How to pay tax for a third party

In order to pay tax for a third party, the following rules must be observed:

- Any other person can pay tax on behalf of the taxpayer. There are no restrictions on who the third party should be in this situation. Such a payer can be either a legal entity or an individual. This person may have some direct relationship with the taxpayer, or be a third party.

- Paying tax in this way applies not only to tax payments, but also to insurance premiums (including penalties and fines on them). The only exception is insurance premiums for insurance against accidents and occupational diseases. An organization or entrepreneur can only pay for them independently.

- You cannot pay tax on any specific transaction for the sale of goods or services. For example, when purchasing goods from a seller, the buyer does not have the right to pay income tax on a specific transaction.

- The obligation to pay tax will be considered fulfilled at the time of submission to the bank of an order to transfer funds to the budget from the account of a third party, if it pays the tax for the taxpayer.

- The obligation to pay tax will be recognized as unfulfilled if the person who presented the order to the bank withdraws the order, or if the bank returns the unfulfilled order to such person, for example, in case of errors or insufficient funds in the account (

Who pays for what?

It turned out that not all payments and contributions to third parties can be paid for the main payer. In fact, this may be retained for all those taxes that are in the department of the Federal Tax Service. These include: VAT, personal income tax, income tax, water tax, mining tax, state duties, unified agricultural tax, unified tax on the simplified tax system, tax on personal personal income tax, UTII, insurance premiums, corporate property tax, gambling business tax, transport tax , Land tax, Personal property tax, Trade tax. It seems we haven't missed anyone.

Please note that “injury” contributions are excluded from this list. Their payment by third parties is not yet possible due to the fact that they are under the jurisdiction of the FSS. As for other insurance premiums, payments for them are already accepted by the Federal Tax Service, therefore, you can pay your friend for them if you follow all the rules that we indicated above.

In fact, payments from third parties are a fairly variable method of settlement with the Federal Tax Service. For our part, we can offer several possible situations for clarity in order to understand how these rules can work in practice:

- For example, an organization can pay taxes and fees for another organization, individual entrepreneur or individual;

- Or an individual entrepreneur can transfer taxes and fees for another individual entrepreneur, organization or individual;

- An individual also has the right to pay taxes and fees for another individual, organization or individual entrepreneur.

In other words, the Federal Tax Service gives us more freedom in this matter and this, admittedly, should be convenient. Because, firstly, no one exempts us from tax payments anyway, and, secondly, it gives us the opportunity to help “our neighbor” or for him to help you when there is a direct need for it. However, with all this, a completely logical question arises: “Can a person who made a payment for another organization demand compensation from it?” It turned out that she does not have such a right, because... it is assumed that such “charity” was a completely free service. There is another one: “Is it possible to clarify the payment for compulsory pension insurance if the Pension Fund has managed to record the amounts paid in the personal accounts of the insured?” Again, you can't. If the amounts have been taken into account, then consider that your train left a long time ago and no one will give you any information.

How to fill out a payment order to pay tax for a third party

In order for the tax payment to be executed correctly in relation to the taxpayer for whom it is paid, it is important that the payment order be drawn up in accordance with the new rules for indicating information (Rule No. 58n dated 04/05/2017).

Important! Even if the tax was paid by a third party, the taxpayer needs to have a copy of the order confirming payment to eliminate possible tax questions.

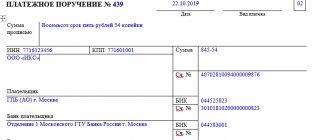

The main difficulties when filling out a payment slip for tax transfers for another person may arise in relation to the payer’s details. Let's look at the main ones:

| Field | What to include | Other Features |

| 60 “TIN of the payer” | INN of the taxpayer, according to which the obligation to pay tax (insurance contributions) is fulfilled | If tax is paid for an individual without a TIN, then “0” is entered, and a unique accrual identifier (UIN) should be entered in the “Code” field. |

| 120 “Payer checkpoint” | Checkpoint of the taxpayer, according to which the obligation to pay tax (insurance contributions) is fulfilled | If the tax is paid for an individual, then “0” is entered, |

| 8 "Payer" | Information about the person making the payment | If a legal entity pays, then the name of the organization that fulfills the taxpayer’s tax obligations is indicated; If an individual entrepreneur or individual pays, then his full name is indicated; |

| 24 “Purpose of payment” | Indicate the TIN and KPP of the person making the payment | You must indicate the TIN and KPP first in the “Purpose of payment” field, while the values of the TIN and KPP are separated by “//”. Then information about the taxpayer for whom the obligation to pay tax is fulfilled is indicated: for individual entrepreneurs - full name, and in brackets “Individual Entrepreneur”, for individuals - full name and address |

| 101 “Payer status” | The status of the one whose tax liability is fulfilled. | Legal entity – “01” IP – “09” Individual – “13” |

Important! If an error was made when paying tax for a third party, which does not entail cancellation of the payment, then it can be clarified by writing a corresponding application to the tax authority. But the application must be submitted by the taxpayer himself, and not by the person who actually made the payment for it.

In what cases is it issued?

At present, the contradiction between the norms of legislation and the principled position of the tax authorities, which previously prevented the making of non-cash payments for third parties, has already been eliminated.

This possibility is no longer disputed by the Federal Tax Service.

The main condition is that payment made for a third party must be correctly documented in the payment order and recognized by all entities participating in the relevant transaction.

In order to pay off tax obligations for a third party, a payment order is issued, and from July 1, 2017, an organization or other person is required to enter into an agency agreement, the form of which is approved by the Federal Tax Service.

Thus, any business entities (organizations, individual entrepreneurs) can legally repay (transfer) a variety of payments for each other:

- tax obligations;

- leasing payments;

- fines, penalties;

- debts;

- duties;

- other payments.

The Civil Code of the Russian Federation (paragraph one of Article 313) provides for the possibility (option) of fulfillment by a third party of debt obligations, if legislation, legal acts, terms of the agreement or the very essence of such requirements do not establish the obligation of the debtor to independently (personally) repay the corresponding debt.

Consequently, the creditor does not have the right to refuse to accept a fulfilled obligation repaid by a third-party entity for the debtor, if the fulfillment of the debt claim is entrusted to this third-party entity by the debtor himself.

If the debtor did not assign the fulfillment of this obligation to a third party, the creditor has an obligation to accept the performance offered by the third party for the debtor in the following typical situations:

- the debtor is late in repaying a financial obligation (for example, a debt);

- the third party who made the payment to fulfill the obligation faces the threat of losing the right to the debtor’s assets if these assets become the object of recovery in enforcement proceedings.

In addition, starting from 2021, the norms of the Tax Code of the Russian Federation (articles , ) provide for the possibility of repaying debt obligations of a business entity by third parties if there are insufficient funds in the bank accounts of the debtor organization.

Now the head of an economic entity, a third-party organization, or any private entrepreneur can make such payments on the basis of payment orders.

Before the corresponding changes were made to these articles, the obligation to transfer taxes, penalties, state duties and other fees was assigned directly to tax agents.

Purpose of payment

In order for payment to be made for a third party, the debtor sends a corresponding letter to the payer with a request for repayment (payment) of a specific obligation.

For example, the essence of such a letter may be that the Alpha company (debtor) asks a certain payer to transfer a specific amount of money to the Beta company (creditor) for some goods (for example, building materials) under a specific supply agreement (number/date).

The letter may also state that Alpha Company and Beta Company have entered into a loan agreement (number/date) for this purpose.

Accordingly, the purpose of payment in the payment order in this case can be indicated as follows: payment for a consignment of construction materials under the supply agreement (number/date) for the Alpha company to repay obligations under the loan agreement (number/date) and under the assignment agreement (number/ date), including VAT (20%).

How to fill out a payment form?

A special letter from the Federal Tax Service of the Russian Federation dated March 17, 2017 explains the procedure for implementing paragraph one of Article 45, prescribed in the Tax Code of the Russian Federation.

We are talking about the rules governing the preparation of a payment order to transfer money from a bank account to the budget for third parties (third parties).

Tax service specialists focus special attention on the following details of such a payment, which are mandatory:

- In the corresponding fields of the payment order, the TIN and KPP of the particular payer (debtor) whose obligation to make the necessary payments to the budget is fulfilled by drawing up this order are indicated.

- In the order field, where the payer is indicated, information about the entity actually making this payment from its bank account is entered (name of the organization, full name of the individual).

- In the field of the payment order, which reflects the purpose of the payment being made, the TIN and KPP of the entity that actually made the transfer (if an individual - only the TIN), as well as information about the payer-debtor, whose obligation to pay the debt is being fulfilled (name of the legal entity, full name of the individual) are written down. . Information about the payer-debtor is highlighted with the sign //. Details are written before other additional information, often reflected in the same field.

- In the order field where the payer status is filled in, the status of the entity (debtor) whose obligation to transfer money is fulfilled by this payment order is entered (01 - legal entity, 13 - individual, 09 - individual entrepreneur, 14 - individual entrepreneur making payments to citizens).

Detailed instructions for filling out a payment order - link.

Download a sample form when paying taxes

payment order when paying for a third party – word.

Agreement between the taxpayer and a third party

The legislation does not establish strict requirements on exactly how the relationship between the taxpayer and the person paying the tax for him should be formalized. However, an agreement or other documentary evidence between the two persons in this situation must be drawn up.

The type of agreement can be one of the following: (click to expand)

- If the third party is a debtor of the taxpayer, then a contract of agency or an agreement to transfer tax for the taxpayer is concluded. One option may also be to write a letter to the debtor asking him to pay the tax to pay off the debt;

- If there are no contractual relations between two persons, then a loan agreement is concluded for the amount of the tax. The agreement can be either interest-free or interest-bearing;

- If the third party is the founder, then the following types of agreement can be concluded: loan, gift or interest-free targeted financing.

How to properly arrange payment of a debt by a third party

What does payment of a company's debt by a third party mean?

This means that the company's debt is repaid by another company. As a rule, she herself is a debtor of the enterprise, and therefore the funds paid to her go towards repaying her debt. In what cases is it relevant to pay a debt by a third party? Almost every company that has been operating for some time is both a creditor and a debtor. That is, it both lends funds and gives them to third-party companies. All this makes it possible to pay off your debt to one organization with the funds of another. This will be relevant if the company currently does not have the required amount of funds. This can be a convenient way for a third party paying off someone else's loans to pay off their debt.

Payment Features

The payer retains the original letter containing the request to make a payment for a third party. The purpose of the payment is indicated in the payment order. To avoid conflict situations, a copy of the letter is kept by the creditor and the company that ordered the transfer of money.

When a third party makes a payment, it does not become one of the parties to the contract. Responsibility for the implementation of the agreement remains with the parties who entered into it. For example, when a company, which the debtor asked to fulfill its obligation to the creditor, did not transfer funds to the creditor, then the debtor remains responsible for the failure to fulfill obligations.

Payment for a third party is not prohibited by law. The lender accepts payment if all the documents described above are presented.

Payment in foreign currency

Similar articles

- Reason for payment 106 explanation

- How to fill out the payment purpose in a payment order?

- Purpose of payment for business needs

- Purpose of payment under the assignment agreement

- Loan repayment purpose of payment

Third party payment procedure

The procedure for one company to pay for another is quite common. Tax legislation also allows for the payment of taxes for another company (Article 45 of the Tax Code of the Russian Federation), therefore, in practice, entrepreneurs everywhere use this payment method. This is especially true for urgent payments, when payments must be made before a certain date, and the debtor company has problems with its current account (seized or blocked). The reason may also be a lack of funds at a particular moment in the current account. The only obstacle to this kind of mutual settlements is if the contract or law governing this type of contractual relationship directly states a ban on payment of obligations by a third party.

The scheme for payment by a third party for the buyer (a sample letter is given below) is as follows:

The seller (company A) issues an invoice to the buyer (company B) for payment for goods, services, etc. Company B writes a letter to a third company (B), which has a debt to company B, with a request to pay for it to its creditor (company A) and thereby repay part of its own debt to B. The payer in the framework of such mutual settlements can be any debtor counterparty , with which firm B has any contractual relationship.

The payer (company B), when transferring to company A, must indicate in the payment order that this payment is made for company B. To confirm the payment to company B, it is necessary to keep a letter from company B requesting payment and the payment order.