What does the adjustment number mean in 3 personal income tax?

Declaration 3 Personal income tax is one of the few types of tax reporting that ordinary citizens face. After all, according to Article 226 of the Tax Code of the Russian Federation, tax agents report for individuals. Only if the agent is unable to withhold personal income tax and submit a report for an individual, the citizen is obliged to report to the tax office and pay tax.

Important! 3 Personal income tax is filed by a citizen if the employer cannot withhold income tax from him.

The most common examples of such cases:

- Payment of income to a person in kind. According to the rules of Article 226 of the Tax Code of the Russian Federation, when issuing income in the form of things, property rights and other non-monetary equivalents, the tax agent is obliged to withhold personal income tax from the next cash payment. But if this is not expected, then the agent reports to the Federal Tax Service that he did not withhold the tax, and the Federal Tax Service itself is already engaged in collecting the amount due from the citizen.

- Receipt of income by an individual from another individual: sales, rental transactions. A tax agent is an organization or individual entrepreneur, and an ordinary individual cannot act as an agent, therefore, in economic relations between an individual and an individual, it is impossible to withhold tax at the source of payment.

- Submitting a return to use the tax deduction. Chapter 23 of the Tax Code of the Russian Federation provides for 5 types of tax deductions, for the application of which it is necessary to submit Form 3 of personal income tax with accompanying documents to the inspectorate.

The following reporting form is currently in effect:

It was adopted by order of the Federal Tax Service of Russia dated October 3, 2021 No. ММВ-7-11 / [email protected] as amended on October 7, 2021. This form is valid from 2021. Required sheets:

- title;

- section 1;

- section 2.

Other pages are added to the form as needed. On the title page 3 of the personal income tax the adjustment number is indicated. What this detail means is the order in which reports are submitted for the same period.

Important! Adjustment is information about how many times the declaration for the same period is adjusted in turn. The adjustment can be zero or numeric.

In what cases is an updated personal income tax declaration 3 submitted?

The requirement to supplement information from the applicant involves correcting a poorly executed page. All documents are provided in 2 copies for the convenience of the Federal Tax Service. The process can take place in three ways:

- personal visit to the service, during which it is necessary to register an application;

- on the official tax website;

- by post with an inventory.

It is not allowed to make corrections or cross-outs in the document. If the declaration form is supplemented with documents, then it is necessary to create a cover letter with a personal signature. You cannot print information on both sides of a sheet. There are a number of circumstances when it is necessary to modify the primary declaration:

- presence of technical inaccuracies;

- detection of receipts later than submission;

- failure to indicate taxable objects or transactions;

- mathematical calculation errors;

- obtaining the right to property and social deductions.

Adjustment 3 is made if an error is made in the information on transactions. For example, the personal data of the parties is incorrectly indicated. Inaccuracies are detected by both the citizen and the tax authority employee in the process of diagnostic activities.

How to find out the number

How to find out the adjustment number in personal income tax return 3:

- if you submit a report for the first time for the period, then your adjustment is zero, that is, there is no adjustment at all, you did not make an adjustment and your report was submitted for the first time;

- if you submitted reports, then there was a need to supplement it or correct errors, then an updated form is submitted and the order of correction is indicated: “1” - correction for the first time, “2” - information is updated for the second time, etc.

Often a citizen does not remember all the transactions made in past periods and misses them when filling out the form. Considering that the statute of limitations for personal income tax is 3 years, this is natural. For example, in 2021 you turned in the 2021 form to receive a property deduction from your paycheck. And in 2021, they remembered that among your income from which the tax was paid was not only your salary, but also the proceeds from the sale of your car. To enter additional information, you will have to fill out the form again and indicate that it is updated, i.e. adjustment “1”.

How to fill it out correctly?

Please note: The Federal Tax Service requires that if there are empty fields on the certificate, there should be dashes after the number.

That is, if you are submitting a declaration for the second time, the line indicating the number should contain the value “1 – -”; if the declaration is submitted for the eleventh time, you need to put “10-”. The Tax Service requires compliance with the rule, because otherwise, it will not be entirely clear to the inspection inspector whether the number is written in full or whether the entrepreneur forgot to add a few digits. Cross-throughs, mechanical damage to the paper (due to an attempt to erase a number with an eraser, for example), are not allowed, and “smearing” the number with a proofreader is also not encouraged.

If for some reason you entered the number incorrectly, but categorically do not want to write a new declaration, you can correct the document: just carefully cross out the incorrect inscription with red ink, and write the correct value on top with the same red ink.

There should be only one dash line, and it should be placed in such a way that the originally entered data is clearly readable. If you do not follow these rules, the tax inspector may not accept the document, requiring you to submit a new declaration.

What number should I indicate when submitting for the first time?

As of 2021, the Federal Tax Service has not changed the rules for indicating the number upon initial submission. Therefore, as before, you need to put “0” in the number column . If you are submitting a document for the second time, you need to put “1” - etc.

During the initial submission, the same registration rules apply as when entering corrective data. This means the following: corrections are not allowed, and if they need to be made, then only according to the instructions above; There should be dashes after the number “0”. The final appearance of the number should be: “0 – -”.

What to write in the declaration

You need to write the adjustment number in 3 personal income tax in a special column on the title page at the top of the page, next to the year and period.

Note! The column “adjustment number” is required to be filled out. Submitting a report without specifying this detail may result in questions from the Federal Tax Service or a negative response based on the results of a desk audit.

Primary

In fact, the primary adjustment code in 3 personal income tax is “0”, since you are submitting the report for the first time. To correct any information, you first need to formalize it at least for the first time.

https://www.youtube.com/watch?v=aItjLw7-1k4

Take into account! Submitting form 3 personal income tax for the first time is accompanied by an adjustment number “0”, which means that the form has no clarifications and has not been submitted before for the same period.

Code “0” is the most common when filling out form 3 of personal income tax. How to write it:

- on a paper form - write down the combination “000” in the column;

- in the program or in the service of the taxpayer’s Personal Account - enter one “0”.

For reference! The income tax return can be submitted in paper or electronic form. The paper form is filled out manually or on a computer with subsequent printing; the electronic format is compiled using a program or online service and submitted to the Federal Tax Service via a telecommunication channel.

Refined

A correction number in the personal income tax return occurs if a citizen:

- supplements the report with new information on its own initiative;

- corrects errors identified by the inspection.

The Tax Code of the Russian Federation has no limits on the number of adjustments to the form. In fact, you can clarify information an unlimited number of times, but, of course, such actions without justification are not welcomed by the tax authorities.

Tax inspectors may not notice that you failed to report an old sale or deduction. The main thing is that the result on the form matches the data in the AIS database: the amount of personal income tax to be paid or refunded.

Results

Errors in already submitted tax reports are divided into 2 groups: those requiring clarification and those left at the discretion of the taxpayer. For whatever reason the reporting is specified, it is formed in the same way as the original one (on the same form and according to the same rules), but filled in with the correct data. What distinguishes such a report from the original one is the serial number of the correction, which is entered in a special field on the title page. In the original report, 0 is indicated there, and the numbering of updated reports, therefore, begins with the number 1.

Sources:

Tax Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Sanctions for errors in the declaration

Responsibility for errors in the tax return 3 personal income tax is regulated by Article 81 of the Tax Code of the Russian Federation. Consider the following nuances:

- errors are divided into 2 types - underestimating the tax payable and not underestimating the tax payable;

- if a citizen himself discovers that he made a mistake that reduces the personal income tax payable, and managed to pay the missing amount before the deadline for paying the tax and before the inspection error was discovered, then no fines will be accepted based on the submitted updated form; Documents confirming that personal income tax has been paid in full within the prescribed period must be attached to the report;

- if the payer submitted the form without independently paying the arrears or after an inspection error was discovered, then he may be held liable; According to Article 81 of the Tax Code of the Russian Federation, such citizens are fined in the amount of 20% of the amount of tax required to be paid to the state budget.

Do I need to submit an updated declaration?

If any deficiencies are found, you will need to submit an amended return, since a return with errors will not be considered valid. Problems and shortcomings must be addressed immediately. However, there are times when you will decide for yourself whether you need to submit an amended return or not.

If, when filling out the declaration, you made errors in calculations in the direction of overpaying taxes, then it is not necessary to correct this. Therefore, you will decide for yourself whether you want to submit a new version of 3-NDFL or leave everything as it is. But if the amount of taxes indicated was less, then the report must be redone.

Features of filling out the document

When preparing tax returns, you should know and use the rules and regulations adopted by law. In particular, they relate to the features of filling out the document. The main nuances include:

- Entering basic data. The 3-NDFL tax return consists of many empty boxes. They all require filling out. A person filling out this form for the first time may be confused, but in practice, filling out the document is not a difficult task. All the necessary information is simply copied from existing documents that must be attached to the 3-NDFL certificate.

- Requirements for registration. Here, too, everything is quite simple: you should enter data (texts, numbers) carefully and without errors. You can use a pen with blue or black ink. It is better to avoid typos or corrections. All amounts required to be filled out should be indicated in Russian rubles, and kopecks should also be noted (if any).

- Registration of details. It is worth making sure that each page of the declaration you fill out has a separate number in order. It is necessary to indicate the payer’s TIN, initials, completion date for filling out the document and personal signature. Also, the declaration must have up to 3 barcodes on each page.

Every taxpayer has benefits and discounts. There are about five of them (according to tax returns). Moreover, sometimes a situation arises when the payer claims to use several benefits at once in one tax period. The 3-NDFL adjustment number serves in such cases, that is, it makes it clear to the tax authorities which tax return form is submitted by the payer for a certain reporting time.

Some taxpayers wonder whether there really is such a need for affixing serial numbering (adjustment code). After all, all the documents are already available to tax inspectors, and there is also a complete database that contains all the necessary information. But the corrective code was created and implemented for some reason.

It is known that declarations can be drawn up and submitted not only through a personal visit to the NI, but also by sending documents electronically via the Internet or sent by mail. And sometimes a taxpayer needs to send several types of reporting to the tax authorities at once. But technical failures may occur, and some of the documents will arrive a little later.

This is where the adjustment code becomes useful. For example, a tax inspector, receiving a declaration with code 1 or 2, understands that another document must be received - coded 0. General reporting is not disrupted, and the taxpayer avoids possible errors when submitting documents.

The 3-NDFL declaration form has a corresponding box for entering the code on the first sheet of the document. Moreover, regardless of the year of issue of the form, the cell does not change its location. This field is located under the name of the form, on the front side. Next to it there is a line reserved for indicating the period for submitting reports, and a little to the right is the NI code (tax office), where you need to send the completed document for review and verification.

How to submit an updated personal income tax return 3 through your personal account

This year it became possible to create a declaration online. To do this, you need to register on the official website of the Federal Tax Service. Registration begins with the initial procedure, in which the person’s login and password are entered. The login is the TIN, and the password is created independently. In your personal account there are a number of items at the top of the panel. You should select Form 3 personal income tax, then fill it out and send it. Documentation is certified through a personalized digital signature. Without it, it is impossible to submit any option.

When the payment is not in favor of the budget

If the Federal Tax Service considers that the initial tax return indicated an underestimated amount of tax, different situations may arise regarding the collection of arrears.

Table 1. Examples of arrears collection

| Example 1 | Tax officials received updated information within the reporting period. For example, in February 2021, an organization filed a declaration under the simplified tax system containing information for the previous year. At the same time, management discovered errors and inaccuracies quite quickly. Such an organization should hurry up and show the changes to the tax office before the end of March 2021. Then the tax office will consider that the date of filing the clarification coincides with the date of filing the primary reporting, and this will not lead to negative consequences. |

| Example 2 | There is still an opportunity to pay the tax, despite the late filing period. Let's consider one of the tax regimes - UTII, for which you need to report no later than July 20, and pay the tax amount no later than July 25 (for the 2nd quarter). Provided that the tax was paid to the budget on time, and the taxpayer himself recognized the error (outside the results of the audit activities of the tax authorities), a repeated application to the tax office will not lead to arrears. |

| Example 3 | When the taxpayer violated the deadlines for payment and transfer of tax information. In this example, before sending the updated declaration, it is necessary to make payments for arrears - information about this can be found in paragraph 4 of Article 81. This is necessary to avoid penalties under Article 122 of the Tax Code of the Russian Federation. In general, a taxpayer's inaction in paying taxes when calculated correctly does not result in penalties. Important! The debt is considered to be repaid at the time the payment order is submitted to the bank branch. Therefore, the period of delay does not include the actual day the tax was paid. The penalty is 1/300 of the refinancing rate and is charged for each day of non-payment of the tax amount. In general, the mechanism for which Art. 122 cannot be applied in the case of correct tax calculation, even if it was paid later than the specified period. The taxpayer becomes a delinquent if arrears arise. There are other methods of influence, including Article 75 of the Tax Code of the Russian Federation (fines), seizure of bank accounts |

| Example 4 | Information about understatement of taxes came from an official letter from the tax inspectorate. Under such conditions, in addition to arrears, the taxpayer is required to pay a fine. In quantitative terms, the fine is equal to 1/5 of the unpaid tax amount (according to Article 122 of the Tax Code of the Russian Federation). For example, an organization showed a tax of 1000 rubles and did not pay it. When reviewing the documents, representatives of the tax inspectorate determined the amount of tax in the amount of 1,200 rubles. Additional tax assessment (200 rubles) means that a fine of 40 rubles (20% * 200 rubles) will be issued. If the taxpayer acted intentionally (such cases are very difficult to prove), the fine for evasion of duties will increase to 40% of the tax amount. |

From the beginning of 2021, Article 122 also covers insurance contributions to extra-budgetary funds, since tax services now oversee their collection.

Remember. If several declarations are submitted sequentially for one period, to calculate a fine, representatives of the Federal Tax Service will compare the amount of tax in the first and last forms, without taking into account intermediate information.

- The payer managed to submit it before the official decision of the Federal Tax Service was made, having previously paid the tax and penalties.

- After the on-site inspection, no violations were found.

In practice, tax authorities actively fine for violations of Article 122 of the Tax Code of the Russian Federation. It is important to know that you can avoid liability even after submitting the clarification. To do this, arrears must be paid and objective reasons for untimely application must be indicated. The consideration of the case regarding penalties is carried out in accordance with Art. 112 of the Tax Code of the Russian Federation.

Didn't find the answer to your question? Find out how to solve exactly your problem - call right now:

+7 (Moscow) (St. Petersburg)

Form 3 Personal Income Tax is a tax return that has many cells and nuances for filling it out, one of which is the correct entry of the adjustment number in the form. This form must be filled out by persons who independently report their income to the tax office.

Firstly, these are persons engaged in entrepreneurial activities and private practice, and secondly, these are all kinds of income that are not listed in certificate 2 of the personal income tax (wages, vacation pay, sick leave, financial assistance, etc.). This type of income includes income from the sale of one’s own property; movable, immovable property, shares, shares received as a gift; income received in the form of winnings, lotteries; income from civil partnership agreements (for example, lease agreements) and others.

Procedure for filling out tax return 3 personal income tax

All possible completions of declaration 3 are carried out by an individual in his own hand, only the title page is filled out by a tax authority employee. The document is created in 2 copies. One remains with the applicant, and the other with the Federal Tax Service. Along with the official papers, a register is provided that lists the applications. Sometimes employees hand over such a form, and the payer fills it out by hand. The declaration can be submitted in electronic format, then all pages are signed and submitted to the inspection.

Filling out takes place in Russian. Amounts are indicated in rubles, with the exception of foreign income. Kopecks are not indicated in the personal income tax amount. Indicators must be rounded, then it is possible to correctly fill out 3 personal income taxes. The taxpayer provides the following information:

- profitability for the reporting period;

- sources of finance;

- deductions: social, property and others;

- retention;

- advance payments;

- amount of refundable tax.

Reasons for adjustments

The taxpayer may make a mistake in the address or provide other incorrect information, underestimate the amount of tax, refraining from reporting the full amount of income. In the latter case, the taxpayer must send repeated information to the regional Federal Tax Service; in all other cases, he has such a right, but they will not be able to force him to adjust the declaration.

Example. If an individual draws up documents to receive a social deduction and makes a mistake by not including the full amount spent on treatment, the funds will not be received from the budget in full. In order for the taxpayer to be paid the missing money, he needs to re-submit the declaration information based on the data of the same tax period.

Article 81 of the Tax Code reveals the concept of false information - this occurs when the taxpayer erroneously records income or expenses, indicates incorrect results of the enterprise’s activities, or makes mistakes in the final values of the amounts payable. In general, tax authorities recognize arithmetic inaccuracies, incorrect indication of the tax period, and standard codes as errors (for example, when submitting information, the TIN number is entered; checkpoints, a list of KBKs, and other unified values may also be included among the marks).

Remember! Reporting within the framework of 3-NDFL falls under the responsibility of the territorial divisions of the Federal Tax Service, therefore information should be submitted to the body where the taxpayer is registered. The updated tax data is transferred to the same department where you will submit the initial declaration. The form on which the primary information is reflected, valid until clarification, remains relevant in the future - thus, the reporting form is preserved for subsequent requests. The taxpayer always relies on information from the period in which the inaccuracy was found (clause 5 of Article 81 of the Tax Code). If in 2021 a situation arises in which data for 2014 is being clarified, the taxpayer must use the appropriate 2014 form for clarification.

For a citizen who applies for a social deduction, wanting to return part of the funds for treatment, the presence of incorrect information that underestimates his actual costs leads to incomplete compensation from the budget. To receive the missing amount in monetary terms, you need to fill out a declaration again - submit a clarifying form to the tax office.

Find out more about the tax deduction for medical services in our article. We will tell you about the features of obtaining this deduction and the necessary documents.

Remember! You can apply for a deduction at any time, and information will be considered for the last three calendar years. Failure to comply with the deadline for submitting the declaration will not affect the transfer of funds in favor of the taxpayer and does not impose liability on the individual. Those who claim deductions in 2021 will receive money based on 2015, 2021 and 2021 data.

When resubmitting, the document must contain current data

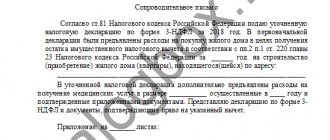

In this case, the tax authority does not officially require clarification, but may subsequently request details and clarifying details. An example of such a situation is a desk audit. It is recommended that you include an explanatory note with comprehensive details in the package.

For a complete picture, the cover letter may include the following information:

- The period for which the declaration is submitted.

- Type of tax.

- Graphs that contain clarifications (it is necessary to explain where the primary data and the newly corrected data are located).

- If the tax amounts and tax base have changed, the latest information is indicated.

- Details of the payment order, if the taxpayer has previously eliminated the arrears and paid the penalty in full.

In case of counting errors, additional documents are not needed. When a taxpayer issues a social deduction (to receive the unpaid balance of the amount), he submits an updated declaration and the necessary confirmations.