Tax base for transport tax

The tax base is considered as the main component of the formula used to establish the size of the fiscal payment.

The tax system reflects different concepts, including base and object. Citizens often use incorrect meanings of these terms. It is important to distinguish between them, since the base is the main element for finding the tax amount. For many types of property, market value is used as a basis. The object must be understood as the property for which the tax is paid. In the case of transport fees, the objects are vehicles. Depending on the type of car, a base is installed.

It is important to note that the car must be registered to a specific citizen. When setting the base, the power of the motor is taken into account. The measurement is in horsepower.

When the calculation of transport tax can be suspended

The only case of suspension of the accrual of transport tax is theft of a car. If a car is stolen (theft), it is necessary to report it to the Federal Tax Service and provide documents about the theft (theft).

More detailed information on actions in this case is presented on the website nalog.ru, section “frequently asked questions” (https://www.nalog.ru/rn77/service/kb/):

“Tax authorities have the right not to assess transport tax to the taxpayer for a vehicle that is on the wanted list, provided that the taxpayer (citizen) submits to the tax authority an original document confirming the fact of theft (theft) of the car, received from the relevant body investigating a crime related to theft (theft) of this vehicle" (

How is the tax base for transport tax determined?

Not in all cases, engine power affects the determination of the base for fiscal payments. This indicates the need to take into account other indicators. Most often, there is no need to calculate the value in question. This is due to the fact that at car manufacturing plants, the documentation initially indicates the parameters that are important when determining the base.

Vehicle with engine

The motor is the main indicator of the category

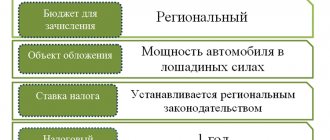

The main group are those that have a motor. In this regard, the basis for them is established based on an assessment of the power of a given unit. It is important to note that the measurement is only in horsepower. Other indicators cannot be used.

This category includes:

- passenger cars;

- motorbike;

- bus and so on.

The exceptions are devices used to move in airspace. These funds are classified in another group.

Air vehicles

The next category is represented by aircraft. In their design, a motor is a mandatory element. However, when setting the size of the base, the thrust of the jet motor is used. This value has a static expression.

The measurement of the indicator in question occurs during takeoffs. It is set as kilograms of force. This group will include helicopters and other vehicles moving in the airspace.

Water towed vehicles

Another group is represented by water vehicles. They cannot be classified as self-propelled vehicles. When establishing the base, gross tonnage is used. The indicated figure is determined in tons. You can find the value in the technical documentation for a specific type of product. In this case, the category is not important.

Unclassified vehicles

There are funds that cannot be classified into a certain category. Their device may or may not have a motor. To establish the base, a unit of such funds is taken into account.

Advance payments during the tax period - when to pay

According to Art. 360 of the Tax Code of the Russian Federation, quarterly reporting periods are valid throughout the year (1st, 2nd, 3rd quarter). The legislation allows regions to introduce or cancel intermediate periods for reporting on transport tax. The authorities of the constituent entities of the Russian Federation can independently decide whether they need this in the territories subordinate to them or not. Here are two examples:

- The decision of the Moscow authorities is formalized by the Moscow Law “On Transport Tax” dated 07/09/2008 No. 33. Here, payers (legal entities) do not report on this tax quarterly and do not make partial quarterly prepayments.

- The Law of the Republic of Tatarstan dated November 29, 2002 No. 24-RT provides for the quarterly obligation of legal entities to report on transport tax and make advance payments, along with a full calculation and an annual declaration, which must be submitted by February 10 of the year following the reporting year.

For individuals, the tax period for transport tax is one - 1 year and no other reporting intervals have been established. They also do not need to transfer advance payments, the calculation is made for them by the tax authorities at the end of the year, and the deadline for payment is set until December 1 of the year following the NP.

For which vehicles do you not need to pay tax?

Wheelchairs are not taxed

It is important to take into account that there are devices for the use of which you do not need to make fiscal payments. This suggests that establishing a tax base will also not be required. These include:

- devices that are used to move through water and are not equipped with motors or are not equipped with them (the power limit is set to no more than 5 horses);

- passenger cars with a capacity not exceeding 100 units;

- means of transportation for the disabled;

- machines used for the purpose of passenger transportation.

In addition, this includes devices used in agricultural activities. If the car is stolen, then the fiscal payment will not be charged. Also included in this category are cars used in military units.

Sale of a car: how the tax period is determined

The sale of a vehicle in no way affects the duration of the NP; it remains equal to 1 year.

A citizen is usually sent a tax notice indicating the amount of tax to be paid no later than 30 days before the final calculation date (December 1). In practice, this document reaches the payer even earlier, in April-August of the next year, so the population always has time to pay the tax.

In this case, the provisions of Art. 362 of the Tax Code of the Russian Federation, according to which the tax is calculated in proportion to the number of months of ownership. So, if a car was deregistered after the 15th day of the month or registered before the 15th day, then the month is taken to be equal to the whole month the vehicle was owned.

Also, to calculate the tax, the so-called ownership coefficient is used, calculated by dividing the number of months the car was owned by 12.

Example 1

In 2021, on January 17, citizen Ivanov sold his old car to citizen Petrov and, accordingly, deregistered it. Based on this, Ivanov owned the car for only 1 month, so he must pay only 1/12 of the annual amount due. However, the NP for him will not change and will end, like for everyone, on December 31, 2021. For the NP (2017), he will be required to transfer the amount due to the budget. Ivanov will not have to calculate the tax himself, and he will make the payment after receiving a notice from the tax office, which will reflect the corresponding amount. He is obliged to make the final settlement with the budget before December 1, 2021.

Citizen Petrov, who became the owner of a vehicle and registered it in January 2021, will have to pay tax for the period from February (ownership transferred after January 15) to December 2021, i.e. for 11 months. The final deadline for tax payment will be the same - December 1, 2018.

For the organization that sold the car, the situation is complicated by the fact that it needs to independently carry out the calculation and only then transfer the tax within the established time frame.

Payers of transport tax and the basic principles of its calculation

Transport payments - regional fees

The fiscal tax is classified as regional. The obligation to pay falls on citizens and organizations. The main condition is the existence of legal ownership of the transport. Company representatives have the obligation to independently calculate and make these payments. For citizens, settlement transactions are carried out by employees of fiscal authorities. The receipt is generated on the basis of data provided by the registration authorities.

The principles include:

- when calculating the tax payment, the base multiplied by the rate is taken into account (other rules are sometimes reflected in the Tax Code of the Russian Federation);

- advance payments are determined every reporting period (a quarter of the base is taken and multiplied by the rate);

- if a tax calculation is necessary for an enterprise, then it is enough to calculate the difference between the amount established for the year and the advance payments made (the law does not provide that citizens must make such contributions);

- Organizations have the right not to pay advance payments for cars that have a permissible weight of more than 12 tons.

In addition, if the vehicle has a high cost, the total amount is calculated taking into account multiplying factors. It is determined based on the price of the car and the number of years that have passed since the car was produced.

Procedure for calculating the amount of transport tax and advance payments

The Tax Code of the Russian Federation obliges all organizations, regardless of what taxation regime they are in, to independently, unlike, say, individuals, calculate both the amount of tax and the amount of the advance payment for it. By the way, the calculation and payment of interim (advance) payments can be canceled by regional legislation. This will be discussed in more detail below, in the section “Procedure and deadlines for payment of transport tax and advance payments thereon” of this article. Let's continue further: the amount of tax payable to the budget at the end of the tax period is calculated for each vehicle as the product of the corresponding tax base and the tax rate (clauses 1, 2 of Article 362 of the Tax Code of the Russian Federation). It is quite logical that the law defines a mechanism for calculating tax in relation to each vehicle, because tax rates are set differentially, and the tax base for each type of vehicle is different. The amount of advance tax payments, unless, of course, the regional legislator has canceled the obligation to make intermediate payments, is calculated at the end of each reporting period in the amount of one-fourth of the product of the corresponding tax base and the tax rate.

Example. A passenger car with an engine capacity of 120 horsepower is registered to the company. The rate for the specified vehicle is 20 rubles. per horsepower. Accordingly, after the first, second and third quarters, the organization must calculate an advance payment in the amount of: 0.25 x (120 x 20) = 600 rubles.

According to the norms of paragraph 2 of Art. 362 of the Tax Code of the Russian Federation, the amount of tax at the end of the tax period is determined as the difference between the calculated amount of tax and the amounts of advance tax payments payable during the tax period.

Example. Let's use the conditions of the previous example: the organization calculates the annual tax amount: 120 x 20 = 2400. All previously paid advance payments are subtracted from this value, and the amount that must be transferred to the budget at the end of the tax period is obtained: 2400 - 600 (Q1) - 600 (II quarter) - 600 (III quarter) = 600 rubles.

But what to do in a situation where the vehicle was registered with the company for an incomplete calendar year? How much tax should I pay? In accordance with the norms of paragraph 3 of Art. 362 of the Tax Code of the Russian Federation in this case, the calculation of the amount of tax (the amount of the advance tax payment) is carried out taking into account a coefficient defined as the ratio of the number of full months during which the vehicle was registered to the taxpayer to the number of calendar months in the tax (reporting) period. In this case, the month of registration of the vehicle, as well as the month of deregistration of the vehicle, are taken as a full month.

Example. Let's consider calculating tax if a vehicle has been registered at an enterprise for less than a year. Let's return to the data of the same example, taking into account the fact that the car was deregistered in November. Let's calculate the coefficient: 11 / 12 = 0.917. The amount of tax payable for the car will be: 2400 x 0.917 = 2200.8 rubles. Advance payments for the 1st, 2nd and 3rd quarters were calculated to be paid: 600 x 3 = 1800 rubles. This means that the amount of tax payable for the year should be: 2200.8 - 1800 = 400.8 rubles.

Quite often the question arises about calculating tax in connection with the re-registration of a vehicle in another constituent entity of the Russian Federation, which has different tax rates. According to the Ministry of Finance, set out in Letter dated August 27, 2009 N 03-05-05-04/11, if a vehicle is deregistered in one subject of the Russian Federation and in the same month registered (re-registered) for the same taxpayer in another subject of the Russian Federation, transport tax for a given month must be paid at the place of registration of transport as of the 1st day of this month. At the new location of the vehicle, the tax will need to be paid starting from the next month, and its calculation and payment must be carried out in accordance with the legislative act of the subject of the Russian Federation on transport tax in force in the territory of the corresponding constituent entity of the Russian Federation.

Object and tax rate

Payment object - vehicle

An object is understood as a vehicle that has undergone the registration process and at the same time complies with the requirements reflected in legal acts. For example, if the car is registered to the father, and the son drives it, the father is obliged to pay. When the right of ownership is with the organization, and the car is used for the personal purposes of the manager, the company pays.

Local authorities are in charge of approving rates in specific regions. They change depending on certain indicators. Including:

- motor power;

- the period during which the product is used;

- its gross tonnage;

- vehicle categories.

It is permissible to adjust the rate no more than 10 times. This ratio is related to the indicator reflected in the Tax Code of the Russian Federation.

Taxpayers of transport tax

In accordance with Art. 357 of the Tax Code of the Russian Federation, such persons are recognized as persons on whom, in accordance with the legislation of the Russian Federation, vehicles are registered , recognized as an object of taxation in accordance with Art. 358 Tax Code of the Russian Federation. And since persons in accordance with Art. 11 of the Tax Code of the Russian Federation recognizes legal entities and individuals, then, accordingly, citizens, individual entrepreneurs, and organizations are recognized as tax payers. At the same time, organizations applying the simplified taxation regime are also payers of transport tax. In the list of taxes from which “simplified people” are exempt, transport tax is not mentioned (clause 2 of Article 346.11 of the Tax Code of the Russian Federation). Enterprises under the simplified tax system calculate and pay tax in the same manner as enterprises under the general taxation regime. True, when switching from one regime to another, organizations may encounter certain features in accounting for transport tax. We will look at them in this article. Let's return to the definition of the concept of a taxpayer for the purposes of calculating and paying transport tax. This is recognized, as already stated above, as the person in whose name the vehicle that is the object of taxation is registered. And this criterion is the main basis for recognizing a person as a tax payer. Therefore, regardless of whether the company owns the vehicle or not, if the car is registered with this company, it will be recognized as a taxpayer and will have to pay transport tax. The following authorities adhere to this conclusion: the Ministry of Finance of Russia. In his opinion (Letter dated 04.07.2006 N 03-06-04-04/28), only those companies with registered vehicles should pay tax. The fact of vehicle ownership does not matter; arbitration court. The Resolution of the FAS VSO dated March 17, 2009 N A33-13239/07-F02-871/09, A33-13239/07-F02-875/09 reflects that an organization writes off vehicles from its balance sheet without deregistering them with the authorities, in which they are registered is not a basis for recognizing this organization as a transport tax defaulter.

How can you reduce transport tax?

Local authorities have the power to reduce the amount of tax payment. This is expressed in different behaviors:

- the company pays tax in an amount similar to that of citizens (the Supreme Arbitration Court explained in this situation that calculations are made depending on the properties of the car, and not the owner);

- to reduce the size of the fiscal payment, it is permissible to purchase a vehicle with less power;

- register in the entity where a lower rate is used.

In addition, the payment amount can be reduced if the owner is a person under the age of majority.

Tax benefits

Citizens can receive tax benefits

From the beginning of 2021, companies owning vehicles are required to submit to the fiscal authority an application for the use of benefits in the area in question. They will also need to document their eligibility to use the exemptions.

If such papers are not submitted, employees of the fiscal authority independently make inquiries and confirm the information reflected in the application.

Procedure for calculating and paying tax

Regional authorities are establishing periods and procedures for making tax payments. This is due to the fact that the tax in question falls within their competence. The federal law reflects that such a period cannot be set earlier than the beginning of February of the year following the previous tax period.

Enterprises are responsible for independently calculating the payment amount. Firms submit declarations to the tax authorities, based on which a conclusion is drawn about the correctness of the contributions paid. Starting from 2021, this obligation will be abolished and there will be no need to submit declarations.

If the cost of the car exceeds three million, then a multiplying factor is used in the calculations.

Procedure for payment of transport tax by individuals

Individuals pay transport tax once a year.

The payment deadline from 2021 is no later than December 1 of the year following the reporting year (the year for which the transport tax was calculated).

Thus, the deadline for payment of transport tax for 2021 by an individual is no later than 12/01/2021.

The order is as follows.

The Federal Tax Service sends a notification of the tax amount for the past year no less than a month before the payment date.

If an individual has not received a notification within the specified period, he is obliged to report this to the Federal Tax Service no later than December 31 of the year following the reporting year.

The message can be composed in any form.

Determination of the tax base

How to calculate the tax base? As such, the tax base for transport tax is not calculated. Usually it is declared by the manufacturer and reflected in technical documents. All that is required of you is to find the required indicator and rewrite it in your tax return.

The tax base for transport tax is determined as:

- for a car, bus, truck or other land or water transport equipped with an engine - this is the power of its engine declared in the registration certificate, expressed in hp;

- for an airplane or other aircraft with an air-breathing engine (engines) - the declared isometric thrust in take-off mode (or the sum of several thrusts), expressed in kgf;

- for water vehicles not equipped with an engine and moving in tow - gross tonnage expressed in reg. tons;

- for other, unclassified water and air vehicles - the entire vehicle.

If in technical documents for a vehicle the power is calculated in kW, it is necessary to convert them into hp using a special coefficient. In this case, the resulting value is rounded to hundredths of a whole.

In section 2 of the tax return, you reflect the base separately for each vehicle registered to your company. In the same way, all calculations are carried out separately, only the final sums are added.