Retained earnings are the financial volume for a certain period from which we subtract fees and taxes and possible fines based on profits. Therefore, retained earnings are often used to increase the authorized capital of LLCs (Limited Liability Company) and joint-stock organizations. The basis for this is the corresponding decision made by the shareholders and members of the Company.

The company's authorized capital is increased at the expense of retained earnings in order to attract the attention of creditors and investors. It happens that the authorized capital is increased due to production needs, for example, to conduct a certain type of activity, the law of the Russian Federation determines the authorized capital in a certain amount. Be that as it may, there are some peculiarities in increasing the capital.

Let's consider what features there are in the formation of the authorized capital.

A special feature is that it is not formed by all entities, but only by commercial legal entities.

The general features of the fund are:

• it is created and used by all non-governmental organizations; • it is determined by the value that is included in the constituent document; • it is used to determine the goals of a legal entity; • it can be increased or decreased, but only to the level provided by law.

As the authorized capital increases, the value of all shares increases. This cost will also increase because profits were not distributed in previous periods. Only shareholders of a given company can use indicators to increase capital on the basis of a decision made.

It is imperative to control that the increased amount is not higher than the value of the assets, from which the amount of the reserve and the authorized capital is deducted according to the reporting that preceded the process of introducing shares.

To begin with, we will offer two main ways to increase the authorized capital:

1. Make additional contributions. Participants or newcomers make contributions to the company. An additional contribution to the management company occurs in the same way as the authorized capital is formed. 2. Dividends are reinvested. If profit appears after the reporting period, then at the general meeting a decision is made to distribute it among the participants (in proportion to the shares that each of them has). But it happens that dividends are not paid. Participants at the general meeting decide to send dividends to increase the capital. It turns out that participants remain without dividends, but their contribution to the company increases. It turns out that instead of profit, they receive company rights.

What reasons could there be for increasing the authorized capital of a company?

1. A new member joins the group. When a new member joins the team, he makes an additional investment (this can be cash or property). Thus, he acquires his interest in the share, the right to vote when making important decisions in the company, but also other rights and obligations that other co-founders of the LLC have, and dividends from the company’s activities. 2. They make large transactions. When transactions are concluded with large companies, including foreign ones, the amount included in the authorized capital is of particular importance. Since its value includes the minimum amount of the enterprise’s property, guaranteeing the interests of shareholders. In the event that the Company becomes bankrupt, the size of the capital is the amount that creditors are able to dispose of. Therefore, this value can be called confidence in creditors, at a time when they invest in the activities of a company that does not have the minimum capital (>10 thousand rubles). In another way, we will say that such an enterprise has a more solid appearance. 3. There are not enough funds for turnover. The funds available in the authorized capital of the Company are used to meet the economic and financial needs of the enterprise. If they are in short supply and there is no necessary profit, then additional investments are made. In addition, when the authorized capital increases due to a lack of funds, the company does not need to pay VAT. 4. Receive a license or certificates. To obtain a license or certificate, certain conditions must be met regarding the amount of the authorized capital. The larger the amount of the authorized capital, the higher the indicators of financial stability of the LLC in front of partners and creditors, and the authorities that issue the license.

Is it possible to increase the authorized capital at the expense of retained earnings,

Article 19. Increasing the authorized capital of a company through additional contributions of its participants and contributions of third parties accepted into the company.

A guide to corporate disputes. Questions of interpretation and application of Art. 191. The general meeting of the company's participants, by a majority of at least two-thirds of the total number of votes of the company's participants, if the need for a larger number of votes to make such a decision is not provided for by the company's charter, may decide to increase the authorized capital of the company by making additional contributions by the company's participants. Such a decision must determine the total cost of additional contributions, and also establish a uniform ratio for all participants in the company between the cost of the additional contribution of a company participant and the amount by which the nominal value of his share is increased. This ratio is established based on the fact that the nominal value of a company participant’s share can increase by an amount equal to or less than the value of his additional contribution.

Each participant in the company has the right to make an additional contribution not exceeding part of the total cost of additional contributions, proportional to the size of the share of this participant in the authorized capital of the company. Additional contributions may be made by the company's participants within two months from the date of adoption by the general meeting of the company's participants of the decision specified in paragraph one of this clause, unless a different period is established by the company's charter or the decision of the general meeting of the company's participants.

No later than one month from the date of expiration of the period for making additional contributions, the general meeting of the company's participants must make a decision on approving the results of making additional contributions by the company's participants and on introducing changes related to increasing the size of the company's authorized capital into the company's charter, approved by the founders (participants) of the company. In this case, the nominal value of the share of each participant in the company who made an additional contribution increases in accordance with the ratio specified in paragraph one of this paragraph.

(as amended by Federal Laws dated December 30, 2008 N 312-FZ, dated June 29, 2015 N 209-FZ)

(see text in the previous edition)

Paragraphs four through five are no longer in force on July 1, 2009. — Federal Law of December 30, 2008 N 312-FZ.

(see text in the previous edition)

2. The general meeting of company participants may decide to increase its authorized capital on the basis of an application from a company participant (applications of company participants) to make an additional contribution and (or), unless prohibited by the company’s charter, an application from a third party (applications from third parties) to accept him into society and making a contribution. This decision is made unanimously by all members of the company.

The application of a company participant and the application of a third party must indicate the size and composition of the contribution, the procedure and deadline for making it, as well as the size of the share that the company participant or third party would like to have in the authorized capital of the company. The application may also indicate other conditions for making contributions and joining the company.

Simultaneously with the decision to increase the authorized capital of the company on the basis of an application from a member of the company or applications from participants of the company about making an additional contribution by him or them, a decision must be made to make changes to the charter of the company, approved by the founders (participants) of the company, in connection with the increase in the authorized capital of the company, as well as a decision to increase the nominal value of the share of a company participant or shares of company participants who submitted applications for making an additional contribution, and, if necessary, a decision to change the size of the shares of company participants. Such decisions are made unanimously by all participants in society. In this case, the nominal value of the share of each company participant who submitted an application to make an additional contribution increases by an amount equal to or less than the value of his additional contribution.

(as amended by Federal Laws dated December 30, 2008 N 312-FZ, dated June 29, 2015 N 209-FZ)

(see text in the previous edition)

Simultaneously with the decision to increase the authorized capital of the company on the basis of an application of a third party or applications of third parties to accept him or them into the company and make a contribution, decisions must be made to admit him or them to the company, to include it in the charter of the company approved by the founders (participants) company, changes in connection with an increase in the authorized capital of the company, on determining the nominal value and size of the share or shares of a third party or third parties, as well as on changing the size of shares of the company's participants. Such decisions are made unanimously by all participants in society. The nominal value of the share acquired by each third person admitted to the company must not exceed the value of his contribution.

(as amended by Federal Laws dated December 30, 2008 N 312-FZ, dated June 29, 2015 N 209-FZ)

(see text in the previous edition)

Additional contributions by the company's participants and contributions by third parties must be made no later than six months from the date of adoption by the general meeting of the company's participants of the decisions provided for in this paragraph.

(as amended by Federal Law dated December 30, 2008 N 312-FZ)

(see text in the previous edition)

The paragraph became invalid on July 1, 2009. — Federal Law of December 30, 2008 N 312-FZ.

(see text in the previous edition)

2.1. An application for state registration of the changes provided for in this article in the charter of the company, approved by the founders (participants) of the company, must be signed by the person performing the functions of the sole executive body of the company. The application confirms that the company's participants have made additional contributions or contributions by third parties in full. Within three years from the date of state registration of the relevant changes in the company’s charter, approved by the founders (participants) of the company, the company’s participants jointly and severally bear, if the company’s property is insufficient, subsidiary liability for its obligations in the amount of the cost of additional contributions not made.

(as amended by Federal Law dated June 29, 2015 N 209-FZ)

(see text in the previous edition)

The specified application and other documents for state registration of changes provided for in this article in connection with an increase in the authorized capital of the company, an increase in the nominal value of shares of company participants who made additional contributions, the admission of third parties to the company, determination of the nominal value and size of their shares and, if necessary, with a change the size of the shares of the company's participants, as well as documents confirming the full introduction by the company's participants of additional contributions or contributions by third parties must be submitted to the body carrying out state registration of legal entities within a month from the date of the decision to approve the results of making additional contributions by the company's participants in accordance with paragraph 1 of this article or making additional contributions by company members or third parties based on their applications.

For third parties, such changes become effective from the moment of their state registration.

If the company operates on the basis of a standard charter, within a month from the date of the decision on approval of the results of making additional contributions by the company's participants in accordance with paragraph 1 of this article or making additional contributions by the company's participants or third parties based on their applications, the company informs the authority carrying out state registration of legal entities, in the manner established by the federal law on state registration of legal entities, on increasing the authorized capital of the company, as well as on increasing the nominal value of shares of company participants who made additional contributions, on admitting third parties to the company, on determining the nominal value and the size of their shares and, if necessary, changing the size of the shares of the company’s participants.

(paragraph introduced by Federal Law dated June 29, 2015 N 209-FZ)

(clause 2.1 introduced by Federal Law dated December 30, 2008 N 312-FZ)

2.2. In case of failure to comply with the deadlines provided for in paragraph three of paragraph 1, paragraph five of paragraph 2 and paragraph 2.1 of this article, the increase in the authorized capital of the company is considered failed.

(clause 2.2 introduced by Federal Law dated December 30, 2008 N 312-FZ)

Advertisement Civil Code of the Russian Federation.

To participants of the company and third parties who have made non-monetary contributions, the company is obliged to return their deposits within a reasonable period of time, and in the event of non-return of deposits within the specified period, also to compensate for lost profits due to the inability to use the property contributed as a contribution.

4. By decision of the general meeting of the company’s participants, adopted unanimously by all the company’s participants, the company’s participants, in exchange for their additional contributions, and (or) third parties, in respect of their contributions, have the right to set off monetary claims against the company.

How do they decide that it is necessary to increase the authorized capital?

As mentioned above, this decision remains with the participants of the company. As a general rule, it is required that the votes be no less than 70% of all participants combined. But such a rule is not the only one that exists. According to the charter of an LLC, it is possible to provide for much more votes that are required to make a decision regarding an increase in the authorized capital (for example, at least 75% of all participants). Note that the rules can only be changed based on the number of votes to increase them.

The decision of the meeting is confirmed by a protocol signed between the company's participants.

How to document an increase in capital

In the decision of the meeting between the participants, you need to indicate some information, namely:

• the total amount by which the authorized capital is increased; • coefficient, which is determined by the amount of increase in relation to the share of each participant; • what size of the capital is planned; • within what period participants must deposit additional funds; • it is prohibited or possible for third parties or participants to make additional contributions to the company; • what are the deadlines for making investments; • what rules are used to resolve issues in the case of competitive proposals among participants.

Increasing the size of the authorized capital

In the course of the company's activities, it is possible to increase the amount of its initial authorized capital. An increase in the authorized capital can be done in one of the following ways:

- by making additional contributions by participants (or third parties who are accepted into the company);

- at the expense of the organization's own property.

Let's look at each of the above options as an example.

Postings to increase the authorized capital due to additional deposits

The participants of Phantom LLC, whose authorized capital is 954,000 rubles, are K.P. Malyshev. (share 22%) and JSC Aurora (share 78%). On 02/02/2016, the minutes of the board’s decision recorded an increase in the authorized capital of Phantom LLC by 265,000 rubles. For the preparation of documents, Phantom LLC paid a state fee in the amount of 780 rubles.

In the accounting of Phantom LLC, entries were made to accounting account 80:

| Dt | CT | Description | Sum | Document |

| 75.01 | The debt of Aurora JSC for an additional contribution to the authorized capital was repaid (RUB 265,000 * 78%) | RUB 206,700 | Bank statement | |

| 50 | 75.01 | The debt of K.P. Malyshev was repaid. for an additional contribution to the authorized capital (RUB 265,000 * 22%) | RUB 58,300 | Receipt cash order |

| 68 | The amount of state duty has been transferred | 780 rub. | Payment order | |

| 75.01 | 80 | The increase in the authorized capital is reflected | RUB 265,000 | Board minutes |

| 91.02 | 68 | The amount of state duty is included in other expenses | 780 rub. | Application for state registration of changes in the charter |

Increase from the organization's own property

According to the decision of the board of LLC “Faza”, the authorized capital of the organization was approved at the expense of additional capital in the amount of 380,000 rubles. The amount of additional capital was formed earlier as a result of the revaluation of a group of fixed assets. For the preparation of documents, Faza LLC paid a state fee of 780 rubles.

In the accounting of Faza LLC, the entries were reflected as follows:

| Dt | CT | Description | Sum | Document |

| 68 | The amount of state duty has been transferred | 780 rub. | Payment order | |

| 83 | 80 | The authorized capital of Faza LLC has been increased due to its own property | 380,000 rub. | Board minutes |

| 91_2 | 68 | The amount of state duty is included in other expenses | 780 rub. | Application for state registration of changes in the charter |

How is reserve capital assessed?

Inventory for reserve capital is carried out in the same way as for additional capital. Check calculations based on reserve amounts:

• which were formed by law; • formed according to constituent documents.

They carry out an inventory of reserve capital to cover losses, pay off company bonds, and to repurchase shares if there are no other means.

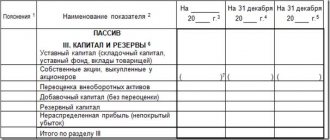

Retained earnings are reflected in the financial statements, divided into four subaccounts:

• as retained earnings for previous years; • uncovered loss for previous years; • retained earnings of the current year; • uncovered loss of the current year.

How is the net profit of a joint-stock company distributed?

According to the law, joint stock companies must be guided by accounting, and at the end of the financial year it is necessary to draw up an accounting report and approve the distribution of profits and losses. Therefore, it is the general meeting of shareholders that makes a decision on how to properly distribute net profit in a joint-stock company. According to the law of the Russian Federation, there are a number of main directions on how to distribute net profit. Among the directions are:

1. Dividends are paid. In this situation, profits are distributed based on the decision of society. 2. Create a reserve fund. Here, the size of the fund is established by the company’s Charter, but the minimum size can be 5% of the total capital according to the Charter. 3. A special fund for the corporatization of company employees is formed. As in the previous situation, this provision is prescribed by the charter of the joint-stock company. All shareholder funds are distributed among the acquisitions of shares that are sold by its shareholders. 4. Increase the authorized capital.

Let us note that whether or not to increase the authorized capital is decided only by the highest management body and is enshrined in the protocol.

The following methods are also used to change the size of the Criminal Code:

1. All members of the company invest additional funds. At the meeting, decisions are made on the size and timing of deposits. 2. Individual participants of the company make additional investments, which can come not only from one, but also from a group of participants. 3. Accept other participants. At the general meeting they decide whether new participants are needed or not. 4. Increase the authorized capital at the expense of retained earnings. In this situation, investment operations are carried out, as a result of which they receive additional profit and increase capital.

In a joint stock company, the authorized capital is the total nominal value of all shares. The increase is driven not only by the rise in the value of each individual share, but also by additional issues. The cost will also increase due to the fact that there is retained earnings from previous periods. Shareholders make decisions using this data.

You should pay attention to how capital moves - this is an indicator of the dynamics of the company’s capital on the last day of the current year:

• the year for which the report is being prepared; • the previous year; • two years ago.

Indicators that have an impact on the size of a company’s capital are divided into the following groups:

• increased capital, also net income; • if the property is overvalued; • income that is aimed at increasing capital; • additionally issue shares or increase the par value of these shares; • reduce capital and loss; • property is revalued; • reduce the value of shares or reduce the quantitative status of shares; • reorganize the legal entity and its dividends; • change additional capital; • change reserve capital.

An important condition is to control the increase in the amount so that it is not higher than the value of the assets, from which the amount of the reserve fund and authorized capital is subtracted according to the reporting data.

When a certain amount is contributed, this is not considered as a sale of any share of the company, so the rights to this part are not transferred to the participant. The member who contributes to the fund receives his duties and rights on the basis that he is a member of the company. It turns out that there is no purchase and sale procedure, so there is absolutely no need to use cash register equipment to carry out such operations.

An announcement is made that a member of the company is making a monetary contribution. This document includes three components:

• receipt; • announcement; • receipt order.

At each point, information is entered in the same way. It is imperative to note the basis for which the investment is made - a contribution to the authorized capital.

At the meeting, they decide not only to increase the authorized capital, but also decide whether to change the position of the announced additional shares. There are certain points during the issue of shares:

• number of other shares of different types; • choose a placement method; • form of payment and placement price.

2.6. Analysis of retained earnings as a component of equity

Retained earnings are the portion of net income that is not distributed but retained by the bank, usually for the purpose of reinvestment in its activities.

The specified profit is a source of equity capital of internal origin. It is created as the balance of net profit after accrual of dividends, contributions to general reserves, reserve capital and other funds (reserves) created in accordance with decisions of general meetings of participants (founders, participants) of the bank or in accordance with current legislation. In financial accounting, retained earnings include the result of previous years, the result of last year, which is awaiting approval by the meeting of shareholders (founders), and the result of the current year. The higher the value of retained earnings, the better. However, it should be borne in mind that the current year's result may be adjusted downwards based on the results of audits and until this point cannot be paid in the form of dividends. But the negative value of the results of previous years and the current year means that the bank had losses at one time or another, that is, it “ate away” its own capital. Since the amount of all deductions (except for dividends) is predetermined, the balance of retained earnings for the previous year depends mainly on the amount of dividends that must be paid to shareholders (participants). In order to comply with the “equity / assets” ratio established by the National Bank of Ukraine, banks are often forced to choose between increasing the amount of retained earnings and issuing new shares. However, the bank's shareholders are its owners and are reluctant to expand the circle of shareholders and issue a new share. When a portion of the profits is retained by the bank instead of being distributed as dividends, the bank's owners believe that these retained funds will provide them with the required market return on the common stock in the future. Increasing equity capital through retained earnings is also beneficial because there are no costs associated with it. However, prolonged suppression of dividend payments may lead to a decline in the market value of shares. When analyzing retained earnings as a source of equity capital, it is necessary to combine it with an analysis of the bank’s financial results, as well as take into account the methods for determining dividends that the bank uses when implementing its dividend policy. You should also take into account the forms of payment of dividends, restrictions on their payment, which are established by current legislation and the National Bank of Ukraine, as well as the current procedure for the payment and taxation of dividends (Table 2.6). Table data 2.6 indicate that the bank allocates about 20% of its net profit to pay dividends, although the share of dividend payments decreased over the analyzed period by 1.8 percentage points. In its activities, the bank adheres to the method of constant dividend payments. Payment of dividends was carried out exclusively in cash. Table 2.6 ANALYSIS of dividend payments When analyzing the size of dividends paid to the owners of the bank, it is necessary to find out the type of dividend policy that the bank pursues: conservative, moderate or aggressive. Each type of dividend policy corresponds to specific methods for determining dividends, each of which has both positive features and certain wadis. The residual method and the method of constant dividend payments correspond to the conservative type. The essence of the first method is that the amount of profit for payment of dividends is determined as the remainder after satisfying the bank's investment opportunities. The advantage of this method is that it ensures high rates of bank development and increases its financial stability. The disadvantage is the instability of the size of dividend payments, which negatively affects the formation of the market value of shares and the image of the bank. The essence of the constant dividend payment method is to maintain a stable amount of dividend payments over a long period of time. This method creates a feeling of confidence among owners in the stability of the amount of current income, regardless of various factors, and determines the stability of stock quotes on the securities market. The disadvantage of this method is the weak relationship between dividends and the financial results of a commercial bank. To reduce the impact of this disadvantage, a stable amount of dividend payments is established, as a rule, at a relatively low level. The moderate type of dividend policy corresponds to the method of constant and variable parts of the dividend. The essence of this method lies in the regularity of payments of stable, small dividends in close relationship with the results of the bank’s financial activities, which allows increasing the amount of dividends paid during periods of its effective operation. The disadvantage of this method is that the market value of shares decreases in the case of long-term payment of minimum dividends, and also that it can be effectively used by banks with unstable profits. The aggressive type of dividend policy includes: the method of stable dividend growth and the method of constant dividend ratio. The first method involves a stable increase in the level of dividend payments per share. For this purpose, as a rule, a fixed percentage increase in dividends to their size in the previous period is established. The advantage of this method is to ensure a high market value of the bank's shares and to form its positive image among potential investors during additional issues. The disadvantage of this method is the lack of elasticity in its application, a reduction in investment activity and a deterioration in the financial condition of the bank, subject to an increase in the growth rate of the dividend payment ratio. The constant dividend payout ratio method assumes compliance with the established proportions of distribution of profits received between shareholders (founders) and the bank, i.e. establishing the relationship between profits consumed and capitalized. The advantage of this method is the simplicity of forming a dividend fund and its close relationship with the amount of profit received by the bank. The main drawback is the instability of dividend payments per share, which is associated with the instability of the amount of generated profit. Such instability affects fluctuations in the market value of shares, and also indicates the high riskiness of the bank’s activities. The constant dividend payout ratio method can only be used by banks with stable profits. The decision on the form of dividend payment is made by the General Meeting of Bank Participants, and it can significantly affect the amount of equity capital (Fig. 2.2). Rice. 2.2. Main forms of dividend payment When analyzing equity capital, one should take into account the restrictions established by the current legislation on the payment of dividends: - The Bank is prohibited from paying dividends or distributing capital in any form if such payment or distribution would entail a violation of the capital adequacy standard; — If during the previous year the bank’s activities were unprofitable, the bank is allowed to pay dividends or distribute capital in any form in an amount not exceeding 50% of the difference between the bank’s capital and the level of regulatory capital. The NBU, depending on the level of capital adequacy of the bank, recommends taking the following measures Small and significantly Small banks: - Stop paying dividends in any form, except for paying dividends in the form of own shares (shares, shares) - Stop repurchasing your own shares (shares, shares of participants from Authorized capital). The taxation of dividends has a significant impact on the size and structure of capital. When analyzing the impact of dividend policy on the structure and size of the bank's equity capital, it is necessary to take into account, in particular, the following: 1. If a decision is made to pay dividends, the issuer of corporate rights on which dividends are accrued makes the specified payments to the owner of such rights in proportion to the share in the authorized capital of the issuer regardless of whether the issuer's activities were profitable during the reporting period if there were other own sources for paying dividends. 2. A taxpayer who pays dividends to its shareholders (owners) shall charge and withhold dividend tax in the amount of 30% of the accrued amount of payments from such payments, regardless of whether the issuer is a profit tax payer. Dividend tax is not applied in the case of payment of dividends in the form of shares (shares, units) issued by the bank that accrues dividends, provided that such payment in no way changes the proportions (shares) of participation of all shareholders (owners) in the authorized capital of the issuer. 3. The taxpayer-issuer of corporate rights reduces the amount of accrued income tax by the amount of dividend tax contributed to the budget. If the amount of tax paid on dividends exceeds the amount of tax liabilities of the issuing bank for profit tax of the reporting period, the difference is transferred to reduce the liabilities for profit tax of such bank in future tax periods in the manner prescribed by current legislation.Module. 4. As for the frequency of dividend payments, it is limited for joint-stock companies - once a year based on the results of the calendar year. This issue is regulated by the Law of Ukraine “On Business Companies” and Art. 9 of the Law of Ukraine “On Securities and Stock Exchange”. For other types of business entities, there are no legislative restrictions on the frequency of dividend payments.

When the charter is developed independently, how are changes registered?

Starting from the moment when a decision is made to increase the authorized capital, you need to submit documents to the Federal Tax Service of Russia for the purpose of state registration within a month.

Documents required for the tax office to be submitted in order to record changes:

1. The application form (P13001), which was approved on the basis of an order of the Federal Tax Service of the Russian Federation, is signed by the sole executive body of the LLC (general director). It is necessary to fill out the title page and sheet B. The application records the amount of the contribution, what property is being contributed to the authorized capital, what are the terms and procedure for making investments, and the shares that the participants of this fund want to have. 2. Changes made to the constituent documents of the LLC, as they increase the authorized capital. 3. Charter with new amendments. 4. Receipt stating that the state duty has been paid (800 rubles).

Based on practice, we can say that tax officers, in addition to the main list of documents, also ask for a calculation of net assets and a statement of losses and profits for the past year, which should have a mark on submission to the tax office. When the application is signed, the company registers the fact that all requirements regarding retained earnings have been met and that the amount of the increase in the authorized capital is not greater than the difference between the authorized capital (the reserve fund is added here) and the charter capital.

If the document undergoes state registration and changes are made to the Unified State Register of Legal Entities, the LLC tax authorities will issue both certificates indicating that the data has been entered into the Unified State Register of Legal Entities, based on form P50003.

In the case when the decision on changes to the Charter to increase the authorized capital was not made, along with the decision on increasing the capital, therefore the participants are reassembled to make such a decision. This can happen when a contribution is made in foreign currency, therefore the decision of the meeting participants must fix the amount of the contribution in Russian rubles, translated at the rate of the National Bank of Russia on the date on which this contribution was actually made.

Contributions when forming the authorized capital

The first stage of formation of the authorized capital is the determination of its size by the founders of the organization. At the same time, the size of the authorized capital must comply with the necessary legislative requirements.

The period during which the founders must contribute funds to the authorized capital account should not exceed 4 months from the date of state registration of the enterprise.

Contributions can be made either in full or in the amount of 50% upon the initial deposit.

The founder can make a contribution both in money and in material assets (movable and immovable property, machinery, equipment, etc.).

Payment of the authorized capital in accounting is reflected in the credit of account 80.

Examples of transactions for the formation of authorized capital on account 80

Let's look at an example:

The founders of Admiral JSC are V.I. Shestopalov. (18% shares) and Jupiter LLC (82% shares). The authorized capital of JSC Admiral is divided into 120 ordinary shares with a par value of 380 rubles per share.

In the accounting of Admiral JSC, entries were made on credit to account 80:

| Dt | CT | Description | Sum | Document |

| 75.01 | 80 | The debt of V.I. Shestopalov is reflected. for contribution to the authorized capital 120 pcs. * 380 rub./piece. * 18% | RUB 8,208 | Board minutes |

| 75.01 | 80 | The debt of Jupiter LLC is reflected. for contribution to the authorized capital 120 pcs. * 380 rub./piece. * 82% | RUB 37,392 | Board minutes |

| 50 | 75.01 | The debt of V.I. Shestopalov was repaid. | RUB 8,208 | Receipt cash order |

| 75.01 | The debt of Jupiter LLC has been repaid | RUB 37,392 | Bank statement |

What are the tax features when increasing the capital?

Taxes will have to be paid in the case where, as a result of the increased capital, the participant had income in the form of shares, even if the size of the share increased by 0.01%, or more due to the fact that the shares were distributed disproportionately as a result of the increase in the capital. If income is received as shares, increases in the value of shares, then the date recording the receipt of profit is fixed by the date of this decision.

Income tax is withheld by the Company from any funds that are transferred to the payer if they are actually paid to him or entrusted to other persons.

We can say that the payment of income tax on profits as shares of the management company is charged, as before, when the actual payment of this income to the individual occurs.