By law, companies that accept payments for goods, services or work in the form of cash must use cash registers in their activities. Moreover, each transaction recorded with the participation of the cash desk is confirmed by a paper check, which contains the following data: number, date and essence of the transaction, as well as the amount that was spent on it.

All actions performed over a certain period of time using a cash register are included in the cashier-operator’s journal.

- Form and sample

- Free download

- Online viewing

- Expert tested

FILES

What goals and objectives does the document solve?

The journal is a means of recording all transactions performed using a cash register. It contains information about both the receipt and expenditure of funds.

In cases where an organization has several cash registers, a journal is kept for each of them separately.

Generally speaking, having a magazine allows you to solve several different problems at once. For example, with the help of a journal, the head of an enterprise can quickly determine at any time how much money passed through the cash register for a specific period, and tax service employees, during inspections, have the opportunity to quickly compare cash register readings and figures from reporting documents with information from the journal.

Definition and role of the journal

Another name for the cashier’s book is the KM-4 form. It has been mandatory since December 25, 1998 according to Resolution No. 132 of the State Statistics Committee. For each cash register (cash register), one such summary document is required. Maintaining this journal is the responsibility of the operator, cashier, serving customers using cash registers and accepting cash from the latter as payment for products, services, work, etc. This book is the primary accounting documentation for accounting of incoming funds.

In KM-4, readings taken from the cash register and the amount of money passed through the cash register are recorded daily. At the beginning and end of the day, the employee writes down the readings of the cash register counters (the so-called Z-report) - the difference between them will be considered revenue for the current day. The main role of the cashier's journal is to reconcile the actual balance of money in the cash register with what the cash register has counted.

The need for mandatory maintenance of the KM-4 form is indicated by the letter of the Ministry of Finance No. 104 (08/30/1993) and the letter of the Federal Tax Service No. ED-4-2 / [email protected] (06/23/2014).

Do I need to register?

Like a cash register, the journal must be registered with the tax authorities.

Even the first filling of the journal occurs at the same time as the cash register is registered (the inspector punches a check with the amount of 1 ruble 11 kopecks - this value is not subsequently taken into account by either accountants or tax authorities).

To ensure that the inspector does not refuse to register a cash register, a number of other documents must be provided along with the device itself and the magazine:

- application requesting registration of the cash register;

- certificate of a legal entity or individual entrepreneur;

- KKM passport;

- rental agreement for retail space (if the company does not have its own square meters);

- cash register service agreement concluded with a specialized center, etc.

A complete list of documents can be obtained from the territorial tax service.

Responsibility and sanctions

If violations are detected in the maintenance, execution and storage of the cash register, it is possible to impose penalties on the enterprise and its employees. According to Article 15.1 of the Code of Administrative Offenses of the Russian Federation, administrative liability may be imposed on the organization for incorrect journal maintenance or its absence at the enterprise:

- for an official - from 4,000 to 5,000 rubles;

- for a legal entity - from 40,000 to 50,000 rubles.

Similarly, Article 13.20 of the Code of Administrative Offenses of the Russian Federation also provides for a fine of 100-300 rubles and up to 300-500 rubles for civilians and officials, respectively.

This article provides a detailed analysis of how a cashier-operator should fill out a book (samples are shown in the photo in the text) for a cash register at an enterprise. The duties and responsibilities of other persons (accountant or manager) when working with this document are also indicated.

What is the penalty for not having a cashier-operator’s journal?

Keeping a journal is a legal requirement, so inspectors during on-site tax audits must look at its presence and content. Failure to register a journal may result in a fine (although this penalty is not specified in the law).

It should be noted that conflicts often occurred between business representatives and tax authorities on this issue, leading to court. And, as practice has shown, the administrative penalty for the fact that the enterprise did not keep a log of the cashier-operator was removed from him in most cases.

Procedure for recording cash data

a cashier-operator journal to record data . The journal allows you to take into account data for approximately 1000 cash days, after which you need to create a new form.

To replace the journal, you must contact the Federal Tax Service with the following documents:

- Old magazine of a cashier-operator.

- A new magazine, stitched according to the rules and certified by the manager. The title page must be filled out indicating the mandatory KKM data.

- Equipment passport.

- Account card.

- Agreement with the equipment maintenance company.

- Latest Z-report. Balances at the beginning of the day are not carried over.

- Power of attorney for the person presenting the documents.

Organizations submit a free-form document indicating the employee’s rights to represent the interests of the enterprise to the Federal Tax Service. Individual entrepreneurs are represented only by notarized powers of attorney for representatives. Each of the regional branches of the Federal Tax Service has its own document requirements when replacing a journal upon its completion. The legislation does not contain requirements for annual replacement of the magazine.

Features of the document

Since 2013, unified templates for primary documents have been abolished, so today employees of organizations and enterprises have the opportunity to choose whether to keep a cashier-operator journal in free form, develop their own document form, or use the unified, previously mandatory form KM-4 . The majority, I must say, follow the third path, since the standard form contains all the necessary details and lines, which means there is no need to waste time on creating the structure and content of the journal.

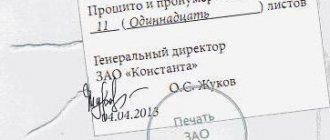

The document should be kept in paper (printed) form. In this case, all its sheets must be numbered and fastened together using a thick thread (but not with a stapler). You can use a ballpoint pen of any dark color to fill out the journal (other writing tools - felt-tip pens, pencils, etc. are unacceptable).

On the last page of the document, you must indicate the number of sheets, put a stamp (unless, of course, the use of stamps is enshrined in the company’s accounting policy), and the signature of the responsible person (accounting department specialist or chief accountant).

Entries in the journal are made strictly chronologically (without gaps), while blots and errors are extremely undesirable.

If such an oversight does occur, the incorrect data should be corrected by carefully crossing out the incorrect information and entering the correct information, making o next to it. All adjustments must be dated and certified by the signature of the cashier-operator and the chief accountant.

The book can be maintained either on a regular basis (if a retail outlet or enterprise operates every day) or as needed.

If there were no transactions involving a cash register during the accounting period, you do not need to fill out the form.

Cash book for online cash register

The cash book keeps records of all amounts received and spent: revenue, cash issued, cash deposited at the bank.

Individual entrepreneurs maintain a cash book at will and can refuse it. But for companies, a cash book is required, even if there is an online cash register.

How to keep a cash book for online cash registers

According to the Decree of the State Statistics Committee of Russia dated August 18, 1998 No. 88, the cash book is kept in the KO-4 form. But the company can approve its form according to its accounting policies.

What does a cash book look like?

The cash book can be in 3 formats:

- paper;

- electronic with file printout;

- only electronic on PC.

The cash book on paper forms must be stitched and numbered. It is operated by a cashier throughout the working day. He fills it out, having received receipt and expenditure orders from the accounting department. They allow the cashier to receive and issue funds.

How to flash a cash book and its sample

In the electronic version, the cash book is also filled out by the cashier or a responsible person appointed by management. An electronic signature issued to an official in accordance with the law dated 04/06/11 No. 63-FZ is used for it.

The cash book is filled out only once a day when funds are posted to the company. For example, if salaries were issued through the cash register on May 1 and May 15, then the corresponding dates will be recorded in the book.

If you don't keep records, the tax office may fine you. According to paragraph 1 of Art. 15.1 Code of Administrative Offenses of the Russian Federation:

- for organizations - a fine of 40–50 thousand rubles;

- for individual entrepreneurs and heads of companies - 4–5 thousand rubles.

Step-by-step cash book maintenance

Is it possible to make corrections to the cash book?

Yes, but only on paper forms. To make corrections, cross out the incorrect entry and enter the correct value. You cannot erase entries in the book. According to Instructions No. 3210-U, all corrections are certified by the cashier or chief accountant.

Corrections cannot be made to a book formatted and signed in electronic format.

How to correct an error in the cash book

How many cash books should be kept?

If you are an individual entrepreneur and optionally keep a cash book, then one is enough for you.

For organizations, the number of cash books depends on the number of branches, according to Directive No. 3210-U. If they are not there, then keep 1 book, even when combining tax regimes.

Sample document

At the beginning of the document, on the title, it is written:

- name of the organization, its address, as well as (on the right) codes: OKUD, OKPO, OKPD, INN number;

- The cash register on which the log is kept: its name (model, brand), numbers (manufacturer and registration);

- the period during which the information specified in it was entered into the journal;

- designate the employee responsible for creating the journal.

In the second part of the document, in the table, the following are entered in order:

- day-month-year of filling, and also, if the cash register operates in two shifts - shift number;

- department (here you can put dashes if the cash register serves one department, or enter all the department numbers to which the checks “went” during the current shift);

- Full name of the employee sitting at the cash register;

- serial number of the control counter at the time of shift delivery (i.e. serial number of the Z-report - its type depends on the cash register model);

- the values of the control counter, the amount of cash that has passed through the cash register since its registration with government agencies, plus the amount received during the current shift are recorded;

- The signature of the administrator and the cashier is immediately placed (if this is the same person, then you need to sign in both cells);

- the last column includes the amount of revenue for the previous day.

Next, enter into the form

- amount deposited in cash

- the amount returned to customers due to the fact that cash receipts were not used,

- signatures of responsible persons.

After compiling the journal

Since the journal is an accounting document, the procedure for its content and storage is determined either by law or by internal regulations of the organization. Regarding the storage of a document during the period of its validity, one thing can be said - it should be located either in the accounting department or next to the cash register in a place inaccessible to strangers.

After the journal expires, it must be transferred to the enterprise archive, where it must remain for at least three years, then it can be disposed of in compliance with the procedure prescribed in the legislation of the Russian Federation.

How long should you keep cash documents?

In accounting and tax legislation, there are different opinions regarding the storage period for cash documents.

In accordance with tax law, cash records must be kept in the company's archives for four years. Accounting legislation states that such papers must be kept for at least five years. The Ministry of Culture has also established a storage period for documents of five years.

Thus, based on the maximum period, cash register papers must be stored in the archive for at least five years. It is worth considering that documents can only be destroyed if an audit has been carried out over these five years. If it was not there, the papers cannot be destroyed even after five years.

The storage periods for cash documents must be observed, since the following fines are provided for their violation:

- For employees responsible for storage – from two to three thousand rubles;

- For citizens - from two hundred to three hundred rubles.

Similar articles

- Receipt cash order

- The procedure for documenting cash transactions

- Cash book (form and sample)

- Journal of registration of incoming and outgoing cash orders

- Accounting of cash transactions