Control over the calculation and payment of insurance premiums intended for the Pension Fund, Compulsory Medical Insurance Fund, Social Insurance Fund (except for contributions for injuries) has been transferred to the tax authorities. The calculation rules and description of the procedure for paying contributions to those who replaced the administrator were included as an integral part in the text of the Tax Code of the Russian Federation. These changes have led to the fact that insurance premiums have become subject to most of those provisions of tax legislation that are common to all tax payments. It is precisely because of this that the use of the term “taxes to extra-budgetary funds” has become fair in relation to insurance premiums (

Rules for calculating and paying contributions

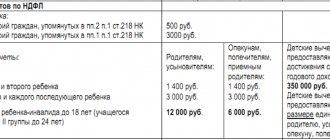

The main points about paying insurance premiums are presented in the table:

| Payer | Difference | general |

| employers | all 4 types of contributions (pension, medical and social insurance (sick leave and maternity), injuries) intended for all 3 extra-budgetary funds (PFR, MHIF, Social Insurance Fund). The basis for their calculation is income paid to employees. Reporting on accrued/paid/used contributions is generated quarterly. | accruals are made by them independently; • the billing period, defined as a year, is the same; • payment to each fund is calculated and paid separately; • when calculating contributions, the same basic tariffs are applied; • established deadlines are subject to the rule of being postponed to a later date if they fall on a weekend; • the same rules for processing payment documents are used. |

| self-employed persons | Contributions are paid only to the Pension Fund and the Compulsory Medical Insurance Fund; The volume of their payments to each of the funds depends on the federal minimum wage established at the beginning of the year and is fixed in nature, but for accruals to the Pension Fund it can acquire a variable part; Reporting is not provided and, as an exception, is submitted only by the heads of peasant farms that ceased operations before the end of the accounting year. |

Contributions from the income of employees are calculated by employers monthly when calculating salaries for the next month and are also paid monthly (but in the month following the billing month). The last day of payment for all types of contributions is the same - the 15th

The accrual base is formed on an accrual basis from the beginning of the year, and the amount that is actually accrued for the last month of the period is actually subject to monthly payment. The basis is reduced by payments that are not subject to taxation.

Payments to extra-budgetary funds in 2021 for individual entrepreneurs

Legislative dispositions indicate that an individual entrepreneur is obliged to make all required contributions without any exceptions.

Every year the norms undergo direct additions, so the procedure for making payments, as well as their size, change.

Next, we will tell you about the federal contributions and payments that will need to be made in 2021. At the same time, we will also present some regional tariffs.

How much are insurance contributions to extra-budgetary funds in 2021?

Due to the indexation of the minimum wage from January 1, 2021, all fixed insurance (basic) premiums and taxes for individual entrepreneurs have increased more. Now an individual entrepreneur with a total annual salary of 300,000 rubles. and only two payments are paid less in their respect for a total amount of 23,153.33 rubles.

Official individual entrepreneurs with a total income of more than 300,000 rubles. contribute for themselves (plus the indicated amount of 23,153 rubles) further 1% of the profit that exceeds 300,000 rubles.

Individual entrepreneurs also pay prescribed fixed insurance funds for themselves through a single payment document (or one receipt/official payment order). The Pension Fund of Russia now independently divides the entire amount paid into the calculated insurance and savings shares (if any). That is, the following is necessary:

- It is allowed to pay taxes either quarterly or once a year;

- The entire amount of paid specified contributions can be reduced and the simplified tax system “profit” (6%).

Individual entrepreneurs pay social contributions to the Compulsory Medical Insurance Fund. This is another extra-budgetary body.

The fixed insurance payment to the FFOMS for 2021 is 316.40 rubles. per month (it turns out 949.21 rubles for the quarter, 3796.85 rubles for the year).

Enrollment in the state FFOMS for profits greater than 300,000 rubles. are not provided.

On topic: Amnesty 2021 in Russia in criminal cases: latest news

Table of insurance contributions to extra-budgetary funds 2018

All designated receipts are drawn up only according to form No. (in words) PD or according to sample No. PD-4sb (withholding) and are accepted for crediting only at Sberbank (when an individual entrepreneur has a current account in a third-party bank, it means that you should pay from that bank, no additional commissions for this are not charged). When structuring receipts for payment of contributions for extra-budgetary areas, you should know the indicated BCC (or Budget Classification Codes). All BCCs can always be viewed on the Pension Fund of Russia resource.

When you are directly registered as an individual entrepreneur only at the beginning of the year, you should pay extra-budgetary contributions not for the current year, but for the entire time that the entities are registered (to approximately calculate the state payment and enter all receipts, you need to use an accounting resource). When the work of an individual entrepreneur is combined with activities under an employment contract, and the boss is already making extra-budgetary payments - here you still need to make all the payments specified and fixed only for the individual entrepreneur.

Table:

After this, be sure to save the paid receipts of extra-budgetary payments. Because reporting since 2012 for individual entrepreneurs without workers (calculating only for themselves) has been abolished.

To track whether all payments have reached the place of claim, call the address district office of the Pension Fund of the Russian Federation and contact the employee authorized for individual entrepreneurs without a staff.

Next, the entire amount of contributions made can be reduced by the amount of the prescribed tax (which is paid according to the 6% “profit” system). This is an easy way to save on government funds.

The designated Fixed Insurance Funds are calculated based on the minimum wage in effect as of January 1, 2021. When the minimum wage is indexed in Russia during the period, state insurance enrollments as of the year DO NOT change.

https://www.youtube.com/watch?v=z11-Dyh3cb0

For example, a subject uses basic tariffs independently. If there is no excess of state prerequisites, then the standard formula for all funds will appear here. It turns out the following:

- The specified 6.2 thousand rubles are contributed to the Russian Pension Fund. it turns out 30 thousand * 22%;

- In further MHIF cash 30 thousand * 5.1% amount - 1530 rubles;

- It is also calculated in the Social Insurance Fund 30 thousand * 2.9% comes out to 870 rubles.

As a result, we get the following: 6.2 thousand + 1530 + 870 = 9 thousand.

Rates of insurance contributions to state extra-budgetary funds

You can view the current rates in the rates table above. Reporting is submitted in the order of administration to each fund separately.

If you have questions, consult a lawyer

You can ask your question in the form below, in the online consultant window at the bottom right of the screen, or call the numbers (24 hours a day, 7 days a week):

- 7

— Moscow and region; - 7

— St. Petersburg and region; - 7

— all regions of the Russian Federation.

(1 4,00 of 5) Loading...

Source: https://ogic.ru/pravo/straxovye-vznosy-vo-vnebyudzhetnye-fondy-v-tablice.html

Off-budget funds rates

Contributions are calculated taking into account the maximum base. It depends on it at what rate to make contributions to the funds in 2021.

Limit base for calculating insurance premiums:

- for compulsory pension insurance in 2021 is equal to RUB 1,021,000,

- for social insurance - 815,000 rubles.

When these values are reached, the rate for calculating contributions changes.

The table shows the rates that apply to legal entities:

| Type of insurance premium | Within the established limit base | Above the established limit base |

| Contributions to OPS | 22% | 10% |

| Contributions for temporary disability and maternity insurance | 2,9% | – |

| Social insurance contributions for foreign citizens temporarily staying in the Russian Federation. | 1,8% | – |

| Contributions to compulsory medical insurance | 5,1% | – |

Organizations that are on the simplified tax system, whose annual income exceeded 79 million rubles, lose the right to a reduced tariff, and contributions must be paid in accordance with the basic tariffs. Previously there was no such restriction.

Deadlines for contributions to extra-budgetary funds – Legalists

How to calculate the tax base Organizations and individual entrepreneurs separately calculate the base for each employee and for each contractor.

The taxable base is calculated on an accrual basis from the beginning of the billing period, which corresponds to one calendar year.

In other words, the base is determined during the period from January 1 to December 31 of the current year, then the calculation of the taxable base begins from scratch. The base is determined at the end of each month after salary calculation.

The taxable base for contributions in case of temporary disability and in connection with maternity should not exceed the maximum amount. Its value is approved by law and is indexed annually by decree of the Government of the Russian Federation.

In 2015, the size of the maximum base is 670,000 rubles. This means that contributions are accrued until the employee’s tax base reaches 670,000 rubles. Payments in excess of this amount are exempt from contributions.

Funds are used to provide assistance to the disabled, large and single-parent families.

From the funds received from the services provided, income is generated, which is used for the development and maintenance of social assistance departments.

Important

on the topic The correctly chosen tax regime for your organization guarantees at a minimum savings and optimization of tax payments, as well as minimizing the costs of maintaining tax and accounting records.

In the tax code at the moment there are only two types of regime: special and general (UTII, simplified tax system, unified agricultural tax). Instruction 1 Any tax regime can be applied by both individual entrepreneurs and legal entities, except for UTII based on a patent.

Insurance contributions to extra-budgetary funds in 2018

Attention

Sanctions for late payment of STS Responsibility regarding STS arises for the taxpayer when the reason for their non-payment is:

- during the calculation, the base for STV accruals was underestimated, that is, the policyholder missed out on some amount subject to STV;

- incorrect calculation of STV.

For example, the policyholder used a reduced tariff in the calculation completely unreasonably;

- other actions (inactions) of the entrepreneur-insurer that are recognized as unlawful.

- overdue for more than 30 calendar days. days

Fines: Violation Fine, % of the unpaid amount Delay in reporting 5.0 Minimum 1000.0 rub.

and a maximum of 30% of the total payment amount

Underestimation of the base - the basis for determining the amount of STV 20.0 Intentional non-payment of STV 40.0 When an enterprise missed the deadline for paying STV, the penalty begins to increase from the next day.

Its size is (in%):

How are insurance premiums paid to extra-budgetary funds in 2018?

Funds are accumulated in the Pension Fund;

- from accidents that may occur during the production process, from occupational diseases. Funds are transferred to the Social Insurance Fund;

- medical (MHIF).

Funds should be transferred unconditionally to extra-budgetary funds:

- Persons paying salaries and other types of remuneration to employees:

- companies and firms with the status of legal entities;

- IP;

- individuals without individual entrepreneur status.

- Businessmen practicing privately according to the rules established by law.

Their distinctive feature is that entrepreneurs work independently and do not have official employees or assistants who are paid wages.

Important! When the STV payer can simultaneously be classified into several categories, then he is obliged to pay funds for each basis separately.

Insurance contributions from wages

Contribution rate for transfers to a foreign worker: For which person is the payment made by the Pension Fund of the Federal Compulsory Medical Insurance Fund FSS For a person who is considered a resident of the country and is not a highly qualified specialist 22% 5.1% 2.9% For a person who resides on a temporary basis within the country and is not is a qualified specialist 22 5.1 2.9% For a person who is temporarily in Russia and does not belong to the category of highly qualified personnel 22 01 1.8% For a highly qualified resident worker 22 0 2.9% For foreigners who temporarily reside in Russia and are considered highly qualified employees 22 0 2.9% For temporarily staying foreigners classified as highly qualified specialists 0 0 0% Tariffs and rules for transferring insurance amounts for a compulsory type of insurance against accidents and occupational diseases have been established since 2006 (according to the law of December 22, 2005 year No. 179-FZ).

February 16 is the deadline for paying insurance contributions to extra-budgetary funds

Timing and sequence of payment of STV to extra-budgetary funds The period of time that determines the payment of STV has remained unchanged for several years. All ETS must be deposited into the appropriate funds by the 15th of the following month.

This date is the final date. But if it falls on a holiday or weekend, then the deadline is moved to the next working day.

It is important not to forget that:

- STV accounting is maintained and payment is made in rubles.

Insurance contributions to extra-budgetary funds

Taxable payments include the following:

- compensation for unused vacations;

- financial assistance, which is paid to the family of the deceased employee;

- funds that are paid to employees who have difficult working conditions;

- price of workwear;

- the price of travel benefits that were provided to those who study and are brought up.

In 2021, the following tariffs apply: Conditions of the Pension Fund of the Federal Compulsory Medical Insurance Fund FSS Limit standards are established by Art.

58 part 1 of Law No. 212-FZ and amount to 670 thousand rubles in the Social Insurance Fund, 711 thousand.

4.6. payments to extrabudgetary funds

Payments are made separately to each fund. The object of accrual of insurance amounts that are transferred by employers and persons who pay only for themselves is the same.

All transfers to employees will be subject to a contribution if the accrual is made in accordance with: Payment should be made in relation to the type of insurance for which the person is insured according to the norms of the document from: The base is determined on an accrual basis from the beginning of the tax period (Art.

8, 10 of Law No. 212-FZ). If the established limit is exceeded, funds from the amount that is in excess of the limits will not be charged.

Every year, income is indexed in accordance with government regulations, based on earnings growth.

The base will include funds that are paid to individuals, without taking into account the fact whether they are considered expenses, which will reduce the income tax base.

Deductions to extra-budgetary funds deadlines

Pension Fund 22% 5.1% 2.9% Tariff that is set above the limit 10% 0% 0% IT companies 8% 4% 2% Firms that pay wages or benefits to a ship’s crew member (clause 9 of the same article) 0 % 0% 0% NPOs, pharmacy chains, simplified enterprises 20% 0% 0% Participants in the Skolkovo project 14% 0% 0% Participant in the free economic zone 6% 0.1% 1.5% Resident within the framework of advanced social economic development 6% 0.1% 1.5% Additional tariffs in the Pension Fund of the Russian Federation are established taking into account the class of working conditions (after a special assessment).

Deadlines for contributions to extra-budgetary funds

Moreover, this year, insurance contributions to the Pension Fund are made using one general payment order without breaking down into savings and insurance parts. Monthly mandatory contributions are paid by companies and enterprises within strictly defined deadlines.

Payment is made and transferred by the 15th day of the month following the month of assessment. The category of the reporting period is determined by one quarter, the first half of the year, 9 months and a year.

Various penalties are provided for violations of the rules for deductions and payments to extra-budgetary funds.

If insurance premiums are paid at a later date, penalties will be charged.

https://www.youtube.com/watch?v=kZR9vsNnODY

For each day they amount to one three hundredth of the Central Bank refinancing rate for the specified period.

Moreover, penalties can be forcibly collected by withdrawing them from the bank accounts of the defaulter or at the expense of his property.

“Individuals” transfer medical contributions no later than December 31 of the current year.

And those of them who have voluntarily insured themselves in case of temporary disability and in connection with maternity make transfers to the Social Insurance Fund no later than December 31 of the current year.

If the last date for payment of contributions falls on a weekend or holiday, you can transfer the money on the first working day following it, and this will not be considered late.

When to report on contributions For employers, the acceptable deadlines for submitting calculations on accrued and paid contributions to the Pension Fund and the Federal Compulsory Medical Insurance Fund since 2015 depend on the form in which the reporting is submitted: “on paper” or electronically. Thus, you should report to the Pension Fund “on paper” no later than the 15th day of the second calendar month following the reporting period (quarter, half-year, nine months and year).

Source: https://zakonbiz.ru/sroki-otchislenij-vo-vnebyudzhetnye-fondy/

Reduced insurance premium rates

| Policyholders | Pension Fund | FSS | Compulsory Medical Insurance Fund |

| Companies, firms, individual entrepreneurs on the simplified tax system. A prerequisite is a maximum income of 79 million rubles. | 20,0 | 0 | 0 |

| Pharmacy establishments, individual entrepreneurs that have received a license to sell dosage forms on UTII. Reduced rates - only for workers engaged in pharmacy activities | 20,0 | 0 | 0 |

| IP for PSO | 20,0 | 0 | 0 |

| IT companies and firms | 8,0 | 2,0 | 4,0 |

| Participants of the Skolkovo project | 14,0 | 0 | 0 |

| Enterprises involved in free economics. zone in Crimea | 6,0 | 1,5 | 0,1 |

Insurance premium rates 2021 for individual entrepreneurs

Since 2021, the amount of individual entrepreneur contributions is not tied to the minimum wage. The Tax Code of the Russian Federation now specifies the amount of fixed payments in rubles

For entrepreneurs whose income does not exceed 300 thousand rubles, the amount of contributions for compulsory pension insurance and compulsory health insurance is paid in a fixed amount.

However, individual entrepreneurs whose annual income is more than 300 thousand rubles must pay additional pension contributions at a rate of 1%. That is, if the income of an individual entrepreneur for a year exceeds 300 thousand rubles, then in addition to fixed contributions, the entrepreneur must transfer to the Federal Tax Service an additional amount in the amount of 1% of the amount exceeding the limit (clause 1 of Article 430 of the Tax Code of the Russian Federation).

Insurance premium rates for individual entrepreneurs

| Type of contribution Rate Amount | Type of contribution Rate Amount | Type of contribution Rate Amount |

| Fixed contributions to pension insurance if the amount of income for the year does not exceed 300 thousand rubles | – | RUB 26,545 |

| Additional contributions to pension insurance if the amount of income for the year is more than 300 thousand rubles | 1% | 1% of the amount of the individual entrepreneur’s annual income, reduced by 300,000 rubles. |

| Fixed premiums for health insurance | – | RUB 5,840 |

When do you need to report contributions (deadlines)

| Fund | Reporting on paper | Electronic reporting |

| Pension Fund | no later than the 15th day of the second calendar month following the reporting period | no later than the 20th day of the second calendar month following the reporting month. |

| FFOMS | ||

| FSS | no later than the 20th day of the calendar month following the reporting period | no later than the 25th |

Monthly reporting to the Pension Fund of the Russian Federation in the form SZV-M

According to the Resolution of the Board of the Pension Fund of February 1, 2016 No. 83p, the SZV-M form is intended to reflect information about insured persons - employees of companies and individual entrepreneurs.

Employers submit the SZV-M report to the Pension Fund of Russia every month before the 15th.

The procedure for filling out the report provides for the reflection of all employees of organizations and individual entrepreneurs: actually working, absent due to illness, on vacation, etc.

It is important to note that the SZV-M includes information about those working both under an employment contract and under the GPA.

Legislators do not plan to introduce a new SZV-M form in 2021; the report is submitted on the form approved in December last year.

Penalties for non-payment of insurance premiums

For non-payment of insurance payments, legislative acts provide for the following sanctions:

- Penalties for each day of non-payment in the amount of 1/300 of the refinancing rate (from October 1, 2021, it is planned to increase the penalty for non-payment for organizations to 1/150 of the refinancing rate if the delay exceeds 30 days).

- The fine for non-payment is 20% of the debt amount if the violation of the law was not planned (in other words, you might have forgotten to transfer money to the Federal Tax Service).

- A fine of 40% of the outstanding premiums if the non-payment is intentional (for example, you deliberately do not pay payments or lower the insurance rate).

It is worth noting that the above measures are taken in relation to the following offenses related to non-payment of contributions:

- Lack of payment;

- Failure to meet the payment deadline;

- Partial payments;

- Incorrect payment calculation (for example, you made a mistake in some number);

- Understating the basis for calculating contributions.

Contributions to extra-budgetary funds in 2021

Insurance contributions to extra-budgetary funds in 2018

Listed by entrepreneurs, employers and self-employed persons. An individual entrepreneur whose staff includes employees is obliged to transfer funds not only for himself, but also for his employees.

STV refers to amounts intended for pension insurance. Funds are accumulated in the Pension Fund; from accidents that may occur during the production process, from occupational diseases.

Insurance contributions to extra-budgetary funds in 2021 in the table

When you are directly registered as an individual entrepreneur only at the beginning of the year, you should pay extra-budgetary contributions not for the current year, but for the entire time that the entities are registered (to approximately calculate the state payment and enter all receipts, you need to use an accounting resource). When the work of an individual entrepreneur is combined with activities under an employment contract, and the boss is already making extra-budgetary payments - here you still need to make all the payments specified and fixed only for the individual entrepreneur.

When you are directly registered as an individual entrepreneur only at the beginning of the year, you should pay extra-budgetary contributions not for the current year, but for the entire time that the entities are registered (to approximately calculate the state payment and enter all receipts, you need to use an accounting resource). When the work of an individual entrepreneur is combined with activities under an employment contract, and the boss is already making extra-budgetary payments - here you still need to make all the payments specified and fixed only for the individual entrepreneur.

Insurance premium rates in 2021: table

According to paragraph 1 of Article 419 of the Tax Code of the Russian Federation, insurance companies pay:

- individual entrepreneurs.

- persons making payments and other rewards to citizens;

If an entrepreneur has employees or makes payments to other persons, he simultaneously belongs to both the first and second groups of insurance premium payers.

This means he pays contributions both as an employer and for himself personally.

What taxes should I pay to the funds in 2021?

The calculation rules and description of the payment procedure for those who replaced the administrator were included as an integral part in the text of the Tax Code of the Russian Federation.

These changes have led to the fact that insurance companies have become subject to most of those provisions of tax legislation that are common to all tax payments. It is precisely because of this that the term “taxes to extra-budgetary funds” has become fair in relation to insurance premiums.

According to paragraph 1 of Article 419 of the Tax Code of the Russian Federation, insurance premiums are paid by:

- individual entrepreneurs.

- persons making payments and other rewards to citizens;

If an entrepreneur has employees or makes payments to other persons, he simultaneously belongs to both the first and second groups of insurance payers.

This means he pays contributions both as an employer and for himself personally.

We recommend reading: Direct communication with Shoigu

Contributions are made by entrepreneurs, employers and self-employed persons. An individual entrepreneur whose staff includes employees is obliged to transfer funds not only for himself, but also for his employees.

STV refers to amounts intended for pension insurance. Funds are accumulated in the Pension Fund; from accidents that may occur during the production process, from occupational diseases.

Responsibility for non-payment of insurance premiums

There are the following types of liability for non-payment of contributions:

- Tax - occurs in case of minor errors made by an individual entrepreneur or an official of the company. In such a situation, a penalty is charged.

- Administrative – occurs when gross errors are made, which lead to a significant reduction in the base for calculating contributions, and, consequently, a decrease in the amount of the latter.

- Criminal - occurs in extreme cases when the amounts of debt are too large. Ordinary organizations with a small overdue payment are not afraid of this type of liability.

Criminal prosecution may have the following consequences:

- An individual (IP) can be fined up to 300,000 rubles and arrested for up to 36 months;

- An official of an organization may be imprisoned for up to 6 months, fined up to 500,000 rubles, or required to vacate his position for a period of up to 3 years.

Rate the quality of the article. Your opinion is important to us: