Cancellation of UTII: what to do?

Many businessmen now use a single tax on imputed income (UTI). This significantly simplifies accounting and makes it possible to save on mandatory payments.

However, at the end of 2021, all “imputed” workers will have to think about switching to other operating modes. And for those whose business is related to trade, problems can begin much faster. Let's look at the upcoming changes and tell you what businessmen should do to reduce losses during the transition period.

What is UTII and why is it convenient for business?

The main difference between “imputation” and most other tax regimes is that with UTII, the amount of payments to the budget is not tied to the results of activities.

Imputed (i.e., predetermined) tax is calculated based on certain physical indicators. This may be the number of employees, the area of retail premises, etc.

Therefore, if a business develops and increases profits, then it is much more profitable to pay one fixed amount than constantly growing “current” taxes.

Restrictions for using UTII

Naturally, the use of such a beneficial regime for businessmen is associated with a number of restrictions.

- UTII can only be used for a certain list of activities (clause 3 of Article 346.29 of the Tax Code of the Russian Federation). We are talking about trade, catering and some types of services.

- If the “imputed” person is a legal entity, then the share of other organizations in the authorized capital should not exceed 25%.

- The number of employees should not be more than 100 people.

- Other physical indicators are also limited: the area of a store or cafe can be no more than 150 square meters. m, and the number of vehicles is no more than 20.

A specific list of activities for which UTII can be used is determined by regional authorities within the framework of the federal list.

Also, local legislators can do so entirely on their own territory. For example, in Moscow, UTII has not been valid since 2012.

When will UTII be cancelled?

“Imputation” appeared in Russian legislation about 20 years ago. Then it was regulated by a separate law No. 148-FZ of July 31, 1998. Then, with the introduction of the Tax Code of the Russian Federation, a special chapter 26.3 appeared in it, dedicated to UTII.

The purpose of the “imputation” when it was introduced was to collect at least some taxes from small businesses. However, in recent years, the efficiency of tax administration has increased significantly, and officials have drawn attention to the fact that the use of UTII significantly reduces budget revenues.

Discussions about this have been going on for a long time, and initially UTII was supposed to “disappear” in 2021. However, due to the crisis of 2014-2015. the termination of UTII was postponed for three years, i.e. until 01/01/2021 (law dated 06/02/2016 No. 178-FZ)

The deadline for canceling UTII is approaching, and it is unlikely that the state will “change its mind” this time either. The fact that the fiscal authorities are determined is evidenced by the general tightening of control over business: the introduction of online cash registers, product labeling, etc.

By the way, in connection with the labeling of goods, for many entrepreneurs UTII will actually be abolished from the beginning of 2020. On September 19, 2021, the State Duma adopted the Federal Law on the abolition of UTII and PSN for certain labeled goods (clauses 58, 59 of Article 2 of the Federal Law of September 29, 2019 N 325-FZ “On Amendments to Parts One and Two of the Tax Code of the Russian Federation” ).

The upcoming changes provide, among other things, for the removal from UTII of retail trade of certain goods subject to mandatory labeling from 01/01/2020.

Therefore, those who work with such goods need to think about changing the tax regime now.

To categories that “fall out” from UTII, in accordance with paragraph 58 of Art. 2 bills No. 720839-7 include:

- Medicines.

- Shoes.

- Clothing and accessories made from natural fur.

Which mode is more convenient to change UTII to?

The tax regime closest to UTII is the patent system (PSN). But not everyone can simply switch from “imputation” to a patent:

- Only individual entrepreneurs have the right to use the patent system.

- Restrictions on the scale of business for PSN are much more stringent: the number of employees is no more than 15, and the area of a store or cafe is no more than 50 square meters. m.

- For a patent, there is a revenue limit of 60 million rubles. per year (clause 6 of article 346.45 of the Tax Code of the Russian Federation).

In addition, from 01/01/2020, when retailing the above-listed labeled goods, it will be impossible to use not only UTII, but also PSN.

Therefore, the transition to the PSN will not be suitable for legal entities, large entrepreneurs and many retailers. They will have to choose between the general tax system (OSNO) and the simplified tax system (STS).

At first glance, it seems that the choice is obvious. Even the very name of “simplified” hints that working in this format will be easier than with OSNO.

However, not all so simple…

If either at a loss, then under the simplified tax system you will still have to pay taxes. This will be 6% of revenue for the “Income” object or a minimum 1% tax for the “Revenue minus expenses” option.

And with OSNO, work without profit does not imply the payment of turnover taxes at all. Moreover, with this system, you can return VAT from the budget or transfer losses to reduce income tax in the future.

Although we should not forget that with OSNO you will in any case have to keep the most complex and detailed records.

But if your business is highly profitable, then, of course, it will be more profitable to work on a “simplified” basis. But even here the businessman faces a dilemma: he can pay (excluding benefits) 6% of income or 15% of the difference between income and expenses.

of taxation object here is primarily influenced by the share of costs in revenue: the greater it is, the more profitable the “Income minus expenses” object will be for the businessman. You also need to take into account the possibility of applying tax deductions associated with the payment of insurance premiums and trade taxes.

But if costs and revenue are approximately comparable, then it is worth reconsidering the option of using OSNO.

Let's go to patent

With the abolition of UTII when combined with the simplified tax system, a patent looks like the most suitable tax regime for replacement. It is most compatible with UTII, and it was created as an alternative to imputation. Their permitted types of activities are basically the same (Article 346.43 of the Tax Code of the Russian Federation).

PSN, like UTII, is regulated by regional legislation, and to make sure that you can work on a patent, you need to go to the special website of the Federal Tax Service for calculating the amount of tax. If, after selecting a municipality and a branch of the tax service, the activities of an individual entrepreneur are on the list of choices, then there are no problems with the transition to PSN.

But if suddenly the activity of an individual entrepreneur is not suitable for a patent, you will have to conduct it using the simplified tax system. Simplified law has no restrictions on permitted types of activities.

The requirements for a patent are more stringent than for imputation:

- no more than 15 employees (UTII - no more than 100);

- no more than 60 million rubles of revenue per year (imputation does not have such a limitation, but we believe that no more than 150 million rubles, since when this amount is reached, all taxpayers are transferred to OSNO);

- in public catering, the area of the hall for serving visitors is up to 50 square meters, at UTII - up to 150 square meters;

- the tenant cannot sublease space or leased property; there is no such restriction in the UTII.

At the same time, PSN payers do not have to submit declarations like imputed taxpayers. When choosing a patent, newly created individual entrepreneurs can count on tax holidays for up to two years. What types of activities fall under this benefit, and whether it is valid in your region, check on the website of the local branch of the Federal Tax Service.

The basis for calculating the cost of a patent is the estimated income for the year, and it is established by the legislative authorities of the region for each type of activity and locality. They are all listed in the annex to the special patent law.

The tax rate is 6% of the estimated amount of income (in the Republic of Crimea and Sevastopol - 4%). What can the simplified tax system be combined with? Definitely with PSN. A patent can be combined with both OSNO and Unified Agricultural Tax.

It is allowed to purchase several patents, including in different regions. At the same time, you cannot go beyond the limits on revenue and number - in the sum of all patents.

You can switch to PSN for any period from 1 to 12 months, but within one calendar year. For example, if an individual entrepreneur decides to switch to a patent in August, then he will not be able to buy it for more than 5 months.

To switch to PSN, you need to fill out an application using any of the two forms recommended by the tax service:

- according to form 26.5-1 (by order of the Federal Tax Service of the Russian Federation dated July 11, 2017 No. ММВ-7-3/ [email protected] );

- in accordance with the letter of the Federal Tax Service of the Russian Federation dated February 18, 2020 No. SD-4-3/ [email protected]

The deadline for filing an application is 10 working days before the start date of using the patent.

If you need to start on January 1, 2021, we send the application to the Federal Tax Service no later than December 31, 2021.

How to switch from UTII to other tax regimes

The easiest way is to switch to OSNO, because... To do this, you don’t need to do anything at all, but just wait until the UTII expires. After this, all businessmen who have not expressed a desire to change the tax regime will “automatically” switch to the common system.

You can switch to the “simplified” system voluntarily from the beginning of the year. To do this, you need to submit an application to the Federal Tax Service no later than December 31 of the previous year (clause 1 of Article 346.13 of the Tax Code of the Russian Federation). The organization should check its scale limitations:

- Revenue for 9 months of the current year should not exceed 112.5 million rubles.

- The residual value of fixed assets as of October 1 should not exceed 150 million rubles.

Only entrepreneurs have the right to switch to PSN. If the individual entrepreneur meets the restrictions on the scale and type of activity, then he can “go for a patent” at any time. You only need to submit a corresponding application 10 days in advance (clause 2 of Article 346.45 of the Tax Code of the Russian Federation).

From simplified tax system to UTII

In 2021, the Ministry of Finance confirmed that it is possible to transfer activities from the simplified tax system to UTII at any time, and it is not necessary to wait until next year. Moreover, both current activities on the simplified tax system and completely new ones. The main thing is that it falls under the conditions for applying UTII in your region.

In this case, it is not necessary and not even necessary to abandon the simplified tax system. It is better to leave the simplified tax system as a safety net in case some income does not fall under UTII. Otherwise, you will have to report under a complex basic tax system (OSNO). If your income is only within the framework of UTII, at the end of the year, simply submit a zero declaration under the simplified tax system.

Lost the right to the simplified tax system

If you have lost the right to the simplified tax system, then first switch to the general taxation system (OSNO). And after that, transfer the business to UTII from any date.

Submit reports in three clicks

Elba will calculate taxes and prepare business reports based on the simplified tax system and patent. It will also help you create invoices, acts and invoices.

Try 30 days free Gift for new entrepreneurs A year on “Premium” for individual entrepreneurs under 3 months

Features of the transition from UTII in tables

Transition from UTII to the simplified taxation system (STS)

| Questions | Conditions for switching to the special regime |

| Who can switch to the simplified tax system | Companies (IP) whose income excluding VAT for January - September 2019 did not exceed 112.5 million rubles. |

| Scope of application of the simplified tax system in comparison with UTII | UTII: applies to a limited list of activities, the rest of the activities are taxed under other regimes. |

| Limitations of the use of the simplified tax system in comparison with UTII | UTII: no restrictions on revenue, on the cost of fixed assets. Simplified Taxation System: cannot be used for revenues exceeding RUB 120 million during a calendar year. or if the residual value of fixed assets exceeds 150 million rubles. |

| Pros and cons of the simplified tax system compared to UTII | With UTII there is no tax accounting; the tax return is submitted quarterly. Under the simplified tax system, it is necessary to keep tax records, but the tax return is submitted only once a year. |

| How to switch to the simplified tax system from 01/01/2020 | Before December 31, 2019, submit to the Federal Tax Service at your place of location (residence) a notification of the application of the simplified tax system in form No. 26.2-1. Before 01/05/2020, submit to the Federal Tax Service at the place of registration as a UTII payer an application for deregistration as a UTII payer in form No. UTII-3 (for individual entrepreneurs - in form No. UTII-4). |

| Object of taxation | It can be changed at the choice of the taxpayer annually by submitting to the Federal Tax Service at the place of location (residence) a notification in Form No. 26.2-6 no later than December 31 of the year preceding the year of change of the taxable object. "Income": — rate from 0 to 6% (specific rates are established by regional laws); — expenses are not taken into account; - tax (advance payments) is reduced by the amount of insurance premiums paid: for individual entrepreneurs without employees - in full; for others - within 50% of the tax amount; - can be beneficial if expenses do not exceed 60% of income. “Income minus expenses”: — rate from 3 to 15% (specific rates are established by regional laws); 0% - for individual entrepreneurs in some cases, taking into account regional legislation (“tax holidays”); — expenses are taken into account strictly according to the list established in clause 1 of Art. 346.16 Tax Code of the Russian Federation; - can be beneficial if expenses exceed 60% of income; - mandatory for participation in a simple partnership agreement or trust management of property |

| Features of the application of the simplified tax system | Income and expenses are accounted for on a cash basis; advances are included in income on the date of receipt; expenses for goods are taken into account after their sale; expenses for fixed assets and intangible assets are taken into account during the calendar year in equal shares quarterly after commissioning. |

| Tax accounting and reporting on the simplified tax system | Tax accounting is kept in the book of income and expenses (approved by Order of the Ministry of Finance of Russia dated October 22, 2012 No. 135n). The tax return is submitted only at the end of the year. |

| Paying tax | Advance payments are paid quarterly, the tax is paid no later than the deadline for filing the declaration. |

Transition from UTII to the patent taxation system (PTS)

| Questions | Conditions for switching to the special regime |

| Who can switch to PSN | Only individual entrepreneurs engaged in the types of activities specified in clause 2 of Art. 346.43 of the Tax Code of the Russian Federation, as well as the provision of household services, in addition to those specified in paragraph 2 of Art. 346.43 of the Tax Code of the Russian Federation, if the law of the subject of the Russian Federation in which the relevant activity is carried out introduces this regime for specific types of household services. |

| Scope of application of PSN in comparison with UTII | UTII: can be used by both individual entrepreneurs and legal entities. PSN: can only be used by individual entrepreneurs. |

| Limitations of the use of PSN in comparison with UTII | UTII: there is no limit on revenue, the permitted number of employees is up to 100. PSN: income limit for all types of activities subject to PSN (including income under the simplified tax system, if this regime is applied simultaneously with PSN) - 60 million rubles. per calendar year. The limit of employees engaged in all types of individual entrepreneur activities subject to PSN is no more than 15. |

| Pros and cons of PSN compared to UTII | With UTII there is no tax accounting; the tax return is submitted quarterly. With PSN, it is necessary to keep tax records, but there is no tax reporting. |

| How to switch to PSN from 01/01/2020 | Before December 17, 2019, submit an application to the Federal Tax Service for a patent in form No. 26.5-1. Before 01/05/2020, submit to the Federal Tax Service at the place of registration as a UTII payer an application for deregistration as a UTII payer in form No. - UTII-3 (for individual entrepreneurs - in form No. - UTII-4). |

| Tax calculation procedure | In general, the tax is calculated using the formula: tax = ST X (PVGD / 12 X KM), where ST is the tax rate (from 0 to 6%); PVGD - the amount of potential annual income established by regional law; KM - the number of months for which the patent was received (no more than 12). |

| Tax accounting and reporting on PSN | Tax accounting is kept in the book of income and expenses (approved by Order of the Ministry of Finance of the Russian Federation dated October 22, 2012 - 135n), which is maintained for each patent. No tax return is submitted. |

| Paying tax | If the patent was received for a period of up to 6 months - in the amount of the full amount of tax no later than the expiration date of the patent. If the patent was received for a period of 6 months to a calendar year: - in the amount of 1/3 of the tax amount no later than 90 calendar days after the patent comes into effect; - in the amount of 2/3 of the tax amount no later than the expiration date of the patent. |

Transition from UTII to professional income tax (NPT)

| Questions | Conditions for switching to the special regime |

| Who can switch to NAP | Individual entrepreneurs operating in the territories of those constituent entities of the Russian Federation in which the NAP taxation system has been introduced. |

| Scope of application of NPD in comparison with UTII | UTII: can be used by both individual entrepreneurs and legal entities. NAP: applied only by individuals (including those with individual entrepreneur status). |

| Limitations of the use of NPD in comparison with UTII | UTII: it is possible to use a special regime for the resale of purchased goods in retail trade. The limit on the number of employees is up to 100 people. NAP: not applicable:

|

| Pros and cons of NPD compared to UTII | For UTII, it is necessary to use online cash register when receiving payments from individuals (except for individual entrepreneurs on UTII who do not have employees and do not resell purchased goods) and submit a tax return. For NPAs, there is no need to use online cash registers, since receipts are generated in the “My Tax” mobile application; There is no tax reporting. With UTII, individual entrepreneurs are required to pay insurance premiums in a fixed amount. The NAP payer is not required to pay insurance premiums. |

| How to switch to NPD from 01/01/2020 | On 01/01/2020, submit an application for registration as an NPT payer through a special service on the website of the Federal Tax Service “My Tax”. Before 01/05/2020, submit to the Federal Tax Service at the place of registration as a UTII payer an application for deregistration as a UTII payer in form No. UTII-3 (for individual entrepreneurs - in form No. UTII-4). |

| Tax calculation procedure | The tax rate is 4% of revenue received from individuals and 6% of revenue received from legal entities. Income is recognized on a cash basis, i.e. on the date the payer receives the NPD (for settlements through an agent - on the last day of the month in which the agent received payment in favor of the payer of the NPD). When calculating tax, a one-time tax deduction in the amount of RUB 10,000 is applied. |

| Tax accounting and reporting on NAP | Tax records are not kept. There is no tax reporting. |

| Paying tax | The tax is calculated monthly by the tax authority and paid no later than the 25th day of the following month. |

The end of UTII: nine important questions about the abolition of the special tax regime

From January 1, 2021, Russian entrepreneurs will no longer be able to use one of the most popular special tax regimes - the single tax on imputed income. In this regard, by the end of 2021, organizations and individual entrepreneurs on UTII will have to change the tax regime. In this article we answer the most important questions regarding the abolition of UTII and changes in the tax regime.

Why is UTII being cancelled?

This tax regime was introduced by the state for taxation in those areas of activity where buyers made predominantly cash payments - retail trade, household services, private transportation, etc. It was impossible to effectively control the amount of income received by an entrepreneur or company.

Over the years of using UTII, in the absence of control over the real income of taxpayers, a situation has arisen where small companies with small revenues pay the same tax as those taxpayers with extremely high incomes. In fact, from the point of view of tax specialists, UTII has become not only a tool for supporting small businesses, but also a way to optimize taxation for large taxpayers.

Since the beginning of 2021, the list of those who can apply UTII has been reduced due to the introduction of additional conditions for the application of this regime. Now it could not be used by individual entrepreneurs and companies whose activities are related to the sale of goods subject to mandatory labeling:

- products made from natural fur;

- shoes;

- medications.

From July 1, 2021, all UTII taxpayers with hired employees are required to use cash register equipment (CCT). And individual entrepreneurs who, without the help of hired personnel, perform work or provide services, as well as sell goods of their own production, are required to use CCP from July 1, 2021. Thus, the state has practically solved the problem of obtaining information about the real income of taxpayers.

If we consider foreign experience, most of the world's leading economies (EU countries, Brazil, Canada, Norway, USA, Japan and others) do not have such tax regimes. Peculiar analogues of imputed income can be found only in developing countries (Vietnam, Zimbabwe, India, Kenya, Colombia, El Salvador and others).

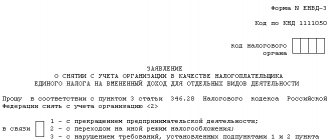

Do I need to deregister with the tax authorities?

UTII as a tax regime ceases to operate on January 1, 2021. From the same day, organizations and individual entrepreneurs whose business activities were subject to a single tax on imputed income will be automatically deregistered as UTII payers.

To automatically deregister as a payer of this tax, you do not need to provide any documents to the tax authority. Notifications that a company or individual entrepreneur has been deregistered will not be sent.

How to choose the optimal tax regime

By the end of 2021, companies and individual entrepreneurs using UTII will have to choose a different taxation regime and notify the tax authorities about it. According to the Tax Code, small and medium-sized businesses can use the general tax regime and four special tax regimes:

- STS (simplified tax regime);

- PSN (patent system);

- Unified Tax for Agricultural Producers (Unified Tax for Agricultural Producers);

- NPI (professional income tax).

There is a service on the Federal Tax Service website. It allows you to select the optimal mode based on specified conditions - expected income, number of employees, the need to maintain tax records, the presence of production of excisable goods, etc.

You can use another method to select a tax regime - a program that has a “Comparison of Tax Regimes” function, which allows you to select the optimal regime based on your data. It is enough to indicate revenue, the number of employees and their salaries, the approximate amount of expenses - and the program will show the applicable tax regimes and the size of the tax burden for each of them. You can learn more about this from the video:

The 1C:BusinessStart program can be used free of charge for 30 days; you can register in the service.

How to switch from UTII to simplified tax system

The simplified taxation system is the most popular of the special tax regimes. Now in Russia it is used by 3.2 million taxpayers.

For taxation under the simplified tax system, you can choose “income” as an object (taxed at 6%) or “income minus expenses” (rate 15%). At the same time, constituent entities of the Russian Federation can reduce these rates to 1% and 5%, respectively. Therefore, when deciding on a new tax regime, you should study the legislation of the subject of the Russian Federation in which the legal entity or individual entrepreneur is located.

There is a limitation for switching to the simplified tax system - this regime cannot be used by organizations and entrepreneurs whose income exceeds 150 million rubles per year and who have more than 100 employees.

Under the simplified tax system, the taxpayer, just like under UTII, is exempt from paying certain taxes:

- VAT;

- property tax;

- income tax;

- Personal income tax (only for individual entrepreneurs).

He must submit a tax return once a year - at the end of the year and make advance payments based on the results of the reporting period (first quarter, half a year and 9 months). A taxpayer who applies the simplified tax system with the object “income” can reduce the calculated tax on insurance premiums paid.

Payers of the simplified tax system must keep a book of income and expenses to calculate the tax base. In it they must reflect all business transactions.

Notification of the transition to the simplified tax system must be sent to the tax office at the place of registration of the legal entity or place of residence of the individual entrepreneur no later than December 31, 2021. This can be done in several ways:

- come to the tax authorities in person;

- send a legal representative to the tax authorities;

- send a registered letter;

- send an email with an electronic digital signature;

- for individual entrepreneurs - submit an application through your personal account on the Federal Tax Service website.

The notice must indicate the residual value of the legal entity's fixed assets (for individual entrepreneurs it is not necessary to indicate). There is a limit of 150 million rubles as of January 1, 2021. If now the residual value is, for example, 200 million rubles, but by January 1, 2021 it will be 150 million rubles, you can switch to the simplified tax system. The amount of income as of October 1 of the current year (the last year before the transition to the simplified tax system) is also indicated. The limit is 112.5 million rubles. If it is greater, switching to the simplified tax system is prohibited.

Most UTII payers use the type of activity “Trade through retail chain facilities.” In anticipation of the abolition of UTII, many of them have accumulated inventory, which will most likely be sold in 2021, when these taxpayers begin to apply the simplified tax system. The question arises - how to take these costs into account? A payer of the simplified tax system with the object of taxation “income minus expenses” has the right to take into account expenses on the purchase of goods for further sale, but only if there are documents that confirm these expenses.

How to switch from UTII to PSN

The patent system can be used by individual entrepreneurs; the object of taxation under this regime is potential income. PSN is applied for certain types of activities. At the same time, the constituent entities of the Russian Federation can supplement the common list of activities related to household services.

This regime sets restrictions - individual entrepreneurs must have no more than 15 employees, and income cannot exceed 60 million rubles per year. If the payer combines the PSN with the simplified tax system (this is permitted by law), then he has the right to attract up to 100 employees. An entrepreneur can use up to 15 of them for the purpose of applying PSN.

To obtain a patent from January 1, 2021, he must submit a corresponding application to the tax authority at his place of residence no later than 10 days before the start of application of the regime (that is, before December 17, 2021). Now, for the convenience of users, the tax service accepts such applications not only at the place of residence of the entrepreneur, but also at any tax authority that serves taxpayers. The patent or refusal to issue it will be sent to the entrepreneur no later than 5 days from the moment the tax service receives the corresponding application.

When switching from UTII to PSN, the payer himself chooses for how long he wants to receive a patent - from 1 to 12 months. In this case, you can obtain several patents for carrying out different types of activities. The advantage of a patent over UTII is that you do not need to provide a tax return. An entrepreneur submits an application to switch to PSN, receives a patent, along with a payment receipt, which he pays - and that’s it.

How to switch from UTII to NAP

The professional income tax is valid in all regions of the Russian Federation, and it is aimed at reducing the tax burden on the self-employed. When using this mode, you do not need to register as an individual entrepreneur, you do not need to use cash registers or provide tax reporting. But there is one caveat - you can conduct business without registering as an individual entrepreneur, if the law provides for it. For example, if your type of activity requires obtaining a license, then you should register as an individual entrepreneur.

The main restrictions for the application of the NPD regime:

- a ban on the resale of goods purchased from third parties (you can sell goods of your own production);

- it is impossible to attract employees under employment contracts;

- cannot be combined with other tax regimes;

- a self-employed person cannot act as an intermediary - resell goods or property rights.

The most important advantage of this tax regime is that the NAP payer does not pay insurance premiums.

Individual entrepreneurs on UTII can switch to NAP. To do this, they must submit an application to the tax authorities through:

- mobile application “My Tax”;

- government services website;

- taxpayer’s personal account on the Federal Tax Service website;

- authorized bank.

The date the application is sent to the tax authority is considered the date of registration as a tax payer. Moreover, if the transition is carried out during 2021, then the individual entrepreneur must refuse to use UTII. To do this, you must send a refusal within one month from the date of registration as self-employed. If this refusal is sent later than within a month, then the registration of the individual entrepreneur as a self-employed person will be cancelled.

How to switch from UTII to Unified Agricultural Tax

This tax regime can be chosen only by organizations or individual entrepreneurs engaged in agriculture - producing agricultural products or processing and selling them, as well as providing services in the field of crop production and livestock farming. The only limitation is that the share of their total income from the sale of these services must be at least 70%.

In order to switch to the Unified Agricultural Tax from next year, you must submit a corresponding application to the tax office at the place of registration of the organization or place of residence of the individual entrepreneur before December 31, 2021. The application must indicate data on the share of income from the sale of agricultural products and from the provision of services to agricultural producers.

What happens if you don’t choose a tax regime in 2021

Individual entrepreneurs and organizations that, upon registration, submitted an application only for the use of UTII, formally combine it with the general taxation regime (OSNO). If they do not provide notice of their chosen regime by the end of 2020, they will automatically switch to OSNO. It provides for the payment of several taxes, including VAT.

Organizations and individual entrepreneurs engaged in agriculture will also be transferred to the general taxation regime if they do not submit an application to switch to the Unified Agricultural Tax by December 31, 2020.

Is it possible to change the decision to switch to a different tax regime before the end of 2021?

If an individual entrepreneur or organization submitted an application to the tax office to switch to a new tax regime, but then changed their mind, then they can change their decision until December 31, 2021. In this case, a new notification must be submitted. It must be accompanied by a letter in free form about the cancellation of the previous notification.

Also in the Tax Code there is a provision according to which the taxpayer has the right to change the tax regime from the beginning of the calendar year. To do this, you need to notify the tax authorities of your new decision before January 15, 2021.

In order not to miss an interesting and useful article about small business for you, subscribe to ours

, and .

biz360

Conclusion

From the beginning of 2021, UTII will be abolished. Therefore, all “imputed” businessmen now need to think about what tax regime they will work under in the future.

And those who sell retail medicines, shoes and fur products need to hurry up with a decision: for them the UTII will not be valid from the beginning of 2021.

The possibility and benefit of switching to a particular tax regime depends both on the organizational and legal form of the business and on its financial performance.

How to switch to simplified tax system

If you can still switch to the simplified tax system, then do it from the beginning of the month in which you stopped being a UTII payer. To do this you need:

— refuse UTII within 5 working days from the date of termination of activity. Organizations submit an application for UTII-3, individual entrepreneurs - UTII-4;

- switch to the simplified tax system. Send the notice within 30 calendar days after you withdraw from UTII.

This is important to know: Line 010 VAT in the declaration: what is reflected

On May 4, the tax office deregistered Insight LLC from the UTII register; the LLC can apply the simplified tax regime from May 1. But to do this, no later than June 3, she must notify the inspectorate about the transition to the simplified tax system.