One of the ways to advertise and find new customers is to participate in exhibitions where samples of products are shown to potential buyers.

As a rule, such copies lose their original appearance and are subsequently either sold at a reduced price or written off. Tengiz Bursulaya, leading auditor of AKF MIAN CJSC, spoke about the accounting of exhibition samples.

In accounting, products intended for sale are accounted for in account 41 “Goods” (clause 2 of the Accounting Regulations “Accounting for Inventories” PBU 5/01, approved by Order of the Ministry of Finance dated June 9, 2001 No. 44n, Instructions for the Application of the Plan accounting accounts of financial and economic activities of organizations, approved by Order of the Ministry of Finance of October 31, 2000 No. 94n).

As for exhibition items, since the products may still be sold in the future, they continue to be counted as goods intended for resale. Consequently, the transfer of samples to the exhibition is reflected by an entry in subaccounts opened to account 41, or in analytical accounting, for example, like this:

Debit 41-5 Credit 41-1

– goods were transferred from the warehouse to the exhibition.

At the end of the exhibition and when transferring the samples to the warehouse, an entry is made in the accounting records as a debit to account 41-1 in correspondence with a credit to account 41-5. Such goods are accounted for at actual cost, which does not change in the future, except for cases established by the legislation of the Russian Federation (clauses 5, 12 of PBU 5/01).

Documenting

The internal movement of goods between divisions of one company - the warehouse and the department that will organize participation in the exhibition - is not regulated in any way. The organization itself decides what documents to formalize this procedure. For example, you can prepare the following set of documents: an order from the manager on the allocation of samples for the exhibition (Clause 2.2.6 of the Methodological Recommendations, approved by letter of Roskomtorg dated July 10, 1996 No. 1-794/32-5) - such an order can be given to him in orally; two invoices for internal movement in the TORG-13 form (Decree of the State Statistics Committee of December 25, 1998 No. 132) or in the company’s own form. The first invoice is for moving the demonstration goods to the exhibition, while in the “Sender” column you need to indicate the structural unit - the warehouse, and in the “Recipient” column - the department that will organize participation in the exhibition; the second is for moving from the exhibition to the warehouse.

On a note

By virtue of paragraph 4 of clause 4 of Article 264 of the Tax Code of the Russian Federation, non-standardized advertising expenses include expenses for the markdown of goods that have completely or partially lost their original qualities during exposure.

Write-off of product samples

Write-off of even small batches of goods - samples - must also be formalized. If samples are given free of charge to sales agents, partners, or displayed on shelves, the accountant must create a separate sub-account in the “Goods” account to reflect these transactions.

The transfer of free samples must be issued with an invoice for the release of materials to the third party in the form M-15. When transferring samples to sales agents and partners, documents are drawn up in accordance with the agreement with the future buyer. This can be formalized by an agreement, or it can be transferred without formalization. In the second case, it is necessary to make all the primary documents for the transfer and receipt of samples (for the process of acceptance of goods) and to write down the rationale for such transfer in internal documents.

If the samples are not transferred to anyone, but are needed to organize a tasting, then for this you need to issue an invoice in the TORG-13 form - for internal movement and save it for reporting. The invoice is signed by the employee who gives samples of goods to visitors for testing.

Please note that outsourced sample costs cannot reduce your taxable income as they are not advertising expenses. But the costs of tasting are normalized advertising costs of the reporting (tax) period. This will be counted as tax if the cost of tasting products does not exceed 1% of sales revenue.

Keep in mind that the tax code requires VAT to be paid on donated goods - samples fall under this category and tax must be paid on them.

Product losses

During the event, goods may completely or partially lose their consumer qualities or even become completely unusable due to damage or breakdown. In this situation, we should talk about non-standardized commodity losses. They can be documented in the following way: in accordance with the law, any fact of the organization’s economic activity is reflected on the basis of the primary accounting document. Let me remind you that this rule is enshrined in Article 9 of the Federal Law of December 6, 2011 No. 402-FZ.

As you know, the forms of primary accounting documents are approved by the head of the organization on the recommendation of the official responsible for maintaining records. At the same time, the development and approval of independent “primary” forms is a rather labor-intensive matter, so a company, as a rule, uses forms approved by the State Statistics Committee to reflect the facts of economic life.

To document losses of goods due to damage, damage, scrap of goods, Goskomstat Resolution No. 132 approved the following forms of documents: act on damage, damage, scrap of inventory items (form No. TORG-15); act on write-off of goods (form No. TORG-16).

To draw up an act in the TORG-15 form, a special commission is created in a trade organization, which includes a representative of the company administration and a financially responsible person. The document is drawn up in triplicate. The act indicates all the information about the product subject to markdown or write-off, namely: its name, price, quantity, article, grade, the reasons for the loss of goods, as well as the possibility of its further use - sale at a reduced price, disposal or destruction . The accountant must check the document signed by all members of the commission for completion and submit it for approval to the head of the organization, who makes the final decision regarding the use of the product.

One copy of the act remains in the accounting department, where, on its basis, losses are written off, the second remains in the department where product damage was detected, and the third is handed over to the financially responsible person.

If the goods are not subject to further sale, then act No. TORG-16 (or a document in the company form) is drawn up. It is also drawn up in triplicate and signed by the members of the commission. The act is approved by the head of the company, and he also decides from which source the damaged goods are written off. The act indicates all information about the product, as well as the reason for its write-off.

If the goods are subject to destruction, then in order to avoid their repeated write-off, they are destroyed in the presence of members of the commission.

How to document the write-off of illiquid inventory items

The procedure for writing off inventories is determined:

- based on materials - section. VI Guidelines for accounting of inventories (approved by Order of the Ministry of Finance of Russia dated December 28, 2001 N 119n) (hereinafter referred to as the Guidelines);

- on workwear and special equipment - section. IV Methodological guidelines for accounting of special tools, special devices, special equipment and special clothing (approved by Order of the Ministry of Finance of Russia dated December 26, 2002 N 135n).

To write off inventory items, by order of the head of the organization, a special commission is created, which includes financially responsible persons. These can be both employees of the organization and third parties.

The work of the commission should include sequentially the following stages (clause 125 of the Guidelines):

- inspection of inventory items;

- establishing the reasons why inventory items became illiquid;

- identification of persons responsible for damage to goods and materials;

- determining the suitability of inventory items for any further use (for its intended purpose, for another purpose, for sale, etc.);

- drawing up an act for writing off inventory items and its approval by management;

- determination of the residual (cost of scrap, scrap) or market value of inventory items;

- control over the disposal of unusable goods and materials.

It is necessary to draw up an act recording the damage to inventory items, as well as an act for their write-off. An organization may approve in its accounting policy the use of forms NN TORG-15 “Act on damage, damage, scrap of inventory items” and TORG-16 “Act on write-off of goods” (approved by Resolution of the State Statistics Committee of Russia dated December 25, 1998 N 132) or others independently developed forms containing the mandatory details established by Part 2 of Art. 9 of the Federal Law of December 6, 2011 N 402-FZ “On Accounting” (Part 4 of Article 9 of the Federal Law N 402-FZ).

We recommend paying attention to the following details:

- The name of the written off inventory items should be as detailed as possible. Otherwise, organizations may be subject to claims from tax authorities due to the inability to accurately identify inventories being written off.

- The act must indicate in detail the reason why inventory items are subject to write-off, which can confirm the economic justification of this fact of economic activity, which is the main requirement for recognizing an expense (paragraph 2, clause 1, article 252 of the Tax Code of the Russian Federation). For example, the requirement to write off a number of inventory items due to the expiration of their shelf life is directly provided for by current legislation and does not require any other additional grounds (clause 2, article 3 of the Federal Law of January 2, 2000 N 29-FZ “On the quality and safety of food products").

- Losses (shortages) within the limits of natural loss norms approved by law are part of material expenses and are subject to write-off for profit tax purposes in accordance with paragraphs. 2 clause 7 art. 254 Tax Code of the Russian Federation.

- To confirm the economic feasibility of writing off inventory items as a result of loss of physical qualities and properties, it is recommended to describe the defects that the inventory received. This information will also be required both to confirm the economic feasibility of the write-off, and, subsequently, to determine the residual (market) value of inventory items.

- Since the procedure for recognizing inventory items as illiquid, provided for by the Methodological Instructions, includes control over the disposal of unusable inventories (clause “h” of paragraph 125 of the Methodological Instructions), when writing them off, it is necessary to indicate information either about the document certifying the fact of disposal, or directly about the fact itself recycling, if the organization does not provide for the preparation of a separate document on this fact.

Sales at a reduced price

If an exhibition copy has lost its original appearance or partially lost its consumer qualities, then it can subsequently be sold at a reduced price. In this case, you should pay attention to the following points.

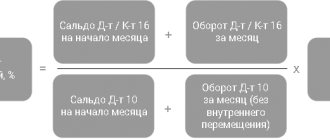

Thus, in accounting there is a need to recognize a reserve for reducing the value of inventories (clauses 2, 3 of the Accounting Regulations “Changes in Estimated Values” (PBU 21/2008), approved by Order of the Ministry of Finance dated October 6, 2008 No. 106n).

A change in the estimated value when the cost of inventories decreases is included in the company’s other expenses (clause 4 of PBU 21/2008, clause 11 of the Accounting Regulations “Expenses of the Organization” PBU 10/99, approved by Order of the Ministry of Finance dated May 6, 1999 No. 33n, p 20 Guidelines for accounting of inventories, approved by Order of the Ministry of Finance dated December 28, 2001 No. 119n).

The amount of the reserve is determined as the difference between the current market value of the product and its actual cost. According to paragraph 9 of PBU 5/01, the current market value is understood as the amount of funds that can be received as a result of the sale of assets. It is determined on the basis of available information and must be confirmed (paragraph 3, 7, paragraph 20 of the Guidelines for accounting for inventories).

The creation of a reserve in accounting is reflected in the debit of account 91 “Other income and expenses”, subaccount 91-2 “Other expenses”, in correspondence with the credit of account 14 “Reserve for reduction in the value of material assets” (clause 20 of the Guidelines for accounting for inventories , Instructions for using the Chart of Accounts):

Debit 91-2 Credit 14

– a reserve has been created in accounting.

If at the end of the year the exhibition samples were not sold, then in the balance sheet (section “Current assets”, line “Inventories”) they will be reflected at actual cost minus markdowns. The amount of the reserve for a decrease in the value of inventories is indicated in the explanation to the balance sheet in section 4.1 “Availability and movement of inventories” (Section 4 of Appendix No. 3 to Order of the Ministry of Finance dated July 2, 2010 No. 66n).

On a note

The procedure for calculating the markdown of the Tax Code has not been specified; accordingly, when determining its value, the Law on Accounting can be applied.

I believe that a markdown can be recognized as an expense in an amount calculated as the difference between the cost of purchasing samples and the market value.

Write-off of goods sold: postings

The fact of sale of goods, i.e. paid transfer of ownership rights to them is recorded in accounting by writing off their cost from the credit account. 41 to the debit of the sales account - which is the main one for recording sales and combining information on revenue, costs and results obtained.

The sale of goods with revenue recognition at the time of shipment is recorded using the following transactions:

| Operations | D/t | K/t |

| Sales revenue taken into account | 62 | 90/1 |

| Cost of goods sold written off | 90/2 | 41 |

| VAT is charged on the cost of goods sold | 90/3 | 68 |

| Sales-related costs written off | 90/2 | 44 |

| Payment received from buyers | 51 | 62 |

If the contract provides for the transfer of ownership of goods not upon shipment, but, for example, after payment, then the transactions formalizing the transaction will be different, and the goods will be written off not from account 41, but from the “Goods shipped” account:

| Operations | D/t | K/t |

| Goods shipped | 45 | 41 |

| VAT charged at the time of shipment | 76 | 68 |

| Receipt of payment | 51,52 | 62 |

| Sales revenue recognized | 62 | 90/1 |

| Cost of goods sold written off | 90/2 | 45 |

| Accrued VAT included | 90/3 | 76 |

| Sales-related costs written off | 90/2 | 44 |

Income tax

As for the formation of a reserve for reducing the value of material assets for income tax, Chapter 25 of the Tax Code of the Russian Federation does not provide for such a possibility.

At the same time, by virtue of paragraph 4 of clause 4 of Article 264 of the Tax Code of the Russian Federation, non-standardized advertising expenses include expenses for the discounting of goods that have completely or partially lost their original qualities during exposure.

The procedure for calculating markdowns is not defined by the Tax Code; accordingly, according to paragraph 1 of Article 11 of the Tax Code of the Russian Federation, when determining its value, the Accounting Law can be applied. I believe that a markdown can be recognized in expenses in the amount calculated as the difference between the costs of purchasing samples and the market value determined by an expert. In this case, the amount of the markdown will be equal to the amount of the reserve created in accounting.

On a note

When selling a product for which a reserve was created to reduce the price, its purchase price will correspond to the difference between the actual cost and the amount of the restored reserve. In this regard, there are no differences between accounting and tax profit.

HOW TO REFLECT EXHIBITION SAMPLES OF PRODUCTS IN ACCOUNTING?

Trade organizations often place some of their goods or products as samples in the showroom. Subsequently, some exhibits completely lose their marketable appearance and have to be written off, while others can be sold at a discount. This article describes how organizations using the OSNO or simplified tax system can correctly record the receipt, markdown and write-off of exhibition samples.

Introductory part

Recently, many trading companies have been creating showrooms (another name is “show room”). Most often, sellers of large-sized products do this: furniture, prefabricated houses, etc. Product samples are displayed in the hall so that customers can familiarize themselves with them and make a choice. After the client has made payment, he is given not an exhibition sample, but exactly the same product stored in a warehouse. Meanwhile, the sample continues to stand in the hall, attracting new buyers.

This method of trading is very convenient. Firstly, it allows the seller to save on payment for services for assembling and disassembling the product, because the client takes the product in disassembled form and pays for installation himself. Secondly, the goods in the warehouse are stored in packaging that can protect them during transportation. As for the sample from the exhibition, after assembly, disassembly and repackaging, it is no longer so reliably protected and can be damaged on the road. To avoid customer complaints, traders prefer to ship products not from the showroom, but from the warehouse.

As a rule, over time, samples lose their original qualities: the colors fade, the upholstery wears out, etc. In such a situation, sellers usually sell samples at a discount. If, after being in the showroom, the products become completely unusable, the dealer will only have to write them off. How can an accountant correctly record each of these transactions?

Receipt of samples

Strictly speaking, samples are goods because the organization subsequently expects to sell them. Products purchased from a third-party supplier must be reflected in the debit of account 41 subaccount “Goods used as samples.” If the company sells products of its own production, samples must be reflected in the debit of account 43 subaccount “Finished products used as samples.”

Some organizations account for samples worth more than 40,000 rubles as fixed assets. This is not entirely correct, but sometimes it is still justified, especially if the exhibit performs not only basic but also additional functions (for example, a manager sits in the “exhibition” house and concludes contracts). In addition, by reflecting samples on account 01, the seller has the opportunity to account for them separately from other products stored in disassembled form, which is very convenient. In our opinion, this method is completely acceptable and has a right to exist.

Selling an exhibit at a reduced price

By selling an exhibition sample at a reduced price, the company incurs certain losses. How to reflect them in accounting?

If the sample is capitalized as a product or as a finished product, it is best to make a markdown in advance (that is, before sale). To do this, the manager must sign the appropriate order, on the basis of which a commission will be created. She will decide on the markdown and draw up a corresponding act. You can mark down an exhibit regularly, for example, once a month or quarter. Another option is to discount the sample once, immediately before selling it.

Please note: after the markdown, the cost of the sample reflected in invoice 41 or 43 will remain the same. The fact is that paragraph 12 of PBU 5/01 “Accounting for inventories” prohibits changing the actual cost at which inventories are accepted for accounting. The results of the markdown will be reflected as the financial result from the sale of the property*.

In tax accounting, the amount reflected in the act can be written off as advertising costs on the basis of paragraph 4 of Article 264 of the Tax Code of the Russian Federation. It states that advertising costs, among other things, include the costs of discounting goods that have completely or partially lost their original qualities during exhibition. Taxpayers using the simplified tax system with the object “income minus expenses” are guided by subparagraph 20 of paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation. It allows “simplifiers” to reduce taxable income by advertising costs, which are accepted in the manner prescribed by Article 264 of the Tax Code of the Russian Federation.

Example 1

An organization selling furniture purchased a table at a price of 11,800 rubles. (including VAT 18% - 1,800 rubles). This product was placed in the showroom as an exhibit. They planned to sell it after the lease for the exhibition hall expired. The accountant made the following entries: DEBIT 41 subaccount “Goods used as samples” CREDIT 60 - 10,000 rubles. (11,800 - 1,800) - reflects the cost of the goods received; DEBIT 19 CREDIT 60 – 1,800 rub. — “input” VAT is reflected.

Shortly before the end of the lease, a commission was created that decided to discount the table to 6,000 rubles. Soon the product was sold at a price of 7,080 rubles. (including VAT 18% - 1,080 rubles). The following entries appeared in accounting: DEBIT 41 subaccount “Goods for sale” CREDIT 41 subaccount “Goods used as samples” - 10,000 rubles. — revenue from the sale of the table is reflected; DEBIT 62 CREDIT 90 – 7,080 rub. — revenue from the sale of the table is reflected; DEBIT 90 CREDIT 68 – 1,080 rub. — VAT charged; DEBIT 90 CREDIT 41 subaccount “Goods for sale” – 10,000 rubles. — the purchase price is reflected; DEBIT 99 CREDIT 90 – 4,000 rub. (7,080 - 1,080 - 10,000) - reflects the loss from the sale of the table.

In tax accounting, the organization reflected advertising expenses in the amount of 4,000 rubles.

If the exhibit is put on the balance sheet as a fixed asset, a markdown will not be necessary. In this case, the company will charge depreciation monthly and charge it to expenses. The sale of an exhibition sample should be reflected as the sale of a “regular” OS.

Disposal of a sample that has become unusable

Exhibits that have completely lost their marketable appearance must be written off. To do this, it is necessary to create an inventory commission that will record the presence of products unsuitable for sale (usually an act is drawn up in form No. TORG-16). Next, the cost of samples capitalized as goods or as finished products should be reflected in the debit of account 44 “Sales expenses”.

In tax accounting, the cost of written-off exhibits can be included in advertising expenses, because these include, among other things, amounts spent on decorating sample rooms and showrooms (Clause 4 of Article 264 of the Tax Code of the Russian Federation). In a simplified system with the object “income minus expenses,” writing off samples also applies to advertising costs (subclause 20, clause 1, article 346.16 of the Tax Code of the Russian Federation).

Example 2

An organization selling furniture purchased a cabinet at a price of 23,600 rubles. (including VAT 18% - RUB 3,600). This product was placed in the showroom as an exhibit.

The accountant made the following entries: DEBIT 41 subaccount “Goods used as samples” CREDIT 60 - 20,000 rubles. (23,600 - 3,600) - reflects the cost of the goods received; DEBIT 19 CREDIT 60 – 3,600 rub. — “input” VAT is reflected.

A year later, the company conducted an inventory, which showed that the exhibit had fallen into disrepair and could not be sold. Based on the results of the inventory, it was decided to write off the sample. The following entry appeared in accounting: DEBIT 44 CREDIT 41 “Goods used as samples” - 20,000 rubles. — the cost of the sample is written off as current expenses.

Advertising expenses in the amount of 20,000 rubles appeared in tax accounting.

If an exhibition sample is capitalized as a fixed asset, it must be written off in the same way as any other fixed asset.

*Hereinafter it is assumed that the trading company keeps records in purchase prices.

Application of PBU 18/02

The amount of markdown of goods exhibited at the exhibition is recognized in the same month in which the reserve is created.

In this regard, there are no differences in accounting and tax accounting, which are taken into account in the manner established by the Accounting Regulations “Accounting for Income Tax Calculations” PBU 18/02, approved by Order of the Ministry of Finance dated November 19, 2002 No. 114n.

When selling a product for which a reserve was created to reduce the price, its purchase price will correspond to the difference between the actual cost and the amount of the restored reserve. In this regard, there are no differences between accounting and tax profit.