Table of KBK used by taxpayers of the simplified tax system in 2020

The simplified tax system with the object “income minus expenses” and the minimum tax should be calculated and paid according to the following BCC:

- 18210501021011000110 - tax;

- 18210501021012100110 - penalties;

- 18210501021012200110 - interest;

- 18210501021013000110 - fines.

The simplified tax system with the object “income” should be accrued and paid according to the following BCC:

- 18210501011011000110 - tax;

- 18210501011012100110 - penalties;

- 18210501011012200110 - interest;

- 18210501011013000110 - fines.

The sample payment system for the simplified tax system “income minus expenses” 2021 contains details that are applicable both for paying tax in connection with the simplified tax system and for paying the minimum tax calculated at a rate of 1% of annual income. The only difference will be in the purpose of payment.

When paying tax in connection with the simplified tax system, in the purpose of payment we write: “Tax in connection with the application of the simplified tax system for the 1st quarter of 2021.”

When paying the minimum payment, the following text is appropriate in the purpose of payment: “Minimum tax for 2021.”

The minimum tax is calculated at the end of the year; at the end of the quarter, advance payments are made according to the simplified tax system.

Code to list the simplified tax system in 2021

We provide a table that summarizes the deadlines for transferring advance payments under the simplified tax system in 2021, and also indicates the deadline for paying the single tax for 2021.

| Payment period | Term |

| For 2021 (only organizations pay) | No later than 03/31/2020 Transfer to 09/30/2020 |

| For 2021 (paid only by individual entrepreneurs) | No later than 04/30/2020 Transfer to 10/30/2020 |

| For the first quarter of 2021 | No later than 04/27/2020 Transfer to 10/26/2020 |

| For the first half of 2021 | No later than 07/27/2020 Transfer to 11/25/2020 |

| For 9 months of 2021 | No later than October 26, 2020 |

KEEP IN MIND

Federal Law No. 172-FZ dated 06/08/2020 for those affected by the coronavirus has written off tax under the simplified tax system for the 2nd quarter of 2021. Namely, the advance payment for the reporting period of half a year 2021, reduced by the advance payment for the reporting quarter of 2021. For more information, see “ To whom and what taxes will be written off for the 2nd quarter of 2021: list.”

Sample payment order for payment of the minimum tax in 2020 for individual entrepreneurs

Since the minimum tax is paid only at the end of the year, field 107 should always contain the value KV.04.2019; For advance payments, use the value of the quarter for which the payment is made.

The sample payment system for the simplified tax system “income” 2021 contains the same values of fields from 104 to 110 for both organizations and individual entrepreneurs.

An example of a payment order under the simplified tax system “income” in 2021

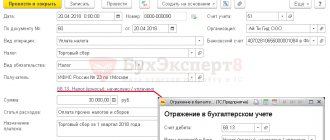

Payment orders for the transfer of tax (advance payments) must be completed in accordance with the Central Bank Regulations dated June 19, 2012 No. 383-P and taking into account the Rules approved by Order of the Ministry of Finance dated November 12, 2013 No. 107n.

Transfer the single tax and advance payments for it to an account in the territorial department of the Treasury of Russia according to the details of the tax inspectorate to which the organization is attached at its location. That is, at the address at which the organization was registered. It is listed in the Unified State Register of Legal Entities (clause 2 of Article 54 of the Civil Code). Even if the organization has separate divisions, transfer the single tax and advance payments according to the details of the inspectorate in which the head office is registered.

For an individual entrepreneur, this is the tax office, where he was registered at his place of residence.

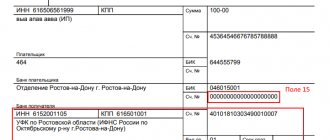

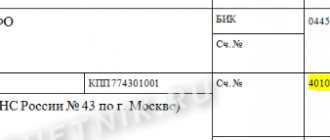

In field 16 “Recipient”, indicate the abbreviated name of the Federal Treasury body and in brackets - the abbreviated name of the revenue administrator: the name and number of the tax inspectorate or territorial branch of the Federal Social Insurance Fund of Russia. For example, “UFK for Moscow (IFTS No. 43 for Moscow).” The name of the recipient should not exceed 160 characters (Appendix 11 to the Regulations approved by the Central Bank of June 19, 2012 No. 383-P).

Here is a sample payment order under the simplified tax system “income” for 2019.

Read also

14.03.2018

General procedure for processing tax payment orders

Order of the Ministry of Finance of the Russian Federation dated November 12, 2013 No. 107n determines the mandatory details for paying taxes and insurance premiums:

- 101 - status of the payer who issued the payment document;

- 104 - twenty-digit budget classification code, where the first three digits correspond to the tax administrator number;

- 105 - OKATO;

- 106 - basis of payment, consists of two letters (TP, ZD, AR);

- 107 - frequency of tax payment - month, quarter, half year, year;

- 108 — document date, filled in depending on the indicator of field 106;

- 109 - document number, if the debt is repaid on demand;

- 110 - payment type, currently not filled in.

Receipt of the simplified tax system using the tax service!

Do you know that the tax office has made a service for entrepreneurs that allows them to fill out a simplified taxation system receipt? Are you glad that your taxes were used to do something useful specifically for entrepreneurs? Let's figure it out. On the tax website you can fill out a simplified taxation system receipt, no matter the payment of taxes, penalties or anything else, as if for all occasions. In common parlance this form is called a “stuffer”:

You indicate all the details one by one, the data from the databases is automatically entered and as a result you have a file with a completed receipt. Should you rush to use it?

Let's figure it out. The receipt for payment of the simplified tax system will be filled out, but... your details will not be saved. And every time you have to go through all the stages again, including if you want to redo something. The service (although it’s better to call it a “stuffer”?) will not remember either your details or your documents. It will not be possible to be surprised by the fact that codes from databases are substituted on the tax website; in times of automation, the Internet and numerous technologies, this is all simply done. But why do you need to stop? Is it possible to save the details?

Receipts for payment of tax according to the usn for individual entrepreneur form

Passport office (FMS in the category passport office has collected detailed information on the topics: Passport of a citizen of the Russian Federation: initial receipt at 14 and further replacement at 20 and 45 years old. Foreign passport of the Russian Federation: how to get a new (biometric) and old foreign passport in person and via the Internet? Constant registration at the place of residence and temporary registration at the place of stay. Temporary residence permit in Russia 2021. Residence permit in Russia: how to obtain, validity period, cost and necessary documents. How to obtain Russian citizenship? Russian citizenship, in general and simplified procedure Notary office, in the notary office category you will find answers to all the main questions that arise when contacting.

At the same time, the amount of advance tax payments cannot be reduced by more than 50. Individual entrepreneurs using the simplified tax system (reduced income cannot reduce the tax by the amount of expenses, but have the right to take the payment into account as expenses. Unified Income Tax (once a quarter until the 25th day of the month following the reporting quarter ) Declaration of UTII (once a quarter submitted before the 20th day of the month following the reporting quarter) Declaration of UTII Xls The amount of UTII tax payable can be reduced: from the amount of calculated UTII you can subtract a fixed payment to the Pension Fund of the Russian Federation minus the Federal Insurance Fund, but at the same time the amount single tax cannot be reduced by more than 50. Also, all payments in.

17 Jul 2021 stopurist 439

Share this post

- Related Posts

- Traffic rules lane for public transport

- If you bought a car and immediately sold it, do you need to pay tax?

- Recognition of paternity outside of marriage Russia through the court by the child’s mother

- Sample act for writing off goods and materials into production

How to pay taxes for individual entrepreneurs in a simplified manner: terms and methods

- income. In this case, 6% of the profit received by the entrepreneur is subject to payment;

- the difference between income and expenses. In this case, the tax is equal to 15% of the profit reduced by the amount of expenses. The rate for the “income minus expenses” object can be differentiated in regions. The tax amount varies from 5 to 15%.

Also read: Changing your last name a few years after marriage

When choosing such an organizational and legal type of business as an individual entrepreneur, many prefer to pay tax obligations under a simplified system. This is a type of taxation that is designed to reduce pressure on small businesses. When starting a business, you need to learn how to pay taxes for individual entrepreneurs using a simplified method, and what payment deadlines are provided for by law in the current year.

Sample of filling out a payment order for penalties under the simplified tax system for income

In addition to changes in the KBK, when paying penalties, filling out tax fields depends on whether you are paying the debt calculated independently or at the request of the Federal Tax Service. We reflected all the differences in the tables. Let's look at the filling samples.

Voluntary transfer of penalties according to the simplified tax system for income

If penalties for taxes from previous years are transferred, enter the tax period as year. If there are penalties on advance payments of the current year, then you need to indicate the quarter. Although it is quite difficult to meet such eccentrics who voluntarily list the penalties of the current period. In the latter case, there will be no error if you put the value “TP” in the “Base of payment” detail, since these are payments for the current year. However, penalties are still a debt, so it is better to write “ZD” in cell “106”.

Filling out the basic details for penalties under the simplified tax system is voluntary

| Field no. | Props name | Contents of the props |

| 101 | Payer status | 09 |

| 18 | Type of operation | 01 |

| 21 | Payment order | 5 |

| 22 | Code | 0 |

| 104 | Budget Classification Code (BCC) | 18210501011012000110 |

| 105 | OKTMO | OKTMO code of the municipality in which the individual entrepreneur is registered at the place of residence (stay) |

| 106 | Basis of payment | ZD |

| 107 | Taxable period | GD.00.2013; KV.01.2014; KV.02.2014; KV.03.2014; KV.04.2014 |

| 108 | Document Number | 0 |

| 109 | Document date | 0 |

| 110 | Payment type | 0 (from March 28, 2021, the value of attribute 110 is not indicated) |

Voluntary payment of penalties for the simplified tax system income sample of filling out a payment order 2014 for individual entrepreneurs

Download in format or

Penalty of the simplified tax system for income at the request of the Federal Tax Service

The debt for penalties under the simplified tax system with the object of taxation is income, paid upon request received from the tax authority, is transferred by payment order, samples of which are presented below. Depending on whether the UIN code is indicated in the Federal Tax Service’s request or not, the “Code” detail is filled out differently.

There is no UIN in the request

Penalties for the simplified tax system income on request sample payment slip 2014 for individual entrepreneurs

Download in format or

Sample payment slip for penalties of the simplified tax system (USN) for income with UIN

Similar to the example above, we fill out a payment order for the transfer of penalties for the simplified tax system on income at the request of the Federal Tax Service, which indicates the UIN code. We put it in the appropriate field. Can be done in several lines.

Sample payment order for

penalties of the simplified tax system income on demand for individual entrepreneurs in 2014 with UIN

Download in format or

Sample payment order for payment of a fine under the simplified tax system for income

The fine for non-payment or incomplete payment of the simplified tax system with the income base, presumably, is transferred only if there is a request from the tax inspectorate. Of course, rare entrepreneurs, without waiting not only for the requirement, but even for the decision to hold them accountable for a tax offense to come into force, rush to pay a fine. But these movements are unnecessary. You know when you need haste. However, this is not the case.

Penalty for the simplified tax system on income if there is a requirement

So, after the tax authority’s decision to prosecute came into force, you received a demand to pay a fine. The first thing you need to do is try to find a special field in it where the UIN code is printed. If such details cannot be found, or a zero (“0”) is indicated in it, then you can safely fill out the payment form according to the sample below.

Filling out the basic details for a fine under the simplified tax system for income

| Field no. | Props name | Contents of the props |

| 101 | Payer status | 09 |

| 18 | Type of operation | 01 |

| 21 | Payment order | 5 |

| 22 | Code | 0 |

| 104 | Budget Classification Code (BCC) | 18210501011013000110 |

| 105 | OKTMO | OKTMO code of the municipality in which the individual entrepreneur is registered at the place of residence (stay) |

| 106 | Basis of payment | TR |

| 107 | Taxable period | The payment deadline date established in the requirement DD.MM.2014 |

| 108 | Document Number | Requirement No. |

| 109 | Document date | Request date |

| 110 | Payment type | 0 (from March 28, 2021, the value of attribute 110 is not indicated) |

The request for a fine does not contain a UIN

Fine on the simplified tax system for income sample payment order 2014 for individual entrepreneurs

Download in format or

Deadline for payment of the simplified tax system for 2021

The deadline for paying the simplified tax depends on who pays it:

- until 31.03 – tax is paid by organizations;

- until 30.04 - individual entrepreneur.

If the deadline for payment falls on a holiday or weekend, it is postponed to the first working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

The deadline for paying the simplified tax for 2021 does not fall on holidays and weekends and is transferred to the budget:

- until March 31, 2020 - by companies;

- until 04/30/2020 - individual entrepreneurs.

Let's consider the order in which the simplified tax system payment order for 2021 is filled out for the “income” object (6%).