Legislative acts on insurance premiums

The listed changes were put into effect on the basis of Federal Law dated July 3, 2016 No. 243-FZ and Federal Law dated July 3, 2016 No. 250-FZ. They provide for the following changes:

- in January 2021, Chapter 34 entitled “Insurance premiums” was added to the Tax Code of the Russian Federation. It contains articles 419 to 432, which set out the rules for calculating and paying contributions;

- Amendments have been made to the first part of the Tax Code of the Russian Federation. According to the innovations, all basic principles that previously applied only to taxes now apply to insurance premiums;

- Federal Law No. 212-FZ of July 24, 2009 on insurance premiums is no longer in force;

- The new version of the Federal Law dated 01.04.96 No. 27-FZ “On Individual Accounting...” comes into effect;

- The new version of the Federal Law of December 29, 2006 No. 255-FZ “On Compulsory Social Insurance...” comes into effect;

- The new version of the Federal Law of July 24, 1998 No. 125-FZ “On compulsory social insurance against accidents...” comes into force.

Insurance premiums

Insurance premiums provided for in Ch. 34 Tax Code of the Russian Federation

Salary as a payment made to an employee within the framework of an employment relationship is subject to insurance contributions for compulsory pension insurance (hereinafter referred to as OPS), compulsory social insurance in case of temporary disability and in connection with maternity (hereinafter referred to as OSS in case of VNiM), for compulsory medical insurance (hereinafter referred to as compulsory medical insurance) (clause 1, clause 1, article 420 of the Tax Code of the Russian Federation).

The date of payment in the form of wages is the day they are accrued (clause 1 of Article 424 of the Tax Code of the Russian Federation).

The amount of accrued wages is included in the base for calculating insurance premiums, which is determined at the end of each calendar month separately for each individual from the beginning of the billing period (calendar year) on an accrual basis (clause 1 of Article 421, clause 1 of Article 423 of the Tax Code RF).

In general, insurance premiums are calculated based on the tariffs established by Art. 426 of the Tax Code of the Russian Federation, which are:

- for mandatory pension insurance - 22% (within the established maximum base for calculating contributions to mandatory pension insurance);

- for OSS in case of VNiM - 2.9% (within the established maximum base for calculating contributions to OSS in case of VNiM);

- for compulsory medical insurance - 5.1%.

Calculation and payment of insurance premiums are made based on the results of the calendar month based on the base for calculating insurance premiums from the beginning of the billing period until the end of the corresponding calendar month and the tariffs of insurance premiums minus the amounts of insurance premiums calculated from the beginning of the billing period to the previous calendar month inclusive (clause 1 Article 431 of the Tax Code of the Russian Federation).

The amount of insurance premiums is calculated and paid separately in relation to insurance premiums for compulsory health insurance, insurance premiums for compulsory medical insurance in case of VNIM, insurance premiums for compulsory medical insurance (clause 6 of Article 431 of the Tax Code of the Russian Federation). The amount of insurance premiums to be transferred is calculated in rubles and kopecks (clause 5 of Article 431 of the Tax Code of the Russian Federation).

The amount of insurance premiums calculated for payment for a calendar month must be paid no later than the 15th day of the next calendar month (Clause 3 of Article 431 of the Tax Code of the Russian Federation).

[B=63]

Insurance contributions for compulsory social insurance against industrial accidents and occupational diseases

Wages are subject to insurance contributions for compulsory social insurance against accidents at work and occupational diseases (OSS from NSPiPZ) and are included in the base for their calculation (clauses 1, 2, article 20.1 of the Federal Law of July 24, 1998 N 125 -FZ “On compulsory social insurance against accidents at work and occupational diseases” (hereinafter referred to as Law No. 125-FZ)).

The tariff for insurance premiums for OSS from NSPiPZ is established taking into account the class of professional risk to which the economic activity of the organization belongs (Article 21 of Law No. 125-FZ). Insurance premiums for OSS from NSPiPZ are paid based on the insurance tariff, taking into account the discount or surcharge established by the insurer (Clause 1, Article 22 of Law No. 125-FZ).

In this consultation, we proceed from the condition that the economic activity of the organization is classified as class 1 of professional risk and the insurance premium rate for it is set at 0.2%, discounts (surcharges) to the insurance rate are not established (Article 1 of the Federal Law of December 22, 2005 N 179-FZ “On insurance tariffs for compulsory social insurance against industrial accidents and occupational diseases for 2006”).

Insurance premiums for OSS from NSPiPZ are calculated based on the results of each calendar month based on the amount of payments and other remunerations accrued from the beginning of the billing period (calendar year) to the end of the corresponding calendar month, minus the amounts of insurance premiums calculated from the beginning of the billing period to the previous calendar month inclusive (as follows from clause 9 of article 22.1, clause 1 of article 22.1 of Law No. 125-FZ).

The amount of insurance premiums calculated for payment for a calendar month must be paid no later than the 15th day of the next calendar month (Clause 4 of Article 22 of Law No. 125-FZ).

Changes in tax base

The rules for calculating the amounts of contributions to the Social Insurance Fund, pension and medical contributions remain practically unchanged. All benefits and existing tariffs remain in effect. As before, payments and other remuneration in favor of individuals accrued in accordance with employment and civil law contracts remain a taxable object.

The taxable base, as before, is calculated separately for each individual on an accrual basis from the beginning of the year. The maximum amount of the base for contributions in case of temporary disability and in connection with maternity is also preserved. The reduced rate for pension contributions in relation to payments accrued in excess of the limit will also remain.

In this area, the only change will affect the daily allowance. At the moment, daily allowances fixed in a local regulation or collective agreement are completely exempt from insurance premiums. From January 1, according to paragraph 2 of Art. 422 of the Tax Code of the Russian Federation, only amounts up to 700 rubles for business trips within the country and amounts up to 2,500 rubles for foreign business trips will be exempt from contributions.

At the same time, the rules for determining the tax base for income in kind will change. Until January 1, the database included the prices of goods, works and services specified in the contract. Now, according to Art. 105.3 of the Tax Code of the Russian Federation, the price will be determined based on market prices. And in accordance with paragraph 7 of Art. 421 of the Tax Code of the Russian Federation, VAT is not excluded from the taxable base.

The listed changes do not apply to insurance premiums in 2021 “for injuries”. Daily allowances are completely exempt from them, and income in kind is taken into account in the taxable base at the contractual value.

Deductions: calculation to the Pension Fund for individual entrepreneurs in 2021

The legally established minimum wage for the current year is 7,500 rubles. The formula for calculating insurance premiums remains unchanged:

• for the Pension Fund = 12 minimum wage x 26% = 12 x 7500 x 26/100 = 23,400 rubles;

• for the Compulsory Medical Insurance Fund = 12 minimum wage x 5.1% = 12 x 7500 x 5.1/100 = 4590 rubles.

So, the total minimum fixed amount of contributions of individual entrepreneurs for themselves with an income for the year within 300 thousand rubles. is 27,990 rubles. For businessmen who have not been running a business for a whole year, the amount of deductions is recalculated in proportion to the time worked as an entrepreneur.

The rules for calculating additional deductions if the annual profitability of a business exceeds the three hundred thousandth threshold - 1% of the excess amount - also remained unchanged. Restrictions on pension contributions also apply. In 2021, the “ceiling” will be 187,200 rubles. It is calculated by the formula: 8 minimum wage x 12 x 26%.

The businessman pays 4,590 rubles for medical insurance. regardless of the amount of income received. A businessman has the right to choose whether to deduct money for temporary disability and maternity insurance or not, but an individual entrepreneur cannot make contributions to the Social Insurance Fund for injuries and industrial accidents for himself.

The deadlines for payment of contributions have not changed either: fixed amounts must be paid before the end of the reporting year, additional accrued amounts must be paid before April 1 of the next year.

An example of calculating insurance premiums for an individual entrepreneur working as a “one person”

Income of individual entrepreneur Ivanov O.M. for 2021 – 850 thousand rubles.

Calculation of contributions to the Pension Fund for individual entrepreneurs: fixed contribution: 23,400 + 4590 = 27,990 rubles. The businessman must transfer the amount before the end of the year.

Calculation of insurance premiums for individual entrepreneurs on income exceeding the established limit:

((850,000 – 300,000) * 1%) = 5,500 rub. (must be entered before 04/01/2018).

Total deductions from individual entrepreneur Ivanov O.M. will be:

27,990 + 5,500 = 33,490 rub.

Reporting on insurance premiums to the Federal Tax Service in 2021

Perhaps the main innovation in the legislation on insurance premiums was the need to report not only to the funds, but also to the Federal Tax Service. For these purposes, a single quarterly report is being introduced. It immediately replaces four forms that were in force previously: 4-FSS, RSV-1, RSV-2, RV-3.

In accordance with paragraph 7 of Art. 431 of the Tax Code of the Russian Federation, submission of a single calculation to the Federal Tax Service must be carried out no later than the 30th day of the month following the reporting period. If the average number of employees is less than 25 people, then the report can be submitted in paper form. Legal entities and individual entrepreneurs with an average number of employees of more than 25 people must submit this report in electronic form.

The total amount of pension contributions in the calculation must match the amount of contributions for each insured person. Otherwise, the report will be considered not submitted.

There is no need to report to the Federal Tax Service on insurance premiums for 2021.

For insurance premiums from January 1, 2021

The organization needs:

- From the 1st quarter of 2021, provide the Federal Tax Service of Russia with a calculation of insurance premiums no later than the 30th day of the month following the reporting period.

- Pay insurance premiums in case of temporary disability and in connection with maternity to the Federal Tax Service of Russia for the new KBK opened by the Federal Tax Service of Russia from 01/01/2017.

- If there is an overpayment of insurance premiums for periods after January 1, 2021, submit an application for a refund of the overpayment of insurance premiums to the Federal Tax Service of the Russian Federation.

- Conducts reconciliation of calculations for accrued and paid insurance premiums after January 1, 2021 with the Federal Tax Service of Russia.

- If a decision is made based on the results of a desk or field audit regarding the payment of insurance premiums for the period after January 1, 2017, the organization does not agree with it, appeal the decision to the Federal Tax Service of Russia.

- Submit an application, including during the inter-reporting period, for reimbursement of expenses for the payment of insurance coverage to the Federal Social Insurance Fund of Russia.

- Appeal a decision made based on the results of a desk or on-site audit of the correctness of the policyholder's expenses for the payment of insurance coverage in the Federal Insurance Service of Russia.

Reporting on insurance contributions to funds in 2021

As stated above, forms 4-FSS, RSV-1, RSV-2, RV-3 have been cancelled. Other changes have also been adopted.

The deadline for submitting monthly reports to SZV-M is changing. Previously, it had to be submitted to the Pension Fund by the 10th day of the month following the reporting month. The deadline has now been extended. Starting from 2021, SZV-M must be submitted to the Pension Fund no later than the 15th day of the month following the reporting month.

Starting in 2021, new annual reporting will be introduced, the form of which has not yet been approved. The report must be submitted by March 1 of the year following the reporting year. For individual entrepreneurs and organizations with an average number of employees of up to 25 people, the report can be submitted in paper form. If there are 25 or more people, it is allowed to submit the report only in electronic form.

Starting from 2021, it is necessary to submit reports to the Social Insurance Fund only on contributions “for injuries”. As before, individual entrepreneurs and organizations with an average number of employees of less than 25 people can submit reports in paper form, others - only in electronic form. These reports have the same deadlines for submission as for Form 4-FSS: paper reports must be submitted no later than the 20th day of the month following the reporting one, electronic reports must be submitted no later than the 25th day of the month following the reporting one. reporting.

We remind you that all these innovations do not apply to reporting for 2021.

Deadline for payment of contributions to the Social Insurance Fund “for injuries” in 2017

Insurance premiums for injuries in 2021 will still need to be transferred to the Social Insurance Fund. The deadlines for paying contributions for injuries are given in the table.

| Payment period | Payment due in 2021 |

| December 2021 | no later than January 16 (since January 15 is Sunday) |

| January 2021 | no later than February 15, 2021 |

| February 2021 | no later than March 15, 2021 |

| March 2021 | no later than April 17 (since April 15 and 16 are Saturday and Sunday) |

| April 2021 | no later than May 15 |

| May 2021 | no later than June 15 |

| June 2021 | no later than July 17 (since July 15 and 16 are Saturday and Sunday) |

| July 2021 | no later than August 15 |

| August 2021 | no later than September 15 |

| September 2021 | no later than October 16 (October 15 – Sunday) |

| October 2021 | no later than November 15 |

| November 2021 | no later than December 15 |

Read also

09.08.2016

Reimbursement of social insurance expenses in 2021

Employers retain the right to reimburse sick pay from the Social Insurance Fund. As before, the employer pays for the first three days. Contributions can be transferred minus benefits paid. If the amount of benefits exceeds the amount of contributions, the difference can be offset against payment of contributions in the following periods, or you can request the missing funds from the Social Insurance Fund.

Expenses will be verified as follows. After receiving the quarterly payment from the employer, the Federal Tax Service Inspectorate transmits the information to the territorial body of the Social Insurance Fund. FSS inspectors verify the accuracy of the declared expenses through an on-site or desk audit, the results of which are reported to the Federal Tax Service. If the result is negative, the Federal Tax Service will send the policyholder a demand for payment of the missing funds. If the result is positive, the expenses will be accepted, and the Federal Tax Service, if necessary, will return the difference between contributions and expenses or offset it.

This scheme will be valid until December 31, 2018 in regions that have not yet joined the pilot project for paying benefits directly from the Social Insurance Fund.

Calculation of taxes on wages under the main tax regime in 2021: instructions

Calculating payroll taxes is a serious and responsible process, errors in which can lead to serious consequences. In order to determine the correct size of this value, you must go through the following steps:

- determine the amount at which the deduction will be determined;

- determine the tax rate that will be applied to the employee’s income;

- calculate personal income tax;

- subtract the required deductions from the amount received;

- determine the amount of insurance premiums, as well as the amount of contributions to extra-budgetary funds.

The most important tax that is calculated when determining the final salary is personal income tax, or personal income tax. In 2021 it is 13% of wages. Payroll tax table:

| Tax rate | Income | Procedure for calculating payroll tax | Governing Law |

| 13% | Salaries of Russian residents | Cumulative total with the use of deductions and subsequent offset of the paid personal income tax amount | Clause 1 of Article 224 of the Tax Code of the Russian Federation |

| 13% | Salaries of EAEU citizens and refugees | Separately for each type of income - without offsets or deductions | Clause 3 of Article 224 of the Tax Code of the Russian Federation |

| 30% | Salaries of non-residents of the Russian Federation | Separately for each type of income - without offsets or deductions | Clause 3 of Article 224 of the Tax Code of the Russian Federation |

You can determine the amount for which the deduction will be determined as follows:

Calculating payroll taxes is very simple:

- First of all, you need to decide on the initial parameters. Let's take the average person who works 5 days a week, which is approximately 21 days a month. Let's assume that out of these he went to work only 15 times. The employee’s salary is 20,000 rubles, which means that for the time worked the person received: 20,000 * (15/21) = 14,286 rubles.

- After this, you can start calculating the tax: 14,286*13%=1,857 rubles.

- Now we subtract the tax amount from the salary and get a net salary with taxes already paid in the amount of 12,429 rubles.

Federal Tax Service checks of insurance premium payments

The Federal Tax Service, starting in January 2021, will begin to conduct on-site and desk audits of insurance premiums. The only exception will be contributions “for injuries”. Please note that employees of the Federal Tax Service will check the correctness of the accrual and payment of insurance premiums in 2021, taking into account the rules that apply to verify the accrual and payment of taxes.

As was the case previously, the FSS will be responsible for checking the costs of compulsory social insurance. That is, the same period can be checked twice - by the tax service and the Social Insurance Fund.

The Pension Fund of Russia will control only personalized reporting: form SZV-M, as well as new annual data on work experience. Thus, the rules of the transition period look like this: checks on insurance premiums (with the exception of “injury” contributions), which are scheduled for 2021 (and for subsequent periods), while relating to 2021 and previous periods, will be carried out by the funds.

If any violations (arrears) are discovered during the audit, fund employees report this to tax inspectors, and they, in turn, take the necessary measures.

Control of contributions “for injuries” will be carried out by the Social Insurance Fund (for all periods).

***

The transfer of control functions in the field of settlements of contributions to extra-budgetary funds to the jurisdiction of the Federal Tax Service has led to numerous changes in the order of their transfer, as well as in the deadlines for submitting insurance contributions in 2021. In addition, the list of reporting on them has changed. The obligation to transfer contributions is established for all individual entrepreneurs and companies, including their branches and representative offices, if they make payments to hired employees. However, contributions for injuries and occupational diseases still go through the Social Insurance Fund. The period allotted for payment of contributions ends on the 15th day of the month following the reporting month, or if it coincides with a weekend or holiday, it is postponed to the first nearest working day.

Similar articles

- Entrepreneurs will be exempt from paying insurance premiums

- Procedure and terms for payment of insurance premiums

- KBC for insurance premiums for 2021

- Details of the Social Insurance Fund and Pension Fund for payment of insurance premiums in 2017

- Overpayment of insurance premiums in 2021

Fines for violations

From 2021, violations that are related to insurance premiums (except for “injuries”) will be fraught with the imposition of fines by the Federal Tax Service. It should be borne in mind that all sanctions provided for violations of tax laws will also be used in relation to contributions. For example, if the policyholder did not provide a calculation of contributions, he will be fined on the basis of Article 119 of the Tax Code of the Russian Federation, and for violation of the rules for accounting for the base of contributions, sanctions of Article 120 of the Tax Code of the Russian Federation will be applied.

For violations related to insurance premiums for injuries, employees of the Social Insurance Fund will, as before, be punished. The new edition of the Law on Compulsory Social Insurance against Accidents at Work contains all types of FSS sanctions. For example, for refusing to provide documents for verification, on the basis of Article 26.31 of the above law, the policyholder faces a fine of two hundred rubles (for each document not provided).

The pension fund has the right to apply two types of sanctions:

1. For failure to provide annual information about the length of service - 500 rubles (for each insured person).

2. For violation of the procedure for submitting reports in the form of electronic documents - 1,000 rubles.

These rules are contained in the new version of Article 17 of the Law on Personalized Accounting.

General rates

Insurance premium rates are set in the following amounts (Articles 425, 426 of the Tax Code of the Russian Federation):

- for compulsory pension insurance within the established maximum value of the base - 22%, above the maximum value of the base - 10%;

- for compulsory social insurance in case of temporary disability and in connection with maternity within the established maximum base value - 2.9%; in relation to payments and other remuneration in favor of foreign citizens and stateless persons temporarily staying in the Russian Federation, within the established maximum value of the base for this type of insurance - 1.8%;

- for compulsory health insurance – 5.1%.

For 2021, the maximum base for calculating insurance premiums for OSS in case of temporary disability and in connection with maternity is set at 755,000 rubles, for OPS - 876,000 rubles (Resolution of the Government of the Russian Federation of November 29, 2021 No. 1255).

Read also “Limits and base for insurance premiums for 2021”

In 2021, the maximum base for calculating insurance premiums in the Pension Fund was 796,000 rubles, in the Social Insurance Fund - 718,000 rubles (Resolution of the Government of the Russian Federation of November 26, 2015 No. 1265).

Refund of overpaid contributions in 2017

From January 2021, policyholders will, as before, have the right to return overpayments of insurance premiums. The difference is that the refund will now be carried out not by the funds, but by the tax office. As for the refund procedure, it will be the same as in previous periods, as for taxes.

A new condition will appear. If overpaid insurance premiums in 2021 to the Pension Fund of the Russian Federation were included in personalized reporting, and the Pension Fund distributed them to personal accounts, then employees will not return the tax overpayment. This rule is in the newly created clause 6.1 of Article 78 of the Tax Code of the Russian Federation.

The Social Insurance Fund will return overpaid contributions “for injuries”. Article 26.12 of the new edition of the Law on Compulsory Social Insurance against Accidents at Work contains an algorithm for offsetting and returning overpayments on insurance premiums.

Due dates for payment of contributions in 2021: table

However, the deadline for paying insurance premiums in 2021 will not change. Employers-insurers (organizations and individual entrepreneurs) will have to transfer insurance premiums no later than the 15th day of the month following the month of accrual of contributions (clause 3 of Article 431 of the Tax Code of the Russian Federation).

Further in the table we present the deadlines for payment of insurance premiums to the Federal Tax Service, which policyholders must pay in 2021 from payments to their employees and other individuals.

| Payment period | Payment due in 2021 |

| December 2021 | no later than January 16 (since January 15 is Sunday) |

| January 2021 | no later than February 15, 2021 |

| February 2021 | no later than March 15, 2021 |

| March 2021 | no later than April 17 (since April 15 and 16 are Saturday and Sunday) |

| April 2021 | no later than May 15 |

| May 2021 | no later than June 15 |

| June 2021 | no later than July 17 (since July 15 and 16 are Saturday and Sunday) |

| July 2021 | no later than August 15 |

| August 2021 | no later than September 15 |

| September 2021 | no later than October 16 (October 15 – Sunday) |

| October 2021 | no later than November 15 |

| November 2021 | no later than December 15 |

Blocking of accounts by tax authorities

It is still unknown whether tax officials will have the right to block the policyholder’s current account if he does not submit payment for insurance premiums. The new version of paragraph 11 of Article 76 of the Tax Code of the Russian Federation states that the blocking rules should apply to payers of insurance premiums. At the same time, paragraph 3 of Article 76 of the Tax Code does not contain any mention of what was not submitted during the calculation of contributions.

It is quite possible that in the near future legislators will eliminate this contradiction in the Tax Code. If this does not happen, policyholders and tax authorities will resolve disputes in court.

Payment of taxes and contributions from salary

Taxes and salary contributions are paid in 2021 depending on their type. The following procedure applies to personal income tax in the Tax Code of the Russian Federation:

- Salary taxes must be paid the next day after payment

- for vacation pay or sick leave, tax is transferred on the last day of the month the money is issued to employees

Payment is made by payment order, in which a certain BCC must be indicated in field 104.

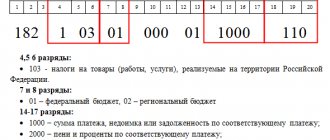

KBK for personal income tax in 2017-2021

| Personal income tax of employees | 182 1 0100 110 |

| Penalties for personal income tax | 182 1 0100 110 |

| Personal income tax fines | 182 1 0100 110 |

KBC on insurance premiums in 2017-2021

| Type of contribution | Contribution | Penalty | Fines |

| OPS | 182 1 0210 160 | 182 1 0210 160 | 182 1 0210 160 |

| OSS | 182 1 0210 160 | 182 1 0210 160 | 182 1 0210 160 |

| Compulsory medical insurance | 182 1 0213 160 | 182 1 0213 160 | 182 1 0213 160 |

| Contributions for injuries | 393 1 0200 160 | 393 1 0200 160 | 393 1 0200 160 |

Changes for separate divisions

It should be noted that significant innovations are provided for both organizations and individual entrepreneurs. Previously, it is necessary to pay contributions and submit reports at the location of the organization’s division only if it has a separate balance sheet or its own current account.

Starting from 2021, the requirement to have a current account ceases to apply. Consequently, this year and in subsequent periods, separate divisions that are located in the Russian Federation, accruing remuneration (or other payments) in favor of individuals, will stop transferring insurance payments (except for the contribution “for injuries”), as well as submitting settlements at the place of their registration (based on paragraph 11 of Article 431 of the Tax Code of the Russian Federation).

In addition, from 2021, policyholders will receive a new obligation to inform the Federal Tax Service at the location of the head office that the Russian division of the organization has the authority to charge remuneration (or other payments) in favor of individuals.

This must be done within one month from the date of granting authority. It must be taken into account that the new obligation applies to divisions that began making payments to individuals in 2021 and in subsequent periods. If rewards were awarded to individuals before 2021, then no notifications need to be made.

There are no changes to “injury” contributions. Thus, in 2021, separate divisions will continue to pay insurance premiums and submit reports on them only if they have an account and balance.

Payroll tax: features

Depending on the type of employment contract and the enterprise itself, there are various forms of remuneration. The labor legislation of the Russian Federation determines that an organization must pay wages to its employees twice a month: at the beginning and at the end, and contributions to extra-budgetary funds - once a month from the total amount of wages, taking into account all advances, vacation and sick leave payments.

The difference between the actual salary the employee receives and the accrued salary may also include other types of deductions. However, it must be taken into account that its size cannot exceed 20%.

Determining payroll tax and the amount of contributions to insurance and pension funds is a rather labor-intensive process that requires extensive knowledge of accounting and tax accounting. Errors may be considered an intentional violation and may be subject to penalties.

Payroll tax what percentage in 2017:

Insurance premiums in 2021 for individual entrepreneurs

In 2021, self-employed citizens will pay fixed payments for health insurance, as was the case previously. Contributions for insurance in case of temporary disability and in connection with maternity will also remain voluntary. Self-employed citizens do not need to pay insurance premiums.

The change is provided for pension contributions. This applies to individual entrepreneurs who received income of more than 300,000 rubles. As before, 1% of the amount of income that exceeds 300,000 rubles must be added to the fixed amount of contributions.

Tax inspectors will continue to receive income data from declarations. At the same time, the rule according to which a maximum fine is charged for failure to submit a declaration is cancelled.

Reporting on contributions for individual entrepreneurs has not changed - they will again submit calculations for fixed contributions. And the heads of peasant (farm) households will submit reports on new deadlines. Thus, they will need to submit their calculations no later than January 30 of the year following the billing period. Previously, the deadline for submitting reports was the last day of February.

Deadlines for transferring insurance premiums in 2017-2018

The deadlines for payment of insurance contributions for compulsory pension and health insurance, as well as social insurance in case of disability and maternity for employers making payments to employees, have been established since 2021 by Art. 431 Tax Code of the Russian Federation. According to the text of paragraph 3 of this article, contributions calculated for a calendar month, as before, must be paid no later than the 15th day of the month following the one for which these contributions were calculated. Moreover, if the 15th is a red day of the calendar, then the last day for transferring contributions to the tax authorities is the first worker following it.

The rules for calculating and paying contributions for insurance against industrial accidents and occupational diseases are reflected in the Law “On Compulsory Social Insurance...” dated July 24, 1998 No. 125-FZ. According to it, the amounts calculated at the insurance rate must be transferred to the Social Insurance Fund also no later than the 15th day of the following month. Insurance premiums are calculated and paid in rubles and kopecks.

IMPORTANT! Starting from 2021, organizations and separate divisions that make payments to employees transfer insurance premiums (except for payments for injuries) to the Federal Tax Service inspectorates. The amounts of contributions transferred by the organization and its separate division are determined from the amounts paid to employees at their location.

As for individual entrepreneurs who do not have employees, as well as notaries and lawyers engaged in private practice, the deadlines for paying contributions for themselves from 2021 are established by Art. 432 of the Tax Code of the Russian Federation. Such taxpayers pay fixed amounts for compulsory pension and health insurance, as well as contributions to pension insurance, calculated on income over 300,000 rubles, based on the following terms:

- fixed amounts for the year - no later than December 31 of the current year;

- contributions calculated on income exceeding RUB 300,000. - until April 1 of the year following the billing year.

Read more about mandatory contributions payments made by individual entrepreneurs here.

Read about the rules for filling out payment slips for contributions in the article “How to fill out payment slips for insurance premiums in 2017-2018?” .

This might also be useful:

- Deadline for submitting 2-NDFL in 2021 for 2021

- How to calculate the simplified tax system?

- How to register as a UTII payer

- Payment of 1% on income over 300,000 rubles

- Fixed payments for individual entrepreneurs on UTII in 2021

- Fixed payments for individual entrepreneurs in 2021 for themselves

Is the information useful? Tell your friends and colleagues

Dear readers! The materials on the TBis.ru website are devoted to typical ways to resolve tax and legal issues, but each case is unique.

If you want to find out how to solve your specific issue, please contact the online consultant form. It's fast and free!

Error when submitting reports

The employer is obliged not only to transfer taxes and contributions from the employee’s salary on a monthly basis, but also to provide reporting in a timely manner. Such reports are submitted to the Federal Tax Service:

| According to personal income tax | |

| 2-NDFL | Annual – last date of the first reporting year |

| 6-NDFL | Quarterly – the last date of the next quarter and annual – the last date of the first reporting year |

| 3-NDFL | Annual – last date of the first reporting year |

| By contributions | |

| RSV | Quarterly – 30th day of the month following the reporting quarter |

Social contributions – changes for 2021

In order to reduce the administrative burden on taxpayers, optimize document flow and increase the level of collection of tax payments, starting from 2021, control functions for accepting reports and collecting contributions regarding the ESSS have been transferred to the Federal Tax Service of the Russian Federation. Reporting periods are: quarter, half-year, 9 months, year. Submission of reports RSV, 4-FSS has been replaced with a single form (approved in Order No. ММВ-7-11/551 dated 10.10.16).

Payers of social contributions are recognized as employers-enterprises/individual entrepreneurs, self-employed categories of persons. The rules for determining the base for calculating charges and tax objects have not changed globally. The deadline for submitting a single calculation is the 30th day of the calendar month following the reporting period. Amounts must be paid to the Federal Tax Service using new details, including KBK.

Important! The social authorities are left with the function of administering the following reports: FSS - “injuries”, Pension Fund of the Russian Federation - monthly reporting on f. SZV-M, SZV-Stazh.