general characteristics

The money that the employer transfers for the employees of his organization gives citizens the opportunity to count on receiving several types of payments in the future:

- Pension provision.

- Disability benefits.

- Other benefits of a social nature.

At the moment, all financial resources that are transferred in this way to the country’s budget are immediately used to provide disabled citizens with all the social benefits they are entitled to.

Reducing the cost of taxes on insurance premiums

In general, this entire process is regulated in tax legislation.

Changing tariffs

Let's take a closer look.

Cancellation of benefits

The preferential rates for social contributions were abolished for the two largest categories of payers for whom it was most convenient to enjoy the privileges:

- Entrepreneurs.

- Companies under special regimes.

This category of beneficiaries previously had the opportunity to pay only contributions to the Pension Fund in the amount of 20% of the wages of their employees.

A large number of entrepreneurs and organizations fell under the terms of the benefit, thanks to which they had the opportunity to officially employ people for themselves, and at the same time save their money without making much effort.

So, if these organizations had officially employed persons, then the company could save up to 10% of the payroll precisely by making such contributions.

Attention! This benefit existed until 2021, when it was refused to be extended. Now this preferential category of payers does not enjoy any benefits and is obliged to pay the full amount of contributions for their employees - 30%.

Who doesn't have to pay fees?

Who is entitled to benefit?

Since 2021, new benefits have been introduced into the legislation, which will be valid until 2024. All categories except those listed above can take advantage of the benefits, although interest rates will also increase for them.

To take advantage of the benefits, the organization must meet a number of conditions:

- Have sufficient turnover.

- Business should be considered rare.

- The organization must confirm its status.

For each type of activity, the legislation provides for its own requirements. For example, this may be a requirement that the organization be in a special reserve, have a sufficient number of employees, or obtain a document indicating the existence of the status.

Reduced rates

| Type of payers | Rates, % | ||

| Pension insurance | Social insurance | Health insurance | |

Russian organizations that work in the field of information technology and are engaged in:

| 8,0 | 2,0 | 4,0 |

| Organizations and entrepreneurs with payments and remunerations for the performance of labor duties to crew members of ships registered in the Russian International Register of Ships (except for ships for storage and transshipment of oil and petroleum products in Russian seaports) | |||

Non-profit organizations that use the simplified approach and operate in the field of:

Exception: state and municipal institutions | 20,0 | ||

| Charitable organizations simplified | |||

| Organizations participating in the Skolkovo project | 14,0 | ||

| Organizations and individual entrepreneurs that have received the status of participant in a free economic zone in accordance with Federal Law No. 377-FZ dated November 29, 2014 “On the development of the Republic of Crimea and the federal city of Sevastopol and the free economic zone in the territories of the Republic of Crimea and the federal city of Sevastopol” | 6,0 | 1,5 | 0,1 |

| Commercial organizations and entrepreneurs with the status of residents of the territory of rapid socio-economic development in accordance with Law dated December 29, 2014 No. 473-FZ | |||

| Commercial organizations and entrepreneurs with the status of residents of the free port of Vladivostok in accordance with the Law of July 13, 2015 No. 212-FZ | |||

| Organizations with resident status of a special economic zone in the Kaliningrad region in accordance with the Law of January 10, 2006 No. -FZ | |||

| Russian organizations that produce and sell animated audiovisual products they produce | 8,0 | 2,0 | 4,0 |

Federal Law of November 29, 2014 N 377-FZ “On the development of the Republic of Crimea and the federal city of Sevastopol and the free economic zone in the territories of the Republic of Crimea and the federal city of Sevastopol”

Federal Law of December 29, 2014 N 473-FZ “On territories of rapid socio-economic development in the Russian Federation”

Federal Law of July 13, 2015 N 212-FZ “On the Free Port of Vladivostok”

Federal Law of January 10, 2006 N 16-FZ “On the Special Economic Zone in the Kaliningrad Region and on Amendments to Certain Legislative Acts of the Russian Federation”

Federal Tax Service control over reduced insurance premium rates in 2021

Reduced rates for insurance premiums for a large category of entrepreneurs were canceled from January 1, 2021. Benefits were used by:

- applying a simplified taxation system, the main types of economic activities of which are named in subparagraph 5 of paragraph 1 of Article 427 of the Code;

- individual entrepreneurs using the patent tax system;

- taxpayers of the single tax on imputed income are pharmacy organizations (individual entrepreneurs) with a license for pharmaceutical activities.

At the same time, in 2021, the Federal Tax Service will administer insurance premiums, as in 2019. Thus, a single calculation of insurance premiums for the current year will need to be submitted to the Federal Tax Service.

After receiving calculations for insurance premiums, tax officials will conduct desk audits of the calculations provided to them. Thus, based on paragraph 1, Article 88 of the Tax Code of the Russian Federation, tax inspectors will need to check the validity of the application of reduced insurance premium rates by entrepreneurs.

Reduced insurance premium rates in 2021 are indicated in Section 1 of the DAM report in Appendix 5 - Calculation of compliance with the conditions for applying the reduced insurance premium rate by payers specified in subparagraph 3 of paragraph 1 of Article 427 of the Tax Code of the Russian Federation to section 1.

Let us recall that the reduced rates of insurance premiums until 2021 were indicated in Section 1 (Appendices 5–8) of the calculation of insurance premiums. For example, Appendix 6 of Section 1 of the calculation should have been completed by:

- Individual entrepreneurs who combine the Simplified and Patent tax systems;

- organizations (entrepreneurs) on the simplified tax system that work in the production or social spheres (subclause 5, clause 1, subclause 3, clause 2, article 427 of the Tax Code of the Russian Federation) have the right to apply reduced tariffs for insurance premiums.

From 2021, due to the abolition of reduced insurance premium rates for the above categories, Appendix 6 was removed from the DAM. And for entrepreneurs who lost the right to a reduced tariff, the tariff payer code was changed. Now, instead of code 12, such payers indicate code 02.

The tax office, conducting a desk audit of the provided calculations, may require the following from an individual entrepreneur or organization:

1. Provide documents. 2. Provide written and oral explanations about identified errors or inconsistencies or eliminate them.

Contribution rates for employers

Until 2021, insurance premium rates were considered temporary, since they were planned to increase from 2021. However, this decision was later revised, and all rates were transferred to the category of constant, that is, their increase is not planned.

- The rate for pension insurance is 22% - the maximum value and 10 percent if it is exceeded.

- Insurance premiums for temporary disability - 2.9%.

- Health insurance is 5.1%.

- Personal injury premiums range from 0.2% to 8.5%.

Distribution of insurance premiums

Reduced insurance premiums due to coronavirus

Law No. 102-FZ established for representatives of small and medium-sized businesses a two-fold (from 30 to 15%) permanent reduction in the total tariff of insurance premiums from payments above the minimum wage.

Thus, the new amounts of insurance premiums for SMEs are as follows:

- for mandatory pension insurance – 22.0% (if the payment is less than the minimum wage), within the base and above – 10.0% ;

- in cases of temporary disability and maternity – 0%;

- for compulsory medical insurance – 5.0% (until 04/01/2020 – 5.1%).

Thus, as the President promised in his address to the nation on March 25, 2020, the amount of insurance premiums has been reduced by half - from 30 to 15% (10% in the Pension Fund of the Russian Federation + 5% for compulsory medical insurance).

Further in the table we will explain in more detail the changes to the Law of December 15, 2001 No. 167-FZ “On Compulsory Pension Insurance in the Russian Federation” concerning the reduction of insurance premiums for small and medium-sized businesses.

| IF THE PAYMENT IS WITHIN THE LIMITED BASE FOR CALCULATING INSURANCE PREMIUMS | IF THE PAYMENT IS EXCEEDING THE LIMIT BASE FOR CALCULATING INSURANCE PREMIUMS |

| 22.0% – monthly payment does not exceed the minimum wage (it is believed that this rate should stimulate an increase in small salaries) 10.0% – for payments above the minimum wage | 10.0% – for payments less than the minimum wage 10.0% – for payments more than the minimum wage |

Small and medium-sized businesses are also exempt from paying insurance contributions to the Social Insurance Fund for compulsory social insurance in case of temporary disability and in connection with maternity.

These reduced tariffs apply to income accrued from April 1, 2021, and are valid indefinitely (in Law No. 102-FZ, as amended in the Tax Code of the Russian Federation, two articles establish reduced tariffs: one from 04/01/2020, the other from 01/01/2021). At the same time, payments for March 2021 must be calculated and paid as usual.

Moreover, in the period from April 1, 2021 to December 31, 2021, the rate of contributions for compulsory pension insurance within the framework of the maximum base value is not 22.0%, but 10.0%.

REFERENCE

Until April 1, 2020, the employer had to pay insurance premiums for the employee at a rate of 30% of the salary. Of them:

- 22% – in the Pension Fund of Russia;

- 5.1% – in the Federal Compulsory Medical Insurance Fund;

- 2.9% - in the Social Insurance Fund.

If the salary is more than 1.29 million rubles. from the beginning of the year, the pension contribution rate is reduced to 10%. Social insurance contributions are zeroed out when the salary is over RUB 990,000. per year cumulative total.

Conditions under which preferential rates apply

Individual business entities have the right to expect to receive certain concessions when determining the amount of payments transferred to the funds.

In particular, companies that are engaged in activities aimed at introducing the results of intellectual work and their partners have the right to take advantage of such privileges. The amount of preferential rates for such organizations in 2021 is:

- Pension insurance - 20%.

- Disability contributions are 2.9% for foreign employees and 1.8% for stateless persons.

- Medical insurance - 5.1%.

In order for a company to benefit from preferential tariffs, it must fulfill several conditions:

- Carrying out development and design activities.

- All activities should be carried out in a simplified manner.

- The register must contain information about the creation of this company.

Companies and individual entrepreneurs who are engaged in:

- Technology and innovation activities.

- Tourist and recreational activities.

Preferential rates for this category of organizations are similar.

Resident organizations that develop information systems and software have the right to use other preferential tariff rates:

- 8% of wages is transferred to the Pension Fund and Social Insurance Fund.

- Health insurance premiums are 4%.

But you can take advantage of such benefits only if a number of conditions are met:

- There is a document confirming accreditation.

- The income received from the main activities of the company is 90% for the reporting period.

- The average number of employees is more than 7 people.

Legal entities and entrepreneurs who have one of the following statuses can take advantage of benefits when paying contributions:

- Member of the free economic zone.

- Resident of a zone with advanced socio-economic development.

- Resident of the port of Vladivostok.

The lowest contribution rates apply to this category of payers:

- Pension insurance is only 6%.

- In case of temporary disability - 1.5%.

- For health insurance - 0.1%.

Benefits are provided for ten years from the date of registration of the corresponding status.

Background

Initially clause 3.4. Federal Law No. 212-FZ of July 24, 2009 “On insurance contributions to the Pension Fund of the Russian Federation, the Social Insurance Fund of the Russian Federation, the Federal Compulsory Medical Insurance Fund” (hereinafter referred to as Federal Law No. 212) established that during 2012–2018 years for payers of insurance premiums (in our case, organizations whose main activity is the management of real estate, reduced rates of insurance premiums are applied, namely: to the Pension Fund of the Russian Federation - 20%, the Social Insurance Fund of the Russian Federation and the Federal Compulsory Medical Insurance Fund - 0 .

However, Federal Law No. 212 lost force as of January 1, 2021 due to the adoption of the new Federal Law of July 3, 2021 No. 250-FZ; all issues related to the regulation of insurance premiums moved to Chapter 34 of the Tax Code of the Russian Federation.

In accordance with paragraphs. 3 clause 1.1 art. 427 of the Tax Code of the Russian Federation for payers whose main activity is the management of real estate for a fee or on a contractual basis, during 2017–2018 the rates of insurance contributions for compulsory pension insurance are set at 20%, for compulsory social insurance in case of temporary disability and in connection with maternity, compulsory health insurance - 0%.

Thus, from 2012 to 2021 (Federal Law No. 212) and from 2021 to 2018 (Tax Code of the Russian Federation), in relation to organizations that are on the simplified taxation system (hereinafter referred to as the simplified taxation system) and managing real estate, reduced insurance premium rates. An extension of reduced insurance premiums for such organizations for 2021 is not provided.

In 2021, reduced tariffs will remain for several more years for the following categories of payers (clauses 7 and 8, clause 1, article 427 of the Tax Code of the Russian Federation):

- socially oriented non-profit organizations (hereinafter referred to as NPOs) that apply a simplified taxation system (hereinafter referred to as the simplified taxation system) and carry out activities in the field of social services for citizens, scientific research and development, education, healthcare, culture and art (activities of theaters, libraries, museums and archives) and mass sports (with the exception of professional);

- charitable organizations using the simplified tax system.

Payments not subject to contributions

First of all, income that is not subject to insurance premiums includes amounts that are not subject to taxation.

For example, payments and rewards that were received by a person under a gift, lease, loan and sale agreement. Contributions do not accrue for dividends either, since taxes are not paid on them.

The legislation also lists several other payments for which insurance premiums are not calculated:

- Benefits for temporary disability, BIR, child care.

- Daily payments.

- Material assistance, the amount of which does not exceed 4,000 rubles per employee.

Who applies the benefits?

By law, the person who pays the premiums is the insurer for all of his employees. Among such payers are:

- Organizations where employees work under an employment contract or a GPC agreement.

- Individual entrepreneur.

- Individuals, if they are sources of income for other citizens, even if they do not have the status of an entrepreneur.

- Individuals engaged in the practice of law or providing notarial services.

Attention! Individual entrepreneurs, lawyers and notaries must additionally pay insurance premiums for themselves.

Receiving benefits

The moment of accrual of a person’s income and all payments due to him is determined by the date of such accrual.

Most often this is the last day of the billing period. Accordingly, until this moment the organization does not have any arrears in contributions. But not everyone can take advantage of such conditions. For example, individual entrepreneurs, lawyers and notaries are required to pay contributions from the date of their insurance. That is, the absence of hired workers on the staff cannot be a reason for non-payment of contributions, since this category of citizens is obliged to contribute funds for themselves.

All payers independently determine the size of their contribution rates. The main indicators take into account the Tax Code article and several conditions:

- The period of time during which the payer carries out its activities.

- Number of employed workers.

- Revenue volumes

- Type of preferential activity.

Attention! If an organization uses two taxation systems at once, then all preferential income should be taken into account separately. If this condition is not met, the payer loses his right to receive benefits.

Additional conditions for receiving benefits

The benefit is provided to enterprises engaged in social and industrial activities (Article 427 of the Tax Code of the Russian Federation) in the amount of more than 70% of the total. To be able to apply reduced rates, the specified OKVED must be declared by the enterprise in the constituent documents and register as the main one. If the preferential type of activity is not recognized as the main one in the documents of the enterprise, the organization or individual entrepreneur using the simplified tax system will lose the right to reduced rates.

Let's name the main requirements for receiving benefits: (click to expand)

| Required condition for the benefit | Criterion |

| Type of activity carried out by the enterprise | Established for the main type of OKVED and coincides with the list of paragraph 5 of paragraph 1 of Art. 427 Tax Code of the Russian Federation. |

| Revenue from the main activity | 70% of total revenues |

| Enterprise's marginal income | The annual income of the enterprise should not exceed 79 million rubles |

To determine the indicator of priority receipts for the main type of activity, it is allowed to add up revenues for one OKVED class. In the absence of revenue or other income, there is no way to determine the right to a reduced tariff. Companies using the simplified tax system determine income without taking into account the company's expenses.

To apply the benefit, enterprises do not have to submit an application and supporting documents. Taxpayers using the simplified tax system fill out Appendix 6 of Section 1 of the calculation of contributions. When filling out the data, it is necessary to ensure compliance with the information on the OKVED title and the income indicated in the application for the main type. In the calculation, you must correctly indicate the payer code depending on the benefit applied. If the right to a reduced tariff is lost and adjustment calculations with additional payment are submitted, Appendix 6 is not submitted.

Insurance contributions from the self-employed population

Self-employed citizens are individuals who are engaged in private practice and individual entrepreneurs who are required to make contributions to the fund, regardless of whether they have employees or whether they have received any income.

For this category of payers, several types of tariffs are provided:

- With incomes of less than 300,000 rubles, you will have to pay for pension insurance according to the formula 12 months * equal to the minimum wage * 26%.

- If a person’s income exceeds 300,000 rubles, then in addition to the basic payment for pension insurance, the payer must transfer 1% of the amount exceeding the minimum threshold.

- Contributions for compulsory medical insurance are fixed and do not depend on the amount of income received: 12 months * by the minimum wage * by 5.1%.

The law provides for several situations in which a person may be exempt from paying contributions:

- Completion of emergency service.

- BIR leave.

- Holiday to care for the child.

Checking the policyholder's right to a reduced insurance premium rate

If the right to reduced rates for insurance premiums depends on what type of business the insurance company is engaged in, then the inspection has the right to apply an expanded “package” of control measures, including inspection of the premises.

Preferential tariff

The Tax Code of the Russian Federation provides for reduced tariffs for certain payers of insurance premiums. What does a preferential tariff give to payers? Firstly, the amount of premiums for all types of insurance can be reduced down to 0.

Secondly, companies and individual entrepreneurs that apply reduced insurance premium rates do not pay pension contributions on payments exceeding the maximum base.

Also, contributions for compulsory social insurance - no one charges them for payments above the maximum base.

There is no limit on the base for contributions to compulsory health insurance. Therefore, medical premiums are charged on all income subject to insurance premiums both by insurers applying general tariffs and by insurers with benefits if their tariffs set a rate other than 0.

Depends on the type of activity

The Ministry of Finance in a commented letter explained that in the case where the right to a reduced rate of insurance premiums depends on the type of activity, the tax authorities have the right to in-depth check the insurer company and its accounting and reporting data. They can study the company’s contracts with contractors, as well as inspect the premises and even become familiar with the technological processes.

This letter talks about some simplified workers (without specifying the type of activity) who conducted business in areas provided for in a special list from the Tax Code of the Russian Federation and paid contributions at reduced rates until 2021.

Among the simplifications, starting from 2021, only non-profit organizations, but also those engaged in certain types of activities, have the right to a preferential tariff.

Thus, in a letter dated March 7, 2019, the Federal Tax Service warned that when conducting a desk tax audit of the calculation of insurance premiums, the inspectorate may request information and documents confirming the validity of the application of reduced insurance premium rates. In addition to the constituent documents (subclause 7 of clause 1 of Article 427 of the Tax Code of the Russian Federation), non-profit organizations using the simplified tax system can confirm the benefit with the following documents:

- application for transition to the simplified tax system (form 26.2-1);

- a copy of the tax return according to the simplified tax system with the tax office’s mark of acceptance;

- a copy of the income and expense ledger;

- breakdown of income by type of income (certificate of the organization, certificate confirming the main type of economic activity).

Article 427 of the Tax Code of the Russian Federation establishes a list of beneficiaries who have the right to apply reduced rates of insurance contributions. There are several groups of them. In addition to simplified NPOs, paragraph 1 of Article 427 of the Tax Code of the Russian Federation establishes a list of other contribution payers who are entitled to reduced tariffs. Among them are those that receive preferential treatment depending on the type of activity.

For each group of beneficiaries, criteria have been established that entitle them to a reduced rate of insurance premiums.

Preferential tariff for simplified tax system

Since the letter deals with simplifications, we’ll start with them.

During 2021 - 2021, simplified firms engaged in the production and social spheres (subclause 5, clause 1, article 427 of the Tax Code of the Russian Federation) paid insurance premiums only for compulsory pension insurance at a rate of 20% (subclause 3, clause 2 Article 427 of the Tax Code of the Russian Federation).

The category of beneficiaries included, in particular, companies (subclause 5, clause 1, article 427 of the Tax Code of the Russian Federation):

- producing food products, textiles, footwear, clothing, furniture, paper, vehicles and equipment;

- carrying out scientific research and development;

- engaged in the repair of household products and vehicles;

- conducting activities in the field of education, healthcare, construction, provision of social services, transport and communications;

- retail traders of pharmaceutical, medical and orthopedic products;

- producing furniture, musical instruments;

- manufacturing computers, electronic and optical products;

- producing films, videos and television programs;

- producing sporting goods, games and toys, etc.

From January 1, 2021, they all switched to a common tariff of 30%.

Preferential tariffs have been preserved for 2021 - 2024 only for non-profit and charitable simplified taxation organizations specified in subparagraphs 7 and 8 of paragraph 1 of Article 427 of the Tax Code of the Russian Federation, respectively.

Such simplifications must be registered in the Unified State Register of Legal Entities on the basis of information received by the tax office from the Ministry of Justice. They pay insurance premiums of only 20% for compulsory pension insurance.

The conditions for applying the reduced tariff are standard. The activities of NPOs in socially oriented areas should be the main one. That is, the share of income from services provided must be at least 70% of total income. And the total annual income of the “simplified” person should not exceed 79 million rubles (subclause 3, clause 2, article 427 of the Tax Code of the Russian Federation)

In addition, income must be from the main types of activity (subclauses 7, 8, clause 1, article 427 of the Tax Code of the Russian Federation). These include:

- scientific research and development (OKVED code 73);

- education (OKVED code 80);

- healthcare and provision of social services (OKVED code 85);

- activities of sports facilities (OKVED code 92.61);

- other activities in the field of sports (OKVED code 92.62);

- activities of libraries, archives, club-type institutions (except for the activities of clubs) (OKVED code 92.51);

- activities of museums and protection of historical sites and buildings (OKVED code 92.52);

- activities of botanical gardens, zoos and nature reserves (OKVED code 92.53).

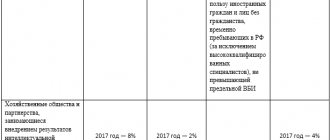

Preferential rates of insurance premiums for the information technology sector

For organizations operating in the field of information technology, from 2021 to 2023, the following insurance premium rates are also established:

- for compulsory pension insurance - 8%;

- for compulsory social insurance in case of temporary disability and in connection with maternity - 2%;

- for compulsory health insurance - 4%.

The conditions for the application of benefits to organizations working in the field of information technology are set out in paragraph 5 of Article 427 of the Tax Code of the Russian Federation.

The first criterion is the share of income from:

- implementation of copies of computer programs, databases;

- services for the development and modification of these programs and databases;

- services for installation and maintenance of programs and databases.

Based on the results of nine months of the year preceding the year of the organization’s transition to paying insurance premiums at reduced rates, the share of income from these types of activities must be at least 90 percent of the total income of the organization for this period.

The second criterion is the average number of employees for the reporting (calculation) period, which must be at least 7 people.

The third criterion is the presence of a document on state accreditation.

If the parent IT company has the right to apply reduced rates of insurance premiums, then its branch can also take advantage of the benefit (letter of the Federal Tax Service of Russia dated October 1, 2018 No. BS-4-11 / [email protected] ).

Preferential tariffs for film industry enterprises

Finally, for 2018-2023, a reduced rate of insurance premiums has been established for Russian film industry organizations for the following types of activities:

- production and sale of animated audiovisual products produced by them (including transfer of exclusive rights, granting rights of use);

- provision of services (performance of work) for the creation of the specified products.

This is provided for by Federal Law No. 95-FZ dated April 23, 2018.

For Russian film industry enterprises, insurance premium rates are:

- for compulsory pension insurance – 8%;

- for compulsory social insurance in case of temporary disability and in connection with maternity – 2%;

- for compulsory health insurance – 4%.

The conditions for the application of reduced tariffs have also been determined.

By share of income: the share of income from these types of activities, as well as from budgetary funds for production, promotion, rental and display of animated audiovisual products must be at least 90% of the total income of the organization for the period.

The average number of employees must be at least 7 people.

You also need a document confirming that the payer is in the register of organizations producing animated audiovisual products and (or) providing services (performing work) for its creation. This register is maintained by the Ministry of Culture.

Responsibility for individual entrepreneurs

If an individual entrepreneur does not make payments within the time limits specified by law or does not transfer them in full, he may be held liable in the form of a fine.

The penalty is 20% of the amount not transferred to the funds. If such non-payment was made intentionally, the fine increases to 40%. Most often, territorial authorities apply only penalties to such a violator, but only if the payment was made within a short period of time and the amount of the debt turned out to be small.

Penalties are accrued regardless of what exact penalties were applied to the debtor. The accrual is made in the amount of 1/300 of the refinancing rate.