Good afternoon, dear readers. The next tax year has ended, according to the results of which the company reports for all its employees to the Federal Tax Service.

And today we will talk about 2-NDFL certificates (When there are more than 25 employees, certificates are provided electronically. If there are less than 25 people, you can submit them on paper), more precisely, about the mistakes and mistakes made when submitting these certificates.

Today you will learn:

- What are the mistakes when submitting 2-NDFL;

- What are the fines for these violations?

- How can they be avoided?

We work on new forms

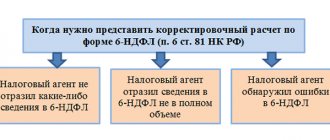

From 2021, income reporting will be submitted using new forms. The forms are now filled out in two versions: the first is suitable only for the Federal Tax Service of Russia, and the second can be prepared at the request of the employee.

Report forms differ significantly from each other. It is important not to confuse the formats. If you send an outdated or incorrect format to the inspectorate, the tax authorities simply will not accept the report. Penalties will be applied to the violating taxpayer. So pay attention to how to adjust 2-personal income tax for 2021 in accordance with the requirements of the Federal Tax Service.

Current forms are approved by Order of the Federal Tax Service No. ММВ-7-11/ [email protected] dated 10/02/2018. Fill out the new reporting with information about employee income accrued for 2021. If an organization needs to submit adjustment reports for earlier dates, then fill out the forms corresponding to the reporting periods.

Rules on how to submit an adjustment for 2-NDFL

Remember that the 2-NDFL certificate number does not need to be changed when making adjustments. Because the “Adjustment number” in 2-NDFL and the number of the reporting certificate itself are completely different details.

Another nuance on how to correctly submit the 2-NDFL adjustment is its form. Use the form you used to submit your initial income certificate (KND number and the corresponding approval order from the Federal Tax Service).

Understanding how to correctly submit a 2-NDFL adjustment means correctly forming its content. So: in the certificate, include all the indicators - both those that were corrected and those that were correct and remained untouched.

In the header, do not forget to indicate the new date of drawing up the individual’s income certificate.

According to Section II of the Procedure for filling out the certificate, the sign of adjustment in the 2-NDFL certificate is given according to the principle of serial numbers - “01”, “02”, etc.

Thus, the adjustment number in the 2-NDFL certificate in 2021 can take values from “01” to “98”.

Of course, the adjusted 2-NDFL sample is no different in appearance from a regular income certificate for an individual with the index “00”. In it you do not cross out anything or mark it separately in order to draw the attention of tax authorities to the changes made. At the same time, in order not to confuse the Federal Tax Service, it recommends drawing up a cover note in which you name the details of the 2-NDFL certificate that you have corrected.

Fill out sections 1 – 5 of the corrective income certificate in the same order as the primary 2-NDFL.

Since 2021, it has become clear how to submit 2-NDFL adjustments to successors of tax agents. Exactly according to the same rules as listed above. The corresponding addition to the law was made by order of the Federal Tax Service dated January 17, 2018 No. ММВ-7-11/19.

Also see “Certificate 2-NDFL: sample of filling out the new form from 2021.”

Filling Features

To avoid a fine, check the income tax return forms you have already submitted, and if you find any inaccuracies in them, submit a corrected return. Even if there is an inaccuracy in one certificate, it will have to be corrected. Otherwise, the employer faces a fine of 500 rubles.

Consider the specifics of how to submit the 2-NDFL adjustment for 2019 for one employee. If the personal data of employees, for example, last name or passport number and series, has changed after submitting information, clarification is not required (letter of the Federal Tax Service No. GD-4-11 / [email protected] dated March 27, 2018). In addition, the employee is recommended to issue a report on income and income tax with new passport details, and this is not a violation, despite the fact that you reported to the tax authority using old information (letter of the Federal Tax Service No. GD-4-11 / [email protected] dated 03/27/2018).

The updated reporting of the employee's income is submitted in the form that was in force in the period for which the error was discovered. The special adjustment number in the 2-NDFL certificate “99” means that the document submitted for this individual is cancelled. That is, adjustment 99 in the 2-NDFL certificate does not clarify, but completely cancels the data on an individual, for example, in the case of an erroneous filling out of a document for a person who did not receive income in the reporting year. In this case, in the cancellation certificate, the information in sections 1 and 2 is repeated from the one already submitted, and sections 3, 4 and 5 are not filled out.

The procedure for filling out and the form for income received in 2021 by individuals was approved by Order of the Federal Tax Service No. ММВ-7-11/ [email protected] dated 10/02/2018.

Types of errors in the 2-NDFL certificate

The first option is being late.

If the first of April has passed and you have not submitted certificates to the tax office (they are accepted by the Federal Tax Service according to the attached register), prepare to pay a fine.

If your certificates do not pass the entrance control for any reason (whether in paper or electronic form you report to the tax office) and there is no time left to correct the documents on time, then these 2-NDFL certificates will also be considered not provided.

During incoming control, the completion of all required fields of the document is checked.

Example: a street is missing from the address - the certificate will definitely not be accepted, however, if the employee’s TIN is missing, then this will not be a violation during entry control.

Based on the results of the inspection, a protocol is issued or sent through the electronic document management operator, indicating the not accepted certificates and errors found in them.

You can calculate the total amount of the fine for the first version of violations as follows: (“Number of certificates not submitted” + “Number of not accepted”) * 200 rubles for each form.

The second option is, in fact, errors.

For example:

- There is a TIN, but for another person;

- A letter is missing from the surname;

- The street was renamed last year;

- Errors in rounding of income received, etc.

The 2-NDFL certificates accepted from you (entrepreneurs) are then subjected to a second (office) inspection. Tax inspectors check documents against databases to identify all inaccuracies and violations. Previously, it was enough to simply submit corrected documents. Since 2021, an accountant’s mistake began to cost 500 rubles for each certificate.

Example: The program has incorrect rounding configured. You have twenty-five employees. The fine will be twelve thousand five hundred rubles (25*500).

How to prepare an adjustment

To make an adjustment means to fill out the information for an individual again, but with the correct information and details. Algorithm for submitting a 2-NDFL adjustment for 2021 in five steps:

- In field No. - the number of the submitted certificate, which contains inaccuracies.

- In the field “from__.___.__” - the date of registration of the clarifying information.

- In the “Adjustment number” field - a number starting with 01. For example, 03 means that you are submitting a third corrected form for this employee.

- Indicators (information) in which an error was made in the previously provided forms should now be indicated correctly.

- Indicators (information) that did not contain errors in the previously provided certificates should be duplicated.

Canceling clarifying certificates

From the name itself it is clear that the meaning of this certificate is to cancel the one submitted earlier (the initial certificate 2-NDFL was simply superfluous). The updated certificate form now includes the “adjustment number” field.

When submitting the initial certificate, “00” is entered in the field. When submitting a cancellation certificate “99”. Next, you need to fill out section 1 “Data about the tax agent” and section 2 “Data about the individual - recipient of the income.” The remaining help topics are left blank

Example: for an employee who works in a separate division, the accounting department reported at the place of registration of the head office. At the same time, tax accruals and payments were made correctly, i.e. to the tax office of a separate division. It is necessary to send the cancellation certificate to the Federal Tax Service Inspectorate of the head office and the initial one to the tax inspector of the separate division (note that if the certificate for the separate division is submitted later than April 1, you will have to pay for the delay).

How to check reporting information

Before sending the corrected information to the tax office, you need to check the information. How to correctly check a report, what to compare information with - consider important recommendations:

- Information on income and deductions must match the organization’s accounting data. Check the information on the income tax certificate with the employee’s personal card. Also monitor the indicators of payroll records and wage journals. The information must match the monthly accounting data.

- If, in addition to wages and remuneration for labor, other types of income are accrued to employees, then it is necessary to include information in the 2-NDFL adjustment. Example: an organization pays dividends to subordinates, distributes profits, or pays for health packages. Include such income in the 2-NDFL certificate according to the appropriate income code.

- Different tax rates apply to different categories of income. For each rate you will have to draw up a separate 2-NDFL certificate.

- Similar rules apply to the adjustment attribute field in the 2-NDFL certificate. If the tax is withheld by the employer on time, then indicator “1” is indicated. If it is impossible to withhold income tax, then sign “2” is indicated in the 2-NDFL certificate.

- The deadlines for submitting reports for various characteristics of a taxpayer have been equalized. Report by March 1 of the year following the reporting year. If the due date falls on a weekend, submit the form on the first working day.

IMPORTANT!

Deductions and benefits for personal income tax are documented. Applications, certificates of study, birth certificates and other papers must be collected annually from subordinates. Based on the received certificates, adjust the benefits and deductions provided.

Fined without camera

So, certificates in form 2-NDFL have been submitted. And since they are neither declarations nor calculations, these certificates will not be subject to desk verification. According to clause 1 of Article 88 of the Tax Code of the Russian Federation, a desk audit is carried out on the basis of tax returns (calculations) and documents submitted by the taxpayer, as well as other documents on the activities of the taxpayer available to the Federal Tax Service. The 2-NDFL certificate is neither a declaration nor a calculation. The Federal Antimonopoly Service of the North-Western District, in Resolution No. A66-4514/2008 dated May 12, 2009, confirms this conclusion, adding that the certificate in Form 2-NDFL contains only information about income paid to individuals and the amounts of accrued and withheld tax.

However, the fact that 2-NDFL certificates are not subject to desk verification does not guarantee the absence of consequences as a result of submitting certificates with erroneous information. After all, clause 1 of Article 126.1 of the Tax Code of the Russian Federation states that for the presentation by a tax agent of documents containing false information, a fine of 500 rubles is imposed. for each document containing an error. At the same time, it does not follow from the Tax Code of the Russian Federation that this fine will be imposed only based on the results of a desk audit. Thus, 2-NDFL certificates will still come under the close attention of tax authorities. And if they discover errors, the company faces sanctions.

By the way, please note that the penalty for submitting a certificate with a “defect” is much harsher than for failure to submit it.

How to make a 2-NDFL adjustment in “Taxpayer”

The described algorithm of actions when entering clarifying information is the same both for providing corrections on paper and using any software products. This is 1C, online services, free software of the Federal Tax Service “Taxpayer Legal Entity”. The modern 2-personal income tax adjustment for 2021 is presented in any way of the taxpayer’s choice.

Specialized services offer detailed instructions on how to correct an error in 2-NDFL for 2021, tips on filling out reporting and adjustment forms. Carefully study the recommendations for using the services.

It is permissible to send corrections to certificates through the taxpayer’s personal account. This requires registration of the company on the official portal of the Federal Tax Service. Submission of reports requires an electronic signature.

Responsibility

According to the law, the fine for adjusting 2-personal income tax is 500 rubles for each certificate (Article 126.1 of the Tax Code of the Russian Federation). It does not threaten you if you manage to find the error before the Federal Tax Service and submit the correct version of the certificate. But if you do it ahead of schedule - before 04/02/2018 - it will not save you from a fine! (see letter of the Ministry of Finance dated June 30, 2016 No. 03-04-06/38424).

Section 2 of the income certificate with information about the individual: how to make a 2-NDFL adjustment in “Taxpayer” if the personal information, along with the change of passport, was updated after the certificates were submitted to the Federal Tax Service? It's simple: this is not considered an error. It is also not necessary to send the correction.

And vice versa: if at the time of filling out the corrective certificate 2-NDFL for previous tax periods, a person’s personal data has changed, Section 2 must be filled out taking into account these changes (letter of the Federal Tax Service dated March 27, 2018 N GD-4-11/5667).

Read also

24.10.2018

The procedure for correcting errors when calculating personal income tax for an employer

Standard tax deductions can be carried forward to the next month, but only within the same year

Author: Tatyana Sufiyanova (tax and duties consultant)

Every company or individual entrepreneur is faced with the calculation of personal income tax. Especially if they act as tax agents (employers). And here you can often encounter errors that we want to tell you about.

The first mistake is when an organization or individual entrepreneur relieved itself of the obligation to transfer personal income tax and agreed with the employee himself (another individual) so that the tax was paid directly by the citizens themselves. For example, concluding a lease agreement with an individual, performing work (services) for a company by an individual. When concluding contracts of a civil law nature, in the text of the contract itself you can find a condition about who assumes the obligation to pay personal income tax to the budget.

It is worth immediately paying attention to the fact that this is a gross mistake. The agreement does not need to describe the procedure for paying personal income tax. This is the direct responsibility of the company (IP) if they enter into an agreement with an individual. Even if the parties wrote about this in the agreement, this is not a basis for exempting the company (IP) from the status of a tax agent for personal income tax.

As the Federal Tax Service writes in its letter dated January 12, 2015 No. BS-3-11/14, according to paragraphs 1 and 2 of Art. 226 of the Tax Code of the Russian Federation, tax agents are recognized as Russian organizations, individual entrepreneurs, notaries engaged in private practice, lawyers who have established law offices, as well as separate divisions of foreign organizations in the Russian Federation that are the source of payment of income to the taxpayer, with the exception of income in respect of which calculation and payment taxes are carried out in accordance with Articles 214.3, 214.4, 214.5, 214.6, 226.1, 227, 227.1 and 228 of the Tax Code of the Russian Federation.

Tax agents are required to withhold the accrued tax amount directly from the taxpayer’s income upon actual payment. At the same time, the Tax Code does not provide for specific features of the tax agent’s performance of his duties when paying income to the taxpayer based on a court decision.

The Ministry of Finance also considered a similar issue and noted that a Russian organization that pays rent to an individual for residential premises rented from him is recognized as a tax agent in relation to such income of the individual and, accordingly, must perform the duties of calculating, withholding and transferring tax on the amount to the budget. income of individuals in the manner provided for in Art. 226 Tax Code of the Russian Federation.

The second mistake is when the employer calculates the amount of the standard child tax deduction in proportion to the days worked in the month. For example, an employee was registered for work on May 15, 2021, he immediately presented all the documents to provide him with a standard child deduction for one child in the amount of 1,400 rubles. The employer's accountant provided a deduction for May 2021 not in the amount of 1,400 rubles, but calculated it in proportion to the time worked in May. This is mistake.

This is interesting: Deadline for returning personal income tax according to the 3rd personal income tax declaration

Based on sub. 4 paragraphs 1 art. 218 of the Tax Code of the Russian Federation, the standard deduction for the first child is provided in the amount of 1,400 rubles per month and this is a fixed amount. You cannot divide or otherwise calculate the standard deduction for the month. Even if an employee works one working day in a month, he is entitled to a deduction of 1,400 rubles.

The fourth mistake is when the employer's accounting department, at the request or at the request of the employee himself, returns tax for those periods that could not have been deducted. Let's give this example: in April 2021, a company employee brought to work a tax notice for her employer to provide her with a property deduction (she bought an apartment in January 2017). And at work, at the request of the employee, they paid the previously withheld personal income tax for the period from January to March 2021. This is a big mistake.

The procedure for returning to the taxpayer the amounts of personal income tax overly withheld by the tax agent from the taxpayer’s income is established by Art. 231 Tax Code of the Russian Federation.

Refund of tax amounts withheld by the tax agent before receiving from the taxpayer a written application for the provision of property tax deductions and confirmation by the tax authority of the taxpayer’s right to receive these deductions on the basis of Art. 231 of the Tax Code of the Russian Federation is impossible, since the amounts of tax lawfully withheld by the tax agent cannot be qualified as excessively withheld.

Fifth mistake , when personal income tax was transferred by mistake for one or another employee. And after discovering this error, the accountant made amendments the following month. This cannot be done, it was necessary to carry out correct calculations in future periods, and for the amount of overpaid personal income tax it was necessary to submit a refund application to the Federal Tax Service. As advised by the Federal Tax Service of Russia in letter dated 02/06/2017 No. GD-4-8/ [email protected] , clause 9 of Art. 226 of the Tax Code of the Russian Federation establishes that payment of tax at the expense of tax agents is not allowed. Consequently, the transfer to the budget of an amount exceeding the amount of personal income tax actually withheld from the income of individuals does not constitute payment of personal income tax.

In this case, the tax agent has the right to contact the tax authority with an application for the return to the current account of an amount that is not personal income tax and was mistakenly transferred to the budget system of the Russian Federation.

The tax authority, if the specified tax agent has no debt on other federal taxes, shall refund the overpaid amount that is not personal income tax, in the manner established by Art. 78 Tax Code of the Russian Federation.

It should be taken into account that confirmation of the fact of erroneous transfer of amounts according to personal income tax payment details, as well as confirmation of the fact of excessive withholding and transfer of personal income tax, is made on the basis of an extract from the tax accounting register for the corresponding tax period and payment documents in accordance with paragraph. 8 clause 1 art. 231 of the Tax Code of the Russian Federation, and the return to the organization’s current account is carried out taking into account the provisions of paragraph. 2 clause 6 art. 78 Tax Code of the Russian Federation.

In addition, it is possible to offset such erroneously transferred amounts using the personal income tax payment details to pay off debts on taxes of the corresponding type, as well as against future payments for other taxes of the corresponding type.

The sixth mistake is when the accountant transfers standard deductions for the child to the next tax period (year). Standard tax deductions can be carried forward to the next month, but only within the same year.

But if we had such a situation in the period from December 2016 to January 2021, then in this case the amount of unaccounted standard deductions from December would in no way be included in the calculation of wages for January 2021.

Reporting with incorrect data

If the Federal Tax Service Inspectorate finds errors in the personal data of employees in a timely submitted calculation of insurance premiums, the DAM will be refused acceptance and it will be considered not submitted. In this case, the tax authority, no later than the day following the day of submission of the electronic calculation (10 days following the day of receipt of the calculation in paper form), is obliged to notify the payer of the non-acceptance of the document (letter of the Federal Tax Service dated December 21, 2021 No. GD-4-11 / [email protected] ). When receiving from the Federal Tax Service a notice of refusal to accept the DAM or a request to provide explanations or make corrections to the DAM calculation, you must retake it.

Desk audits in relation to 2-personal income tax are not carried out (Article 88 of the Tax Code of the Russian Federation). If errors are detected, the Federal Tax Service must notify the tax agent in writing and indicate exactly what inaccuracies were identified (letter of the Federal Tax Service dated August 9, 2021 No. GD-4-11/14515).

Article 126.1 of the Tax Code of the Russian Federation provides for liability for tax agents for providing personal income tax reports with false information. According to this norm, a company can be fined 500 rubles for each document submitted that contains false information (letter of the Ministry of Finance dated June 30, 2016 No. 03-04-06/38424). Moreover, the list of data recognized as unreliable is not established by law.

The Federal Tax Service considers any completed details that do not correspond to reality to be unreliable information. In particular, incorrect reflection in 2-NDFL certificates of personal data of individuals: full name, tax identification number, passport data, date of birth, other information, incorrect reflection of income and deduction codes, incorrect reflection of amounts, including due to arithmetic, technical errors, typos, even if the error led to an overpayment, non-calculation or incomplete calculation of personal income tax, any other errors (letter of the Ministry of Finance of Russia dated September 6, 2021 No. BS-4-11 / [ email protected] , dated April 21, 2021 No. 03-04-06/23193, Federal Tax Service of Russia, No. BS-3-11/ [email protected] , dated August 9, 2021 No. GD-4-11/14515).

A fine cannot be avoided even if the organization itself corrects all the shortcomings before April 1, but only after the Federal Tax Service has notified the tax agent about the errors.

It should be taken into account that for the use of false passport data in 2-NDFL, a tax agent can be held accountable only if, due to an inaccuracy, it is impossible to identify the individual indicated in the 2-NDFL certificate - the recipient of income for tax control purposes and this resulted in untimely and (or) incomplete transfer of tax to the budget or led to a violation of the rights of company employees (letter of the Federal Tax Service dated December 9, 2021 No. CA-4-9 / [email protected] ).

note

The Federal Tax Service issued a letter dated December 29, 2021 No. GD-4-11/ [email protected] , in which it recalled the need to reflect current personal data of employees in certificates on Form 2-NDFL and calculations for insurance premiums.

The fact that the false information provided did not lead to non-calculation and (or) incomplete calculation of personal income tax, to adverse consequences for the budget, or violation of the rights of individuals, should be considered as a mitigating circumstance (clause 3 of the letter of the Federal Tax Service of Russia dated August 9, 2021 No. GD- 4-11/14515).

At the same time, the qualification of the actions of a company that made an error in 2-NDFL information depends on the actual circumstances (letter of the Ministry of Finance of Russia dated April 21, 2021 No. 03-04-06/23193). From paragraph 10 of the Procedure for submitting information about employee income to tax authorities, approved by Order of the Federal Tax Service dated September 16, 2011 No. ММВ-7-3 / [email protected] , it follows that when accepting information received on electronic media, it is allowed to adjust the address in accordance with the address used address directory (KLADR). The risks of prosecution in such a situation are minimal.

Please note that it is permissible not to fill out the TIN details in the 2-NDFL certificate if the individual does not have one (Section IV of the Procedure for filling out the 2-NDFL certificate, letter of the Ministry of Finance of Russia dated April 18, 2016 No. 03-04-06/22209, dated 9 March 2021 No. BS-3-11/ [email protected] ). In this case, the certificates will be accepted with a warning that the TIN is not indicated (letter of the Federal Tax Service of Russia dated September 6, 2021 No. BS-4-11 / [email protected] ). If there is a TIN, the field must be filled out.