Today we'll figure it out account 20 “Main production”. Why is it needed, what is taken into account on it. Which entries in account 20 reflect the accounting of production costs. For greater clarity, examples of cost accounting and cost formation on accounts are given. 20. In this article we will look at accounting for production costs, typical transactions and situations for account 20.

Account 20 records the costs of the main production, that is, all the organization’s expenses related to production are reflected.

What is production? In fact, production is the process of creating the cost of finished products, and the cost of finished products is, as we found out in the last article, the sum of all costs associated with production and sales. All these costs are collected in the debit of the account. 20 “Main production”, forming the cost.

| ★ Best-selling book “Accounting from scratch” for dummies (understand how to do accounting in 72 hours) > 8000 books purchased |

Accounting for production costs (account 20)

Now let's talk about exactly what costs are taken into account as the debit of account 20, and what entries are reflected in accounting.

- Direct costs, that is, those that are directly related to the production process. This could be the wages of employees (entry D20 K70 ), materials used in production (entry D20 K10 ), depreciation of fixed assets involved in the production process (entry D20 K02 ), social contributions from personnel salaries (entry D20 K69 ).

- Auxiliary production costs. An example of an auxiliary production could be a company’s own boiler room; the costs of its maintenance are taken into account in the debit of the account. 23 “Auxiliary production”, then the amount of all these costs is written off to the debit of the account. 20 “Main production” (posting D20 K23 ).

- Indirect costs, that is, those associated with the management and maintenance of production, are written off from the credit of accounts 25 “General production expenses” and 26 “General expenses” (entries D20 K25 and D20 K26 ).

- Defects in production are products, parts and work that do not meet established quality standards and cannot be used for their intended purpose. We’ll talk more about manufacturing defects in this article. For now, I’ll just say that defects are taken into account in account 28 “Defects in production” and written off as a debit to the account. 20 “Main production” (posting D20 K28 ).

Accounts 23 “Auxiliary production”, 25 “General production expenses”, 26 “General expenses” are not always used by the enterprise. These are intermediate, auxiliary accounts; they are convenient to use in large production. If the company has a small production, then there is no point in entering additional accounts; all costs can be taken into account immediately on the account. 20.

Thus, it was determined that according to the debit of the account. 20, all costs associated with the main production are taken into account, that is, the cost of finished products is formed.

This cost is then written off from the credit account. 20 to the debit of the account. 40, 43 or 90.

If the cost of finished products is taken into account at standard (planned) cost, then all expenses from the credit account. 20 are debited to the account. 40 “Release of products, works, services” (posting D40 K20 ).

If the cost of finished products is taken into account at the actual (production) cost, then all expenses from the credit of account 20 are written off to the debit of account 43 “Finished products” (entry D43 K20 ).

Products can also be immediately sent for sale, bypassing product accounting accounts, then posting D90/2 K20 .

At the end of the month, account 20 “Main production” is closed, the balance on account 20 reflects the value of work in progress, this balance is transferred to the beginning of the next month.

To reinforce the above information, I suggest looking at a couple of examples.

The procedure for accounting for general business expenses

To reflect generalized information about the expenses incurred by the organization in connection with production management processes, account 26 is used. Amounts of expenses are collected according to Dt 26, write-off and reduction of non-production costs are reflected according to Kt 26.

At most industrial enterprises, the main source of non-production expenses is payments to employees of administrative departments and managers. Transactions for the attribution of expenses in this case are reflected in the following entries:

| Dt | CT | Description | Document |

| 26 | 70 | Calculation of salaries for employees of administrative and economic departments | Payroll sheet |

| 26 | 71 | Write-off of amounts of accountable funds previously issued to an employee of a non-production department | Advance report |

| 26 | 69.1.1 | Calculation of insurance premiums from the salaries of employees of non-production units (FSS) | Payroll sheet |

| 26 | 69.3.1 | Calculation of insurance premiums from the salaries of employees of non-production departments (MHIF) | Payroll sheet |

When making settlements with counterparties for goods (work, services) received, non-production expenses are reflected in the following entries:

| Dt | CT | Description | Document |

| 26 | 60 | Expenses for purchased services are written off | Certificate of services rendered |

| 26 | 76 | Expenses for services purchased from other contractors were written off | Certificate of services rendered |

General business expenses in correspondence with production accounts are recorded in the following entries:

| Dt | CT | Description | Document |

| 26 | 21 | Write-off of semi-finished products of own production | Limit and intake statement |

| 26 | 23 | Reflection of auxiliary production work as expenses | Limit and intake statement |

| 26 | 29 | Reflection of service production work as expenses | Limit and intake statement |

Example of reflecting transactions on account 26

Based on the results of January 2021, the expenses of Minotaur LLC, which operates in the field of mechanical engineering, amounted to:

- direct costs of main production 1,413,000 rubles;

- direct costs of auxiliary production 254,800 rubles;

- the total amount of production costs is 1,667,800 rubles;

- general expenses RUB 342,600.

To determine the amount of general business expenses that fall on the main and auxiliary production, the accountant of Minotaur LLC made the following calculations:

- general operating expenses for main production RUB 290,259. (RUB 1,413,000 / RUB 1,667,800 * RUB 342,600);

- general business expenses for auxiliary production 52,341 rubles. (RUB 254,800 / RUB 1,667,800 * RUB 342,600).

The following entries were made in the accounting of Minotaur LLC:

| Dt | CT | Description | Sum | Document |

| 20 | 02 (10, 60, 70, 69, …) | Accounting for direct costs of main production | RUB 1,413,000 | Intake sheet, work completion certificate, payroll sheet, etc. |

| 23 | 02 (10, 60, 70, 69, …) | Accounting for direct costs of auxiliary production | RUB 254,800 | Intake sheet, work completion certificate, payroll sheet, etc. |

| 26 | 02 (10, 60, 70, 69, …) | Accounting for general business expenses | RUB 342,600 | Intake sheet, work completion certificate, payroll sheet, etc. |

| 20 | 26 | Reflection of general business expenses for main production | RUB 290,259 | Accounting certificate-calculation |

| 23 | 26 | Reflection of general business expenses for auxiliary production | RUB 52,341 | Accounting certificate-calculation |

Examples of production cost accounting entries

Example No. 1 of posting cost accounting in production

The organization provides services, revenue for services is 36,000 rubles. including VAT 6000 rub. Expenses associated with the provision of services: salary 8,000 rubles, material expenses 2,000 rubles. What entries are reflected in the accounting department?

| Sum | Debit | Credit | Operation name |

| 8000 | 20 | 70 | Salary expenses included |

| 2000 | 20 | 10 | Material costs taken into account |

| 10000 | 90/2 | 20 | The cost of services for sale has been written off |

| 36000 | 62 | 90/1 | Services provided |

| 6000 | 90/3 | 68 | VAT charged on services provided |

| 20000 | 90/9 | 99 | The financial result is reflected (in this example, profit) |

Account 26: General business expenses. Example, wiring

There are costs that go directly to production; such costs are direct and also directly affect the cost. But there are other costs that are not directly related to production, however, they are necessary in order to manage all economic activities as a system. Such expenses indirectly affect the cost price and are called General business expenses. To track the movement of such expenses in accounting, account 26 of the same name is intended.

The organization determines exactly which costs will be classified as general business expenses depending on the industry in which it operates. There are many such expenses, but we can list them in general terms:

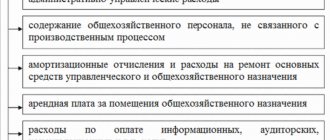

- Administrative and management expenses are always classified as general business expenses, since they are not directly related to production in any industry (for example, salaries of company management, accounting, HR, etc., business trips, security services, office, mail, communications).

- Depreciation of fixed assets that do not have a production purpose, as well as their repair.

- Services of auditors and consultants.

- Mandatory payments to the state budget (taxes, fees, penalties, fines).

- Others

| ★ Best-selling book “Accounting from scratch” for dummies (understand how to do accounting in 72 hours) > 8,000 books purchased |

| ★ Best-selling book “Accounting from scratch” for dummies (understand how to do accounting in 72 hours) > 8,000 books purchased |

For general business expenses, both synthetic and analytical accounting are required. On account 26 “General expenses”, synthetic accounting is maintained, and analytics details by item of expense or place of occurrence of general expenses.

As an example, consider typical business transactions on account 26 “General business expenses”

| Debit | Credit | Operation |

| 26 | 02 | Calculation of depreciation of fixed assets that do not have a production purpose. |

| 26 | 10 | Write-off of materials for general business needs |

| 26 | 70, 69 | Calculation of wages and insurance premiums for employees who are not involved in production (managerial and service personnel) |

| 26 | 60 | Debt to third parties for services provided for general business needs. |

| 26 | 97 | Write-off of deferred expenses |

| 26 | 68 | Tax calculation |

| 26 | 68 | Write-off of accountable funds |

| 23 | 26 | Write-off of general business expenses for auxiliary production |

| 29 | 26 | Write-off of general business expenses for service production |

| 20 | 26 | Write-off of general business expenses for the main production product |

To account for general business expenses, you can use a full or partial journal-order form. If the company uses the full one, then it uses statement 15 for analytics to account for the expenses we are interested in, and for synthetic accounting, journal-order 10 (or 10/1). In the order journal 05, both analytics and synthetic accounting are maintained, in the case of using a partial form.

The information that is reflected in these registers is formed on the basis of tables on the distribution of wages and materials, amounts of depreciation of fixed assets, decoding sheets for various types of cash expenses, which are reflected in other order journals, etc.

How to reflect expenses for main production in transactions

Data on production costs (material costs, depreciation, wages of production workers, etc.), which are core for the enterprise (organization), are reflected in active account 20. The balance of account 20 at the end of the month (in the example given - 1000 thousand rubles) characterizes the cost of work in progress.

Typical transactions for transfer to main production:

| Account Dt | Kt account | Wiring Description | Transaction amount | A document base |

| 20.01 | 02.01, 05 | Depreciation of fixed assets and intangible assets involved in the main production has been calculated | 2500 | Help-calculation |

| 20.01 | 10.01 | Materials were released to main production from the warehouse | 7500 | Limit-fence card, requirement-invoice |

| 20.01 | 97.21 | Part of deferred expenses that relates to the reporting period is written off | 100 | Help-calculation |

| 20.01 | 23, 25, 26 | Part of the expenses of auxiliary production, general workshop and general business expenses for the main production was written off | 600 | Help-calculation |

| 20.01 | 69, 70 | Wages and social benefits accrued to employees of main production | 2300 | Help-calculation, payroll statement |

| 40 (43) | 20.01 | Finished products of the main production are taken into account at their actual cost | 12000 | Help-calculation |

Categories of articles on production

- Postings for manufacturing defects

- Postings to work in progress

- Accounting entries for overhead costs

- Accounting entries for production waste

- Cost calculation and calculation methods

- Cost accounting using the direct costing method: postings, examples, nuances

- Accounting entries for sales of finished products

- Accounting for finished products: postings, examples, nuances

- Postings to the cost of production in accounting

- Accounting entries for main production

- Accounting entries for auxiliary production

- Accounting for production costs in transactions