The state cannot exist without such a function as collecting taxes. One of the main taxes that significantly replenishes the budget of our country is the personal income tax (NDFL).

Personal income tax payers are:

- individuals who are tax residents of the Russian Federation;

- individuals who are not tax residents of the Russian Federation, but receive income from sources in the Russian Federation (clause 1 of Article 207 of the Tax Code of the Russian Federation).

For tax purposes, individuals mean citizens of the Russian Federation, foreign citizens and stateless persons (clause 2 of article 11 of the Tax Code of the Russian Federation).

PROCEDURE FOR REFUNDING PIT FROM THE BUDGET BY NON-RESIDENTS OF THE RF WORKING ON THE BASIS OF A PATENT

The obligation to pay personal income tax does not depend on the legal status of an individual and is conditioned only by the fact of receiving income in the territory of the Russian Federation or abroad. That is, factors such as the presence (absence) of citizenship, place of birth or place of residence, as well as the grounds for stay or residence on the territory of the Russian Federation are not determining indicators when calculating personal income tax.

Thus, a citizen of the Russian Federation may be a non-resident and, conversely, a resident of the Russian Federation may be a foreigner.

According to paragraph 3 of Art. 224 of the Tax Code of the Russian Federation, a tax rate of 30% is established for most income received by individuals who are not residents of the Russian Federation. In most cases, the income of residents of the Russian Federation is taxed at a personal income tax rate of 13%.

A tax rate of 30% is established for all income received by persons who are not tax residents of the Russian Federation, with the exception of income:

- from equity participation in the activities of Russian organizations, in respect of which the tax rate is 15%;

- from foreign citizens carrying out labor activities specified in Art. 227.1 of the Tax Code of the Russian Federation (for hire from individuals, in respect of whom the tax rate is set at 13%;

- from carrying out labor activities as a highly qualified specialist in accordance with Federal Law dated July 25, 2002 N 115-FZ “On the legal status of foreign citizens in the Russian Federation”, in respect of which the tax rate is 13%;

- from the implementation of labor activities by participants in the State program to assist the voluntary resettlement of compatriots living abroad to the Russian Federation, approved by Decree of the President of the Russian Federation of June 22, 2006 N 637, as well as members of their families who jointly moved to a permanent place of residence in the Russian Federation, in respect of which the tax the rate is set at 13%;

- from the performance of labor duties by crew members of ships sailing under the State Flag of the Russian Federation, for which the tax rate is 13%;

- from carrying out labor activities by foreign citizens or stateless persons, recognized refugees or who have received temporary asylum on the territory of the Russian Federation in accordance with the Federal Law “On Refugees”, in respect of which the tax rate is set at 13% (the norm was put into effect by the Federal Law of 04.10. 2014 N 285-F from October 6, 2014 and applies to legal relations arising from January 1, 2014).

Please note that tax residents of the Russian Federation, when determining the size of the tax base for personal income tax, have the right to take advantage of various tax deductions, the types and procedure for the provision of which are regulated by Art. 218-221 Tax Code of the Russian Federation. Non-residents of the Russian Federation do not have rights to such deductions (clause 4 of Article 210 of the Tax Code of the Russian Federation).

PROCEDURE FOR REFUNDING NDFL TO A TAXPAYER – A FOREIGN INDIVIDUALS IN CONNECTION WITH THEIR ACQUISITION OF RESIDENT STATUS OF THE RUSSIAN FEDERATION

Determination of tax resident status

Tax residents are individuals who are actually in Russia for at least 183 calendar days over the next 12 consecutive months. The period of stay of an individual in Russia is not interrupted by periods of his departure outside the Russian Federation for short-term (less than six months) treatment or training (see also letter of the Ministry of Finance of Russia dated October 21, 2013 N 03-04-05/43779), and since 2014 — also for the performance of labor or other duties related to the performance of work (provision of services) in offshore hydrocarbon fields.

When determining the tax base for personal income tax, all income of the taxpayer received both in cash and in kind is taken into account (Clause 1 of Article 210 of the Tax Code of the Russian Federation).

Please note that responsibility for the correct determination of the tax status of an employee, as well as the calculation and payment of tax in accordance with his tax status, lies with the organization. Therefore, despite the fact that Article 65 of the Labor Code of the Russian Federation contains an exhaustive list of documents that can be requested from an employee when hiring him, in order to accurately determine his tax status, the tax agent has the right to request the relevant documents or copies thereof from an individual. If an individual does not submit the requested documents, the tax agent has the right to apply to the income paid the tax rate established for non-residents - 30% (letter of the Ministry of Finance of Russia dated August 12, 2013 N 03-04-06/32676).

The list of documents that confirm the tax status of an individual is not established by law. In practice, they can be certificates from the place of work, issued on the basis of information from the work time sheet, copies of a passport with marks from border control authorities about crossing the border, receipts for hotel accommodation and other documents on the basis of which it is possible to establish the actual presence of an individual in RF (see, for example, Resolution of the Federal Arbitration Court of the North-Western District of June 30, 2014 N F07-8864/12 in case N A13-18291/2011).

Please note that the period of 183 calendar days is not interrupted by the time of departure from the Russian Federation for short-term training or treatment, and since 2014 - also for the performance of labor or other duties related to the performance of work (provision of services) in offshore hydrocarbon fields. There is no list of restrictions by type of educational institutions, academic disciplines, medical institutions, diseases, as well as by the list of foreign countries, the main criterion is the short-term absence - a period of less than 6 months (Letter of the Department of Tax and Customs Tariff Policy of the Ministry of Finance of the Russian Federation dated October 8, 2012 . N 03-04-05/6-1155).

PROCEDURE FOR CALCULATING PIT FROM THE WAGES OF FOREIGN WORKERS

Features of the use of tax deductions in the Russian Federation

The legislation of the Russian Federation regulates the use of six types of tax deductions:

- Professional deduction - is provided for by the specifics of professional activities carried out by entities working under copyright and civil law agreements, self-employed persons, individual entrepreneurs, representatives of the bar and notaries.

- Tax compensations due to the turnover of a wide variety of financial instruments (for example, securities).

- Property deduction - used when taxing income from the sale of any property (for example, when selling an apartment).

- Investment tax benefits associated with the specifics of investing money in any profitable, useful projects.

- Social deduction , which applies to income related to the social security of certain segments of the population (income spent on treatment, study, other needs, as well as donations, pension insurance).

- A routine government refund of a specific portion of previously paid taxes. The amount of such a deduction will depend on the taxpayer’s belonging to one or another category of recipients of this benefit.

The basis for granting any of the above benefits will be the subject’s compliance with two requirements simultaneously:

- he must be a payer of ordinary income tax at the standard rate of 13%;

- he must have legal Russian resident status.

Thus, if an individual does not meet these two requirements at the same time, he is automatically deprived of the right to apply for any of the tax deductions listed above. It turns out that non-residents cannot legally claim compensation for the tax paid provided for by this benefit. According to the law, a tax deduction for a non-resident of the Russian Federation is not possible.

When the rate changes...

To determine the personal income tax rate to be applied, the tax status of the employee is determined by the tax agent for each date of payment of income based on the actual time spent in the Russian Federation.

When determining the tax status of an employee, it is necessary to take into account the 12-month period determined on the date he received income, and this does not have to be the calendar year from January 1 to December 31, it can be any period equal to 12 months, for example from July 12, 2014 to July 12, 2015.

The tax status of an individual may change repeatedly depending on the time of his stay in the Russian Federation and abroad. If an individual becomes a resident of the Russian Federation, then from the moment he acquires resident status, his income must be taxed at a rate of 13% and vice versa, if an individual loses his resident status, then from the moment he loses his status, the income he receives is taxed at a rate of 30% ( Article 224 of the Tax Code of the Russian Federation).

In the event that the tax status has changed from “non-resident” to “resident”, tax legislation provides for the return of personal income tax to the taxpayer in connection with recalculation based on the results of the tax period (clause 1.1 of Article 231 of the Tax Code of the Russian Federation). The refund of the overpayment amount is made by the tax authority with which the taxpayer was registered at the place of residence (place of stay), upon filing a tax return at the end of the tax period, as well as documents (see above) confirming the status of a tax resident of the Russian Federation in this tax period . The procedure for returning the overpayment amount is established by Article 78 of the Tax Code of the Russian Federation.

Previously, in 2011, on the basis of explanatory letters from the Ministry of Finance of Russia, tax recalculation at a rate of 13% was carried out only by the tax authority and only when filing a tax return 3-NDFL complete with documents confirming the status of a resident of the Russian Federation, and the tax authority also returned the overpaid tax. For example, if personal income tax was withheld from a non-resident employee from the beginning of the year at a rate of 30%, and in June the individual received resident status, then the tax agent must then withhold tax at a rate of 13%, but there was no need to recalculate the tax for the period from January to June. This was done by the tax authority on the basis of an individual’s declaration (letter of the Department of Tax and Customs Tariff Policy of the Ministry of Finance of the Russian Federation dated May 16, 2011 N 03-04-06/6-108).

Later, the Russian Ministry of Finance changed its point of view and, along with mentioning the obligation of the tax authorities to return personal income tax, began to say that if during the tax period an employee acquired the status of a tax resident and this status can no longer change (that is, the individual is in RF more than 183 days in the current tax period), all amounts of remuneration received by an employee from the employer for the performance of work duties from the beginning of the calendar year are subject to taxation at a rate of 13%.

In this case, tax agents should be guided by the provisions of paragraph 3 of Art. 226 of the Tax Code of the Russian Federation, according to which personal income tax is calculated on an accrual basis from the beginning of the year based on the results of each month. Thus, starting from the month in which the number of days of an employee’s stay in the Russian Federation in the current tax period exceeded 183 days, the amounts of personal income tax withheld by the tax agent from his income before he received tax resident status at a rate of 30% are subject to offset by the tax agent when determining the tax base on an accrual basis for all amounts of employee income. In fact, this means that personal income tax is recalculated for the entire period from the beginning of the year at a rate of 13% by the tax agent (Letter of the Department of Tax and Customs Tariff Policy of the Ministry of Finance of the Russian Federation dated April 5, 2012 N 03-04-05/6-443 “On the return of amounts withheld personal income tax in connection with a change in the tax status of an individual").

If, after the offset, it turns out that the amounts of personal income tax withheld from the employee’s income at a rate of 30% were not fully offset at the end of the tax period, and there remains an amount of personal income tax that is subject to refund, only the tax authority can return the amount of overpaid personal income tax for the ended tax period to the taxpayer . To do this, the employee must independently submit a declaration in form 3-NDFL to the territorial body of the Federal Tax Service. The procedure for returning the overpayment amount is established by Article 78 of the Tax Code of the Russian Federation.

At the request of the taxpayer, the amount of overpaid tax (penalties, fines) can be returned to him.

Personal income tax rate for foreign citizens

The personal income tax rate will vary depending on the type of income, status and residence. Residence status is determined by the time spent on the territory of the Russian Federation. Thus, foreigners who have stayed in Russia for less than 183 days (calendar) within one year are non-residents. And persons with a special status are recognized as:

- refugees;

- high-class specialists;

- foreigners holding a patent;

- residents of the EAEU countries.

Read also: Immigration to Italy from Russia

| Foreign citizen status | Personal income tax rate (%) | ||

| Income from employment | Other types of income, with the exception of winnings and dividends, which are taxed at a higher rate | Profits from participation in a joint stock company | |

| Special status/resident of the Russian Federation | 13 | 13 | 13 |

| Special status/non-resident of the Russian Federation | 13 | 30 | 15 |

| No special status/resident of the Russian Federation | 13 | 13 | 13 |

| No special status/non-resident of the Russian Federation | 30 | 30 | 15 |

Algorithm for returning amounts of overpaid personal income tax:

1) filing an application - the taxpayer submits an application to the tax authority at the place of his registration in writing or in electronic form with an enhanced qualified electronic signature via telecommunication channels (clause 4 of Article 78 of the Tax Code of the Russian Federation).

The application form for the refund of the amount of overpaid (collected) tax (fee, penalty, fine) was approved by order of the Federal Tax Service dated March 3, 2015 N ММВ-7-8/ [email protected] (Appendix No. 8).

2) verification of compliance with conditions - the tax authority verifies compliance with mandatory conditions:

- registration of the taxpayer with this tax authority;

- absence of debt for other taxes of the corresponding type (clause 6 of Article 78 of the Tax Code of the Russian Federation) and others.

3) decision-making - based on the taxpayer’s application, the tax authority makes a decision:

- about offset or return of the overpaid amount;

- about refusal to carry out offset (refund);

The forms of the decision on offset, decision on refund, as well as messages about the decision on offset (refund) taken by the tax authority were approved by the same order of the Federal Tax Service dated March 3, 2015 N ММВ-7-8/ [email protected]

4) communication of the decision - within 5 working days from the date of the relevant decision, the taxpayer is sent a message (Appendix No. 3 to Order No. ММВ-7-8 / [email protected] ;), as well as a copy of the tax authority’s decision on the refund.

The refund of the amount of overpaid tax is carried out by the territorial body of the Federal Treasury (TOFK) on instructions issued by the tax authority on the basis of the decision made.

Reduction of personal income tax by the amount of a patent for a foreign citizen

Taxes are withheld from foreigners in accordance with the law.

It is not possible to issue a recalculation and receive a refund in advance. This can only be done after the tax period, once a year. In 2021, the previously in force order has been maintained. A foreign worker can apply for a deduction in person by contacting the tax service. Or submit an application to your employer, who will prepare documentation for transmission to the tax authorities.

After receiving an application with a package of documents, a tax officer conducts an inspection with the participation of the migration service. A ten-day period has been established for verification.

Read also: Repatriation to Israel in 2021

A prerequisite for approval of an application for a personal income tax refund is the implementation of legal work activities. The foreign worker must have all the necessary work permits, supporting documents, as well as a formal employment contract with the employer.

If an employee has several jobs, he makes a tax refund once, through the main employer. When conducting an audit, the tax officer will definitely check whether applications for a specific person have been received from other places of work.

If an organization employs several foreign employees, the accounting department prepares a separate package of documents for each employee to reimburse the tax.

Reverse situation: from 13% to 30%

In practice, the situation may be the opposite, when the employee has lost his tax resident status. In this case, the tax agent is obliged to recalculate the tax at a rate of 30% and withhold it from the employee’s income. Amounts of tax not fully withheld are collected by the tax agent from an individual until these individuals fully repay the tax debt in the manner prescribed by Article 45 of the Tax Code of the Russian Federation. If the employee has already quit, then the tax agent must inform the tax authority in writing about the impossibility of withholding personal income tax and the amount of the taxpayer’s debt (clause 5 of Article 226 of the Tax Code of the Russian Federation). The obligation to pay the difference between the amount of tax calculated at a rate of 30% and actually withheld at a rate of 13% in this case must be fulfilled by the taxpayer himself.

For reference: when taxing the income (including wages) of a foreign worker, the provisions of international agreements between Russia and the country of which he is a citizen should be taken into account. They may provide for a special procedure for taxation of personal income, as well as social and pension insurance.

To eliminate double taxation of personal income tax, a taxpayer may need a certificate confirming the status of a tax resident of the Russian Federation. At the same time, in order for a tax agent to apply a tax rate of 13% in relation to income from employment, the taxpayer does not need to receive special confirmation from the Russian tax authority (Letter of the Federal Tax Service dated October 22, 2014 No. OA-3-17 / [email protected] " On the procedure for confirming the status of a foreign citizen as a tax resident of the Russian Federation").

How can a non-resident get a tax deduction?

Any tax deduction for a certain tax period is possible only in one case - in this tax period a non-resident had resident status. Of course, when planning to receive a deduction, it is necessary to foresee a temporary change in status in advance.

The tax status of the personal income tax payer (resident/non-resident) is determined based on the results of the past tax period, calculated by the calendar year. Therefore, if you want to receive a deduction in the coming year, you should foresee in advance the possibility of staying in Russia for at least 183 days from the beginning to the end of the year in which you plan to receive the deduction. This will allow you to acquire resident status, which means all the rights to tax deductions that are provided for such status. The same condition will need to be met in other tax periods if you intend to receive deductions in them as well.

Property deduction

A property deduction for a non-resident is not possible. But deduction is not an end in itself. It only allows you to save on taxes or return part of them paid. Therefore, perhaps an option will suit you that will not give you personally the opportunity to receive a deduction, but will allow you to achieve one of the specified goals.

So, if you have property in Russia that would allow you to claim a property deduction if you were a resident, you can consider the option of transferring it to another person who is a resident of the Russian Federation:

- Conclusion of a gift agreement . This will allow you to change the owner, that is, avoid paying property tax, and avoid paying personal income tax, since the gift does not provide for the receipt of income. In fact, you can even receive some kind of payment for the donated property. But it should be taken into account that in this way you put the transaction at risk of being considered sham (a formal donation covers the actual purchase and sale). In addition, the actual income received is actually income hidden from taxation. It cannot be declared, otherwise at least the tax authorities will become aware of the transaction (the real side of it).

- Conclusion of a purchase and sale agreement . For you, the effect will be the same as when donating property, only you will be able to legally receive and declare income. The downside is that you will have to pay tax on your income. The second party to the transaction, being a resident, in case of resale of the property will have to pay only 13%, and if he remains in the status of owner for 5 or more years - 0%. Of course, the property tax will be transferred to the buyer, but he will also acquire the full right to a property deduction, however, if all other conditions for receiving it are met.

As a rule, all such transactions are made between close relatives. For example, often citizens who live abroad for a long time give (most often) or sell real estate in Russia to their parents or children. If family relations are very good, nothing will prevent you from re-registering the property in your name in the future when you decide to return to Russia. To avoid imposing property tax obligations on your relatives, you can keep these expenses for yourself - of course, unofficially, by simply transferring the money to your relatives or paying the tax instead. There is little point in making a deal if relatives cannot receive a property deduction. In this situation there is no mutual benefit for the parties.

When buying an apartment

Based on Art. 220 of the Tax Code of the Russian Federation, residents of Russia have the right to receive a tax deduction when purchasing housing (apartments, houses, shares in them) in the amount of up to 2 million rubles from the price paid for them and another 3 million from interest on the mortgage if the purchase was made on credit. The tax deduction provides a personal income tax refund in the amount of 13% of the specified amounts.

According to paragraph 4 of Art. 210 of the Tax Code of the Russian Federation, for income on which tax is levied at other rates, a tax deduction under Art. 220 of the Tax Code of the Russian Federation does not apply.

Non-resident individuals pay tax at a rate of 30% of the income received (clause 3 of Article 224 of the Tax Code of the Russian Federation). Therefore, a non-resident cannot receive a personal income tax refund from the purchase of an apartment.

The Russian Ministry of Finance has repeatedly pointed out the prohibition of providing property tax deductions to tax non-residents of the Russian Federation (one of the last letters on this issue, No. 03-04-05/3043, was issued on January 21, 2021).

Procedure for returning personal income tax by a foreigner No. 5 (130) 2013

If during a calendar year a foreigner changes his status from non-resident to resident, he can return the over-withheld personal income tax.

A foreign worker acquires the status of a tax resident of the Russian Federation only if he stays in the Russian Federation for at least 183 calendar days over the next 12 consecutive months (Clause 2 of Article 207 of the Tax Code of the Russian Federation). Moreover, its status may change from month to month. This is due to the fact that the specified period of 12 months is not limited to the calendar year. It must be determined for each date of payment of income to the taxpayer (Letters of the Ministry of Finance of Russia dated July 14, 2011 No. 03-04-06/6-170, dated July 14, 2011 No. 03-04-06/6-169, dated May 25. 2011 No. 03-04-06/6-122, dated 05/19/2011 No. 03-04-06/6-117).

Therefore, each time you accrue income to a foreign worker, you should determine the applicable personal income tax rate. So, if on the date of accrual of payment the employee is a resident of the Russian Federation, the personal income tax rate will be 13%. Otherwise, a rate of 30% is applied (clauses 1, 3, Article 224 of the Tax Code of the Russian Federation).

The procedure for recalculation (recalculation) and withholding of personal income tax when changing the status of a foreign employee (a non-resident has become a resident)

For example, R.M. Kiknadze first entered the territory of the Russian Federation on September 1, 2011 and got a job at the Alpha organization. When calculating wages for the first two months of 2012 (January, February), his tax status was determined as “non-resident of the Russian Federation.” In this regard, the accountant withheld personal income tax from his income at a rate of 30%.

When calculating employees' wages for March 2012, it was determined that the tax status of R.M. Kiknadze changed to “resident of the Russian Federation,” and therefore personal income tax on his income for March was calculated at a rate of 13%. During 2012, R.M. Kiknadze was on long business trips abroad (he did not stay on the territory of the Russian Federation) from April 1 to May 31 inclusive and from July 1 to November 11 inclusive.

Thus, his status as “resident of the Russian Federation” remained until September 2012 inclusive. During this period, to the income of R.M. Kiknadze applied a tax rate of 13%.

At the end of October and the end of November he was recognized as a non-resident of the Russian Federation. Accordingly, for these months the tax on his income was calculated at a rate of 30%.

Information about the tax status of R.M. Kiknadze in the corresponding months of 2012 and the personal income tax rate are shown in Table 1.

At the time of changing the employee’s status (when a non-resident becomes a resident), there is no need to recalculate the tax withheld from the beginning of the year at a rate of 30%. The fact is that the final tax status of an employee, depending on the time of his stay in the Russian Federation, is determined based on the results of the tax period. It is at the end of the year that the tax withheld from its beginning is recalculated (clause 1.1 of Article 231 of the Tax Code of the Russian Federation, Letters of the Ministry of Finance of Russia dated October 28, 2011 No. 03-04-06/6-293, dated May 16, 2011 No. 03 -04-05/6-353).

The difference between personal income tax withheld at a rate of 30% and the tax that you recalculated at a rate of 13% is the amount of tax withheld in excess. It is refundable to the taxpayer.

A foreigner must apply for a refund of over-withheld personal income tax to the tax office where he is registered at his place of residence (place of stay). To do this, he submits in the tax return documents confirming his tax resident status (clause 1.1 of Article 231 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of Russia dated January 16, 2013 No. 03-04-06/4-11, dated August 9, 2012. No. 03-04-06/6-230, dated May 16, 2011, No. 03-04-06/6-108, dated November 22, 2010, No. 03-04-06/6-273 (clause 2), Federal Tax Service of Russia dated March 21, 2012 No. ED-3-3/ [email protected] , Federal Tax Service of Russia for Moscow dated March 22, 2011 No. 20-14/3/ [email protected] , dated February 18, 2011 No. 20-14/3/015325).

Tax authorities explain that among such documents you can submit, for example, travel documents on entry into the Russian Federation and exit from the Russian Federation, a copy of a passport with marks from border control authorities about crossing the border, certificates from the employer drawn up on the basis of a time sheet, receipts about staying in a hotel (Letters from the Federal Tax Service of Russia for Moscow dated May 13, 2011 No. 20-14 / [email protected] , dated February 18, 2011 No. 20-14/3/015325).

But what if the taxpayer leaves the Russian Federation and cannot personally contact the inspectorate for a refund of the overly withheld tax? The Ministry of Finance of Russia in Letter dated January 24, 2013 No. 03-04-06/4-22 explained that the declaration can be submitted without appearing at the tax authorities: submitted through a representative, sent by mail or transmitted electronically via telecommunication channels. The above Letter emphasizes that the authorized representative may also be the employing organization. In such situations, we recommend that you complete all formalities for such representation in advance.

In addition, before the employee leaves Russia, it is necessary to provide for the procedure for receiving funds in the form of personal income tax amounts returned to him, for example, opening a bank account in advance for their transfer.

If on the date of receipt of income, including the day of dismissal, an employee of the organization was a tax resident of the Russian Federation, then upon his dismissal before the end of the tax period, the tax agent does not make any recalculations of tax amounts withheld at the rate of 13% (Letters from the Ministry of Finance of Russia dated July 14, 2011 No. 03-04-06/6-170, dated July 14, 2011, No. 03-04-06/6-169, dated May 25, 2011, No. 03-04-06/6-122).

Let us note that until 2011, the return of excessively withheld personal income tax was carried out by a tax agent on the basis of an application from a foreign employee (clause 1 of Article 231 of the Tax Code of the Russian Federation).

At the same time, officials did not have a clear opinion on how the tax should be recalculated in such a case. So, based on the explanations of the regulatory authorities, such a recalculation could be carried out:

– on the date after which the status of an individual will no longer change in the current year (Letters of the Ministry of Finance of Russia dated July 17, 2009 No. 03-04-06-01/176, dated July 25, 2008 No. 03-04-06-01 /231, Federal Tax Service of Russia dated June 25, 2009 No. 3-5-04/ [email protected] , Federal Tax Service of Russia for Moscow dated January 30, 2009 No. 18-15/3/ [email protected] , dated June 24. 2008 No. 28-10/059251);

– at the end of the tax period, if the status may change before the end of the year (Letters of the Ministry of Finance of Russia dated March 26, 2010 No. 03-04-06/51, dated November 7, 2008 No. 03-04-06-01/331, Federal Tax Service Russia dated June 25, 2009 No. 3-5-04/ [email protected] , Federal Tax Service of Russia for Moscow dated January 30, 2009 No. 18-15/3/ [email protected] , dated June 24, 2008 No. 28-10/05925);

– on the date of termination of labor relations (Letters of the Ministry of Finance of Russia dated November 7, 2008 No. 03-04-06-01/331, dated July 25, 2008 No. 03-04-06-01/231).

Let us clarify that the Tax Code of the Russian Federation did not stipulate that personal income tax is recalculated only if the status of a tax resident cannot change in the current year. That is, you had the right to recalculate the tax on the date of payment of income that the foreigner received already as a resident. However, if he lost his tax resident status, the tax had to be recalculated at a rate of 30%. In this regard, it was advisable to follow the recommendations of the regulatory authorities and recalculate personal income tax when it was finally clear that the foreign worker would not lose the status of a tax resident of the Russian Federation by the end of the year.

If it was impossible to determine this during the year, personal income tax should have been recalculated at the end of the tax period (year), provided that at the end of the tax period the foreigner would remain a tax resident of the Russian Federation.

An example of taxation of wages of a foreign worker when he acquires the status of a tax resident of the Russian Federation

Condition:

Citizen of Ukraine P.V. Grigorenko entered the territory of the Russian Federation on March 2, 2012 (mark of the border control authority in the passport).

On April 20, 2012, he was hired by the Alpha organization as an engineer with a monthly salary of 20,000 rubles.

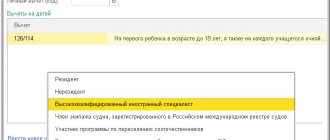

P.V. Grigorenko has one child.

From September 1, 2012 (183rd day of stay on the territory of the Russian Federation) P.V. Grigorenko is a tax resident of the Russian Federation. Until this date, the employer withheld personal income tax from the income paid to him at a rate of 30% and, accordingly, did not provide him with standard tax deductions (clause 4 of article 210 of the Tax Code of the Russian Federation).

In August and September 2012 P.V. Grigorenko was paid an advance in the amount of 10,000 rubles. for each of these months. His salary for August and September 2012 was accrued in the amount of 20,000 rubles. for every month. In accordance with the rules in force in the Alpha organization, wages are paid to employees through the cash desk no later than the 20th day of the billing month and the 5th day of the month following the billing month.

Solution:

1. Let’s calculate the amount of personal income tax from P.V.’s wages. Grigorenko for August 2012

On the date of payment of income, i.e. on the last day of August (according to paragraph 2 of Article 223 of the Tax Code of the Russian Federation), P.V. Grigorenko is not a tax resident, since as of August 31, his stay in the Russian Federation was 182 calendar days over the last 12 months. Consequently, the organization calculates personal income tax at a rate of 30%, without providing a deduction for the child (clause 3 of article 210, clause 3 of article 224 of the Tax Code of the Russian Federation).

The amount of tax that the organization must withhold from wages for August is 6,000 rubles. (RUB 20,000 x 30%).

2. We pay the employee wages through the cash register (taking into account the previously paid advance), withhold personal income tax and transfer it to the budget.

The salary paid to the employee is 4,000 rubles. (20,000 rub. – 10,000 rub. – 6,000 rub.).

The amount of withheld personal income tax (RUB 6,000) must be transferred to the budget no later than September 5, 2012 (clause 6 of Article 226 of the Tax Code of the Russian Federation).

3. Let’s calculate the amount of personal income tax from P.V.’s wages. Grigorenko for September.

On the date of payment of income, i.e. on the last day of September (according to paragraph 2 of Article 223 of the Tax Code of the Russian Federation), P.V. Grigorenko is recognized as a tax resident, since as of September 30, the period of his stay in the Russian Federation over the past 12 months is 213 days. Consequently, the organization calculates personal income tax at a rate of 13% (clause 1 of Article 224 of the Tax Code of the Russian Federation).

To do this, we determine the income of P.V. Grigorenko for September. It will be 20,000 rubles.

A tax at a rate of 13% must be calculated on an accrual basis based on income from the beginning of the year (clause 3 of Article 226 of the Tax Code of the Russian Federation). Therefore, personal income tax must be recalculated from the beginning of the year. However, tax recalculation in connection with the acquisition of the status of a tax resident of the Russian Federation is possible only at the end of the year (clause 1.1 of Article 231 of the Tax Code of the Russian Federation). In this regard, the tax is calculated on an accrual basis, starting from the income received by P.V. Grigorenko since September 2012

Taking into account the provisions of P.V. Grigorenko standard deduction for a child (for September), his tax base is equal to 18,600 rubles. (RUB 20,000 – RUB 1,400)

Let us remind you that the standard deduction for a child is provided until the income, calculated on an accrual basis from the beginning of the tax period, does not exceed 280,000 rubles. (Clause 4, Clause 1, Article 218 of the Tax Code of the Russian Federation). Let us assume that the income of P.V. Grigorenko's cumulative total in September 2012 did not exceed 280,000 rubles.

4. The amount of personal income tax subject to withholding from the income of P.V. Grigorenko for September 2012 will be 2418 rubles. (RUB 18,600 x 13%).

5. We pay the employee wages from the cash register (taking into account the previously paid advance), withhold the amount of personal income tax and transfer it to the budget.

The salary to be paid to the employee will be 7,582 rubles. (RUB 20,000 – RUB 2,418 – RUB 10,000).

The amount of withheld personal income tax (RUB 2,418) must be transferred to the budget no later than October 5, 2012 (paragraph 1, clause 6, article 226 of the Tax Code of the Russian Federation).

An example of recalculating personal income tax at the end of the year from the salary of a foreign employee when he acquires the status of a tax resident of the Russian Federation

Condition:

Let's use the conditions of the previous example and assume that the total income of P.V. Grigorenko for 2012 amounted to 168,571 rubles.

Let’s assume that personal income tax was withheld on an accrual basis at a rate of 30% from April to August 2012 in the amount of 26,571 rubles. of the income received during that period in the amount of 88,570 rubles. And at a rate of 13%, the tax was withheld in the amount of 9,672 rubles. from income for September – December 2012 (13% x (20,000 rub. x 4 – 1,400 rub. x 4)).

Solution:

1. Let’s determine the tax base for employee P.V. Grigorenko for 2012

Taking into account the provisions of P.V. Grigorenko standard deduction for a child (for April - December), its tax base will be 155,971 rubles. (RUB 168,571 – 1400 x 9). Let us remind you that the standard deduction for a child is provided until the income, calculated on an accrual basis from the beginning of the tax period, does not exceed 280,000 rubles. (Clause 4, Clause 1, Article 218 of the Tax Code of the Russian Federation). Income P.V. Grigorenko for 2012 amounted to 168,571 rubles, i.e. did not exceed 280,000 rubles.

2. Let’s determine the amount of personal income tax to be withheld from P.V.’s income. Grigorenko for 2012. It will be 20,276 rubles. (RUB 155,971 x 13%).

3. Let’s determine the amount of personal income tax excessively withheld from P.V.’s income. Grigorenko for 2012. It is equal to 15,967 rubles. (RUB 20,276 – RUB 26,571 – RUB 9,672).

The organization must reflect this amount in clause 5.6 of the certificate in form 2-NDFL, submitted to the tax office at the place of registration no later than April 2, 2012 (Monday), since April 1, 2012 falls on a Sunday (clause 7, article 6.1 , clause 2 of article 230 of the Tax Code of the Russian Federation). For the return of excessively withheld personal income tax P.V. Grigorenko should contact the tax office at the place of registration at the end of 2012, submitting a tax return and documents confirming the status of a tax resident (clause 1.1 of Article 231 of the Tax Code of the Russian Federation).

The procedure for recalculation (recalculation) and withholding of personal income tax when changing the status of a foreign employee (a resident has become a non-resident)

The status of a foreign worker (resident of the Russian Federation or non-resident of the Russian Federation) should be determined on each date of payment of income to him. This is because its tax status may change during the tax period.

Depending on whether your employee is a resident or not when his earnings are calculated, you will apply one of two tax rates - 13 or 30%, respectively (clauses 1, 3 of Article 224 of the Tax Code of the Russian Federation).

Let's consider a situation in which a foreign worker was a tax resident of the Russian Federation from the beginning of the year, but lost this status during the tax period.

For example, a citizen of Kazakhstan, E.I., works in the organization \"Gamma\". Amanzholov, whose salary is 20,000 rubles. per month. Let us assume that when calculating wages for January, February, March, April 2012, his tax status was determined as “resident of the Russian Federation.” From his income for these months, the accountant withheld personal income tax at a rate of 13%. No deductions were provided to him due to lack of grounds. The total amount of personal income tax was 10,400 rubles. (RUB 20,000 x 4 months x 13%).

When calculating E.I. Amanzholov's salary for May, the accountant determined that his status had changed to non-resident, and therefore calculated personal income tax on his income at a rate of 30%. The tax amount was 6,000 rubles. (30% x RUB 20,000).

Information on determining the tax status of E.I. Amanzholova in the corresponding months and the tax rate for personal income tax are shown in Table 2.

When an employee’s tax status changes (a resident becomes a non-resident), there is no need to recalculate the tax withheld since the beginning of the year at a rate of 13%. The fact is that the final tax status of an employee, depending on the time of his stay in the Russian Federation, is determined based on the results of the tax period. It is at the end of the year that the tax withheld from the beginning of the year is recalculated. See Letters of the Ministry of Finance of Russia dated May 21, 2009 No. 03-04-05-01/313, dated July 4, 2007 No. 03-04-06-01/210 (clause 3), Federal Tax Service of Russia for Moscow dated December 29, 2008 No. 19-12/121898.

Let's use the conditions of the previous example. Let's assume that on June 4, 2012 E.I. Amanjolov again acquired the status of a resident of the Russian Federation (as of this date, the number of days of his stay in the Russian Federation for the 12 consecutive months was 183).

As of June 30, 2012, the number of days of stay in the Russian Federation over the past 12 months was 209. Accordingly, E.I. Amanjolov was recognized as a resident of the Russian Federation and for June the tax was calculated for him at a rate of 13%. The personal income tax amount was 2,600 rubles.

However, in July 2012, the status of E.I. Amanzholov was changed to a non-resident and, due to long business trips, he was recognized as a non-resident of the Russian Federation until the end of 2012. The tax on his income for July and subsequent months was calculated at a rate of 30%. The amount of personal income tax for six months (July - December 2012) amounted to 36,000 rubles. (RUB 20,000 x 6 months x 30%).

Relevant information is given in Table 3.

Paid from the income of E.I. Amanzholov, based on a rate of 13%, the amount of personal income tax for January, February, March, April and June 2012 should be recalculated at a rate of 30%.

That is, if at the end of the tax period it is determined that the status of your employee has changed from resident to non-resident, the tax paid in this tax period on his income at a rate of 13% will have to be recalculated.

An example of recalculation of personal income tax when changing the tax status of a foreign worker (a resident of the Russian Federation became a non-resident of the Russian Federation) at the end of the tax period

Condition:

At the end of 2012 E.I. Amanjolov lost his status as a tax resident of the Russian Federation (see example above).

Solution:

1. Let’s calculate the amount of personal income tax paid by E.I. Amanzholov's salary for December.

As of the date of payroll, the employee is not a tax resident of the Russian Federation. Therefore, personal income tax is calculated at a rate of 30% (clause 1 of Article 224 of the Tax Code of the Russian Federation) (20,000 rubles x 30% = 6,000 rubles).

2. Since E.I. By the end of the tax period (2012), Amanjolov lost his tax resident status; the organization needs to recalculate the personal income tax withheld from his income at a rate of 13% for 5 months (January, February, March, April, June). Recalculation must be made at the rate of 30% applied to the income of non-residents.

The amount of personal income tax that E.I. Amanzholov must pay additionally to the budget of the Russian Federation, amounting to 17,000 rubles. (RUB 20,000 x 5 months x 30% – RUB 20,000 x 5 months x 13%).

The total amount of tax that must be paid to the budget on the income of E.I. Amanzholova at the end of 2012 will amount to 23,000 rubles. (6,000 rub. + 17,000 rub.).

3. Let's calculate the amount of wages that need to be paid to the employee for December 2012, taking into account the withholding of personal income tax.

According to para. 2 clause 4 art. 226 of the Tax Code of the Russian Federation, the withheld amount of tax cannot exceed 50% of the cash payment.

Consequently, when paying earnings to E.I. Amanzholov can only withhold 10,000 rubles for December 2012. tax

The remaining tax is 13,000 rubles. (23,000 rubles – 10,000 rubles) is withheld from payments in subsequent months.

It is not always possible to recalculate personal income tax and withhold it from the employee’s income. After all, if the employment relationship with the employee is terminated and you do not pay him income, then, accordingly, you have nothing to withhold the missing amounts of tax from. In this case, you need to inform the taxpayer and the tax authority at your place of registration in writing about the impossibility of withholding tax and the amount of debt of the foreign employee (clause 5 of Article 226 of the Tax Code of the Russian Federation). This employee must pay this amount independently (Letter of the Ministry of Finance of Russia dated March 19, 2007 No. 03-04-06-01/74).

N. Skvortsova

How and by whom is the calculation done?

The calculation of amounts is carried out by tax agents who keep records from the month from which the employee received tax status, provided that he stays in the Russian Federation for more than 183 days. Under such conditions, the amount of deductions from an employee as a non-resident is calculated at the rate of 30 percent of all income.

From the moment of obtaining resident status, the agent recalculates the amounts at a lower rate, which is equal to 13% and determines the total overpayment of personal income tax. Subsequent tax withholding occurs at the key rate, as for all residents, and overpaid amounts are returned to the employee.