Formula for calculating the cost of work in progress

- According to P.

63 Regulations on Accounting and Accounting Reports, work in progress (hereinafter referred to as WIP) are products that have not completed all stages of the production cycle, are not properly equipped, have not passed technological tests, or have been rejected by the customer.Thus, the concept of work in progress covers a wide range of products at different stages of production, services or work.

According to paragraphs 56, 97 and 98 of the Methodological Instructions approved by the Ministry of Finance of the Russian Federation of December 28, 2011 No. 119n, work in progress does not include: materials, raw materials and semi-finished products sent to production sites, but not processed, as well as semi-finished products with defects.

WIP can be recorded in primary and auxiliary production, as well as in the activities of service farms.

Accounting

During the reporting period, the cost of finished products that have gone through all stages of production is formed using the following entries:

Debit 20 (23.29) Credit 10 (02, 05, 23, 25, 26, 69, 70):

Costs for production of products (performance of work) are written off

Based on the quantity of products produced, production costs accumulated on Account 20 are written off in the following order:

- to the Debit of Account 43 (Account 90), if the company keeps records based on actual cost indicators;

- to the Debit of Account 43 (Account 90 or Account 40), if the company operates according to standard indicators.

Debit 43 (40, 90) Credit 20:

The cost of finished products delivered to the warehouse is written off

The release of finished products from servicing or auxiliary production is written off from the credit of Accounts 23 or 29. Depending on the target audience, products can be included in the Debit of accounts for accounting for production costs or financial results.

The cost of remaining consumables (raw materials, semi-finished products) not included in the cost of finished products (balance 20, 23 and 29 at the end of the reporting period) is the cost of work in progress.

Ways to evaluate work in progress

WIP assessment can proceed as follows:

- at the cost of consumables, raw materials and semi-finished products;

- by items of direct costs;

- according to the actual or standard cost of production.

According to Clause 7 of PBU 1/2008, the method used to evaluate work in progress must be fixed in the accounting policy of the enterprise for the convenience of accounting.

WIP assessment

Estimation based on the cost of consumables

If a production organization evaluates work in progress at the cost of consumables (raw materials, semi-finished products, purchased finished products and homogeneous mass), then the cost of the balances is determined by the following formula:

SRM × FO WIP = CO WIP, where

CPM - the cost of consumables, raw materials, semi-finished products, purchased finished products and homogeneous mass transferred to production areas for further processing

FO WIP – actual balances of work in progress, expressed in quantitative terms (g, kg, V, m). The amount of WIP balances can be determined at the end of the month based on the results of the inventory or on the basis of the primary data of the reporting documentation (Form No. MX-15).

CO WIP – the cost of work in progress balances.

An example of determining WIP balances:

A certain company produces A4 paper. Cost accounting is carried out using Account 40, since the accounting policy of this enterprise provides for the assessment of work in progress at the cost of consumables.

In May, 30 m3 of wood was supplied for paper production, the cost of which was 120,000 rubles excluding VAT. The cost of 1 m/cube of wood is 4,000 ₽. As a result of the inventory as of May 31, wood residues in the amount of 4 m/cub. were identified at the production sites.

Direct production costs amounted to 230,711 ₽:

- 120,000 ₽ — cost of raw materials;

- 86,000 ₽ — wages of production workshop employees;

- 24,711 ₽ - the amount of contributions to the funds of compulsory pension, medical social and other types of insurance.

147,000 ₽ - the amount of indirect expenses of the enterprise for the month.

The total amount of the company's expenses for the month of May was: 230,711 ₽ + 147,000 ₽ = 377,711 ₽. Following from these calculations, the following entries must be made in the accounting records of the enterprise:

Debit 20 Credit 10 (25, 26, 68, 69, 70…)

— 377,711 ₽ costs for the production of office paper are taken into account

Debit 40 Credit 20

— 361,711 ₽ (120,000 ₽ ÷ 30 m/cube ×26 m/cube +86,000 ₽ +24,711 ₽ + 147,000 ₽ = 361,711 ₽) — actual cost of finished products

Thus, the cost of WIP balances will be calculated by the difference between direct costs and actual cost: 377,711 ₽ - 361,711 ₽ = 16,000 ₽

This difference is the balance on Account 20 at the end of May.

Estimation based on direct costs

When applying the method of assessing work in progress using direct cost items, direct costs are distributed between the balances of account 20 and finished products.

Assessment based on actual and standard costs

When applying the method of assessing work in progress at actual or standard cost, the volume of work in progress is assessed based on conditional indicators that the enterprise sets independently at the stage of financial planning. As an example, you can use in the quantitative value of finished products a value equivalent to the number of finished products for the previous reporting period.

In order to calculate the equivalent number of finished products, it is necessary to know the value of the finished product coefficient at each stage of the production cycle, as well as the coefficient of non-processed raw materials (or partially processed) in physical units of measurement. To calculate the amount of remaining raw materials and partially finished products, use form No. МХ-19 approved by Rostatat Resolution No. 66 dated August 9, 1999, or form M-17 approved by Roskomstat of Russia Resolution No. 71a dated October 30, 1997.

The readiness coefficient of products that have passed the next stages of the production process is calculated on an accrual basis, taking into account the coefficient for previous stages of production. The value of these coefficients is established by the technological service bodies of the enterprise.

To determine the volume of WIP equivalent to the amount of finished products at the end of the month, it is necessary to calculate the number of finished products after each stage of production. The calculation can be made using the following formulas:

- OS 1× KeGP 1 = EC GP 1, where

OS 1 - remains of raw materials not processed, or partially processed at the first stage of the production process in natural measurements

KeGP 1 - product readiness factor at the first stage of the production cycle

EC GP 1 - equivalent amount of finished products at the first stage of the production cycle

- OS 2× KeGP 2 =EK GP 2, where

OS 2 - remnants of raw materials not processed, or partially processed at the second stage of the production process in natural measurements

KeGP 2 - product readiness factor at the second stage of the production cycle

EC GP 2 - equivalent amount of finished products at the second stage of the production cycle

- EC GP = EC GP 1 + EC GP 2 +…, where

EC GP 1 - equivalent amount of finished products at the first stage of the production cycle

EC GP 2 - equivalent amount of finished products at the second stage of the production cycle

EC GP - equivalent quantity of finished products at the end of the month

An example of determining WIP balances based on actual costs

The company is engaged in sewing mink coats. At the beginning of the month of June, no production balances were recorded. The accounting policy of the enterprise provides a method for assessing production by calculating the actual costs of providing it. All general business expenses are written off to Account 20 at the end of the month.

The chief technologist of the enterprise approved the size of the product (fur coat) readiness factor after each stage of the production cycle:

- processing and processing of raw materials (skins) – 30%;

- local cutting and sewing – 70%;

- laser processing and production of the finished product – 100%.

In June, 650 skins were sent to production sites with a total cost of 650,000 rubles (excluding VAT). According to the standard technological indicators, it is planned to sew 65 fur coats from this amount of raw materials, at the rate of 10 pieces of skins per 1 unit of product. As of June 30, 49 units of finished products were transferred to the warehouse.

Direct production costs were:

- 650,000 ₽ — cost of raw materials;

- 128,000 ₽ — wages of production employees, taking into account insurance contributions (pension, medical, social and other types of insurance);

- 37,000 ₽ - the amount of production costs;

- 44,000 ₽ - the amount of general business expenses.

In June, the accounting department made the following entries:

- Debit 20 Credit 10: 650,000 ₽ - materials for production support were written off.

- Debit 20 Credit 70 (69): 128,000 ₽ wages of production cycle employees are written off, taking into account insurance contributions (pension, medical, social and other types of insurance).

- Debit 20 Credit 25: 37,000 ₽ general production expenses are written off.

- Debit 20 Credit 26: 44,000 ₽ general business expenses are written off.

As of June 30, the following remains of partially processed raw materials were identified:

- at the stage of processing and dressing of skins - 30 pieces;

- at the stage of pattern cutting and sewing - 80 pieces.

Taking into account these indicators, the accountant calculated the equivalent amount of finished products in the balances at each stage of production. The volume of work in progress was:

- at the processing and dressing stage: 30 pcs ÷ 10 pcs/unit × 20% = 0.6 units;

- at the cutting and sewing stage: 80 pcs ÷ 10 pcs/unit × 80% = 6.4 units.

The volume of work in progress at the end of June is: 0.6 units + 6.4 units = 7 units.

Total production for June: 49 units + 7 units = 56 units including work in progress.

The total production costs are: 650,000 ₽ + 128,000 ₽ + 37,000 ₽ + 44,000 ₽ = 859,000 ₽

The actual cost of finished products that were transferred to the warehouse is reflected by the posting: Debit 43 Credit 20,859,000 ₽ ÷ 56 units × 49 units = 751,625 ₽ the actual cost of finished products for June is written off

The value of WIP balances at the end of the month (debit balance on Account 20 as of June 30 is: 859,000 ₽ - 751,625 ₽ = 107,375 ₽

Evaluation of work in progress when providing services

The volume of work in progress in accounting (Debit 20 “Main production”) is formed on the last day of the reporting period (usually a month). According to Clause 2, Art. 720, 783 of the Civil Code of the Russian Federation, the service is considered completed if a mutual agreement is concluded between the customer and the contractor, upon signing of which the customer has no complaints about the quality of the service provided to him

If the service is provided during one reporting period, and before its end the act between the parties to the transaction is signed, then the work in progress is excluded, since all costs incurred by the contractor are included in the financial result at the time when the proceeds from the sale of the service are recognized by the accounting department as profit. If the provision of a service lasts more than a month, then revenue recognition can occur in two ways:

- As a particular service is provided (in stages).

- One-time, as the service is completed and the contract expires.

In the first case, there cannot be any balances of work in progress, since all expenses for ensuring the provision of services during the reporting month are written off from Account 20 in the manner specified in the accounting policy of the enterprise:

- under account 46 “Completed stages of work in progress”;

- without using account 46 “Completed stages of work in progress.”

In the second case, all expenses incurred by the contractor for the provision of services will be written off to Account 90 “Sales” after the parties to the transaction have signed a mutual agreement on the provision of services properly. Until then, the amount of direct costs will accumulate on Account 20 and form the cost of the WIP.

According to Clause 2, Art. 318 of the Tax Code of the Russian Federation, regardless of the duration of the services provided, all costs incurred to ensure the provision of services have the right not to be allocated to work in progress.

Source: https://glavbuhx.ru/otchetnost/buhgalterskaya-otchetnost/formula-rascheta-sebestoimosti-nezavershennogo-proizvodstva.html

The standard for work in progress in monetary terms is found using the formula [p.294] It is necessary to achieve efficient use of working capital at each of the three stages of the procurement, production and sales circuit.

Therefore, along with general turnover indicators, it is advisable to determine specific control indicators for the procurement stage - the standard for industrial inventories, for the production stage - the standard for work in progress, for the sales stage - the standard for finished products in the warehouse. [p.212] Consequently, for this case, the work in progress standard is 80 thousand rubles. is illegal and production should be organized in the form of piece production, not serial production. [p.68]

NNP - work in progress standard [p.74]

Determine the work in progress standard in monetary terms based on the following data. A machine-building plant produces one product in 5 days at a quarterly cost of 80 thousand rubles, another product in 3 days at a cost of 60 thousand rubles. and the third - in 12 days at a cost of 55 thousand rubles. [p.100]

We calculated the standard based on the entire amount of production costs. However, many factories with a long production cycle do not immediately involve the entire mass of auxiliary and other materials into it. The most expensive and labor-intensive processes do not occur immediately. As a result, production costs increase unevenly. Having studied their dynamics, it is necessary to determine the coefficient of increase in costs and, using it, establish a standard for work in progress I according to the formula [p.240]

The standard for work in progress (in days) D in the main production is determined by the formula [p.180]

The standard for work in progress (in days) in auxiliary workshops can be determined in aggregate based on the analysis of reporting data for a number of previous periods [p.180]

Work in progress standard 180 [p.323]

With a long production cycle, the work in progress standard is absolutely necessary. It has not only organizational but also economic significance. Compliance with this standard is important not only for ensuring high production efficiency, but also for the formation of working capital of the enterprise. [p.90]

Standard batch sizes Frequency of repetition in production Duration of the production cycle Standard work in progress + 1 1 [p.396]

The standard for work in progress will be Yn = 4 5 x x 0.8 = 16 million rubles. [p.183]

An important part of the regulated funds is work in progress, the value of which primarily depends on the duration of production of products (production cycle) and the degree of increase in costs. The standard for work in progress is established based on the average daily output, the duration of the production cycle and the cost of production. The longer the production [p.64]

In the balance sheet under consideration, the standard for work in progress is maintained, but its share in the normalized funds is lower, which is mainly due to the increase in stocks of raw materials, materials and finished products. [p.66]

Work in progress at the end of the month is periodically (sometimes once a quarter) calculated based on actual availability (using inventory and standard cost data). Product output is also assessed at standard cost. Therefore, the work in progress standard at the beginning of the month plus the costs of the reporting month minus production and write-offs must always be equal to the work in progress at the standard cost at the end of the month. Such a coincidence of the theoretically derived residual with the actual data should be considered normal. However, there are often discrepancies among enterprises. If we exclude from the discrepancies the shortages and surpluses identified by the inventory of work in progress, then discrepancies will remain due to incorrect accounting of deviations, including incorrect documentation of deviations (for example, the replacement of materials was not properly documented), material was issued for correction of defects without proper assessment in the document, orders were issued for work that was practically not carried out (postscripts), etc. [p.352]

Actual expenses for the maintenance and operation of equipment, shop and general plant expenses are within the approved limits, but there are deviations for certain types of expenses (see p. 110). The actual cost of work in progress balances is reflected in the balance sheet. In our example, the balance of work in progress (balance on the Main production account) as of 01.02 is 77,721 rubles. The balance sheet also reflects the standard for work in progress (required reserve). Let’s say that the standard for unfinished production for a merger is set at 100,000 rubles. In this case, the actual balances will be lower than the standard balances by 22,279 rubles. (100000—77721). [p.116]

The standard for work in progress will be 16 million rubles, i.e. [p.260]

Task 4. Determine the coefficient of increase in costs and the standard of work in progress, if the total value of all costs ZP is 100 thousand rubles, the initial daily costs ZP are 70 thousand rubles. the remaining costs are carried out uniformly, the duration of the production cycle is 6 days. [p.266]

The work in progress standard (WIP) is calculated using the formula [p.231]

The standard for work in progress (based on cost and material costs) is 0.5 (4857 + 1700) 90 x 15 = 546.4 thousand rubles. [p.89]

Standardized working capital includes those types of material assets and costs that are necessary to ensure the uninterrupted operation of the enterprise - inventories, work in progress and self-made semi-finished products, deferred expenses and finished products on salaries (in containers) of enterprises. For each of these groups of working capital, an upper limit for fixed inventories (costs) is established. or working capital standard, i.e. the minimum amount of working capital required by the enterprise. [p.179]

Unfinished production. The standard for work in progress I can be calculated using the following formula [p.209]

The regulated funds are the enterprise's own funds. They are intended to create the necessary reserves in the plant's warehouses, create a stock of semi-finished products and work in progress in production shops, as well as invest in expenses for future years. The standard for normalized working capital is differentiated by year of the five-year plan. Every year, when developing a technical industrial financial plan, the amounts of own turnover are specified [p.323]

As can be seen from the balance shown in table. VI.3, work in progress amounted to 240 thousand rubles at the beginning of the month. and it was less than the standard by 8 thousand rubles. Within a month it increased to 262 thousand rubles. and exceeded the standard by 14 thousand rubles. [p.170]

Each enterprise is provided with its own working capital, which it needs to fulfill the established plan. The standard of own working capital is calculated based on the cost of the minimum required reserves of raw materials, basic and auxiliary materials, fuel, spare parts, low-value and wearable items, containers, work in progress, semi-finished and finished products and the amount of expenses of future reporting periods. The additional need for working capital, arising, as will be shown below, from the normal settlement relationships of the enterprise, is covered by loans from the State Bank. In addition, the State Bank issues loans to enterprises to cover the need for funds necessary to create seasonal reserves of raw materials, fuel and for other temporary needs, if these needs are due to the normal course of production and are not caused by mismanagement. State Bank loans are strictly targeted, urgent and [p.245]

Each enterprise is provided with its own working capital, which it needs to fulfill the established plan. The standard of own working capital is calculated based on the cost of the minimum required reserves of raw materials, basic and auxiliary materials, fuel, spare parts, low-value and wearable items, containers, work in progress, semi-finished and finished products and the amount of expenses of future reporting periods. The additional need for working capital arising from the normal settlement relationships of the enterprise is covered by bank loans. In addition, the bank issues pre- [p.271]

The standard of working capital as a whole for the element Work in progress is equal to the sum of the standards for all n products [p.56]

The standard for work in progress is calculated based on technological data for individual installations. Due to the fact that the vast majority of them are equipped with continuous operation equipment, the duration of the production cycle is short. For this reason, the volume of work in progress is also insignificant. On average, the standard for this article is 1.2-1.5% of the cost of commercial products of the enterprise. [p.265]

The increase in the standards of own working capital is included in the amount determined by the calculation. In the reporting year, the standard was 6,370 thousand rubles. According to the plan, production volume increases by 3.6%; accordingly, the size of stocks of raw materials, auxiliary materials and semi-finished products, work in progress, containers, and finished products should increase in proportion to production volume. The standard was equal to 5,000 thousand rubles, and for the planned year it will increase by 5,000,000 -0.036 = = 180,000 rubles. [p.273]

The rate of working capital is established for each item or group of material resources in days of average daily consumption or in the form of material and monetary unit costs per employee, team (tools, equipment, special clothing, etc.) the percentage of replacement of parts and assemblies during repairs, the rate of increase in costs by work in progress. Based on the norms, the planned amount of standardized working capital, called the standard, is determined. With the established norm, the standard is found as the product of the one-day consumption of material resources in monetary terms by the stock norm in days. The standard is established when drawing up a plan for the financial and economic activities of an enterprise (association) at the end of the planned period for individual items of working capital, taking into account the need for these funds for the production of a certain type of product (work). [p.190]

The basic principle of rationing working capital is linking standards with technical and economic conditions of production. In the new economic conditions, the rights of enterprises (associations) in the field of rationing working capital have been significantly expanded. The enterprise (association) is approved only by the general standard of working capital. The standards for own working capital by type, their increase or decrease are determined and established by the enterprises (associations) themselves and are not subject to approval by higher organizations. In the new economic conditions, the necessary prerequisites are created for the development of scientifically based standards of working capital and the reduction of excess inventories of inventories at enterprises (in associations). To strengthen economic accounting at enterprises (associations), current private standards should be differentiated by individual types of raw materials, basic and auxiliary materials, work in progress, finished products, etc. [p.191]

Then the working capital standard for work in progress [p.215]

From the data in table. 110 it can be seen that in fact the standardized working capital is generally reduced compared to the standard. The reduction was caused mainly by the items work in progress and semi-finished products of own production (RUB 1,046 thousand) and spare parts for repairs (RUB 112 thousand). Both of these are apparently associated with an improvement in the organization of production or with an overestimation of the standard under the first article. Specific reasons can be established through a more detailed analysis of standard calculations. At the same time, for a number of items there is an excess of the standard. The excess is especially large for raw materials - 575 thousand rubles, auxiliary materials - 139 thousand rubles. and finished products - 60 thousand rubles. All this could be caused by an increase in production volume due to exceeding the production plan. Therefore, before comparison, the direct cost standard must be recalculated to the percentage of exceeding the plan. Let's assume that the production plan is 105% fulfilled. Then the standard for raw materials should be (7339-105) = 7700 thousand rubles, for auxiliary materials - 1030 thousand rubles, for finished products - 605 thousand rubles. Comparison of these figures with the actual availability of working capital shows that the norm is [p.211]

The contractor sets a standard for work in progress (approximately 10% of the annual volume of contract work), on top of this - a bank loan, but within the limits of construction and installation work established for each construction project by year of the five-year plan. The loan is provided to pay for construction and installation work and to pay for incoming equipment. [p.200]

In this example, the total amount of quarterly costs for the production of three types of products is 210 thousand rubles, and therefore, in one day 2.33 thousand pyi6. and the work in progress standard in monetary terms will be equal to (210 thousand rubles x 6.57 days)/90 days = 15.3 thousand rubles. [p.240]

N0b.s = N r.3 + Nnp + Ngp + NrbP, where Nprz is the standard for production inventories Nnp is the standard for work in progress Nsh is the standard for inventories of finished products Nrbp is the standard for deferred expenses. [p.161]

Scientific and technical potential 213 Scientific and technical progress 199, 214 Work in progress 56, 92 New economic conditions 174 Normative planning method 74 Working capital standard 52, 53, [p.297]

How to correctly calculate the cost of production for work in progress

Accounting for work in progress (WIP) is an important aspect of the activities of any large enterprise. Correct assessment and reflection of work in progress affects not only the calculation of product costs, but also the final indicators of financial reporting.

WIP accounting

The regulations on accounting and reporting classify the following types of products as work in progress:

- products that have not passed all stages (stages) of the technological process;

- incomplete products;

- products that have not passed technical acceptance or testing;

- work not accepted by the customer.

To understand why WIP assessment affects cost calculation, you need to consider its formula:

Cost = WIP (beginning of period) + Costs - WIP (end of period)

When reflecting work in progress in accounting, the following types of estimates are used:

- according to actual costs,

- at actual or planned production cost,

- at the cost of the raw materials used.

You should know that in mass production you can use any of these options, but in single production - only an estimate based on actual costs.

Organizations that provide complex services or produce products in several stages may recognize the sale as one of 2 methods:

- in general as work (service);

- at separate stages.

If the accounting policy of such an organization assumes the second option, then account 46 “Completed stages for work in progress” is applied and the following entries are made:

- Dt 46 Kt 90 - the cost of completed stages is reflected in the accounting;

- Dt 62 Kt 46 - the customer paid for the work (services).

The balances of work in progress at the end of the period in quantitative terms can be established using an inventory or a documentary method. Then the accounting department calculates their value.

As a result, WIP is the balance of accounts 20 “Main production”, 44 “Sales expenses”, as well as 23 “Auxiliary production” and 29 “Service production and facilities”.

If you own a piece of land, you must pay land tax.

Read this article on how to calculate net working capital.

Tax accounting of work in progress

Article 318 of the Tax Code of the Russian Federation states that the organization independently establishes the procedure for distributing direct costs for finished products (GP) and WIP. It is important to take into account that costs must correspond to the products produced. The taxpayer must reflect this procedure for assessing work in progress in the accounting policy and apply it during two tax periods.

In general, the calculation of work in progress occurs in 4 stages :

- calculation of the total amount of expenses;

- calculation of work in progress balances at the end of the period;

- calculation of GP balances at the end of the period;

- calculation of the cost of the remaining products shipped but not paid for.

WIP Inventory

Inventory of work in progress is carried out in accordance with the order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49, which contains methodological recommendations. According to this order, a mandatory inventory may be carried out (when changing the MOL, reorganization, theft or damage, reporting), and the accounting policy may also establish other cases for conducting an inventory.

First of all, the manager must draw up an order that includes the following points:

- description of the property being inspected,

- reasons for carrying out, start and end date,

- members of the commission,

- deadlines for submitting documents to the accounting department.

WIP verification is carried out by weighing, measurements, and calculations. At the same time, the inventory does not include materials and semi-finished products that have not undergone any processing, as well as defects.

The inventory results are reflected in the inventories for each workshop, site, and division. Based on the inventory results, the following entries are made:

| No. | operations | Corresponding accounts | |

| Debit | Credit | ||

| 1 | surpluses are capitalized | 20 | 91.1 |

| 2 | shortage reflected | 94 | 20 |

| 3 | shortages within the norms are written off as production costs | 20 | 94 |

| 4 | shortage in excess of norms is written off to the guilty person | 73.2 | 94 |

| 5 | shortfalls in excess of norms are written off as other expenses | 91.2 | 94 |

Learn all about the methods of calculating depreciation.

What capital investments are is described here.

You can read about the assignment of the right of claim at https://helpacc.ru/buhgalteria/raschety/ustupka-prava-trebovaniya.html.

Work in progress in reporting

In the balance sheet, work in progress is reflected in the second section “Current assets” on line 1210 “Inventories”. Organizations with a long production cycle can reflect work in progress as part of non-current assets.

If the balance of work in progress is significant, they are reflected as a separate line in the balance sheet, and more complete information about work in progress is also disclosed in the annex to the balance sheet and the income statement (for example, the work in progress is detailed by workshop, production, stage).

Source: https://helpacc.ru/buhgalteria/aktivy/uchet-nzp.html

Calculation of work in progress formula

Vladimir Ivanovich Meshcheryakov advised the largest Russian enterprise on the issue of calculating work in progress. Mr. Meshcheryakov decided to share one of the proposed methods with the readers of the “Consultant” magazine.

One of the most difficult areas of accounting work is accounting for finished products. The greatest difficulties arise when calculating the value of work in progress. Moreover, the tax rules for such calculations have recently changed. So, organizations can now install them themselves.

Moreover, firms can themselves determine the list of direct costs. Of course, the shorter it is, the lower the tax cost of finished products and “work in progress”. The larger amounts the company can take into account as indirect expenses and immediately write them off as a reduction in taxable profit.

So, let’s look at how to implement this in practice using an example (the example numbers are conditional).

Closed joint stock company “Rosdor” is engaged in woodworking. Let's assume that the company had no balances of work in progress at the beginning of 2006. According to the accounting policy for tax purposes of the company for 2006, its direct expenses include:

- costs of purchasing raw materials (wood);

- labor costs for key production personnel;

- unified social tax and pension contributions accrued on the salaries of key production personnel.

According to the accounting policy of the organization, the amount of depreciation accrued on fixed assets for production purposes is taken into account by the company as indirect expenses. And the cost of “work in progress” is calculated based on the amount of raw materials from which the finished product was made.

To do this, a special coefficient is calculated, which is determined by the formula:

Coefficient = (Amount of wood from which finished products were produced per month + Technological losses per month): Total amount of timber received per month.

The cost of “work in progress” at the end of the month is determined as follows:

Cost of “work in progress” = Total amount of direct expenses for the month x (1 - Coefficient).

The amount of direct costs, which are attributed to finished products, is calculated as follows:

The amount of direct expenses that are attributed to finished products = Total amount of direct expenses for the month - Cost of “work in progress”

January 2006

For January, the company's direct expenses were:

- for the purchase of 1000 cubic meters of wood - 1,200,000 rubles;

- for remuneration of production personnel - 300,000 rubles;

- to pay the unified social tax from the salaries of production personnel (including pension contributions) - 78,000 rubles.

200 cubic meters of finished products (boards) were made from the capitalized wood. Technological losses amounted to 400 cubic meters of wood.

Let's calculate the cost of work in progress. First of all, let's determine the coefficient. It will be:

(200 + 400) : 1000 = 0,6.

The cost of “unfinished work” at the end of January will be:

(RUB 1,200,000

Work in progress: invoice

+ 300,000 rub. + 78,000 rub.) x (1 - 0.6) = 631,200 rub.

In January, the amount of direct costs, which is attributed to finished products (200 cubic meters of boards), will be:

1,200,000 + 300,000 + 78,000 - 631,200 = 946,800 rubles.

The cost of one cubic meter of finished boards will be:

RUB 946,800 : 200 cu. m = 4734 rub.

February 2006

In order to calculate the amount of direct costs that are attributed to finished products at the end of February (that is, the next month), you need to use a slightly different algorithm.

The last formula will look like this:

The amount of direct expenses that are attributed to finished products = The total amount of direct expenses for the month + The cost of “work in progress” at the beginning of the month – The cost of “work in progress” at the end of the month.

Let’s assume that in February direct expenses of Rosdor were:

- for the purchase of 5,000 cubic meters of wood - 5,500,000 rubles;

- for remuneration of production personnel - 1,300,000 rubles;

- to pay the unified social tax on wages of production personnel (including contributions to the Pension Fund of the Russian Federation) - 338,000 rubles.

The company produced 900 cubic meters of finished products (boards) from capitalized wood. Technological losses amounted to 1,700 cubic meters of wood.

Let's calculate the cost of work in progress. Let's determine the coefficient. It will be:

(900 + 1700) : 5000 = 0,52.

The cost of the “unfinished project” at the end of February will be:

(RUB 5,500,000 + RUB 1,300,000 + RUB 338,000) x (1 - 0.52) = RUB 3,426,240

In February, the amount of direct costs, which are attributed to finished products (900 cubic meters of boards), will be:

5,500,000 + 1,300,000 + 338,000 + 631,200 - 3,426,240 = 4,342,960 rubles.

The cost of one cubic meter of finished boards will be:

RUB 4,342,960 : 900 cc m = 4826 rub.

Work in progress for March, April, May, etc. should be considered in the same way.

V. Meshcheryakov

head of the expert board

magazine “Practical Accounting”

Work in progress (WIP) is a product (work, service) that is partially finished, i.e. that has not passed all stages of processing, as well as incomplete products that have not passed testing and technical acceptance.

To obtain current data on the size of work in progress, it is necessary to take into account the movement of remaining parts, assemblies, etc.

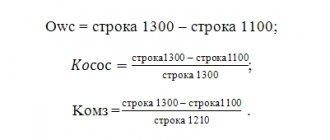

General standard of working capital (concept, calculation formula)

In simple words, the standard is the minimum volume of obs that the enterprise must constantly have. There are specific and general standards. The first ones are established according to individual elements, articles of the OSB. The second, general, or aggregate, is the sum of all particular standards.

Thus, NORtotal (general standard) is a set of private standards. Expressed in money (Russian rubles). Calculated upon completion of rationing. Its value is calculated as follows:

NORtotal=NORpz+NORgp+NORnp+NORbr (1)

The formula uses abbreviations of various standards: NORpz - production. stocks, NORgp – finished products; NORnp - incomplete. production, NORbr - future expenses.

Inventory standard

To calculate NORpz you need: SRdn (average daily consumption) in Russian. rub. and Нз – the stock norm for the corresponding element of the ObS in days. Calculation - according to the generally used formula:

NORpz=SRdn*Nz (2)

The stock norm (Nz) is the totality of the current (Nt), insurance (Nst), transport (Ntrans), technological (Ntech), preparatory (Npod) stock.

Current stock

This is the main stock on which the continuity of the production process between deliveries depends. Ztek norm is half the interval between two deliveries. It is self-evident: its value is affected by the frequency of deliveries and the volumes of resources consumed. The maximum size of the Ztek is determined by the formula:

Ztek=SDS * PMP (3)

Abbreviations: SDS – average daily requirement for the corresponding material, PMP – interval between deliveries.

Insurance (warranty) stock

Provided for in case of short deliveries, supply disruptions, etc. unforeseen circumstances. The Zstr norm is set within 30–50% of the Ztek norm. The amount of safety stock (SAS) depends on the location of the supplier and failures. It can be calculated using the following formula:

Zstr=Norma Zstr*SDP (4)

Abbreviations: ADP – average daily requirement for the corresponding material.

Transport stock

It is formed when there is a discrepancy between the timing of document flow, payment of fees and the time spent in transit of the delivered cargo. It is calculated in two ways based on actual data for the past period.

Direct counting method. It is used when there is an insignificant range of resources coming from a small number of suppliers. It is assumed that payments arrive and are paid before the cargo arrives. Accordingly, the amount of Zt (transport stock) is equal to the interval between payment and arrival of the cargo.

Analytical method. Suitable for significant product ranges and when there are many suppliers. The cost norm is determined based on last year's data on the balances of inventory items in transit (at the beginning of each quarter), minus the price of resources in transit beyond the deadlines.

Technological stock

This stock (Ztech) is formed during the preparation of materials (raw materials) for production. Taken into account when not included in production. process. This includes analysis as well as testing in laboratories.

Preparatory stock

It is formed when received materials with resources undergo preprocessing. For example, sorting, drying, picking, etc. preparatory operations. When determining the norm of this stock (Zpod), the corresponding industries are taken into account. conditions and time for preparation. That is, the time of unloading, acceptance, documentation, etc. The size of the 3D is calculated using the formula:

Zpod = SDS * PTC (5)

Abbreviations: PTC – duration of the technological cycle (days).

An example of rationing in industrial inventories

Conditional data used in normalization:

- number of suppliers =36;

- delivery cycle = 1800 days;

- Norm Zstr = 35% of norm Ztek;

- SDS (need) = 47 kg;

- cost 1 kg = 47 RUS. rub.;

- Norm Ztech = 10 days.

Task: determine NORpz (standard OBS in production inventories). Costing sequence:

- Material consumption per day: 47*47=2,209 RUR. rub.

- Norm Ztek=1800/36/2=25 days.

- Norm Zstr=25*0.35=9 days.

- The cumulative norm of all stocks: 25+9+10=44 days.

- NORpz = 44 * 2,209 = 97,126 RUR. rub.

Work in progress accounting

In order to correctly reflect work in progress in accounting, it is necessary to evaluate it. This assessment is carried out in a special way, taking into account the characteristic differences and specifics of the accounting object. In this article we will tell you how to properly account for and evaluate work in progress.

Work in progress, or WIP, are objects of material assets of an economic entity that have already been introduced into the production cycle, but have not yet gone through all stages of the technological production process. WIP can also include services provided or work performed that have not yet been accepted by the customer.

Work in progress is accounted for in special accounting account 20 “Main production (OP)”. We talked in more detail about the features of reflecting work in progress in accounting and reporting in a separate article “Work in progress in accounting.”

Costs in work in progress - an asset or a liability? Work in progress is part of the company's assets, therefore WIP is an asset and should be reflected on the left side of the balance sheet.

Methods for assessing work in progress

Each economic entity independently determines the method of current assessment of work in progress. This choice must be fixed in the accounting policy. Let's look at the key assessment methods:

- At planned cost.

This method is mainly used in industries characterized by a complex multi-stage technological process. For example, sewing, furniture or metalworking shops. The key rules for the application of this method are enshrined in the Technical Specifications on the application of standard costs dated January 24, 1983 No. 12.

Accounting for costs in work in progress using this method is determined based on the cost of each unit of work in progress at a specific stage, taking into account quantitative indicators. That is, the standard cost of WIP balances is the accounting price for each group.

The formula used for calculations is:

WIP cost = unit cost × quantity.

- At actual cost.

With this valuation method, the cost of manufactured products is determined taking into account the actual expenses incurred: direct and indirect. Consequently, the cost of work in progress in this case is determined in a similar way - by summing up direct, general and general production expenses.

Note that this method should be applied to all types of goods, works and services produced. Thus, the method is convenient for companies with a small range of products.

Actual cost = direct costs + ODP + OCR.

This method is also called raw material. That is, the method is applicable for a production cycle that is considered material-intensive (requires a large amount of raw materials and materials). Consequently, the maximum share in costs is occupied by the cost of purchasing raw materials.

Cost increase factor

The cost structure during the production cycle rarely remains unchanged.

To determine the characteristics of the increase in costs per unit of finished product, a special coefficient is used.

This indicator is used in calculations when it is necessary to characterize the growth dynamics of a specific type of cost as part of the cost of production. For example, determine the dynamics of labor costs.

Cost increase coefficient in work in progress, formula:

K = Unit cost of work in progress / Total production costs.

This formula is generalized and reflects the key essence of the coefficient. Note that in practice, enterprises use more complex calculations that maximally reflect the specifics of their activities and cost structure.

Work in progress: postings

The end of the month is the time to generate accounting entries for account 20. Note that the debit of the account. 20 accumulates all types of costs, that is, not only direct, but also indirect. Depending on the chosen cost formation method, costs in debit 20 of account can be collected in two ways:

- complete, that is, one that includes all types of expenses (basic, ODA, OCR);

- reduced, which includes only direct expenses and general production costs.

After the account is debited. 20, all costs are collected, the cost of finished products is transferred to a special accounting account 43 “Release of finished products” or to account 90 “Sales” if the enterprise sells work and services.

The debit balance 20 of the account at the end of the month is the value of the work in progress. Such balances can be used in the next period or the company decides to write them off as other expenses.

For example, writing off work in progress as a loss is carried out in the event of complete liquidation of the enterprise.

The company also has the right to decide to discontinue production of this type of product, then the balances will be written off by posting:

Dt 91-2 Kt 20.

Sales of unfinished construction

If a construction company owns an unused and unfinished object that it decides to sell, then VAT is charged on the sale. Moreover, the moment of determining the base for calculating value added tax is determined as the date of state registration of the completed purchase and sale transaction.

Sale of unfinished construction (accounting entries):

| Operation | Debit | Credit |

| The moment of recognition of sales revenue is reflected | 62 | 91 |

| Value added tax is charged on the sales amount | 91 | 68 |

| Construction is included in the cost of unfinished construction | 91 | 08 |

| Payment received for completed unfinished construction | 51 | 62 |

Source: https://ppt.ru/art/buh-uchet/nezavershenno-prvo

Work in progress in accounting

Work in progress is the unfinished process of processing raw materials into the final product as of the reporting date, i.e. a situation where materials have already been written off for production, but products have not yet been released. In PBU No. 34 (approved by order of the Ministry of Finance dated July 29.

1998 No. 34n) work in progress (WIP) refers to products/work that have not gone through the full production cycle or all stages of the technical process, as well as those already produced, but not yet tested, not accepted by the quality control department or incomplete.

Let's talk about how work in progress is recorded in accounting and what account is used.

The amount of work in progress must be indicated in the accounting records, for which this asset is assessed using the method established in the company’s accounting policy. For example, it can consist of:

- planned or actual production cost;

- direct costs;

- cost of raw materials and inventory materials used.

If an enterprise specializes in serial production of products, any of the listed accounting methods is suitable for it; if it specializes in individual production, only the method of actual costs is suitable.

In what account is work in progress recorded? To account for refineries, they use the main production account - 20, the debit of which combines all expenses, for example, from the credit of accounts 02, 10, 25, 26, 60, 69, 70, etc. When producing finished products, from the credit account. 20 write off their cost as a debit to accounts 40, 43, 90.

Debit balance 20 denotes the amount of production costs that have not yet reached the finished product (FP) stage, or the amount of expenses for work not accepted by the customer. This is the cost of the WIP.

But not only the count. 20 forms the company's WIP. When using additional farms that provide and support the main production process, costs can be reflected in the debit of the account. 23 “Auxiliary production” and 29 “Service facilities”, and the cost of finished products is written off from the credit of these accounts.

When directly accounting for costs, the cost price includes all expenses directly aimed at the production of objects, including WIP objects. When taking into account full costs, account 20 combines all expenses - direct and indirect (general production costs). The full cost method is more common. Let us give an example of the formation of accounting records for the formation of the cost of work in progress using this method.

Work in progress: postings

The formation of the WIP value is accompanied by the following entries:

| Operations for the formation of costs for work in progress in accounting (account 20) | D/t | K/t |

| Supplier services | 20 | 60 |

| Production costs include: | ||

| – Inventory | 20 | 10 |

| – accrued salary | 20 | 70 |

| – insurance premiums with salary | 20 | 69 |

| – travel expenses | 20 | 71 |

| - Future expenses | 20 | 97 |

| – depreciation of fixed assets | 20 | 02 |

| – shortages within EU norms (natural loss) | 20 | 94 |

| – expenses of auxiliary production in terms of costs of main production (OP) | 20 | 23 |

| – general business and production expenses | 20 | 25, 26 |

| on write-off of the cost of GP | ||

| Written off: | ||

| – cost of finished products | 40,43 | 20 |

| – cost of work/services | 90 | 20 |

Debit balance on account. 20 will reflect the amount of “work in progress” as of the reporting date.

The enterprise is obliged to control the volume of work in progress, preventing its sharp growth, which is possible due to various circumstances, for example, due to equipment failure, the release of a defective batch, the termination of an unpromising project or the cancellation of an order.

The cost of work in progress in accounting can be written off:

| Operations | D/t | K/t |

| – upon termination of the order, or motivated write-off | 91/2 | 20, 23, 25, 26, 29 |

| – when selling unfinished products | 62 | 91/1 |

| – when registering a marriage | 28 | 20 |

Real estate in the WIP stage often becomes the subject of purchase or is sold by the owner. They are listed on account 08 and during a purchase and sale transaction, VAT must be charged on the planned value of the object. Postings:

| Operations | D/t | K/t |

| Payment has been received into the account | 51 | 62 |

| Sales revenue taken into account | 62 | 91/1 |

| VAT charged | 91/3 | 68 |

| The cost of the WIP object is written off | 91/2 | 08 |

Example 1

LLC "Hermes" is engaged in the production of hardware and forms the cost of production at full costs. Let's calculate the amount of work in progress for May 2021 according to accounting data:

Expenses:

- Inventory and materials released into production – 526,300 rubles.

- services of contractors for setting up equipment – 120,000 rubles.

- the wages of workers and AUP were accrued - 200,000 rubles.

- deductions of insurance premiums to funds - 60,000 rubles.

- depreciation of machines per month - 42,000 rubles.

- utility bills - 70,000 rubles.

- general business expenses - 50,000 rubles.

- General production costs – 32,000 rubles.

- the cost price of the produced GP is 856,000 rubles.

At the end of the month, the accountant will issue the following entries:

| Operations | D/t | K/t | Sum |

| Costs taken into account: | |||

| – Inventory and materials transferred to main production | 20 | 10 | 526 300 |

| - salary | 20 | 70 | 200 000 |

| – insurance premiums | 20 | 69 | 60 000 |

| – setup services | 20 | 60 | 120 000 |

| – OS wear | 20 | 02 | 42 000 |

| – payment of utility costs | 20 | 60 | 70 000 |

| - general running costs | 20 | 25 | 50 000 |

| – general production expenses | 20 | 26 | 32 000 |

| GP cost written off | 43 | 20 | 856 000 |

The amount of work in progress as of May 31, 2020 will be 244,300 rubles. (526,300 + 200,000 + 60,000 + 120,000 + 42,000 + 70,000 + 50,000 + 32,000 – 856,000).

Example 2

On the balance sheet of Hermes LLC there is an unfinished building worth 1,200,000 rubles. The company decided to sell the “unfinished project” for 2,000,000 rubles. VAT of 400,000 rubles was charged on the transaction amount. The conclusion of a purchase and sale agreement and the sale of an object are documented by entries in accounting:

| Operations | D/t | K/t | Sum |

| Payment has been received from the buyer | 51 | 62 | 2 400 000 |

| Revenue recognized | 62 | 91/1 | 2 400 000 |

| VAT charged (simultaneously with the sale) | 91/3 | 68 | 400 000 |

| WIP cost written off | 91/2 | 08 | 1 200 000 |

| Financial result from the sale of “unfinished construction” (2,400,000 – 400,000 – 1,200,000) | 91 | 99 | 800 000 |

January 2006

For January, the company's direct expenses were:

- for the purchase of 1000 cubic meters of wood - 1,200,000 rubles;

- for remuneration of production personnel - 300,000 rubles;

- to pay the unified social tax from the salaries of production personnel (including pension contributions) - 78,000 rubles.

200 cubic meters of finished products (boards) were made from the capitalized wood. Technological losses amounted to 400 cubic meters of wood.

Let's calculate the cost of work in progress. First of all, let's determine the coefficient. It will be:

(200 + 400) : 1000 = 0,6.

The cost of the “unfinished project” at the end of January will be:

(RUB 1,200,000