Photo: pixabay.com Updated: 03/27/2020

Are maternity benefits subject to taxation? No, payments related to maternity are exempt from all taxes. If the employer decides to pay the employee extra, then he will have to pay taxes, but not always. If the amount does not exceed 50,000 rubles, then the amount of the additional payment is not taxed.

- Who is paid for maternity leave?

- How long does maternity leave last?

- How to calculate the benefit amount?

- Who is granted parental leave for up to 1.5 years?

- What are personal income tax and insurance premiums, are they withheld from benefits related to maternity?

- How are personal income tax and insurance premiums withheld when maternity benefits are paid up to average earnings?

- How are maternity benefits reflected in 2-NDFL?

- Pilot project for direct payments from the Social Insurance Fund

Who is paid for maternity leave?

After issuing sick leave in connection with maternity, a woman can apply for maternity benefits. The hospital form is filled out by an obstetrician-gynecologist at the 30th week of pregnancy (clause 46 of Order of the Ministry of Health and Social Development No. 624n).

Recipient categories include:

- Officially employed

- Unemployed, if 12 months have not passed since the date of dismissal due to liquidation of the company

- Full-time students

- Military personnel under contract, and civilians in the military, outside the Russian Federation

- Adoptive mothers

Payment of benefits is made: at the place of work, service or study. Dismissed persons apply to the social protection authorities (SZN).

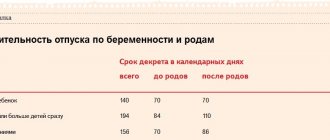

How long does maternity leave last?

After receiving a certificate of incapacity for work, the woman writes an application for maternity leave. Depending on how the pregnancy proceeds, the law (Article 10 of the Federal Law-255) provides for the duration of leave:

- 140 calendar days - for normal pregnancy (70 days before and 70 days after the baby is born)

- 156 days – if there is a difficult birth or pregnancy with complications (70 and 86 days)

- 194 days – for multiple pregnancies (84 and 110 days)

If pregnancy comes with complications, two certificates are issued for temporary disability. One for 140 days - by a doctor observing the pregnancy, the second for 16 days - upon discharge from the hospital with a newborn (clause 48 of Order of the Ministry of Health and Social Development No. 624n).

Social guarantees for expectant mothers: the concept of maternity payments

Women who are expecting a baby need protection and support from the state. That is why for this category of citizens there are a number of benefits and financial payments both before childbirth and after the birth of a child.

The rules for providing these payments are regulated at the legislative level:

- Federal Law No. 81 “On state benefits for citizens with children";

- Federal Law No. 255, dedicated to the concept of compulsory social insurance in case of maternity or temporary disability;

- Federal Law No. 256, regulating the Maternity Capital program.

Also, women’s rights are regulated by tax, labor and civil codes.

The term “maternity leave” does not exist in Russian legislation . This is a popular name that combines two vacation periods at once:

- maternity leave;

- parental leave for children up to one and a half and three years old.

They are called maternity leave, and the benefits paid to parents in such cases are called maternity payments.

A woman can apply for maternity leave at the 30th week of pregnancy on the basis of a certificate of incapacity for work issued by the medical institution where she is registered in connection with pregnancy.

This type of financial support, unlike other maternity payments, can only be provided to a mother who has given birth to or adopted a child no older than 3 months. The father cannot claim this benefit.

Read also: Certificate for childbirth: who needs it and why?

How to calculate the benefit amount?

Maternity benefit (M&B) is calculated based on the amount of wages for the pay period. The billing period is two full years preceding the vacation.

Amount of maternity payments in 2021

After calculating the average daily income, the resulting amount must be multiplied by the number of vacation days (140, 156 or 194 days).

The law establishes the maximum amount of benefit payments under the BiR, limited by the maximum insurance base.

The size of the minimum payment cannot be less than the minimum wage. With less than 6 months of experience, the B&R benefit cannot exceed the minimum wage (Clause 3, Article 11 of Federal Law No. 255-FZ of December 29, 2006).

The period for calculating benefits is up to 10 calendar days from the date of presentation of the certificate of incapacity for work. The employer transfers money per day at the nearest salary (Part 1, Article 15 of Federal Law-255). If the social security authorities are involved in the calculation, the transfer of funds occurs before the 26th of the next month, after the month of presentation of the certificate of incapacity for work (clause 18 of Order of the Ministry of Health and Social Development of Russia No. 1012n).

Online maternity benefits calculator

Income tax on maternity leave in 2020–2021

There were no changes in the rules for calculating maternity benefits or in the issue of taxation of their personal income tax in 2020–2021. This means that in 2020-2021, income tax is still not taken from maternity leave. However, traditional changes have been made to the amounts depending on the size of the minimum wage and the value of the employee’s income, within the limits of which this income is subject to contributions for disability and maternity insurance.

Based on these values, from 01/01/2021 for maternity leave:

- the minimum value in connection with the next increase in the minimum wage (up to 12,792 rubles) will be 58,878.25 rubles. in case of normal birth (within 140 days);

- the minimum amount for complicated childbirth (for 156 days) will be 65,607.19 rubles;

- the minimum amount for a multiple pregnancy (for 194 days) will be 81,588.43 rubles.

How to calculate the maximum amount of maternity benefits, see the Ready-made solution from ConsultantPlus. If you do not have access to the K+ system, get a trial online access for free.

Who is granted parental leave for up to 1.5 years?

After the end of the BiR leave and the closure of the certificate of incapacity for work, a woman has the right to take out maternity leave for up to 1.5 years.

The monthly child care benefit is 40% of average monthly earnings, and not 100% as the B&R benefit.

Amount of maternity payments in 2021

The same categories of recipients as recipients of BiR benefits can receive child care benefits. In addition to the mother of the child, the father or other relatives can take parental leave.

Parental leave is provided upon application. The start date of parental leave is the day after the end of sick leave. In addition to the application, it is necessary to provide a certificate from the second parent’s place of work stating that he did not apply for leave or benefits.

The procedure for calculating and transferring funds is the same as for the B&R benefit.

Who pays maternity benefits?

The basis for the absence of personal income tax is that these benefits are state compensation. They are paid to the Social Insurance Fund. Since 2021, control over benefit payments has been transferred to the Federal Tax Service.

IMPORTANT! Any entrepreneur must make payments for labor and child care. This also applies to individual entrepreneurs who have chosen a special taxation regime: imputation, simplified.

Additional nuances

Let's look at the various features of calculating benefits:

- If an employee works in several places part-time, each company must pay her money. Benefits are issued in a standard manner.

- The funds in question are not subject to personal income tax or insurance premiums. That is, the woman receives payments in full.

- Benefits will be paid only if the woman is officially employed. If she works unofficially, then only the employer makes the decision on payments. If he doesn’t pay anything, the employee won’t even be able to sue him.

The amount of benefits is determined individually in each case, depending on the worker’s salary.

To receive payments, the employee must provide the employer with a corresponding application, as well as a certificate of incapacity for work. Papers must be submitted no later than six months from the date of the end of the leave under the BiR. If an employee wants to go on maternity leave later than the date specified in the certificate of incapacity for work, the employer must provide it from the date specified in the application.

Expert opinion

Lebedev Sergey Fedorovich

Practitioner lawyer with 7 years of experience. Specialization: civil law. Extensive experience in defense in court.

IMPORTANT! It is not recommended to make payments under B&R for the period during which the employee actually worked. This is due to the fact that the Social Insurance Fund is unlikely to reimburse these expenses to the entrepreneur.

FOR YOUR INFORMATION! Tax exemption is due to the fact that the entrepreneur, when issuing benefits, does not spend the funds of his company. All expenses are reimbursed by the state. This is a measure to protect pregnant women, one of the social benefits.

This is important to know: How sick leave is paid if it falls on a weekend

What are personal income tax and insurance premiums, are they withheld from benefits related to maternity?

Personal income tax (tax for individuals) or otherwise income tax is a mandatory fiscal fee in the amount of 13% of a citizen’s income, withheld monthly by the Employer in favor of the Federal budget (Article 208 of the Tax Code of the Russian Federation).

The employer pays monthly insurance contributions for compulsory social insurance (Article 419 of the Tax Code of the Russian Federation). The object of taxation is income from labor activity.

All benefits received related to maternity are not subject to taxation. Articles 217, 422 of the Tax Code of the Russian Federation list benefits that are not subject to insurance contributions, these benefits include:

- Maternity benefit (maternity benefit)

- Child care allowance

These payments are calculated from the Social Insurance Fund. Financing from an extra-budgetary fund is provided from the first day of temporary disability of the expectant mother.

Taxation of maternity leave in 2020–2021: is personal income tax withheld from these payments?

In paragraph 1 of Art. 217 of the Tax Code of the Russian Federation contains an unambiguous answer to the question of whether income tax is withheld from maternity leave. The text of this article states that maternity benefits are not subject to personal income tax. This makes maternity benefits different from regular sick leave, from which personal income tax must be withheld.

Unemployed women are not entitled to maternity leave, with the exception of those who were dismissed due to the liquidation of the organization. Like women who go on regular maternity leave, they receive all the required payments without having to reduce them by the amount of income tax.

In addition, all pregnant women have the right to 2 more benefits:

- A one-time payment for those who registered at the antenatal clinic before the 12th week of pregnancy. Its basic amount established by law is 300 rubles. Taking into account indexation from 02/01/2021, it is equal to 708.23 rubles.

- A lump sum payment for the birth of a child. Its basic value, established by law, is 8,000 rubles. Taking into account indexation, this benefit from 02/01/2021 is equal to 18,886.32 rubles.

Income tax is not deducted from the amounts of these payments, as well as from maternity payments.

Read more about the types and amounts of child benefits in 2021 here.

How are personal income tax and insurance premiums withheld when maternity benefits are paid up to average earnings?

In a standard situation, maternity benefits are calculated taking into account the maximum insurance base.

Example: With a salary of 100,000 rubles, income for 2 years will be 2,400,000 rubles, and the average daily income will be 3,283.17 rubles. To calculate the benefit, the maximum base for the 2 previous years is taken - 912,000 rubles for 2021, and 865,000 rubles for 2021, total 1,777,000 rubles. We find that the average daily earnings cannot be higher than 2,430.92 rubles. Taking into account the size of the insurance base, for 140 days of maternity leave, the maximum benefit amount will be 340,328.80 rubles. The employer may provide for additional payment of maternity benefits up to the actual average earnings. In this case, the additional payment of the difference is calculated at the expense of the organization, and not the Social Insurance Fund.

The Ministry of Finance believes that such additional payments cannot be classified as state benefits. They are not subject to Art. 217 of the Tax Code of the Russian Federation, and are subject to personal income tax and insurance contributions in the general manner (Letter dated February 12, 2009 No. 03-03-06/1/60).

This rule can be circumvented if you issue an additional payment as financial assistance. The payment is excluded from the tax base if the amount does not exceed 50,000 rubles. In the case where the amount of the surcharge is greater, tax must be paid on the difference (clause 8, part 1, article 217, clause 3, part 1, article 422 of the Tax Code of the Russian Federation).

Pilot project for direct payments from the Social Insurance Fund

Since 2012, a pilot project for direct payments from the Social Insurance Fund has been launched in two constituent entities of the Russian Federation. Since 2021, the number of participants has increased to 50. By July 2021, it is planned to transfer all regions of the Russian Federation to the new system.

The essence of the project is that the employer acts as an intermediary between the employee applying for maternity leave and the fund. The project helps a woman draw up an application for benefits using a special form and creates a package of documentation.

Then the employer contacts the Social Insurance Fund on behalf of the employee. The fund assigns benefits and independently transfers funds to the woman’s bank account. At the same time, the transactions are not reflected in the employer’s records, and the question of withholding personal income tax and insurance contributions does not arise.