), earnings of non-residents with a permanent establishment (15%).

- 17% - in Singapore.

- 15% is paid in Germany and Cyprus. However, in addition to the amount of corporate tax, German entrepreneurs will have to pay a solidarity surcharge of 5.5%. In Cyprus, a 15% rate is accepted for dividends, and the base rate is 10%. The same 10% is taken from interest profits.

- 10% is the rate in Bulgaria. It is reduced for enterprises that create jobs in regions with a difficult economic situation, as well as for citizens with disabilities. Enterprises producing agricultural goods also enjoy benefits when paying CIT.

CIT is taken from the company's total income minus production expenses. Taxpayers are considered to be both residents and non-residents of the countries discussed above.

A resident is a company that has the status of a legal entity. Registration and the presence of a permanent legal address in the country of doing business allows one to be considered as such. A non-resident is a company that conducts business activities through a representative office or branch.

Changes 2020–2021 on transport tax for legal entities

In recent years, the following changes have been made to the procedure for paying transport tax:

- Starting from 2021, the procedure and terms for paying advances on it will change.

- Starting from 2021, as we said above, tax declaration has been cancelled, and tax authorities must send companies a message about the tax amount. In this regard, companies have an obligation to inform inspectors about vehicles for which such a report has not been received. Failure to send messages will result in a fine. In addition, due to the cancellation of declarations, legal entities will need to submit applications for benefits to the tax authorities.

Previously:

- In 2021, the list of expensive cars was clarified. Cars are regrouped depending on year of manufacture and price.

- The differentiation of the increasing coefficient for passenger cars costing from 3 to 5 million rubles has been cancelled. As of August 3, 2018, changes to clause 2 of Article 362 of the Tax Code of the Russian Federation came into force, which established a coefficient of 1.1% for all cars in this price category. Let us recall earlier that the coefficient value depended on the year of manufacture of the car: less than 12 months ago, the coefficient was equal to 1.5%, from 1 to 2 years - 1.3%, from 2 to 3 years - 1.1%.

- The procedure for calculating the ownership coefficient in the reporting (tax) period has been clarified, according to which this coefficient upon receipt (disposal) of a vehicle in this period is determined as the ratio of the number of full months of ownership to the total number of months in the corresponding period. The full month is taken to be the month in which the vehicle was purchased before the 15th or was disposed of after the 15th (clause 3 of Article 362 of the Tax Code of the Russian Federation).

- Rules have been established that the list of expensive cars is applicable only to the period in which it was posted on the website of the Ministry of Industry and Trade before March 1 (clause 2 of Article 362 of the Tax Code of the Russian Federation), i.e., with a change in this list, the tax for previous years cannot be recalculated need to.

- Regional laws periodically adjust transport tax rates.

Read about what rates the regions apply in this article.

- Other changes.

Find out how organizations can check and pay transport tax from January 1, 2021 from the Ready-made solution from ConsultantPlus.

Deadline for payment of transport tax for legal entities

From 2021, the deadline for payment of transport tax by legal entities is clearly stated in the Tax Code of the Russian Federation. This is March 1 of the year following the expired tax period. The deadline for paying advance payments (from advances for 2021) is no later than the last day of the month following the expired reporting period (clause 1 of Article 363 of the Tax Code of the Russian Federation).

Previously, there was no indication of specific payment dates in the code. And the answer to this question had to be sought in regional legislation: regional authorities were given the right to independently determine the payment deadline for transport tax and advances. However, the deadline for paying tax at the end of the year could not be set earlier than February 1 of the year following the reporting year (clause 1 of Article 362 of the Tax Code of the Russian Federation).

The amount of the quarterly advance payment is ¼ of the tax calculated for the year (clause 2.1 of Article 362 of the Tax Code of the Russian Federation). The amount of transport tax payable at the end of the current tax period is determined as the difference between the amount indicated in the tax return and the total value of previously paid advances (paragraph 2, paragraph 2, article 362 of the Tax Code of the Russian Federation).

Establishing payment of advance payments for regions, as before, is not mandatory (clause 3 of Article 360 of the Tax Code of the Russian Federation). If advances are not established, then legal entities must pay the entire tax amount at once in the full amount accrued for the year, within the period established by regional law.

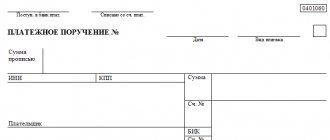

The procedure for preparing a payment invoice for payment of transport tax, including a sample of how to fill it out, is given in the Ready-made solution from ConsultantPlus.

Taxation of legal entities

We already know that a legal entity

is an organization, firm, company registered in accordance with the procedure established by law, which has separate property in ownership, economic management or operational management and is liable for its obligations with this property, can acquire and exercise property and personal non-property rights in its own name, bear responsibilities, be plaintiff and defendant in court.

All legal entities have tax obligations to the state.

Taxes from legal entities are levied on the basis of the Tax Code of the Russian Federation and a number of laws.

Value added tax (VAT) is of great importance in the taxation of legal entities

It is charged at all stages of production from the difference between the cost of goods, works and services sold and the cost of material costs for their production and circulation.

The object of VAT is the turnover of sales of goods, works and services.

For example. 1000 rubles were spent on the production of one iron; the iron was sold to the retail chain at a price of 2500 rubles. Subtracting the first digit from the last digit, we obtain the amount on which VAT must be charged. Naturally, not one, but several hundred irons were released into the trade. By multiplying 1,500 rubles by irons, we determine the amount on which the company will have to pay VAT.

In accordance with Russian tax legislation, VAT is paid by all organizations, regardless of their form of ownership, that have the status of a legal entity; enterprises with foreign investment; private enterprises; branches, departments and other separate divisions of enterprises located on the territory of the Russian Federation; international associations and foreign legal entities carrying out production and other commercial activities in our country.

The maximum VAT rate is 20%. A preferential rate of 10% is applied to the sale of a number of food and children's products, textbooks and books, and medical goods. A zero VAT rate applies to export goods, as well as goods placed under the free customs zone procedure. It also applies to goods, works and services sold for official use by international organizations in Russia.

Another type of tax on legal entities is excise taxes.

These are taxes included in the price of goods and services and paid by buyers and clients. In accordance with the law, not all goods are subject to excise taxes, but those that bring high profits and are intended for the population. These are, in particular, ethyl alcohol, alcohol and tobacco products, cars and motorcycles, gasoline, diesel fuel and motor oils.

The list of these goods is constantly updated in by-laws. With the help of excise taxes, the state regulates supply and demand and thus ensures the efficiency of replenishing the state budget.

It is appropriate to recall that VAT and excise taxes are indirect taxes.

In contrast,

the income tax

is direct , one of the most important in our country, levied in accordance with the Tax Code. Its size entirely depends on the final result of the enterprises’ activities.

Object of taxation

Income tax is the gross profit of an enterprise, measured by the difference between costs and income received.

The amount of income tax is determined as the product of the tax base and the tax rate.

The tax base

- this is a cost, physical or other characteristic of the object of taxation.

Tax rate

— the amount of tax charges per unit of measurement of the tax base.

In 2021, companies must pay income tax of 20%. Moreover, this percentage is distributed among budgets:

· at rates to the federal budget – 3%;

· at rates to the regional budget – 17%.

Let's try to calculate the income tax for Alpha LLC.

Alpha LLC operates in St. Petersburg. The regional income tax rate is 17%.

The organization's income in the first quarter amounted to 1,400,000 rubles, and expenses - 2,000,000 rubles, which means that Alpha LLC received a loss. Its size was 600,000 rubles. The tax base turned out to be 0.

Income in the second quarter amounted to 3,500,000 rubles, and expenses – 2,000,000 rubles.

In total, for 6 months, the accountant of Alpha LLC determined the following figures:

– income – 4,900,000 rubles;

– expenses – 4,000,000 rubles.

The tax base for 6 months of work is 900,000 rubles.

Payments to the regional and federal budgets were calculated as follows:

– to the federal budget – 27,000 rubles. (RUB 900,000 × 3%);

– to the regional budget – 153,000 rubles. (RUB 900,000 × 17%).

Also, if there is movable or immovable property, legal entities pay the organization’s property tax

- this is a tax on real estate (including property transferred for temporary possession, use, disposal or trust management contributed to joint activities).

The interest rate on such a tax is established by the laws of the constituent entities of the Russian Federation and cannot exceed 2.2% of the value of the property.

Legal entities pay a number of taxes only if there is a corresponding object of taxation. For example, if an organization owns transport, it will pay a transport tax; if it owns land, it will pay a land tax; if it extracts minerals, it will pay a mineral extraction tax; if it uses water resources, it will pay a water tax, and so on.

In addition, legal entities can take advantage of special tax regimes when paying taxes.

For example, legal entities starting their professional commercial activities can choose one of two tax system options - general or simplified.

General taxation system –

This is a system in which taxpayers pay taxes to the maximum and must maintain full accounting and tax records.

Simplified taxation system

– this is one of the tax regimes, which implies a special procedure for paying taxes and is aimed at representatives of small and medium-sized businesses.

To use such a system, you must meet certain conditions:

· less than 100 employees on staff;

· income should not exceed 150,000,000 rubles;

· residual value must be less than 150,000,000 rubles.

There are also separate conditions for organizations:

· the share of participation of other organizations in it cannot exceed 25%;

· the use of a simplified taxation system for organizations that have branches is prohibited;

· an organization has the right to switch to a simplified taxation system if, based on the results of nine months of the year in which the organization submits a notice of transition, its income does not exceed 112,500,000 rubles.

With a simplified taxation system, tax rates depend on the object of taxation chosen by the entrepreneur or organization.

If the object of taxation is “income”, the rate is 6%, if the object of taxation is “income minus expenses”, the rate is 15%.

In relation to certain types of business activities, such as:

· retail trade;

· public catering;

· household and veterinary services;

· repair, maintenance and washing services for motor vehicles;

· distribution and (or) placement of advertising;

· services for the temporary use of trading places and land plots;

· temporary accommodation and accommodation services;

· services for the transportation of passengers and goods by motor transport;

· parking services.

It is possible to pay a single tax on imputed income for certain types of activities. The peculiarity of this taxation system is that the tax is levied on imputed income, that is, on expected income, and not on actual income. This means that the real volume of cash receipts does not affect the amount of payment to the budget.

This is both a benefit and a disadvantage. On the one hand, you can earn much more than the expected amount and pay minimal tax. On the other hand, the payment amount will remain the same, even if the business does not generate income or even turns out to be unprofitable.

To transition to this simplified taxation system, legal entities also need to fulfill a number of conditions:

· the share of participation of other legal entities must be less than 25%;

· less than 100 employees on staff;

· this tax regime was introduced on the territory of the municipality;

· the activity is not carried out within the framework of a simple partnership agreement and a trust agreement;

· the type of activity being carried out is mentioned in the local regulatory legal act;

· the taxpayer is not an educational, health and social security institution in relation to the provision of public catering services;

· the taxpayer does not belong to the “largest” category;

· leasing services for gas and gas filling stations are not provided.

The tax amount is 15% of temporary income.

Producers of agricultural products under a simplified taxation system have the right to pay a single agricultural tax.

To switch to such a taxation system, income from agricultural activities must exceed 70%. Payers of this tax need to pay 6% of their profits to the budget.

Some organizations and enterprises receive tax breaks.

This is a statutory full or partial tax exemption.

We can say that tax incentives are a system of tax discounts that are provided to individuals and legal entities to stimulate business development or reduce the tax burden.

The Tax Code does not contain a list and classification of tax benefits, but it can be said that the provision of tax benefits consists of providing a tax credit and tax exemption.

Tax credit

- this is the ability of an organization to reduce its payments for income tax, regional and local taxes during a certain period with the subsequent payment of a loan and interest on it.

Tax exemptions include the following types of tax benefits.

Tax holidays

- This is the exemption of the taxpayer from paying tax for a certain period.

Tax amnesty

- this is the repayment by the taxpayer of overdue debts without the application of sanctions to him for delay.

Full tax exemption

may be provided to some categories for a certain period or indefinitely.

Seizure

- this is an exception from the tax base of its parts, for example, the profits of religious organizations (associations) from religious activities and the sale of items necessary for the performance of worship (for example, candles, icons, temple decorations, and so on) are not subject to taxation.

Reduced tax rate

allows certain categories of taxpayers to pay tax at interest rates lower than generally established rates. For some taxes, preferential rates can be reduced to 0%.

You can learn in detail about taxes on legal entities and preferential tax regimes on the website of the Federal Tax Service, which is already familiar to you, but now let’s try to answer some questions.

1. How is the concept of “legal entity” defined in tax law?

2. What laws determine the procedure for collecting taxes from legal entities?

3. What is value added tax (VAT)?

4. What are excise taxes?

5. What is income tax?

6. What are tax benefits?

7. What taxes - direct or indirect - are VAT, excise taxes and income tax?

Results

Legal entities - owners of vehicles registered with the registration authorities must pay transport tax. It is not paid only in relation to transport, which is mentioned in paragraph 2 of Art. 358 Tax Code of the Russian Federation. Taxpayers who are legal entities must calculate the tax amount independently, but they no longer need to submit a tax return.

Organizations must pay transport tax in advance, unless another method of paying the tax is specified in regional legislation. The deadlines for paying advances and taxes are new from 2021.

Sources:

- Tax Code of the Russian Federation

- Order of the Federal Tax Service dated November 26, 2018 No. ММВ-7-21/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.