What is meant by a corrected invoice?

In ch.

21 of the Tax Code of the Russian Federation, the term “corrected invoice”, as well as “corrective”, is absent. Moreover, in both forms of invoice (both main and adjustment), proposed by Decree of the Government of the Russian Federation of December 26, 2011 No. 1137, there is a line for indicating the details of the corrections made to them. In addition, the preparation of an amended invoice is discussed in clause 6 of the Rules for filling out an invoice. Thus, it is implied that corrections are a thing that has a right to exist. Moreover, changes can be made both to the main document and to the corrected invoice.

However, it should be understood that an adjustment invoice and a corrected invoice are completely different documents:

- An adjustment invoice is needed when changes are made to the original data of the primary document (quantity and price), affecting the calculation of the final sales amount recorded in it and the associated VAT amount. Moreover, the adjustment does not mean that an error was made in the original version of the invoice. No, the issuance of an adjustment invoice can be caused by changes in the source data that occurred under the influence of some factors, most often documented (agreements on price changes, retro discounts, identification of shortages, defects or surpluses among the delivered goods).

Learn more about this invoice - “What is an adjustment invoice and when is it needed?” .

- The need for a corrected invoice arises when technical errors are discovered in the original document, which may have negative consequences for receiving deductions on it. However, not all errors result in the need to create a corrected invoice. If they do not affect the correct understanding of the information on the details in which they are included (even mandatory ones), then a deduction on such a document is permissible (clause 2 of Article 169 of the Tax Code of the Russian Federation) - therefore, there is no need for a corrected invoice.

See also “An error has crept into the invoice: should I draw up a corrected or corrective document?” .

The concept of a corrected invoice as an adjusted source document arose from the adoption of Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137, i.e. since 2012. Previously, a significant part of the technical errors made in the preparation of an invoice could be corrected directly in the incorrect source document, having certified the corrections with the signature and seal of the originator. After the entry into force of this resolution, the amended invoice was given the status of an independent document, with all the ensuing consequences.

Incorrect checkpoint on the invoice

Incorrect indication of the checkpoint on the invoice does not entail tax consequences for either the seller or the buyer. The checkpoint is not a mandatory detail in the invoice according to the Tax Code of the Russian Federation. In addition, an incorrect checkpoint does not interfere with identifying the seller and buyer if other mandatory invoice details (name, tax identification number, address) are indicated correctly (clause 2, clause 5, 5.1, 5.2 of Article 169 of the Tax Code of the Russian Federation).

If the checkpoint is not indicated in the invoice, then the buyer also cannot be denied a VAT deduction if the remaining details of the invoice (name, tax identification number, address) are indicated correctly and allow identification of the seller and the buyer (clause 2, clause 2 p 5, paragraph 2, paragraph 5.1, article 169 of the Tax Code of the Russian Federation).

In what cases is an invoice correction required?

So in what cases is a corrected invoice issued? It is needed when it becomes necessary to correct a technical error in the source document. For example, you may need to create a corrected invoice if there is an error:

- in the date, if the original document was mistakenly issued in a different month, year;

- details of the supplier or buyer, if they are written not just with a typo, but do not correspond to them at all (incorrect TIN, address, name, etc.);

- indication of the shipper and consignee, if they do not belong to the persons who actually sent and received the goods;

- details of the document for the transfer of the advance;

- name and currency code of the document;

- indicating the name of the product (work, service);

- indicating an incorrect price or quantity of goods;

- in the rate and, as a consequence, in the amount of VAT and the final amount of the document;

- or in the absence of data required to be filled in for imported goods (country of origin and registration number of the customs declaration).

It should be noted that most taxpayers, if an error is discovered in a timely manner and has not yet been identified by the tax authorities, prefer not to make a corrected invoice, but simply replace the defective document.

For errors that do not require correction, read the article “What errors in filling out an invoice are not critical for VAT deduction?” .

For information about what errors in the invoice should be corrected, read the article “We made a mistake in the invoice - what and how to correct it.”

Invoice Correction Form

There is no specific form for the revised invoice. It is drawn up in the same form in which the original document requiring correction was drawn up, i.e. main or adjustment. Both forms are contained in Appendices 1 and 2, respectively, of the Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137. In this case, the preparation of a corrected invoice can be carried out if it is necessary to correct invoices previously issued:

- for implementation;

- for an advance;

- for adjustments, including to several amended documents.

You can find the invoice form, including the one intended for correction, in the article .

Technical errors

Let's look at technical errors that are common in invoices.

Document date

The document date (in paper invoices) can be entered in any convenient way. This can be in the format DD.MM.YYYY, DD.MM.YY or DD.month.YYYY.

But in electronic invoices, the date format is set as follows: DD.MM.YYYY (section II of Appendix No. 1 to the order of the Federal Tax Service of Russia dated March 5, 2012 No. ММВ76/ [email protected] ).

Address

Mistakes are often made when indicating the house number, building number, or occupied premises number in the address. In these cases, courts most often rule on deductions in favor of taxpayers. After all, incorrect indication or absence of a house number (or office number, or occupied premises, or absence of a house block number) with the correct TIN and KPP of the counterparty and other details provided for in Article 169 of the Tax Code of the Russian Federation, can be regarded as a clerical error. Of course, this means minimal distortion, which does not allow us to claim that the taxpayer is in bad faith.

Arbitrators note that often an error can be eliminated by submitting corrected invoices, for example, as part of a desk tax audit. At the same time, the remaining details must be sufficient to reliably and unambiguously identify the taxpayer. Such decisions were made, for example, in the resolutions of the Federal Antimonopoly Service of the North-Western District dated January 28, 2013 No. A442943/2012 and dated December 16, 2011 No. A521398/2011, the Federal Antimonopoly Service of the North Caucasus District dated September 30, 2009 No. A5320754/ 2008. But there are judicial acts confirming that failure to indicate or incorrectly indicate in the invoice the number of the house, building or number of the occupied premises is one of the grounds for refusal to deduct (Resolution of the Federal Antimonopoly Service of the North Caucasus District dated August 5, 2008 No. F084431/2008) .

Buyer's name

If the invoice contains typos in the name of the buyer (capital letters are replaced by lowercase ones and vice versa, extra symbols are added (dashes, commas, etc.), but such an invoice does not prevent the tax authorities from identifying the indicated indicators during an audit, then this typo is not a basis for refusal to deduct tax amounts (letter of the Ministry of Finance of Russia dated May 2, 2012 No. 030711/130).

It is permissible to indicate both the full and abbreviated name. If the specified options correspond to the constituent documents, then they are allowed in the invoice (subparagraphs “i”, “k” of paragraph 1 of the Rules for filling out an invoice, approved by Decree of the Government of the Russian Federation of December 26, 2011 No. 1137).

Currency name

The currency is indicated on line 7 of the invoice. This should be done in accordance with the All-Russian Classifier of Currencies. For example, “Russian ruble”, code – 643. Sometimes suppliers may simply indicate “rub.” This is incorrect, but it is possible to determine the currency in which the document is drawn up. Especially if the code is specified. Deductions on such invoices are permissible, but they need to be corrected (letter of the Ministry of Finance of Russia dated March 11, 2012 No. 030708/68).

Data on imported goods

Often in invoices, due to the fault of the importer, the columns “Country of origin of goods” or “Customs declaration number” are filled in incorrectly. According to paragraph 5 of Article 169 of the Tax Code of the Russian Federation, the taxpayer selling these goods is responsible for the compliance of the specified information in the invoices presented to him with the information contained in the invoices he received.

Features of filling out an amended invoice

In both forms of the corrected invoice, under the main heading of the document containing its number and date, a line (or lines) is provided for entering the number and date of the correction:

- there is only one line in the invoice, and it is located directly under the heading;

- in the adjustment invoice—2: one is intended for information about the correction of the adjustment invoice itself, and the second is for indicating the details of the original invoice for which the adjustment invoice was drawn up.

There are no other features in the design of the corrected invoice. It is formatted in the same way as a regular one, only incorrect data in it is replaced with correct ones.

Feature of changing numbers in 1C

Regardless of the 1C version, you will not be able to assign an already occupied number to a directory element or document. This means if this number is already occupied by an object of the same type, since different documents and directory elements have their own numbering. An exception is the ability to assign a busy number, but for another organization in the database, since different organizations also have their own sequence of numbers.

If you want to change the invoice number, for example to 4212, but it is already occupied, then you will first need to free this number. To do this, you must first change the number of the invoice that this number occupies. You can change it, as usual, to any unoccupied one (for example, 99999999).

After this, we assign the vacant number (4212) to the document you need. See for yourself what to do with another renumbered document. For example, you can change the temporary number 99999999 to the one that occupied the invoice you renumbered.

As you can see, I have given here a typical operation for correcting the numbering of 1C invoices, in which it is necessary to swap the numbers of documents. This situation easily arises when a document is recorded with the wrong date (regarding the date, be sure to read this). If you simply need to assign a different number to the invoice and this number is not occupied, then the task is ridiculously simplified and can be done in a few seconds.

If you haven’t even written down the invoice yet, but already want to IMMEDIATELY assign a specific number to it, then this is impossible. So write down the document first, and then change the number. The ability to independently set document numbers is very, very rare, since this is not necessary.

When changing the invoice number in 1C Enterprise, it is not necessary to indicate insignificant zeros on the left.

A special video course on this configuration, which includes 42 hours of practical materials, will help you understand the features of 1C: Accounting 8.3, as well as learn how to keep records without outside help. Check out sample lessons and course curriculum!

Features of registering an amended invoice

If the correction invoice is issued in the same quarter as the original invoice (adjustment invoice), then in the same quarter:

- The seller must register the corrected invoice in the sales book and re-register the erroneous invoice, but reflect all its numerical indicators with a minus sign.

ConsultantPlus experts have prepared an example of registering a corrected invoice in the sales book. Go ahead and get trial access to K+ for free.

- The buyer, if he has reflected an erroneous invoice in the purchase book, must register a corrected invoice in the purchase book and re-register the erroneous invoice, but reflect all its numerical indicators with a minus sign. If the buyer has not shown an erroneous invoice in the purchase ledger, he only records the corrective invoice.

An example of registering a corrected invoice in the purchase book is available in the ConsultantPlus system. Get trial access to the system for free.

In the diagram, we showed the procedure for the seller and buyer when the data in the invoice changes or if there are errors in it.

If the corrective invoice was drawn up in another (next) quarter:

- The seller must record the corrected invoice on an additional sheet of the sales ledger for the quarter in which the erroneous invoice was recorded. In the same additional sheet of the sales book, register the erroneous invoice, indicating all its numerical indicators with a minus sign.

- The buyer must draw up an additional sheet to the purchase book for the quarter in which he registered the erroneous invoice and, in the same additional sheet to the sales book, register the erroneous invoice, indicating all its numerical indicators with a minus sign. If the buyer initially did not reflect the invoice issued with errors in the purchase book, then the corrected one must register the corrected invoice only in the purchase book of the quarter in which this document was received.

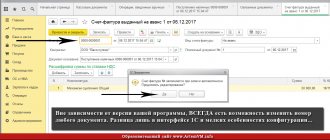

How to correct the invoice number in 1C 8.3

First, you need to be able to see the field of this very number. If this attribute is hidden for some reason, then display it.

To correct an invoice number in 1C, open the document and simply click on the number field and press, for example, the Backspace key (the button above Enter with a left arrow used to erase text). The Number field cannot be easily edited in most documents, so it is locked by default.

Important point:

1C will ask you if you really want to change the number. Answer Yes. In this case, the invoice number field will become active and you can set the number that you need. Don't forget to write down the document.

Results

Changes to the invoice and adjustment invoice not related to amendments to the quantity, cost of goods (work, services) and tax obligations are made accordingly on the form of the invoice, adjustment invoice. When drawing up correction documents, it is necessary to indicate the details of the original document in which the error was made. The procedure for registering a corrective invoice depends on the period in which it was drawn up in relation to the erroneous invoice, and for the buyer also on whether he or she registered an invoice containing errors in the purchase book.

Sources:

- Tax Code of the Russian Federation

- Decree of the Government of the Russian Federation of December 26, 2011 N 1137

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Correction or corrective S-F: what and when is it better to choose to make changes?

Amendments to the invoice only require the correction of one of the parties , while an adjustment to the cost (or quantity of goods) requires the parties to sign an appropriate agreement.

Reference ! The main reason for drawing up an adjustment invoice is changes in the cost of previously shipped goods (services provided or work performed) (clause 3 of Article 168 and clause 10 of Article 172 of the Tax Code of the Russian Federation).

How to correct an error in the invoice number in the VAT return and make changes? Such an invoice contains the number and date of the “initial” one, its numerical indicators and new data (clause 7 of the Rules for filling out the invoice No. 1137 dated December 26, 2011). For this purpose, an additional line 1a “Correction” is provided, in which you need to indicate the number and date of the correction. Based on them, the difference (positive or negative value) is determined, which will be entered in the sales book or purchase book of the seller and buyer.

Not all errors in the invoice require the preparation of a new corrected copy . If the error is not a basis for refusing a VAT refund (does not prevent the tax authorities from identifying the buyer (seller), determining the name of the goods (works, services), cost, tax rate, or tax amount), it is not necessary to prepare a corrected invoice (Resolution of the Government of the Russian Federation dated December 26, 2011 No. 1137).

Errors in the adjustment invoice will only be a reason to check the original document. The error in both documents will have to be corrected using two corrected invoices - for the original invoice and the corrective invoice.