Cash operations are actions related to the receipt, issuance, storage of cash and the execution of cash documents. For their management, the Central Bank has established rules: Directive dated March 11, 2014 N 3210-U and Directive dated October 7, 2013 N 3073-U. These rules are called cash discipline.

Since June 2014, a new procedure for conducting cash transactions in the Russian Federation was introduced. Compared to the previous period, the rules for conducting cash transactions have changed.

Due to the fact that many organizations and enterprises (as well as some individual entrepreneurs) keep accounting records, it would be useful to learn in more detail about the new procedure for conducting cash transactions, which began in 2014 and will continue in 2021.

It should be noted that very often regulatory organizations check the correctness of such operations. In this article we will consider changes in the legislation of the Russian Federation in 2021: organization, procedure, cash documents, as well as the cash balance limit.

Who is covered by the procedure for conducting cash transactions?

By order of the Central Bank of the Russian Federation, new rules for conducting cash transactions were introduced. At the same time, the forms for maintaining cash documents have not undergone any changes.

The changes will most affect individual entrepreneurs. And, despite the fact that individual entrepreneurs will have to change their usual mode of operation, for them this will more than pay off by simplifying cash transactions.

In addition to individual entrepreneurs, the changes will affect enterprises and organizations. In particular, innovations will affect accounting.

It is very important that individual entrepreneurs promptly familiarize themselves with the updated rules for conducting cash transactions in order to avoid penalties.

Nuances of documenting cash transactions for individual entrepreneurs

The main feature of keeping records of cash transactions of individual entrepreneurs is that entrepreneurs are allowed not to use PKO, RKO and Cash Book. The fact is that individual entrepreneurs have the right to document cash transactions in a simplified manner - in accordance with Instructions No. 3210-U.

At the same time, this procedure does not imply that the individual entrepreneur, in principle, will not keep records of the transactions in question. An entrepreneur, one way or another, must use documentation that allows him to take into account revenue, including that generated within the framework of legal relations in which it is necessary to keep a cash register.

The main document in which the individual entrepreneur reflects revenue is, as we have already defined above, the Book of Income and Expenses (or only income accounting - if the individual entrepreneur works on the PSN), or another document approved at the industry level. As a rule, it is sufficient - the need to use other documents may arise only based on the specifics of business processes at a particular facility.

Note that with UTII, the amount of income and expenses does not matter - but it is important to keep correct records of indicators that affect the calculation of tax (first of all, these are physical indicators - for example, the area of the sales floor, the number of salespeople working for individual entrepreneurs). An individual entrepreneur can keep such records on UTII in any convenient way.

At the same time, the law does not prohibit any individual entrepreneur from keeping records using cash registers, cash registers and cash registers. This scheme is quite close to many entrepreneurs, as it allows them to provide the necessary detail of business transactions. Especially if the cash register operates within the framework of labor relations, in which individual entrepreneurs’ employees can be given funds on account. Again, the scale of the business run by an individual entrepreneur plays a role.

As we already know, cash documents (in this case their analogue is the Individual Entrepreneur Income or Expense Accounting Book) are used separately from fiscal documents (although they can be filled out on their basis - since it is the fiscal documents that will be primary relative to the cash register records). In the case of individual entrepreneurs, everything is the same: the rules of fiscalization established by law do not intersect in any way with those that govern the use of cash documents.

With regard to individual entrepreneurs, the legislation on the use of cash register equipment does not establish any special conditions (with the exception of provisions on deferment in the use of online cash registers until July 1, 2019 for some categories of individual entrepreneurs). At the cash register that the entrepreneur uses, exactly the same fiscal documents are generated - checks, reports. The fact that the individual entrepreneur does not use PKO, RKO and Cash Book does not matter. However, filling out alternative accounting documents - primarily the Book of Income and Expenses - is carried out, as in the case of orders, on the basis of fiscal documents. Or - replacing them if it is not necessary to use cash registers (that is, if these are sales receipts or BSO).

Organization and management of cash transactions in 2018

As noted above, from June 2014 a new procedure for conducting cash transactions was introduced. This order can be divided into two parts:

- Regular (for legal entities, except banks).

- Simplified (for individual entrepreneurs and small businesses).

Cash transactions can only be carried out at the cash register. The person responsible for carrying out such operations is the cashier. If the company has several cashiers, then a senior cashier is appointed.

The head of the organization or an individual entrepreneur has the right to conduct cash transactions personally.

The accountant (chief accountant) signs cash documents. If there is no accountant at the enterprise, documents are signed by the cashier and the manager.

Cash transactions carried out personally by the head of the enterprise do not require additional signatures.

Since 2015, it is allowed to conduct cash transactions using software and hardware.

Changes have occurred in the management of cash transactions in separate divisions. A separate division should be understood as any division of the company (at the location of which there is at least one equipped workplace).

For such divisions, a cash balance limit and maintaining their own cash book have been introduced. The cash book sheets are now in one copy. They do not need to be returned the next day to the main office.

Cash discipline in 2021

Home / Cash discipline

| Table of contents: 1. Who is obliged to observe cash discipline 2. About the use of CCP and BSO 3. Cash documents and their execution 4. Compliance with the cash limit | 5. Settlements with accountable persons 6. Limitation of cash payments 7. Monitoring compliance with cash registers. disciplines 8. Penalties |

Cash discipline is a set of mandatory rules that business entities must follow when conducting operations to receive, store and issue cash.

Organizations and individual entrepreneurs carry out settlements using cash through the operating cash desk. It is necessary to distinguish between the concepts: the operating cash desk of an enterprise and a cash register, which in everyday life is also called “cash desk”.

A cash register is a device designed to automate the accounting of receipts of money, registration of the purchase of goods (services, works) and printing of a receipt.

Operating cash refers to the totality of all actions that are performed with cash in the process of business activity.

And the operation of receiving revenue received through a cash register is an integral part of a whole set of procedures related to the receipt, storage and issuance of cash. Any cash transaction requires documentation taking into account the standards of current legislation.

Who is required to maintain cash discipline?

All entities using cash in the process of conducting business activities are required to follow the established requirements for conducting cash transactions, regardless of:

- Tax systems;

- Applications of KKM;

- Using BSO.

Simplified rules apply to individual entrepreneurs. Entrepreneurs have the right:

- do not fill out RKO, PKO and cash book;

- do not set a cash payment limit.

But if an individual entrepreneur has hired employees, he is obliged to draw up documentation confirming the payment of wages.

Small business organizations also have the right not to limit the amount of money kept in the cash register, in accordance with the current version of Art. 4 of the Law of July 24, 2007 No. 209-FZ and the Decree of the Government of the Russian Federation of April 4, 2016 No. 265.

It should be understood that all money received by the company’s cash desk belongs to the legal entity. And even the sole founder has no right to arbitrarily use the company’s cash finances for his own needs.

Individual entrepreneurs can withdraw cash from the cash register at any time and in any quantity, the main thing is to avoid delays in paying taxes and contributions. If an individual entrepreneur uses cash documents, the issuance of amounts from the cash register for his own needs must be formalized with an expense order.

On the use of cash registers and strict reporting forms

Acceptance of revenue in cash obliges the use of cash registers, except for the following cases:

- application of UTII by organizations and individual entrepreneurs, as well as when the entrepreneur is on the PSN (until 07/01/2018, after this period it is necessary to use online cash registers);

- the use of BSO by firms and entrepreneurs when providing services to citizens;

- conducting individual entrepreneurs and organizations activities in difficult territorial conditions in which the use of cash registers is difficult.

The number of CCPs that can be in operation is not limited. All revenue received for a work shift must be posted through the company's cash register (IP).

A cash register (online cash register) is allowed for use, which:

- Registered with the tax office;

- Has a case with a serial number;

- Equipped with a fiscal storage device into which fiscal data is transferred;

- Has a built-in real-time clock;

- Checks the control numbers of the cash register registration number;

- Equipped with functionality that includes printing fiscal documents (this function may not be available for payments made via the Internet);

- Able to generate fiscal documents in electronic form and transmit them to any fiscal operator, as well as receive confirmation from the operator;

- Provides information about violations of the data exchange procedure with the fiscal operator and other problems and malfunctions of the cash register itself;

- Ensures the receipt of information about the payment amount from the terminal that transmits orders to the bank (acquiring device);

- Does not allow the generation of a check (BSO) or a corrective check (BSO) containing more than one payment indicator;

- Provides printing of a two-dimensional QR code on a receipt (BSO);

- Generates a report on the current state of calculations at any time for presentation to the inspecting inspector;

- Provides search for any document by number from the fiscal memory, its printing or transmission in electronic form;

- Executes information exchange protocols.

Cash register models that meet the requirements are entered by the Federal Tax Service into the registers of cash registers and fiscal drives.

Due to the transition to new generation cash registers from July 1, 2017, many unified forms have lost their relevance, since all the necessary information is stored in the cash register memory and can be printed at any time. Organizations (IPs) using online cash registers may NOT fill out:

- certificate-report of the cashier-operator (form KM-6);

- journal of the cashier-operator (form KM-4);

- log of KKM meter readings (form KM-5);

- act of returning money to customers (form KM-3), etc.

This documentation was necessarily completed on old cash registers. It should be noted that the above documents do not (and previously did not have) anything to do with cash discipline.

BSO forms

BSOs are developed by the organization (IP) independently, if the form for the types of services provided by the company (IP) is not approved by law. The developed BSO must comply with the requirements of the Decree of the Government of the Russian Federation dated May 6, 2008 No. 359.

This form can be used until July 1, 2018. After this date, you should use online devices that provide for the generation of BSO in electronic form.

Currently, the use of such devices is voluntary. Mandatory details for new BSOs are listed in the law of July 3, 2016 No. 290-FZ.

Copies of forms (tear-off counterfoils of the BSO) must be transferred to the main cash desk along with cash and serve as confirmation of the amount of revenue received per shift.

Cash discipline also does not include: BSO, BSO accounting book and KUDiR.

Cash documents and their execution

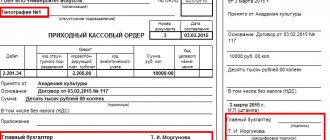

To process cash transactions, use the following standardized forms:

- Receipt cash order (form KO-1).

- Expense cash order (form KO-2).

- Cash book (form KO-4).

- Cash accounting book (form KO-5).

- Payment (form T-53) and payroll statements (form T-49).

The unified form (KO-3) of the order register is not mandatory, and administrative liability is not provided for its absence.

Registration of cash documentation is allowed both on paper and electronically.

Paper forms must contain signatures of authorized persons, electronic documents are certified with a special electronic signature.

The responsibility for conducting cash transactions rests with the cash clerk. The head of an organization or individual entrepreneur can perform the functions of a cashier independently in the absence of an authorized employee on staff.

The above cash documents are generated by the chief accountant or other responsible person appointed by order of the manager.

If there are several cash workers in the company, one of them is appointed to the position of senior cashier.

Compliance with the cash limit

The amount of money that can be in the entity's cash register after the end of the working day is limited by the established limit. All excess cash should be kept in a bank account.

The limit may not be observed:

- on the days of settlements for wages and other payments included in the payroll;

- on weekends and holidays, if the company was operating and receiving cash revenue.

The limit is set by the company independently by issuing an appropriate order. To calculate the cash balance, you should be guided by the formulas given in the Directive of the Central Bank of the Russian Federation dated March 11, 2014 No. 3210-U.

The validity period of the established limit is not established by law. If such a period is not provided for by the current order, the organization uses the approved calculation until a new order is issued by the manager.

If the cash balance limit in the company is not approved, it is recognized as zero. Inspectors will issue a fine for storing amounts in the cash register that exceed the permissible limit.

As noted earlier, small organizations and individual entrepreneurs may not set a limit.

Calculations with accountable persons

Reporting funds are issued to employees to pay expenses related to the company's business activities.

The order of the director of the company approves:

- List of such employees;

- Maximum amounts of funds issued;

- Deadlines for taking necessary actions.

Instructions of the Central Bank of the Russian Federation dated June 19, 2017 No. 4416-U changed the previously existing procedure for receiving accountable funds, namely:

- issuance of money only on the basis of a personal application from an employee (now an administrative document from the head of the organization is sufficient);

- a ban on receiving new accountable amounts by employees who have not reported on previously received funds (it is now allowed to issue money if there is a debt).

At the same time, employers are not prohibited from issuing money on account according to the old procedure - based on an employee’s application.

The employee is obliged, within three working days after the end of the period for which the cash was issued, to submit an advance report accompanied by primary documents justifying the expenses incurred.

Limitation of cash payments

Cash discipline provides for the limitation of cash settlements between organizations (IP) within 100,000 rubles per transaction.

This requirement does not apply to settlements with citizens (individuals).

There are also no limits on the amount of payments for wages, social payments and accountable amounts (the relaxation does not apply if the accountable person pays the company’s contractual obligations under a power of attorney).

It is prohibited to repay and issue loans from the proceeds received at the cash desk, pay for real estate rent and dividends.

The procedure for carrying out cash payments was approved by Directive of the Central Bank of the Russian Federation dated October 7, 2013 No. 3073-U.

Monitoring compliance with cash discipline

All personnel whose functions include conducting cash transactions are required to comply with the requirements related to compliance with cash discipline.

Control over the work of the accounting service, of which the operating cash desk is a part, is carried out by the chief accountant.

The manager (IP) is responsible for conducting business activities as a whole.

Conducting cash discipline checks is the responsibility of the tax inspectorates.

When checking, inspectors pay close attention to the following documents:

- all forms issued for cash transactions;

- order to approve the cash limit;

- accounting registers;

- expense reports;

- books (magazines) on BSO accounting.

Tax authorities exercise control over the use of online cash registers as follows:

- Carry out monitoring and analysis of data (including with the help of automated systems) in order to control the accounting of revenue (a sharp decrease in the level of revenue from a taxpayer is a reason for close attention of the inspection authorities);

- Conduct checks of the use of cash register systems, as well as remote checks of fiscal data operators;

- They check the issuance of cash register receipts (BSO) to customers, including by conducting a test purchase;

- Request additional information from the taxpayer, including through the CCP personal account;

- Get full access to fiscal data in the OFD operator’s database;

- Gain full access to the taxpayer’s cash register to retrieve information from the fiscal storage device.

Inspectors also have the right to demand any documents related to the object of inspection.

As a result of the audit, the following facts may be discovered:

- exceeding the maximum amount of cash payments and the cash limit;

- reflection of received revenue in incomplete volume;

- non-issuance of BSO and cash register checks to clients;

- use of CCP that does not meet established requirements;

- discrepancy between the actual cash balances in the cash register and the amounts stated in the documents;

- unreasonably long terms for issuing financial resources for reporting, etc.

Fines for cash discipline and cash registers

If, as a result of the inspection, inspectors identify violations, fines may be imposed in accordance with the following articles of administrative legislation:

| Cash discipline | |

| clause 1 art. 15.1 Code of Administrative Offenses of the Russian Federation | 4,000 – 5,000 rub. for an official (IP) |

| 40,000 – 50,000 rub. for legal entities persons | |

| Non-use of CCP | |

| clause 2 art. 14.5 Code of Administrative Offenses of the Russian Federation | 25 – 50% of the payment amount accepted without using cash register, but not less than 10,000 rubles. – for an official (IP) |

| 75-100% of the payment amount accepted without using cash register, but not less than 30,000 rubles. - for legal entities persons | |

| Non-use of cash registers repeatedly , if the amount of sales without the use of cash registers exceeds 1 million rubles. | |

| clause 3 art. 14.5 Code of Administrative Offenses of the Russian Federation | 1 – 2 years disqualification of the responsible person |

| up to 90 days – suspension of legal activities. persons (IP) | |

| Use of CCP that does not meet the requirements | |

| clause 4 art. 14.5 Code of Administrative Offenses of the Russian Federation | warning or fine 1,500 – 3,000 rubles. for an official (IP) |

| warning or fine 5,000 – 10,000 rubles. for legal entities faces | |

| Failure to submit documents requested by tax authorities | |

| clause 5 art. 14.5 Code of Administrative Offenses of the Russian Federation | warning or fine 1,500 – 3,000 rubles. for an official (IP) |

| warning or fine 5,000 – 10,000 rubles. for legal entities faces | |

| Failure to issue a paper check (refusal to transmit a check electronically) | |

| clause 6 art. 14.5 Code of Administrative Offenses of the Russian Federation | warning or fine of 2,000 rubles. for an official (IP) |

| warning or fine of 10,000 rubles. for legal entities faces | |

It should be noted that it is possible to bring a taxpayer to administrative liability within two months from the date of the violation.

And in case of a one-time violation of cash discipline, the subject can avoid fines. But such a fact will inevitably attract the attention of the tax authorities and, if additional shortcomings are discovered in the work of the entity, it may provoke an on-site audit.

Read in more detail: Cash discipline and responsibility for its violation

Did you like the article? Share on social media networks:

- Related Posts

- Journal of registration of incoming and outgoing cash documents

- Sample of filling out form AO-1

- Cash payment limit in 2021

- Payroll (form T-51)

- Cash withdrawal from the cash register

- Payroll statement (form T-49)

- Advance report (form AO-1)

- Sample of filling out form T-53

Discussion: 2 comments

- Christina:

07/24/2018 at 18:25Hello! Please help me figure it out! Individual entrepreneurs on UTII do not need to fill out cash receipts/expenses and maintain a cash book? On the basis of what law or legal act is this requirement canceled? The information on the Internet is different, somewhere it is said that no one has canceled the maintenance of a cash book and receipt/expenditure orders... Please provide a legal basis.

Answer

Alexei:

07/28/2018 at 00:11

Hello. Directive of the Bank of Russia dated March 11, 2014 N 3210-U (as amended on June 19, 2017) “On the procedure for conducting cash transactions by legal entities and the simplified procedure for conducting cash transactions by individual entrepreneurs and small businesses”

Quote:

"4.1. Cash transactions are formalized by incoming cash orders 0310001, outgoing cash orders 0310002 (hereinafter referred to as cash documents) ...

...Individual entrepreneurs who, in accordance with the legislation of the Russian Federation on taxes and fees, keep records of income or income and expenses and (or) other objects of taxation or physical indicators characterizing a certain type of business activity, may not draw up cash documents.

4.6. The legal entity records cash received at the cash desk, with the exception of cash accepted during the activities of a paying agent, bank payment agent (subagent), and cash issued from the cash register in the cash book 0310004...

...If individual entrepreneurs, in accordance with the legislation of the Russian Federation on taxes and fees, keep records of income or income and expenses and (or) other objects of taxation or physical indicators characterizing a certain type of business activity, they may not keep a cash book 0310004.”

Answer

Leave a comment Cancel reply

Cash documents in 2021

There were no significant changes in the field of cash documents. The cash book, receipt and expenditure orders, as well as statements have not changed. All previously unified forms continue to be used. These documents should be filled out taking into account innovations.

Individual entrepreneurs, in accordance with the new procedure for conducting cash transactions, are exempt from maintaining the following list of documents:

- cash book;

- cash receipt orders;

- expense cash orders.

Individual entrepreneurs keep tax records of income and physical indicators that characterize their type of activity.

To maintain cash documentation, you can now choose electronic or paper media.

An incoming accountant (an individual who works under a service agreement) has the right to draw up cash documents.

Separate divisions of the enterprise now transfer cash book sheets in a new way. A copy of the book sheet (which is certified by the head of the unit) is transferred in the manner established by the legal entity itself. That is, cash book sheets can be submitted once a year - when preparing financial or accounting statements.

Errors in cash documents (on paper) can now be corrected, with the exception of incoming and outgoing cash orders.

The main innovations are as follows:

- It is allowed to maintain cash documentation in electronic form using an electronic signature;

- paper copies of the cash book and orders (receipt and expense) are not required if electronic documents are available;

- It is impossible to correct errors in electronic documents (a signed document with an error is deleted and a new one is filled out in its place);

- the second sheet of the cash book is no longer relevant;

- a single receipt order can now be issued on a strict reporting form;

- The manager’s own record of terms and amounts is not required;

- there is no register of deposited amounts (but this column is retained in salary slips);

- the recipient can enter the amount in words on the expense order;

- the cash book is not filled out if no cash payments were made on any day.

The cashier puts a stamp and his signature on the receipt for the cash receipt order. Cashiers can now transfer money without a debit order based on the cash ledger.

How to simplify cash management using cash discipline

For some categories of entrepreneurs, the law provides for a simplified procedure for maintaining cash records.

According to the decree of the Central Bank of the Russian Federation, issued in March 2014, businessmen who own enterprises classified as small or micro businesses, as well as individual entrepreneurs, may not set a cash limit.

Individual entrepreneurs, in addition, may not draw up PKO and RKO (receipt and expense cash order), and also have the opportunity to refuse the cash book.

However, these privileges do not replace the obligation to create payroll records when paying wages and benefits to employees.

The category of small businesses includes organizations that fall under the conditions of Law No. 209-FZ (clause 1 of Directive No. 3210-U). They can be briefly summarized as follows:

- The organization is classified as consumer cooperatives or organizations equivalent to commercial ones (except for municipal and federal state unitary enterprises);

- The number of such enterprises should vary from 16 to 100 employees;

- Income for the year should not exceed 400 million rubles.

- If the enterprise employs up to 15 people inclusive, and the revenue for the previous year, according to reporting, did not exceed 60 million rubles, this enterprise will be classified as a micro-business.

Important!

The share of state ownership in such enterprises should not exceed 25%.

Despite the obvious conveniences, a businessman must understand that if the receipt of funds is not confirmed by a cash receipt order, the cash may simply not reach the company’s cash desk, remaining with an unscrupulous employee.

In this connection, we can conclude that simplified management of cash discipline will primarily be convenient for entrepreneurs who do not have hired employees.

Cash balance limit in 2021

In 2015, the cash balance limit was changed. The new formula for calculating the cash limit is not tied to cash receipts. The organization has the right to make calculations based on the amount of expenses or revenue.

The cash limit is mandatory, except for small and micro enterprises. It establishes the amount of funds that can be freely stored in the cash register. Enterprises and organizations have the right to personally introduce a certain limit. If the limit has not been entered, it is considered zero. The entire remaining amount is deposited into the bank account at the end of the day.

The formula for calculating the cash limit is regulated by the new regulation. An enterprise can choose one of two proposed calculation formulas:

- The calculation is made based on cash proceeds (receipts from goods, services, etc.).

- The calculation is made based on the amount of funds issued.

If there are separate divisions, the total cash limit is determined taking into account the limit established for the division.

That is, the amount of the limit can be distributed among separate divisions.

The cash limit of a separate division is established by a responsible administrative document.

The first formula for calculating the cash limit looks like this:

L = V / P x Nc , where: L - limit in rubles; V is the volume of revenue in cash; P - billing period, the number of working days for which the volume of cash receipts is recorded (but not more than 92 working days for legal entities). Nc - the period of time between depositing proceeds to the bank: 1–7 working days (if there is no bank nearby, up to 14 days).

The second formula for calculating the cash limit is L = R / P x Nc , where:

R is the volume of cash disbursement (excluding the amounts of salaries, stipends or other payments to employees).

Cash limit for small and micro enterprises

The instruction of the Bank of the Russian Federation No. 320-U dated March 11, 2014 states that all small and micro enterprises are exempt from the mandatory establishment of a cash limit. This means that these types of enterprises have the right to keep any amounts in the cash register.

The criteria for classification as micro and small enterprises are as follows:

For micro-enterprises:

- income limits on the tax return for the previous year - 120 million;

- The average number of employees for the previous year was 15 people.

For small businesses:

- income limits on the tax return for the previous year - 800 million;

- the average number of employees for the previous year was 100 people.

According to these criteria, individual entrepreneurs are classified as micro or small enterprises, therefore, it is not necessary for individual entrepreneurs to introduce a cash limit.

Issuing money from the cash register for reporting

Accountable persons are employees who are given money from the company's cash register to pay for any production services or purchase goods for internal needs. Since August 19, 2017, money against the report is issued to the employee on the basis of an internal document. Moreover, the form and name of this document are not regulated in any way by the Central Bank. Those. it must be drawn up in any form, indicating in it, in accordance with clause 6.3 of the Bank of Russia Directives dated March 11, 2014, as amended, the following data:

- Full name of the person to whom the cash is issued;

- amount of cash;

- the period for which cash is issued;

- manager's signature and date.

Until August 19, 2017, money should have been issued only on the basis of an employee’s application.

The article was edited in accordance with current legislation 06/04/2018

Filling out the cash book

If we talk about registration of KO-4, then the following requirements must be met:

- the title page of the cash book reflects the details of the organization and the responsible department (if any);

- the form corresponds to one financial year;

- Each page must be numbered.

You can fill it out manually or in accounting programs.

Some institutions maintain the form manually. On the first sheet, serial numbering opens. Entries are made with a ballpoint pen with black and blue ink. When entering information into the columns, the cashier uses a carbon copy to duplicate the entry being made. The detachable part is the one on which the “live” recording is applied. The duplicate portion remains in the cash book. Each part is signed separately. Information about RKO and PKO is included in each line. It should be the same in each of the two parts of the cash book. If on the reporting day many transactions with funds are made, and one page is not enough to deposit them, then “transfer” is marked. This column reflects the incoming and outgoing values at the time of transfer. Entries on the next sheet begin with the same number.

The end of the period is recorded by the results of PKO and RKO, and the cash balance at the end of the day is displayed. The chief accountant reconciles with primary receipts and expenditures and certifies the cash book.

The journal is stitched at the end of the year, the period is from January 1 to December 31 of the financial year. Each sheet must be numbered, stitched and stamped on the last page. It is also necessary to indicate the number of sheets stitched. The entry “In this book there are _______ sheets numbered and laced together” is required. It is certified by stitching together the signatures of the head and chief accountant of the organization (Resolution of the State Statistics Committee of the Russian Federation dated August 18, 1998 No. 88).

This might also be useful:

- Online cash registers in 2021

- Taxpayer personal account Nalog.ru

- Chart of Accounts 2019

- What an individual entrepreneur needs to know about auditing cash transactions

- Cash discipline for individual entrepreneurs in 2021

- How can an individual entrepreneur keep accounting records?

Is the information useful? Tell your friends and colleagues

Dear readers! The materials on the TBis.ru website are devoted to typical ways to resolve tax and legal issues, but each case is unique.

If you want to find out how to solve your specific issue, please contact the online consultant form. It's fast and free!